Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

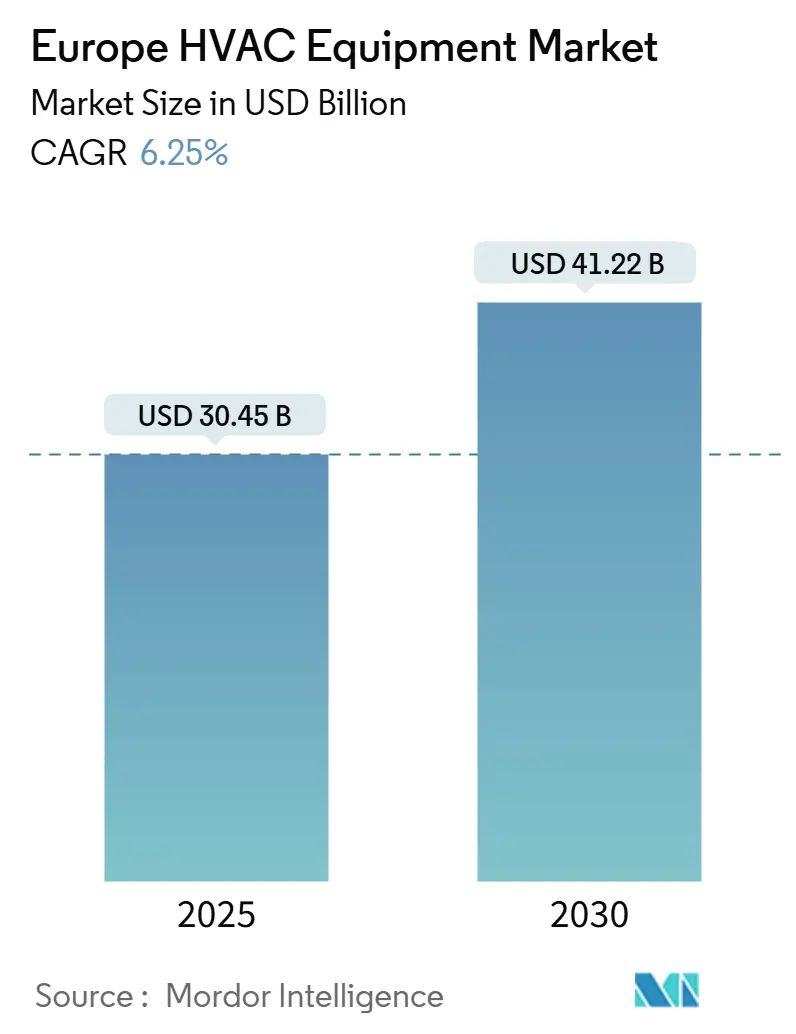

| Market Size (2025) | USD 30.45 Billion |

| Market Size (2030) | USD 41.22 Billion |

| Growth Rate (2025 - 2030) | 6.25% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe HVAC Equipment Market Analysis by Mordor Intelligence

The European HVAC equipment market size reached USD 30.45 billion in 2025 and is forecast to attain USD 41.22 billion by 2030, advancing at a 6.25% CAGR. This growth positions the region as a critical arena for vendors contending with stricter decarbonization mandates and evolving energy policies. Mounting heat-pump incentives under the EU Green Deal, intensifying summer heatwaves that lift cooling demand, and accelerated replacement of aging boilers collectively fuel the adoption of electrified systems. Meanwhile, supply-chain inflation and high upfront capital requirements temper near-term momentum but have not derailed the long-term trajectory of electrification. Competitive pressure has risen as conglomerates pursue billion-dollar acquisitions to scale production capacity and consolidate fragmented installer networks, aiming to meet the bloc’s 60 million heat-pump target by 2030.

Key Report Takeaways

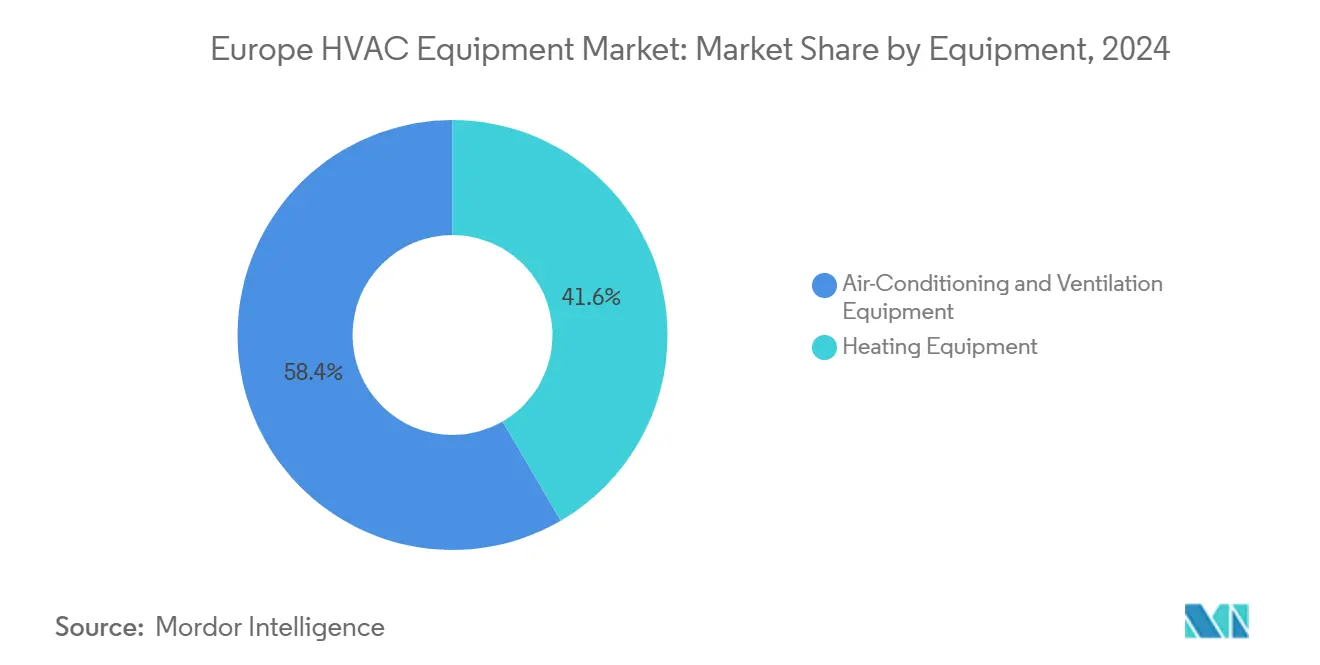

- By equipment type, air conditioning and ventilation led with a 58.4% share of the European HVAC equipment market in 2024; ground-source heat pumps are projected to expand at a 10.2% CAGR through 2030.

- By end-user industry, the residential segment held 47.3% of the European HVAC equipment market size in 2024, while institutional and public buildings recorded the strongest 10.6% CAGR through 2030.

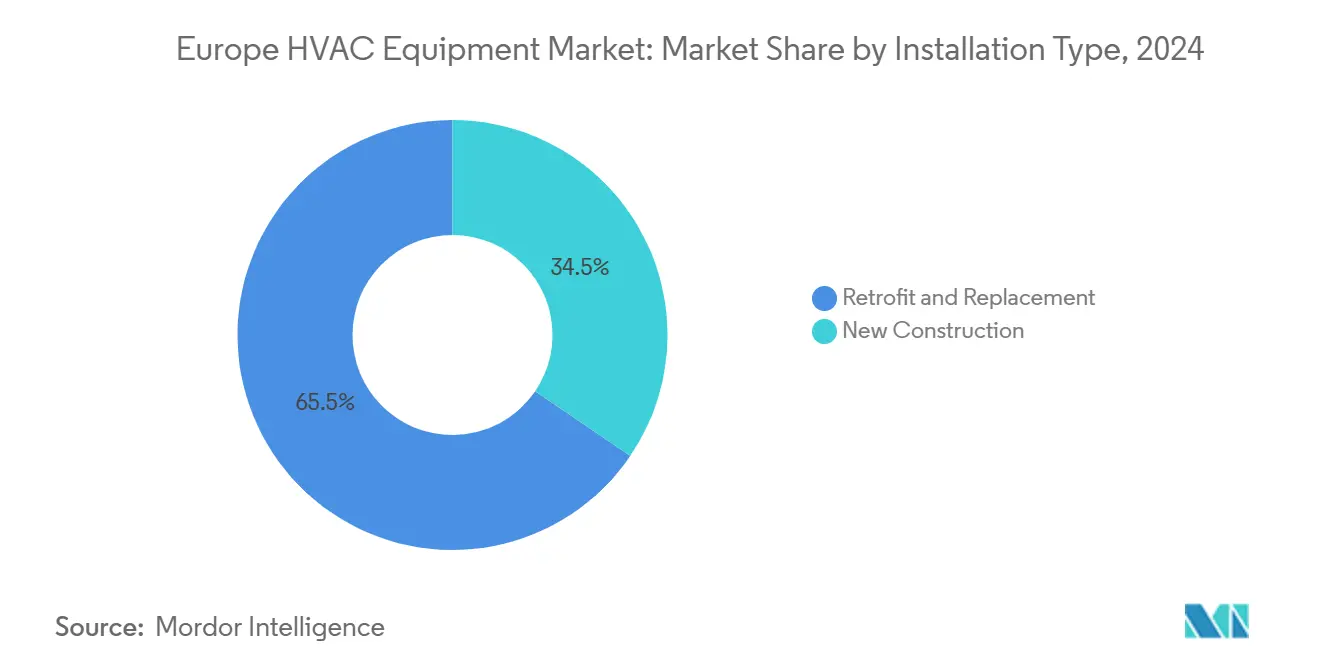

- By installation type, retrofit and replacement accounted for 65.5% of Europe's HVAC equipment market activity in 2024; new construction is increasing at a 7.5% CAGR.

- By distribution channel, OEM-installer networks commanded 62.4% share of the European HVAC equipment market size in 2024; direct-to-consumer and e-commerce are growing at a 12.1% CAGR.

- By country, Germany led the European HVAC equipment market with a 26.1% share in 2024; the Netherlands is the fastest-growing national market, growing at a 9.7% CAGR.

Europe HVAC Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green-Deal efficiency mandates and heat-pump subsidies | +1.1% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Accelerating replacement of ageing boiler stock | +0.8% | Northern Europe, UK, Germany, Netherlands | Long term (≥ 4 years) |

| Intensifying summer heatwaves boosting residential AC uptake | +0.7% | Southern Europe, expanding northward | Short term (≤ 2 years) |

| Rapid electrification of commercial HVAC retrofits | +0.6% | Urban centers across EU, led by Germany, France | Medium term (2-4 years) |

| Propane (R290) heat-pump launches post-F-Gas revision | +0.5% | EU-wide, manufacturing hubs in Germany, Italy | Medium term (2-4 years) |

| Scale-up of installer-training programs unlocking latent demand | +0.4% | Skills-shortage regions: Germany, Netherlands, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

EU Green Deal efficiency mandates drive market transformation

Mandatory minimum-efficiency standards and EUR 56 billion (USD 65.57 billion) in heat-pump incentives rolled out across the bloc in 2024 reshaped equipment demand, pushing heat-pump installations in Germany up 60% year-over-year to 43,000 units in Q1 2025.[1]Woninglabel, “Verkoop van warmtepompen begin 2025 stijgt flink,” woninglabel.nl Subsidies favored air-to-water models whose sales jumped from 22,000 to nearly 38,000 units, underscoring policymakers’ bias toward hydronic integration. Although Dutch ISDE rebates were reduced in 2025, the Netherlands still aims to install heat pumps in 20% of homes by 2030, sustaining a 9.7% CAGR for the European HVAC equipment market. Manufacturers have responded with natural-refrigerant designs and financing schemes that shield buyers from upfront costs.

Aging boiler replacement accelerates market expansion

Roughly 130 million legacy boilers across Europe became ripe for swap-out as gas prices climbed in 2024 and carbon penalties tightened. OEMs accelerated M&A to secure installer capacity, highlighted by Daikin’s purchase of Sweden-based Kylslaget AB in August 2024. Retrofit-oriented heat-pumps engineered for compatibility with existing hydronic circuits shortened installation times and boosted contractor productivity, lifting replacement demand even in markets with modest new-build volumes.

Summer heatwave intensity reshapes residential AC demand

The scorching 2024 summer season drove residential AC sales beyond Southern Europe into Germany, the Netherlands, and Scandinavia, prompting brands to tailor their product lines for mixed-climate territories. Dual-mode heat pumps gained favor because they handle both peak-season cooling and winter heating, improving annual utilization and reinforcing the 58.4% dominance of air-conditioning and ventilation equipment in the European HVAC equipment market.

Commercial HVAC electrification gains momentum

Institutional retrofits, notably in hospitals, demonstrated 43.6% energy savings and <1.3-year paybacks after switching to integrated heat-pump systems. Corporate ESG targets amplified adoption, giving OEMs clearer build-out pipelines than the price-sensitive residential space. This driver added predictable volume for large-capacity chillers and VRF platforms, underpinning the 10.6% CAGR outlook for institutional buildings within the European HVAC equipment market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex versus gas boilers | -0.9% | Price-sensitive markets: Eastern Europe, rural areas | Short term (≤ 2 years) |

| Supply-chain and commodity-price inflation | -0.7% | Manufacturing hubs: Germany, Italy, supply chains globally | Medium term (2-4 years) |

| Skilled-labour bottlenecks delaying installations | -0.5% | High-demand regions: Germany, Netherlands, Nordic countries | Long term (≥ 4 years) |

| OEM re-tooling risk amid refrigerant transition uncertainty | -0.4% | Manufacturing centers with legacy R-410A production | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront capital expenditure constrains market penetration

Heat-pump systems still cost 3-5 times more than a boiler swap, deterring households in Eastern Europe and rural districts despite subsidies. Complex financing packages introduced by OEMs raise administrative hurdles and slow sales cycles. Where disposable income is lower, the European HVAC equipment market expands largely through publicly funded social-housing programs rather than private purchases.

Supply-chain inflation pressures profitability

Copper, steel, and semiconductors remained elevated through 2024, prompting Danfoss to raise prices and cite weaker demand in its H1 2024 results. To offset volatility, manufacturers diversified sourcing but incurred extra logistics costs that squeezed margins and forced leaner inventories, slightly trimming the medium-term growth rate for the European HVAC equipment market.

Segment Analysis

By Equipment: Ground-source systems drive premium growth

Ground-source heat pumps recorded the fastest 10.2% CAGR through 2030, even though air-conditioning and ventilation maintained the largest 58.4% share within the European HVAC equipment market. Institutional buyers favored geothermal solutions that deliver higher seasonal efficiencies and longer lifespans, justifying the drilling expenses that residential customers often avoid. As Nordic geology supports closed-loop borefields, installers are reporting an increase in multi-megawatt campus-scale projects.

In parallel, air-to-water heat pumps remained dominant in heating retrofits, leveraging existing radiators and earning policy preference due to their simplification of the fossil-fuel phase-out. Daikin’s R-290 modular platform, unveiled in March 2025, exemplified the natural-refrigerant progression that meets F-Gas regulations while enhancing part-load efficiency.[2]Ref Industry, “Daikin Unveils Modular Air-to-Water Heat Pump with R-290 Refrigerant,” refindustry.com Hybrid boiler-pump kits gained traction as interim solutions in colder interiors. Collectively, these innovations sustain the European HVAC equipment market’s technology shift from gas-fired packages to electrified variants without sacrificing performance.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Institutional buildings lead growth trajectory

Residential users contributed 47.3% of 2024 sales, while public and institutional estates, schools, and hospitals are projected to post the highest 10.6% CAGR, increasing their share of the European HVAC equipment market size by 2030. Government decarbonization budgets funded large-scale retrofits that pair heat pumps with demand-controlled ventilation.

Institutional project cycles are longer but guarantee volume, encouraging OEMs to offer energy-as-a-service contracts that bundle equipment, maintenance, and monitoring. Commercial offices continue to experience steady demand from ESG-driven landlords, while industrial sites explore process heat recovery integrations. These varied user needs prompt suppliers to expand their portfolios and develop software analytics capabilities, further driving competitive differentiation in the European HVAC equipment market.

By Installation Type: Retrofit market dominates activity

Retrofit jobs accounted for 65.5% of 2024 revenue, underscoring the vast aging building stock that characterizes European cities. Such projects favor modular indoor units and flexible refrigerant pipes that navigate tight shafts, thereby propelling innovation in plug-and-play kits. Installers developed phased execution models to keep premises operational, sustaining Europe's HVAC equipment market growth even when new-build permits slow.

New construction, expanding at a 7.5% CAGR, benefits from net-zero building codes that standardize heat-pump specifications at the design stage. Prefabricated mechanical rooms simplify commissioning and reduce on-site labor, but volume remains tempered by mature real-estate cycles in Western Europe. Retrofit proficiency, therefore, remains the critical differentiator for contractors competing in the European HVAC equipment market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Digital transformation accelerates direct sales

OEM-installer alliances accounted for 62.4% of turnover in 2024, while direct-to-consumer portals experienced a 12.1% CAGR, as households increasingly adopted online quotation tools and simplified split-system kits. Electric Air’s web-based configurator significantly reduced sales lead times, illustrating how digital engagement converts latent interest into orders.

Wholesale distributors still anchor rural markets, where local stock and credit terms are crucial. OEMs now deploy omni-channel strategies, balancing e-commerce reach with installer loyalty programs that protect technical support revenues. Managing this channel blend is pivotal to capturing the European HVAC equipment market demand while avoiding margin erosion.

Geography Analysis

Germany retained top status with a 26.1% share amid stable consumer confidence and deep industrial capabilities that support domestic manufacturing. However, labor shortages slowed installation throughput, prompting OEMs such as Daikin to augment service capacity via the Kylslaget acquisition in 2024.[3]Daikin Europe N.V., “Daikin acquires Swedish heat pump service company Kylslaget,” daikin.eu

The Dutch market’s double-digit growth reflected synchronized policy execution: simplified permitting, nationwide installer upskilling, and low-interest financing that lowered payback thresholds. Heat-pump unit sales rose 60% in Q1 2025, signalling demand durability despite subsidy adjustments.

Elsewhere, Nordic countries enjoy high per-capita deployment, shifting focus to refrigerant upgrades and large-capacity communal systems. Southern Europe’s hotter summers lifted AC penetration rates, while Eastern Europe remained price-constrained, relying on EU cohesion funds to bridge capex gaps. Together, these patterns create a patchwork of opportunity pockets that sustain the European HVAC equipment market’s 6.25% compound annual growth rate.

Competitive Landscape

The market shifted from moderate fragmentation to consolidation as multinationals sought to achieve scale in order to meet the EU’s 60-million-unit target. Bosch’s USD 8.1 billion takeover of Johnson Controls-Hitachi in 2024 nearly doubled its HVAC revenue, signalling aggressive positioning. Samsung’s EUR 1.5 billion (USD 1.7 billion) purchase of FläktGroup in May 2025 expanded its European data-center cooling foothold.

Strategic deals also targeted installer networks, Daikin added, with the Danish firm BKF Klima and Swedish Kylslaget, highlighting the service bottleneck as a key battleground. Disruptors like Aira have pledged EUR 300 million for a Polish factory capable of producing 500,000 heat pumps annually, combining equipment with financing bundles to attract cost-conscious homeowners.[4]Aira, “Aira to invest €300 million and manufacture up to 500,000 heat pumps a year in Poland,” airahome.com

Technology differentiation centered on natural refrigerants and smart connectivity. Daikin’s R-32 rooftop units and R-290 heat pumps, Lennox-Samsung smart mini-splits, and Danfoss-Google AI drives illustrate the pivot toward digital energy management. Competitive intensity, therefore, hinges on R&D velocity, supply-chain resilience, and omnichannel service prowess, reshaping power balances within the European HVAC equipment market.

Europe HVAC Equipment Industry Leaders

-

Daikin Industries, Ltd.

-

Robert Bosch GmbH

-

Mitsubishi Electric Europe BV

-

Vaillant Group

-

Danfoss A/S

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Daikin Applied introduced the Trailblazer Heat Pump Chiller, delivering up to 300% efficiency.

- May 2025: Samsung Electronics acquired FläktGroup for EUR 1.5 billion (USD 1.7 billion).

- April 2025: Daikin Applied added R-32 air-source heat pumps to its Premier Rooftop line.

- March 2025: Daikin unveiled a modular R-290 air-to-water heat pump.

Europe HVAC Equipment Market Report Scope

The European HVAC Equipment Market is segmented by Equipment, which includes Air-Conditioning/Ventilation Equipment (Single-Split and Multi-Split Units, Variable Refrigerant Flow (VRF) Systems, Air-Handling Units (AHU), Chillers, Fan-Coil Units, Packaged/Rooftop Units, and Other AC/Ventilation Equipment) and Heating Equipment (Air-to-Water Heat Pumps, Ground-Source Heat Pumps, Boilers/Furnaces/Radiators, and Hybrid Heat-Pump Systems). End-User Industry further categorizes the market into Residential, Commercial (Offices, Retail, and Hospitality), Industrial and Manufacturing, and Institutional/Public Buildings; by Installation Type into New Construction and Retrofit/Replacement; and by Distribution Channel into OEM-Installer Networks, Wholesale/Distributor, and Direct-to-Consumer/E-commerce. Geographically, the report covers Germany, United Kingdom, France, Italy, Spain, Russia, Netherlands, and Rest of Europe. The market forecasts are provided in terms of value (USD).

By Equipment

| Air-Conditioning / Ventilation Equipment | Single-Split and Multi-Split Units |

| Variable Refrigerant Flow (VRF) Systems | |

| Air-Handling Units (AHU) | |

| Chillers | |

| Fan-Coil Units | |

| Packaged / Rooftop Units | |

| Other AC / Ventilation Equipment | |

| Heating Equipment | Air-to-Water Heat Pumps |

| Ground-Source Heat Pumps | |

| Boilers / Furnaces / Radiators | |

| Hybrid Heat-Pump Systems |

By End-User Industry

| Residential |

| Commercial (Offices, Retail, Hospitality) |

| Industrial and Manufacturing |

| Institutional and Public Buildings |

By Installation Type

| New Construction |

| Retrofit / Replacement |

By Distribution Channel

| OEM-Installer Networks |

| Wholesale / Distributor |

| Direct-to-Consumer and E-commerce |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Rest of Europe |

| By Equipment | Air-Conditioning / Ventilation Equipment | Single-Split and Multi-Split Units |

| Variable Refrigerant Flow (VRF) Systems | ||

| Air-Handling Units (AHU) | ||

| Chillers | ||

| Fan-Coil Units | ||

| Packaged / Rooftop Units | ||

| Other AC / Ventilation Equipment | ||

| Heating Equipment | Air-to-Water Heat Pumps | |

| Ground-Source Heat Pumps | ||

| Boilers / Furnaces / Radiators | ||

| Hybrid Heat-Pump Systems | ||

| By End-User Industry | Residential | |

| Commercial (Offices, Retail, Hospitality) | ||

| Industrial and Manufacturing | ||

| Institutional and Public Buildings | ||

| By Installation Type | New Construction | |

| Retrofit / Replacement | ||

| By Distribution Channel | OEM-Installer Networks | |

| Wholesale / Distributor | ||

| Direct-to-Consumer and E-commerce | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Europe HVAC equipment market?

The market was valued at USD 30.45 billion in 2025.

How fast is the Europe HVAC equipment market expected to grow?

It is projected to register a 6.25% CAGR, reaching USD 41.22 billion by 2030.

Which equipment segment is expanding the fastest?

Ground-source heat pumps are forecast to grow at 10.2% CAGR through 2030.

Why is the Netherlands the fastest-growing national market?

Coordinated policies aim for heat-pumps in 20% of Dutch homes by 2030, driving a 9.7% CAGR.

What restrains wider adoption of heat-pump technology?

The main barriers are high upfront costs versus boilers and ongoing supply-chain inflation for key materials.

How are manufacturers addressing installer shortages?

Leading OEMs are acquiring service firms and funding large-scale training programs to expand qualified labor capacity.

Page last updated on: