Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

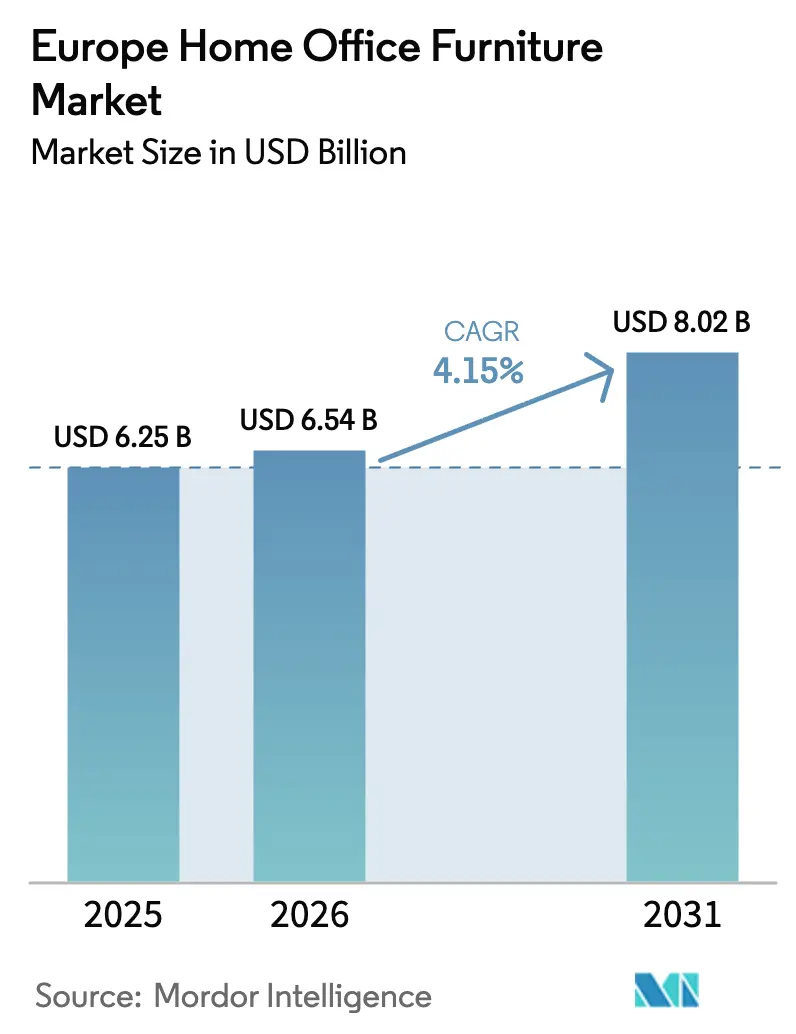

| Base Year Market Size (2025) | USD 6.25 Billion |

| Market Size (2026) | USD 6.54 Billion |

| Market Size (2031) | USD 8.02 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Home Office Furniture Market Analysis by Mordor Intelligence

The Europe Home Office Furniture Market size is expected to grow from USD 6.25 billion in 2025 to USD 6.54 billion in 2026 and is forecast to reach USD 8.02 billion by 2031 at 4.15% CAGR over 2026-2031.

Sustained hybrid work adoption has shifted home office furniture from discretionary purchasing to planned capital spending among employers and households that support remote and flexible work. Purchases are trending toward ergonomic compliance and higher specifications as European employment codes and workplace safety practices extend to hybrid arrangements, increasing the baseline quality of seating and desks. The channel mix continues to shift online as retailers scale e-commerce, add city logistics nodes, and integrate visualization tools that reduce showroom dependence. Regulatory momentum favors certified and traceable materials, which support wood-based products with a credible chain-of-custody and accelerate the transition to recycled and bio-based inputs in plastics. Companies able to execute omnichannel retail, digital features in products, and supply-chain compliance are using these capabilities to consolidate share across the Europe home office furniture market.

Key Report Takeaways

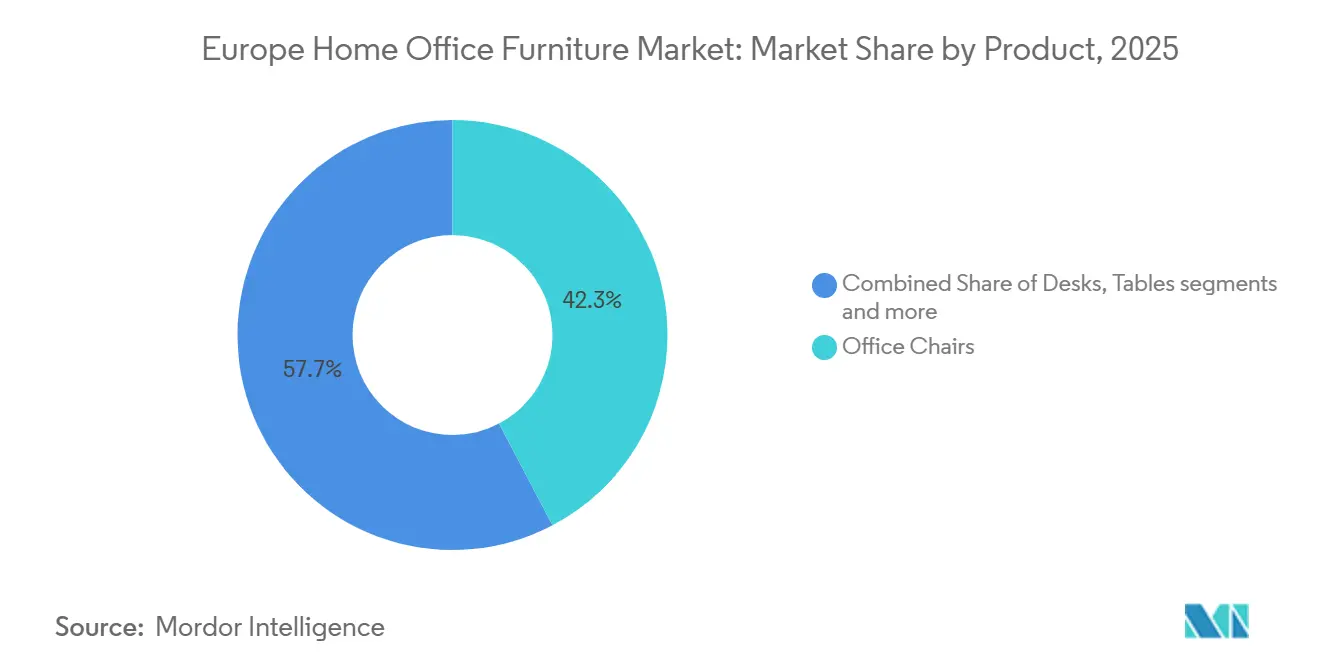

- By product type, office chairs accounted for the largest share of the Europe home office furniture market, representing 46.35% of the total market size in 2025, and are expected to register an 8.65% CAGR during 2026–2031.

- By material, wood held 51.37% of the Europe home office furniture market share in 2025, while plastics and polymers are projected to grow at a 9.32% CAGR through 2031.

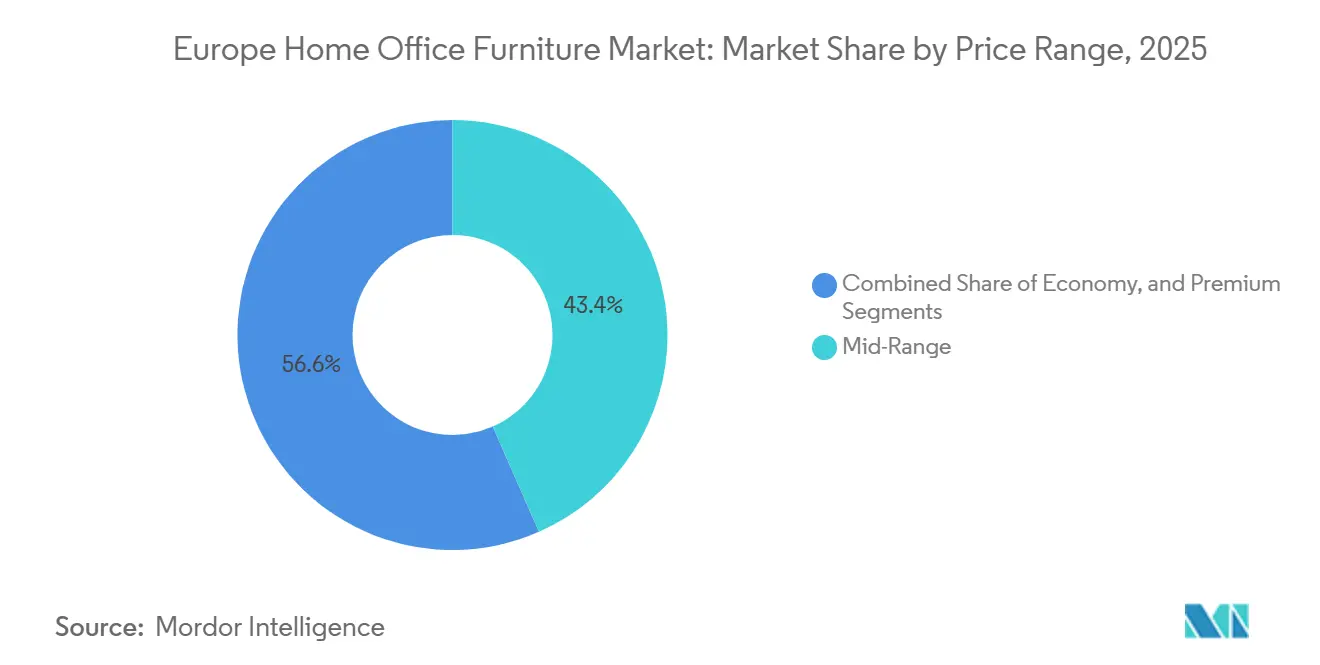

- By price range, the mid-range tier accounted for 43.35% of the Europe home office furniture market share in 2025, and the premium tier is forecast to expand at an 11.75% CAGR to 2031 as smart features and sustainability drive willingness to pay across the market.

- By distribution channel, specialty stores held 42.38% of the Europe home office furniture market share in 2025, while online is the fastest-growing channel at a 13.76% CAGR through 2031.

- By geography, Germany accounted for 26.36% of the European home office furniture market share in 2025, while Spain is projected to record the fastest growth at an 11.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Home Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Hybrid Work Models Across Europe | +1.8% | Global, with the highest concentration in the Netherlands, the UK, and Germany | Medium term (2-4 years) |

| Advancements in Smart and Connected Furniture Technologies | +1.2% | Western Europe's core with adoption in Germany, the Netherlands, Nordics | Long term (≥ 4 years) |

| Surge in Online Furniture Sales Across Europe | +1.4% | Global, led by the UK, the Netherlands, the Nordics, with Southern Europe accelerating | Short term (≤ 2 years) |

| Increasing Consumer Preference for FSC/PEFC-Certified Sustainable Furniture | +0.9% | EU-wide, with strong traction in Germany, the Netherlands, Nordics | Medium term (2-4 years) |

| Rising Demand for Modular and Space-Saving Furniture Due to Urban Downsizing | +0.7% | Urban cores of major European cities with micro-living hubs | Long term (≥ 4 years) |

| Growing Awareness and Adoption of Ergonomic Furniture | +1.0% | Pan-European, with higher adoption in Germany, the UK, and Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Hybrid Work Models Across Europe

Hybrid working has shifted from a pandemic-era exception to a sustained norm across European labor markets, underpinning steady demand for home office furniture. Hybrid arrangements now constitute the dominant flexible work model in the EU, with around 44 % of telework-capable employees working in hybrid patterns and full remote work stabilizing above pre-pandemic levels, indicating a durable equilibrium of remote and in-office days. Eurostat data show that over 50 % of European enterprises held remote meetings in 2024, reflecting widespread adoption of hybrid collaboration infrastructure. Country‑specific figures highlight the Netherlands, where more than half of the workforce (≈52 %) work from home at least part‑time, and the UK exhibits strong hybrid prevalence, with approximately 28 % of workers in hybrid roles. [1]Eurostat, 53 % of EU enterprises held remote meetings in 2024, European Commission, europa.euPolicy momentum, such as forthcoming Europe directives on platform work and telework rights, continues to shape formal hybrid work frameworks that embed remote setup expectations into employer compliance and worker benefits. Employer adoption of hybrid norms, combined with persistent worker preference for flexible arrangements, supports consistent replacement cycles for ergonomic chairs and adjustable desks as part of compliant home workspaces, reinforcing growth in the home office furniture market.

Advancements in Smart and Connected Furniture Technologies

Digital features such as app-linked height presets, posture coaching, and occupancy analytics have moved into mainstream assortments in premium and mid-range seating and desks. Leading manufacturers have launched upgraded collections that make active ergonomics more accessible and integrate electric actuators, safety features, and cable management to support all-day usage for hybrid workers. For instance, JIECANG Group launched smart motion furniture solutions for home and commercial offices at Interzum 2025 in Cologne, featuring advanced actuators, smart standing desks with OTA updates, and energy-efficient power systems. The company also opened a new manufacturing facility in Hungary to serve European demand, highlighting the growing adoption of connected furniture technologies across Europe [2]JIECANG Group, “JIECANG Group at Interzum 2025: Empowering the European Furniture Industry with Tech Innovation and Local Manufacturing,” JIECANG Group, jiecang.com. Peer-reviewed research and early market deployments suggest that smart furniture can support healthier sitting behaviors and provide real-time feedback through sensors, which aligns with employers’ broader push for wellness and ergonomic risk mitigation across home workstations. Brands are also emphasizing residential warmth through material palettes and finish choices while preserving commercial durability, which improves acceptance in living spaces. As these use cases become familiar and prices normalize, the Europe home office furniture market will see higher smart feature attachment rates within higher-value SKUs.

Surge in Online Furniture Sales Across Europe

E-commerce has solidified as a durable route to market for furniture, with growing consumer comfort in purchasing large items online supported by better delivery options and visualization tools. Official statistics confirm meaningful engagement with online purchasing of furniture and home products across the EU, while leading retailers report material online shares of total sales in large European markets. For instance, in 2024, European B2C e-commerce turnover grew by 7 %, rising from around €784 billion to €842 billion, with real growth of about 4.6 % after adjusting for inflation. This performance reflects strong consumer demand, broader product offerings (including second-hand and circular options), increased trust, and continued business investment in technology, logistics, and customer service [3]Ecommerce Europe and EuroCommerce, “New Growth in European E‑commerce Indicates Sector’s Ability to Adapt and Reinvent,” Ecommerce Europe, europa.eu. Network investments, including more local pickup points and store-based fulfillment, have shortened delivery windows and increased the effective assortment online. Premium brands are expanding direct-to-consumer online stores in more European countries, recognizing that omnichannel reach is now essential for discoverability and conversion. These advancements strengthen the share capture of online against traditional formats across the Europe home office furniture market.

Increasing Consumer Preference for FSC/PEFC-Certified Sustainable Furniture

Certification has become a core component of the European furniture market as supply chain due diligence requirements tighten, and buyers adopt stricter sustainability standards. FSC and PEFC frameworks provide verified chain-of-custody assurance for wood inputs, offering companies a practical means to demonstrate low-risk, responsible sourcing. In December 2024, the European Union extended the implementation timeline of the Regulation on Deforestation‑Free Products (EUDR), which mandates that timber-based goods placed on the European market do not contribute to deforestation or forest degradation. Under this extension, compliance will be required from 30 December 2025 for large and medium companies and 30 June 2026 for micro and small enterprises, including geolocation tracking and evidence of sustainable sourcing after 31 December 2020 [4]European Commission, “Regulation on Deforestation‑Free Products,” European Commission, europa.eu. While certification alone does not replace the regulation’s due diligence obligations, it provides essential documentation and credibility that support risk assessments and supplier engagement. These regulatory and market pressures enhance the attractiveness of FSC/PEFC-certified products and encourage broader adoption among consumers and businesses alike. As a result, larger players with the capacity to implement robust compliance systems are particularly well-positioned to capture growth in the Europe home office furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Wood and Metal Prices Affecting Production Costs | -1.1% | Global pressure on Scandinavian and Central European supply chains | Short term (≤ 2 years) |

| Eurozone Inflation Reducing Consumer Spending on Home Furniture | -0.8% | Eurozone-wide, with notable pressure in large economies | Medium term (2-4 years) |

| Growth of Second-Hand and Furniture-Rental Services Limiting New Furniture Sales | -0.6% | Urban cores in major European markets with advanced circular schemes | Long term (≥ 4 years) |

| Rising Energy Costs Increasing Manufacturing & Logistics Expenses | -0.7% | Pan-European, with the highest impact in Germany, Italy, and France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fluctuating Wood and Metal Prices Affecting Production Costs

Sawmills and downstream manufacturers have managed significant price swings in wood products that affected margins in 2024 and 2025, with signs of stabilization toward the turn of 2025 as capacity adjusted. Industry updates from large European producers indicate a period of weak demand and oversupply in parts of the wood chain, which triggered capacity reductions and price compression that fed through to furniture inputs. The regulatory environment also introduces new cost layers for timber-based materials due to traceability and due diligence requirements under the Regulation on deforestation-free products that begin to apply from late 2025 for larger operators. In metals, energy cost pressures and global supply issues affected aluminum more than steel across 2025, while policy frameworks like CBAM in 2026 will shape the cost competitiveness of imported and emissions-intensive inputs for furniture frames. These combined cost dynamics create planning challenges for manufacturers and retailers that serve the Europe home office furniture market and increase the value of scale procurement and hedging.

Eurozone Inflation Reducing Consumer Spending on Home Furniture

Household purchasing power in the euro area improved into 2025 as headline inflation moderated, although consumer goods spending remained uneven and sensitive to price levels. ECB projections and bulletins document a gradual easing of inflation, with non-energy industrial goods pricing steadying at moderate rates through mid-2025 and producer prices in several consumer categories cooling. Aggregate saving rates remained relatively high in late 2025, reflecting caution and preference to rebuild buffers, which weighed on discretionary categories like furniture. Retail sales volumes have shown signs of stabilization rather than a strong rebound, which suggests that price and value positioning will remain central to winning share. This backdrop reinforces the role of value-engineered mid-range products and sustained promotions across the Europe home office furniture market as purchasing power normalizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Seating Dominance Anchored by Ergonomic Mandates and IoT Integration

Office chairs accounted for 46.35% of the Europe home office furniture market size in 2025 and are projected to be the fastest-growing product category, expanding at an 8.65% CAGR through 2031, reinforcing their central role in ergonomic compliance and daily comfort for hybrid workers. Employers and insurers recognize the value of well-designed seating, and brands have refreshed offer lines with chairs that blend residential aesthetics and commercial performance to better fit living spaces. Several manufacturers have brought to market updated chairs with enhanced adjustability, new materials for warmth, and options that pair with app-based guidance. Peer-reviewed work on smart chairs supports a long-run innovation path that includes sensors for posture, pressure mapping, and real-time behavior cues that can reduce musculoskeletal risks. These dynamics reinforce the category's lead as connectivity and comfort converge in the Europe home office furniture market.

Height-adjustable desks have broadened into mid-range budgets, helped by component and actuator advances that increase reliability and safety while reducing noise and complexity. Actuator suppliers and desk manufacturers now emphasize smoother transitions, collision protection, cable management, and integrated power to better support work devices used at home. As price points normalize, households treat electric sit-stand desks as long-term wellness purchases, often coordinated with ergonomic chairs to build a coherent workstation. Storage and shelving tie directly to the needs of small apartments and flex rooms, with vertical solutions that help reclaim floor space and maintain sightlines in multi-use areas. Together, the product mix shifts toward devices that actively support better work habits and space optimization within the Europe home office furniture market.

By Material: Wood’s Certified Hegemony Challenged by Recycled Plastics’ Regulatory Tailwind

Wood products held 51.37% market share in 2025 backed by robust forest certification coverage in core markets and long-standing consumer preference for natural aesthetics and tactile quality in the Europe home office furniture market. National certification participation in countries like Germany strengthens supply continuity for EUDR compliance, as due diligence rules start to apply for large and mid-sized operators from December 30, 2025. Certification schemes like PEFC and FSC remain central to chain-of-custody assurance, and their scope across companies and hectares allows buyers to reduce procurement risk under the new Europe regulation. At the same time, plastics and polymers are the fastest-growing material category at a 9.32% CAGR through 2031 as manufacturers raise recycled content and trial bio-based materials for foams and shells. The result is a portfolio rebalancing that keeps wood at the center while unlocking new growth in recycled plastics for cases where durability and circular content can be credibly demonstrated in the Europe home office furniture market.

Metals face a bifurcation as imported and emissions-intensive inputs will increasingly be priced under the future CBAM application, which draws a premium to lower-carbon routes and renewable power sourcing in smelting. This favors brands that secure certified supply and communicate embedded carbon values within the Digital Product Passport framework under the European product policy. Recycled plastics gain from investments by large retailers into pre-processing and reprocessing networks that can reuse foams and rigid polymers, which further accelerate adoption in casters, arm caps, backing, and trays. Certification and design validation for recycled content also aid in product claims during procurement and help with future take-back loops. As compliance requirements intensify and the DPP registry takes shape, materials with traceable properties and proven recyclability will gain share in the Europe home office furniture market.

By Price Range: Premium Tier Surges as Sustainability and Smart Features Command Willingness-to-Pay

The mid-range tier held 43.35% market share in 2025 as it balances price with credible ergonomic features, while the premium tier is the fastest-growing at 11.75% CAGR to 2031 in the European home office furniture market. Premium demand is buoyed by the willingness to pay for durable materials, attractive finishes, and integrated smart features that support healthier workdays and offer a cohesive aesthetic with living spaces. Premium brands have expanded their direct retail presence in major European cities, offering a mix of contract showrooms and consumer-facing floors that help translate brand narratives to home buyers. Product development in this tier invests in connectivity, sustainability claims backed by materials choices, and collaborations or licenses with design houses to differentiate. These features appeal to households that view home workstations as permanent fixtures and to employers that co-fund home setups, supporting premium outperformance within the Europe home office furniture market.

Mid-range assortments continue to improve with more certified wood, better surface durability, and stable mechanisms, while large retailers emphasize affordability and faster delivery. Multiple large retailers have executed price investments and online network upgrades, aiming to sustain volumes despite consumer caution in 2025. Economy tiers remain challenged by the growth of second-hand supply and rental options in cities, which can substitute for new purchases among price-sensitive households. Over time, the diffusion of better features down the price ladder will support mid-range competitiveness, while the premium tier maintains an edge through materials, finishes, and digital experiences. This barbell pattern keeps volume anchored in mid-range while margin growth concentrates in premium across the Europe home office furniture market.

By Distribution Channel: Online Ascendancy Reshapes Retail Economics as Specialty Stores Face Margin Compression

Specialty stores held 42.38% market share in 2025, while online channels are set to grow at a 13.76% CAGR to 2031 and take a larger role in discovery and fulfillment across the European home office furniture market. Online sales shares at leading retailers rose through FY2025 and are supported by investments in pickup points, localized logistics, and store-based fulfillment that turn retail footprints into e-commerce hubs. EU-level data confirm significant recent purchasing of furniture and home accessories online, with penetration broadening to older age cohorts as experience improves. Premium manufacturers expanded direct-to-consumer online stores in more European countries, reflecting a durable omnichannel reality that blends physical showrooms with online conversion. This shift intensifies competition for independent specialty retailers and rewards scale players that deliver fast, transparent, and affordable fulfillment in the European home office furniture market.

Store experiences are adapting to emphasize test-and-try for ergonomic seating, personalized configuration, and room planning that complements online tools. Retailers use smaller urban formats that showcase edited assortments and provide instant pickup, while large suburban stores shift some space to support last-mile fulfillment. As online traffic compounds, retailers integrate AR for fit and finish previews, while customer data supports better inventory placement and capacity planning. The net effect is a higher return on retail space where experiential roles and logistics roles are both optimized. These changes support the continued climb of online in the channel mix for the Europe home office furniture market while preserving high-value physical touchpoints.

Geography Analysis

Germany accounted for 26.36 % of the Europe home office furniture market size in 2025, remaining the largest national base due to strong forestry certification coverage and a large hybrid workforce. National environmental compliance supports a traceable wood supply under the upcoming due diligence regulations. Public investment programs and gradual recovery of real incomes provide a positive backdrop for household spending, despite slower construction completions in 2024 and 2025. Germany’s import and export patterns underline its central role in the Europe furniture trade, supporting scale retailers and premium design brands. Meanwhile, France faces restrained household demand as high savings rates keep consumer durables spending cautious.

Circular-economy adoption in France, including high-performing EPR schemes, enables take-back and remanufacturing models that moderate new product volumes at lower price points. Hybrid work adoption continues to expand, driving demand for space-efficient and flexible furniture in urban apartments. Policy frameworks focused on durability and repairability further guide assortments and influence procurement decisions. Urban living cores increasingly favor modular and adaptable solutions, aligning with consumer and business preferences. These initiatives also create additional service revenue pools for larger operators in the home office segment.

Italy remains a key design and supply hub, combining a deep manufacturing base, craft traditions, and global exports, although 2024 saw pressure on exports to mature European markets. Domestic demand is sensitive to household purchasing power, while EPR programs are promoting repair and second-hand pathways in line with Europe circular policy. Hybrid work legislation, effective in late 2024, supports ongoing demand for home workstation upgrades, complemented by contract projects in hospitality and mixed-use developments. Spain is the fastest-growing national market through 2031, at 11.38 % CAGR, driven by strong telework adoption, expanding e-commerce, and supportive residential activity. The United Kingdom maintains high hybrid-work penetration and online retail share, with flexible working rights and circular practices supporting both consumer and contract segments.

Value Chain Analysis

The value chain starts with certified raw materials and components, including FSC/PEFC wood panels and veneers, steel and aluminum for frames, plastics and foams, textiles, and electric actuators for sit-stand desks. Upstream traceability and documentation are getting more embedded as EU due-diligence requirements tighten for timber-based goods under the Regulation on Deforestation-Free Products (EUDR), with simplified obligations clarified via Regulation (EU) 2025/2650. This increases the need for mapped supplier data and auditable chain-of-custody alongside conventional cost and quality controls. Downstream, products move through branded DTC sites, online marketplaces, specialty retail, and omnichannel networks that connect store inventory with last-mile fulfillment and pickup points. Packaging efficiency and damage control are central for flat-pack and mixed-assembly SKUs.

Service layers, including installation, returns handling, refurbishment, and recycling, are also taking on more operational weight as furniture aligns with the Ecodesign for Sustainable Products Regulation (ESPR) priority set under the EU Working Plan 2025-2030. Manufacturers and retailers are adjusting design choices around repairability, parts availability, and future Digital Product Passport needs while managing input volatility, particularly wood and energy-linked metals, and handling cross-border logistics complexity across Europe.

Competitive Landscape

The Europe home office furniture market exhibits moderate concentration, led by large omnichannel retailers and premium design brands, while numerous regional and online players form a competitive long tail. The sector is shaped by three tiers of competitors: vertically integrated global players, premium design-led brands, and national or online retailers. Global players invest heavily in e-commerce hubs, new-format stores, and recycling infrastructure to support omnichannel operations and circular material use. These companies maintain significant online sales, implement pricing strategies for affordability, and continue capital investments in fulfillment and energy efficiency. This structure reinforces advantages for scale players while sustaining competition from smaller operators.

Leading brands emphasize active ergonomics and residential-friendly designs that integrate seamlessly into living spaces. Chair lines are updated with diverse finish options, and desk systems feature smooth electric lifts and integrated power management. Smart seating concepts incorporate sensors to encourage movement and healthier sitting habits during long work sessions. Sustainability initiatives include eliminating harmful chemicals, adopting recycled or bio-based materials, and planning long-term environmental strategies that guide product and supply choices. Brands that demonstrate these efforts through certifications and transparent reporting are better positioned to meet procurement requirements.

Regulations such as the Europe due diligence framework and Ecodesign for Sustainable Products are shaping company strategies, including readiness for digital product traceability. Companies with strong sourcing systems, geolocation tracking, and verified chain-of-custody credentials can navigate compliance more efficiently. These capabilities also support take-back and remanufacturing programs that recover materials and create value from residual assets. Investments in recycling capacity and strategic partnerships signal commitment to circularity goals and help future-proof material supply. Combined, these regulatory and operational dynamics reinforce consolidation advantages for large players while raising the compliance threshold for smaller competitors.

Europe Home Office Furniture Industry Leaders

Sedus Stoll AG

Bisley Office Furniture

Poltrona Frau

BoConcept

MillerKnoll, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

ESPR implementation creates a product and data readiness opportunity for home office furniture portfolios that can show durability, reparability, and circular attributes in a standardized way. Regulation (EU) 2024/1781 has been in force since 18 July 2024, and the European Commission adopted the ESPR Working Plan 2025-2030 on 16 April 2025, with furniture prioritized. That setup leaves near-term whitespace for building test methods, spare-part strategies, and product information systems ahead of the furniture-specific preparatory study scheduled for publication in early 2026. Certifications used in European office furniture, such as FEMB Level, provide an established pathway for sustainability claims that brands can leverage as they sell into more compliance-aware procurement and consumer channels.

Omnichannel expansion and DTC localization remain practical growth levers because online is the fastest-growing channel in the report scope, and leading brands are widening country coverage with dedicated e-commerce. Digital feature attachment, including power management, app-linked height presets, and posture guidance, also supports upsell in premium and upper mid-range SKUs, with supplier-side investments such as actuator and motion-component localization in Europe. In parallel, compliance-driven traceability under EUDR and emerging product-passport workflows reward manufacturers and retailers that can consolidate supplier data, including material origin and recycled content evidence, at SKU level across multiple European markets without fragmenting assortments by country.

Recent Industry Developments

- June 2026: Sedus Stoll Group communicated progress on strategic growth initiatives while navigating a challenging European office-furniture demand environment. The update reinforced continued focus on product and channel initiatives that overlap with home office demand, particularly where ergonomic seating and desks are bought for residential use through omnichannel routes.

- May 2026: MillerKnoll, through its Knoll brand, unveiled the Konzert private office system at Clerkenwell Design Week 2026. The launch highlighted continued premium product development and design-led differentiation, influencing how high-value workspace solutions are merchandised across Europe alongside home office assortments.

- April 2025: Herman Miller expanded its European direct-to-consumer footprint by launching dedicated online stores in Denmark, Finland, Spain, and Sweden. This rollout strengthened localized e-commerce access to core ergonomic chair and workspace products and increased competitive pressure on specialty retail by improving brand-controlled discovery and fulfillment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers home office furniture sold for use inside homes across Europe, mainly desks, chairs, tables, and storage units that support work or study from a residential setup. We size the market in value terms using manufacturer-level selling prices.

Scope exclusions: We exclude bulk purchases for corporate offices, contract furniture for co-working spaces, and second-hand furniture sales.

Segmentation Overview

- By Product

- Office Chairs

- Desks

- Height Adjustable Desks

- Fixed Desks

- Tables (side tables, printer tables, etc.)

- Storage Cabinets & Shelving

- Other Products (stools, bookcase, desk accessories, etc.)

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Home Centres

- Specialty Stores (including exclusive brand outlets)

- Online

- Other Distribution Channels

- By Geography

- Germany

- France

- Italy

- Spain

- United Kingdom

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a consistent fact base on furniture demand, trade flows, and pricing signals across Europe, then narrowing it to home office use. We reference public sources such as Eurostat structural business statistics and international trade tables, national statistics offices for household spending and housing indicators, and EU policy pages that shape product requirements (for example, chemical and material compliance rules that affect finishes and foam). We also review association and standards sources, such as European furniture industry bodies and ergonomics-related guidance, to keep product boundaries realistic.

After that, we align the market model to what suppliers actually report, using items like annual reports, investor presentations, and press releases for revenue splits and channel focus. These are checked against reported import and export trends. A paid subscription covering company financials and news, plus an import or export shipment-level database, is used selectively to clean up ownership changes and to sanity check where trade dynamics are shifting. The desk sources listed here are illustrative only, and many other public references are used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test what we built from public data, especially on mix shifts between chairs, desks, and storage, and on how online-led purchasing changes price points by country. We speak with manufacturers, distributors, retailers, and industry experts across major European markets. We then reconcile differences between what is said in interviews and what is visible in trade and consumption indicators, so the final view stays grounded in observable patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 18% | |

| Mid tier: 42% | Functional/Unit leaders: 35% | |

| Smaller Players: 19% | Managers: 47% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up approach, starting from Europe-level furniture and household spend signals, then filtering to the home office furniture demand pool using work-from-home incidence, home improvement spend direction, and home office penetration by country. The model is corroborated through selective bottom-up approximations, such as supplier revenue splits tied to home office ranges, sampled price bands for key items (chairs and desks), and channel checks on online versus offline mix.

Key inputs used in the model include household consumption and discretionary spend direction, furniture production and trade flows, typical price movement by product type (especially for ergonomic chairs), the share of hybrid work in the employed population, and housing indicators that influence space availability and move-in related purchases. Where direct splits are not available, we handle gaps by applying conservative proxy shares that are validated in interviews and then sensitivity tested, so one assumption does not drive the total.

For forecasting, we rely mainly on scenario analysis, where the pace of hybrid work adoption and replacement cycles forms the core scenarios, and then pricing and channel mix are adjusted based on what industry participants expect in the next few years. The final forecast is reviewed country by country to ensure the growth pattern aligns with realistic consumer demand and observed trade momentum.

Data Validation & Update Cycle

Validation is done through several checks that compare the market totals against independent signals, such as production and trade direction, household spending patterns, and the implied per-household spend on relevant furniture items. We review outliers, including sudden jumps in value that are not supported by volume or pricing logic, and then re-check assumptions with follow-up calls when a variance cannot be explained.

Before sign-off, the model goes through multi-step internal review, including consistency checks on currency conversion timing, inflation treatment, and country roll-ups to the regional total. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes, supply disruptions, or demand shocks. Right before delivery, the latest public updates are rechecked so clients receive an up-to-date view.

Mordor Intelligence's Europe Home Office Furniture Market Size Versus Other Published Estimates

Published market sizes for Europe home office furniture can look far apart because the scope line is drawn differently and the price basis is not always consistent, and then the forecast year chosen adds another layer of spread. We also see variation when some estimates use retail value and others use supplier selling price, which changes the total even if unit volumes are similar.

Trade and production signals, plus household consumption patterns for furniture categories, are the evidence checks that keep Mordor Intelligence aligned to a residential-only home office furniture demand pool rather than broader office furniture or full home furniture spending. The biggest gaps usually come from whether second-hand sales are counted, whether corporate bulk procurement is included, and how online channel markups and currency timing are treated when converting country totals to USD.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.25 B (2025) | |

| Trade Journal A | USD 7.20 B (2025) | Uses end-user prices and often blends in adjacent categories like broader home furniture spend, which can lift value beyond manufacturer selling prices for dedicated home office items. |

| Regional Consultancy B | USD 5.10 B (2025) | Applies conservative penetration assumptions for hybrid work and may exclude smaller online-led purchases and accessories, which can reduce the captured demand in countries with higher e-commerce share. |

Overall, the spread is mostly explained by price basis and boundary choices, rather than a true disagreement on demand direction. When scope is kept to residential use and totals are checked against trade and consumption indicators, the market size becomes easier to trace back to clear, repeatable steps.

Key Questions Answered in the Report

What is the current size and growth outlook of the Europe home office furniture market?

The Europe home office furniture market size is USD 6.54 billion in 2026 and is projected to reach USD 8.02 billion by 2031 at a 4.15% CAGR during 2026-2031, supported by hybrid work, online expansion, and sustainability-led material shifts.

Which product category leads demand in the Europe home office furniture market?

Office chairs lead with 46.35% share in 2025 and are also the fastest-growing product at an 8.65% CAGR to 2031, reflecting ergonomic compliance and comfort needs in hybrid work.

How is online retail changing the Europe home office furniture market?

Online is the fastest-growing channel at a 13.76% CAGR through 2031, driven by higher online shares at leading retailers, better delivery, and visualization tools that reduce showroom dependence.

Which materials will gain share in the Europe home office furniture market?

Wood remains the largest at 51.37% in 2025 due to certification, while plastics and polymers grow fastest at a 9.32% CAGR as recycled content and bio-based inputs scale under Europe product policy.

Which country will drive the fastest growth within Europe?

Spain is projected to be the fastest-growing geography at an 11.38% CAGR through 2031, helped by telework adoption, e-commerce growth, and improving residential activity.

Page last updated on: