Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

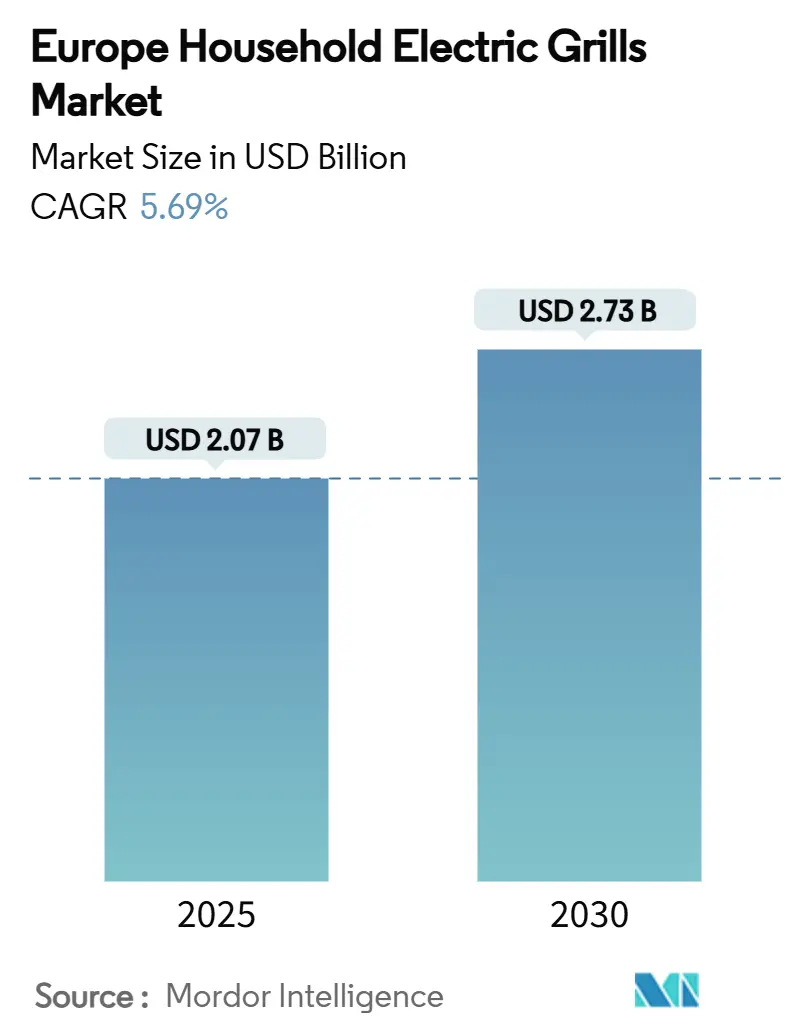

| Market Size (2025) | USD 2.07 Billion |

| Market Size (2030) | USD 2.73 Billion |

| Growth Rate (2025 - 2030) | 5.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Household Electric Grills Market Analysis by Mordor Intelligence

The Europe household electric grills market size is estimated at USD 2.07 billion in 2025 and is forecast to reach USD 2.73 billion by 2030, advancing at a 5.69% CAGR. Urbanization, tighter fire safety codes, and the European Union’s push for low-emission home appliances have accelerated adoption. Manufacturers are focusing on compact, high-performance models that fit small balconies while achieving searing temperatures comparable with gas grills. Smart-home integration and connected cooking apps are justifying premium prices, and e-commerce is widening access across the region’s fragmented retail landscape. Regulatory initiatives under the Eco-design for Sustainable Products Regulation (ESPR) have further raised the bar on energy efficiency, creating a competitive arena where sustainable design is a prerequisite rather than a differentiator.

Key Report Takeaways

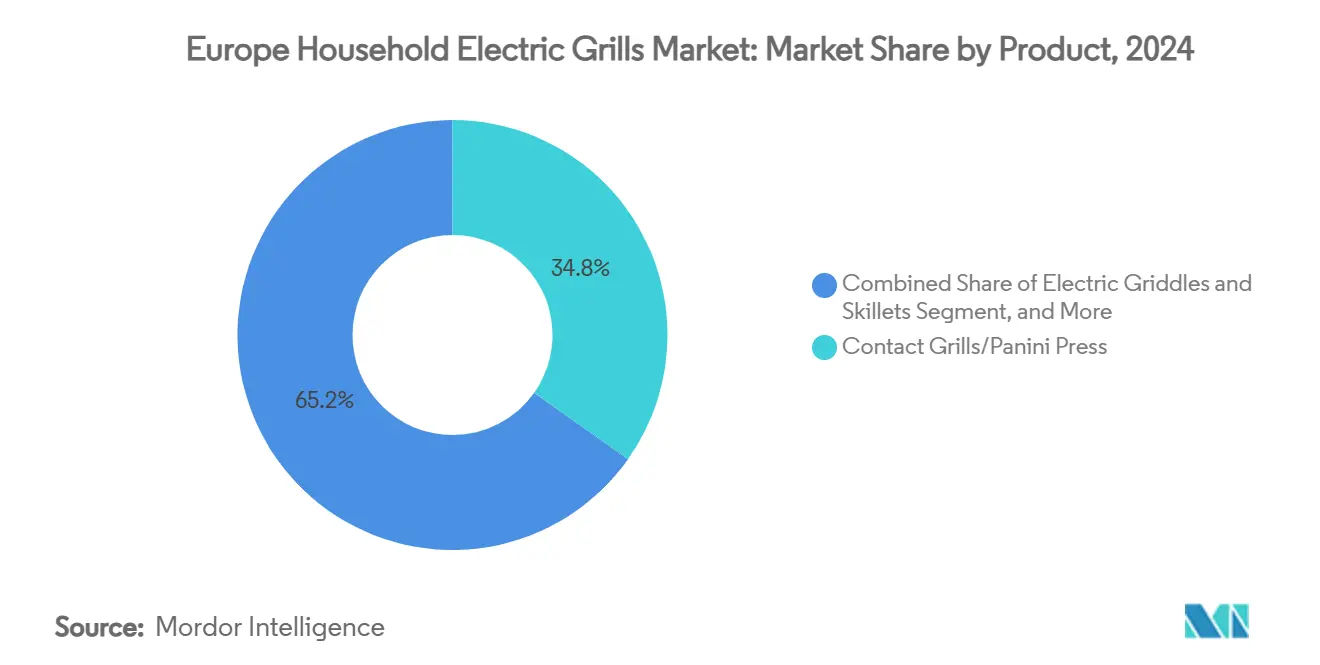

- By product category, contact grills led with 35% revenue share in 2024, while electric smokers are projected to expand at a 5.9% CAGR to 2030.

- By functionality, indoor models held 70.3% of the European household electric grills market share in 2024; outdoor units record the fastest CAGR at 6.1% through 2030.

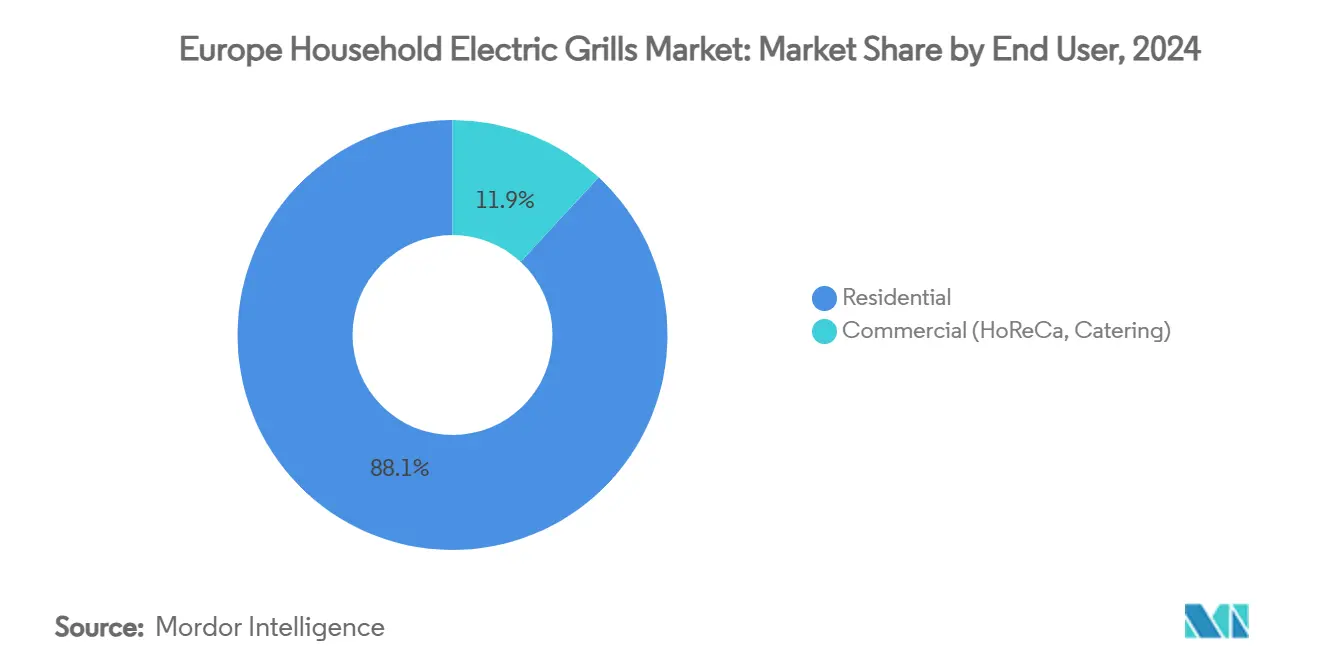

- By end-user, the residential segment accounted for 88.1% share of the Europe household electric grills market size in 2024, while commercial applications are advancing at a 5.7% CAGR.

- By distribution channel, offline retail commanded 60.4% of 2024 revenue, whereas online retail is forecast to grow at 7.1% CAGR.

- By geography, Germany led with a 20.2% share in 2024, and the Nordic region is poised for the quickest expansion at a 6.4% CAGR to 2030.

Europe Household Electric Grills Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban apartment fire-code limits | +1.4% | Germany, UK, France, urban centers | Short term (≤ 2 years) |

| EU Green-Deal electrification policies | +1.7% | EU-wide; strongest in Nordics, Germany | Medium term (2-4 years) |

| Social-media-driven home-gourmet trend | +1.1% | Pan-European; highest in UK, France | Short term (≤ 2 years) |

| Smart-IoT integration | +0.9% | Germany, Nordics, UK | Medium term (2-4 years) |

| Compact balcony/patio models | +1.0% | Southern Europe urban areas | Medium term (2-4 years) |

| E-commerce direct-to-consumer brands | +0.7% | UK, Germany, Pan-European | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Apartment Fire-Code Limits Boosting Electric Grill Adoption

European city councils have tightened fire-code restrictions, prohibiting open-flame cooking on many balconies. In markets where 72% of residents already live in urban settings, this policy shift has channeled demand toward electric solutions that meet safety regulations. The European household electric grills market is, therefore, benefiting from compact units that still reach 600°F, satisfying consumers who feared inadequate heat for searing.[1]Rylander, Summer, “Best Grills, Tested and Reviewed,” foodandwine.com German and French retailers reported double-digit sales growth in 2024 for models explicitly labeled “balcony-safe.” Manufacturers continue to miniaturize heating elements and incorporate ceramic coatings that boost thermal efficiency without increasing footprint.

EU Green-Deal Electrification Policies Favoring Emission-Free Cooking

The European Green Deal has embedded efficiency labels into appliance buying decisions, with 93% of consumers consulting the rating before purchase. As energy-saving measures delivered household savings up to EUR 266 (USD 313.28) in 2020, the policy narrative strengthened the total-cost-of-ownership case for electric grills. Competitive pressure within the Europe household electric grills market now centers on meeting or exceeding the A-class benchmark under the ESPR framework. Brands that earn the top tier can advertise quantifiable running-cost benefits, capturing share in price-sensitive regions and driving premium model upgrades in high-income markets.

Social-Media-Driven Home-Gourmet Grilling Trend

Lockdowns created a cohort of amateur chefs who publicize cooking results on Instagram and TikTok. Precision temperature control and smoke-free indoor operation allow visually appealing plates, positioning electric grills as tools for social affirmation. Younger urban consumers - especially in France and the UK - have broadened category participation beyond traditional barbecue audiences. The European household electric grills market is responding with colorful chassis designs, LED interfaces, and quick-share recipe libraries that transform a utilitarian appliance into a lifestyle accessory.

Smart-IoT Integration Enhancing Premium Grill Appeal

Connected grills equipped with Wi-Fi monitoring fetch price points 70% above basic models. Sensors and predictive algorithms maintain stable heat zones from 200°F to 700°F, enabling restaurant-quality results at home. Early adopters in the Nordics and Germany - regions with high smart-home penetration - are embracing remote control functions that let users adjust settings from a smartphone. As firmware updates deliver new cooking modes, owners perceive the product as an evolving platform rather than a static appliance, extending upgrade cycles and boosting repeat sales across the Europe household electric grills market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High average price vs charcoal/gas | -0.9% | Southern & Eastern Europe | Medium term (2-4 years) |

| Energy-cost inflation | -1.1% | Germany, Italy, Pan-European | Short term (≤ 2 years) |

| Perceived flavor inferiority | -0.6% | Southern Europe, Germany | Long term (≥ 4 years) |

| EU eco-design compliance costs | -0.5% | EU-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Average Price vs Charcoal/Gas Alternatives

Electric grills still command list prices 40-60% above entry-level charcoal units, testing consumer budgets in price-sensitive regions. The economic slowdown has accelerated a “trading down” trend, with households delaying discretionary appliance purchases. Manufacturers have added lower-wattage models to mitigate sticker shock, yet engineering standards needed for fast heat-up times prevent the deep cost cuts seen in other small-appliance categories. This price gap tempers headline growth in the Europe household electric grills market, especially in Southern and Eastern Europe, where traditional wood-fired grilling remains culturally entrenched.

Energy-Cost Inflation Across Europe

Electricity tariffs rose by 12.3% in Germany and 14.7% in Italy during 2024, narrowing the operating-cost advantage once touted by electric-grill advocates. Consumers are acutely aware that a 2,000-watt grill draws similar power to a kettle or space heater. In response, vendors incorporate reflective liners, zoned heating, and idle-mode algorithms that cut power draw when the lid is closed. Although these features reduce real-world consumption, bill-shock fears continue to affect purchase intent, producing a short-term drag on the Europe household electric grills market.

Segment Analysis

By Product: Electric Smokers Disrupting Traditional Segment

Electric smokers registered a 5.9% CAGR outlook for 2025-2030, challenging the dominance of contact grills that accounted for a 35% Europe household electric grills market share in 2024. Innovations such as automated smoke generators and closed-loop thermostats let novices achieve authentic barbecue flavors without constant supervision. This technology convergence has expanded the segment’s addressable audience from outdoor enthusiasts to weekday users seeking slow-cooked meals with minimal prep time.

Contact grills continue to anchor category revenue because they excel in day-to-day tasks like sandwiches and steak searing. Meanwhile, raclette tables and tabletop party grills have carved a social-dining niche, and convertible indoor-outdoor platforms cater to small-space owners wanting flexible setups for different seasons. The product spectrum illustrates a maturing European household electric grills market where consumers own multiple specialized devices rather than a single all-purpose grill.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Functionality: Outdoor Segment Gaining Momentum

Outdoor-rated units are forecast to grow at 6.1% CAGR, eroding the indoor segment’s 70.3% market hold. Weather-sealed heating elements now reach 650°F, overcoming the historical performance gap with gas grills and enabling authentic sear marks outdoors. Balcony-sized frames comply with local bylaws, further stimulating adoption in apartment-dense cities.

The indoor category remains the workhorse of the Europe household electric grills market size due to its all-season practicality. Convertible models target households that entertain on patios during summer yet rely on countertop cooking in colder months. Vendors are layering smart-weather alerts, lid-open sensors, and recipe-driven automation across both formats, blurring the distinction and driving an upsell path toward premium SKUs.

By End-User: Commercial Applications Expanding Rapidly

The commercial channel is projected to advance at 5.7% CAGR, even though residential buyers generated 88.1% of 2024 revenue. Hotels, cafés, and quick-service restaurants favor electric grills for smoke control in open-kitchen environments. Energy-efficiency scores heavily influence procurement teams because small percentage gains translate into measurable utility-bill savings over long service lives in the Europe household electric grills industry.

Household demand keeps pace through urbanization and the ongoing replacement of aging gas grills. Premium residential models now feature dual-zone thermostats and sous-vide integration, technologies once reserved for professional kitchens. This crossover fuels brand awareness and reinforces the perception that an electric grill can deliver professional-grade results without special ventilation infrastructure

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Online Retail Reshaping Market Access

Online sales are expected to climb 7.1% annually, leveraging detailed product videos and algorithmic recommendations that simplify complex specification comparisons. Direct-to-consumer entrants exploit this channel to collect first-party data and iterate designs rapidly, shortening time-to-market for new features. In Norway, for example, barbecues sold online already represent 49.3% of the garden e-commerce segment, signaling how digital-first behavior can spill into higher-ticket appliances.

Physical showrooms retain a 60.4% revenue lead because consumers still value tactile assessment before committing to premium purchases. Retailers are therefore blending QR-code-enabled demo stations and augmented-reality apps to merge the immediacy of in-store trials with the breadth of online catalogues, reinforcing omnichannel loyalty across the Europe household electric grills market.

Geography Analysis

Germany retained a 20.2% share of the Europe household electric grills market in 2024, underpinned by stringent urban fire codes and a culture that prizes outdoor cooking. Retail assortments emphasize balcony-safe grills capable of 600°F sear zones, features that resonate with consumers seeking authentic steakhouse results on limited outdoor space. Specialty outdoor-living chains work alongside electronics stores to showcase live demonstrations that convert sceptics.

Nordic countries are forecast to grow at a 6.4% CAGR. High disposable income, environmental stewardship, and robust smart-home adoption make consumers comfortable paying premiums for connected energy-efficient models. Indoor and convertible units dominate sales due to long winters; nevertheless, summer festivals spur seasonal spikes for portable outdoor grills, highlighting cross-merchandising opportunities between appliance and leisure retailers.

The United Kingdom, France, and Italy each contribute significant volume but display distinct buyer personas. British shoppers gravitate to weather-resilient grills that promise year-round patio use. French households - often in compact apartments - prioritize slim, stylish chassis that complement modern kitchens. Italians remain wary of flavor trade-offs, so vendors promote hybrid designs capable of adding wood chips for smoke infusion. Spain, Benelux, Switzerland, and Austria round out the landscape with steady demand anchored in urban centers. These regional nuances compel brands to tailor feature sets, marketing messages, and distribution partners to local habits, ensuring the Europe household electric grills market achieves granular rather than blanket growth.

Competitive Landscape

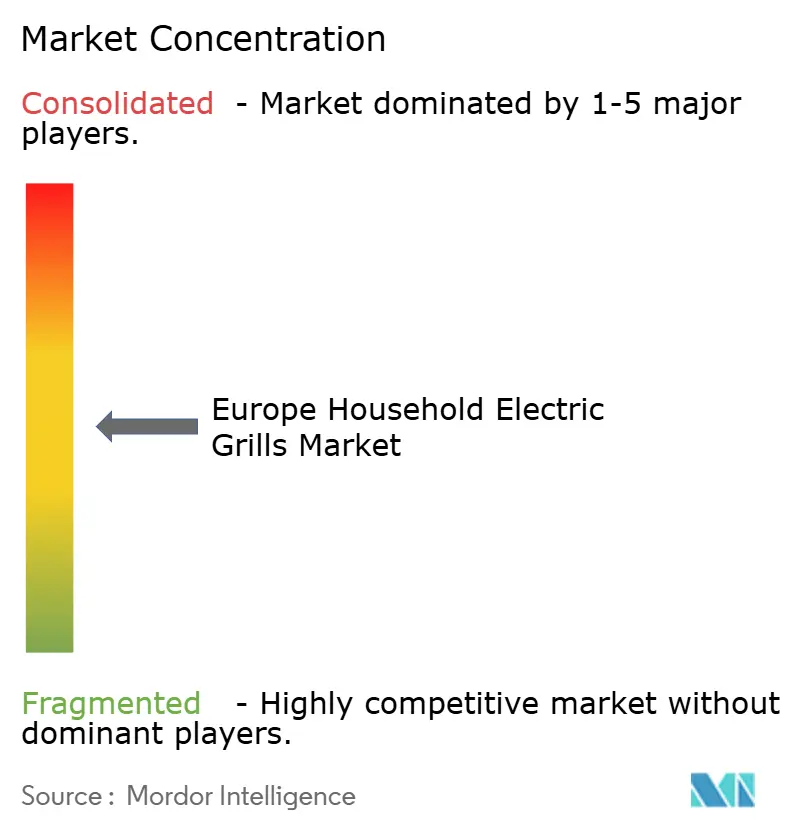

The market remains moderately fragmented: global appliance powerhouses, niche grill specialists, and agile direct-to-consumer labels all stake claims. Groupe SEB, through Tefal and Moulinex, reported EUR 8.3 billion (USD 9.78 billion) in sales in 2024 and controls about one-third of Europe’s small electrical cooking-appliance segment, underscoring the benefits of established channel relationships and deep R&D pipelines.[3]Groupe SEB, “Universal Registration Document & Annual Financial Report,” groupeseb.comElectrolux secured a EUR 200 million European Investment Bank loan in April 2025 to accelerate energy-efficient product development, highlighting sustainability as a capital-attractive theme.

Smart-first challengers such as Current Backyard differentiate with app ecosystems and firmware-upgradable hardware, positioning themselves as tech platforms rather than appliance vendors. At the entry-level, Asian contract manufacturers are white-labeling basic grills for online marketplaces, compressing margins in the value tier. Mid-market players therefore face a squeeze between premium connectivity and budget commoditization, prompting joint ventures and component-sharing agreements to manage costs while adding features.

Strategic moves over the past 18 months include Weber’s January 2025 electric-focused product line, designed to compete directly with high-end gas grills, and Groupe SEB’s December 2024 acquisition of Sofilac to deepen professional-grade know-how transferable to upscale residential models. These actions illustrate how scale and specialized expertise both serve as levers to secure competitive advantage in the evolving Europe household electric grills market.

Europe Household Electric Grills Industry Leaders

Philips Domestic Appliances

Groupe SEB (Tefal, Krups)

Spectrum Brands (Hamilton Beach/George Foreman)

Weber-Stephen Products LLC

Kenyon

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Electrolux Group obtained a EUR 200 million loan from the European Investment Bank to develop energy-efficient household appliances, including electric grills European Investment Bank.

- February 2025: Current Backyard released a Wi-Fi-enabled dual-zone smart grill capable of 700°F searing, priced at USD 899 Home Living Handbook.

- January 2025: Weber LLC introduced its 2025 electric grill range featuring advanced temperature control Weber LLC.

- December 2024: Groupe SEB finalized its acquisition of Sofilac to bolster professional cooking technology Groupe SEB.

Europe Household Electric Grills Market Report Scope

Electric Grills were substituted with Gas Grills in order to reduce the smoke and ease the cooking process . These are used to grill the food and they supply constant heat by using an electric element. TheEurope Household Electric Grills Market is segmented By Product (Electric Griddles, Electric Smokers), By End-use (Residential and Commercial), By Type (Indoor and Outdoor) and By Geography (Germany, Italy, Spain,United Kingdom,France and Rest of the Europe))

By Product

| Contact Grills/Panini Press |

| Electric Griddles and Skillets |

| Electric Smokers |

| Raclette and Table-top Party Grills |

| Convertible Indoor-Outdoor Grills |

By Functionality

| Indoor |

| Outdoor |

| Convertible |

By End-User

| Residential |

| Commercial (HoReCa, Catering) |

By Distribution Channel

| Offline Retail - Specialty Stores |

| Offline Retail - Hyper/Supermarkets |

| Department Stores |

| Online Retail |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Nordics (Sweden, Norway, Denmark, Finland) |

| Benelux (Netherlands, Belgium, Luxembourg) |

| Switzerland and Austria |

| Rest of Europe |

| By Product | Contact Grills/Panini Press |

| Electric Griddles and Skillets | |

| Electric Smokers | |

| Raclette and Table-top Party Grills | |

| Convertible Indoor-Outdoor Grills | |

| By Functionality | Indoor |

| Outdoor | |

| Convertible | |

| By End-User | Residential |

| Commercial (HoReCa, Catering) | |

| By Distribution Channel | Offline Retail - Specialty Stores |

| Offline Retail - Hyper/Supermarkets | |

| Department Stores | |

| Online Retail | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics (Sweden, Norway, Denmark, Finland) | |

| Benelux (Netherlands, Belgium, Luxembourg) | |

| Switzerland and Austria | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Europe household electric grills market?

The market stood at USD 2.07 billion in 2025 and is projected to reach USD 2.73 billion by 2030.

Which product segment is growing fastest?

Electric smokers are forecast to grow at 5.9% CAGR, outpacing other categories due to innovations that replicate traditional smoking with minimal effort.

Why are outdoor electric grills gaining traction?

Improved heating elements now achieve authentic sear temperatures, while balcony-friendly footprints and compliance with fire regulations make them attractive for urban residents.

How are EU regulations influencing product design?

The Eco-design for Sustainable Products Regulation requires higher energy efficiency and repairability, pushing manufacturers toward modular components and A-class energy labels.

What role does smart-home technology play in market growth?

Wi-Fi connectivity and predictive cooking algorithms command price premiums and appeal to tech-savvy consumers, especially in the Nordics and Germany.