Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

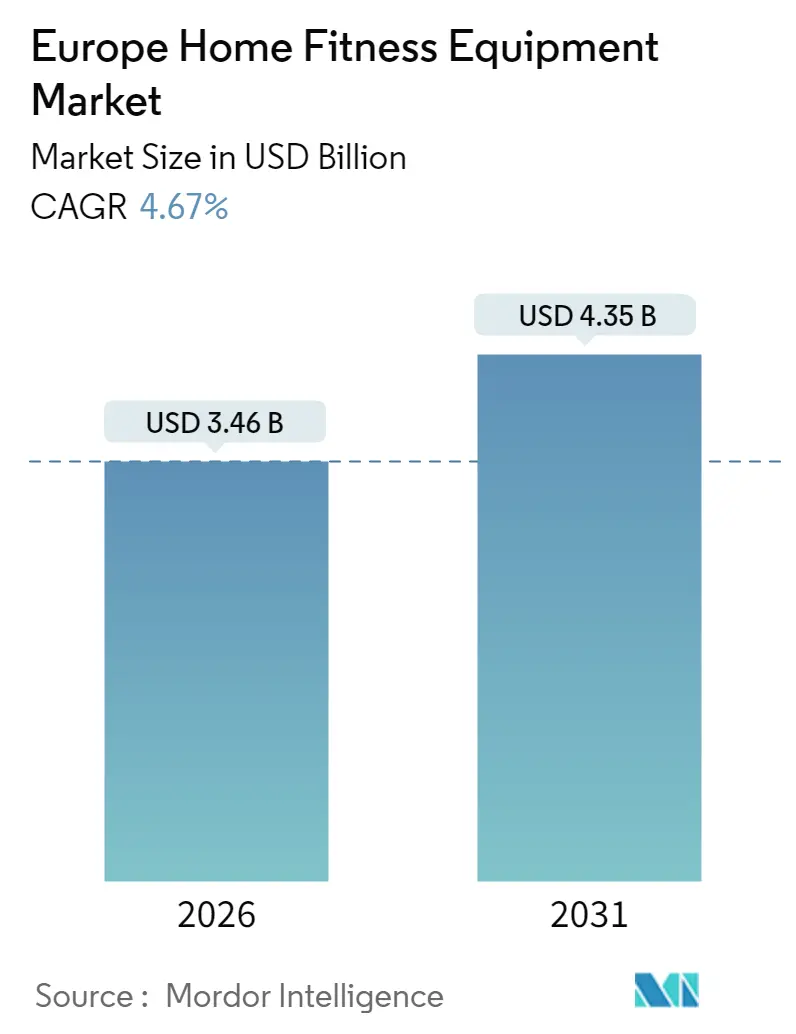

| Market Size (2026) | USD 3.46 Billion |

| Market Size (2031) | USD 4.35 Billion |

| Growth Rate (2026 - 2031) | 4.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Home Fitness Equipment Market Analysis by Mordor Intelligence

The Europe home fitness equipment market size in 2026 is estimated at $3.46 billion, growing from 2025 value of $3.31 billion with 2031 projections showing USD 4.35 billion, growing at 4.67% CAGR over 2026-2031. This demand surge signals a lasting lifestyle transformation, not merely a fleeting response to the pandemic. Alarmingly, the World Health Organization reports that 59% of adults in the region are overweight, and 1 in 3 children grapple with obesity[1]Source: World Health Organization, “European Regional Obesity Report 2024,” who.int. Retail giants are taking note. In January 2025, Decathlon unveiled its Compact Run 100 treadmill, Training Rower 900, and Training Bike 900. These space-efficient, mid-priced offerings cater to the 70% of urban Europeans, where floor space is at a premium. Furthermore, smart equipment with AI-driven form correction is paving the way for subscription-based revenues. Following this trend, Technogym's Checkup platform played a pivotal role in boosting their H1 2024 sales by 11.3%, reaching EUR 406.3 million (USD 440 million). The rise of e-commerce and direct-to-consumer logistics not only streamlines the purchasing process but also allows brands to gather valuable usage data, contributing to a notable 5.82% CAGR in online sales. While Germany holds a dominant 27.63% revenue share, attributed to its established wellness culture, Italy outpaces with a 5.19% growth rate, fueled by proactive government wellness initiatives and a younger, more affluent demographic.

Key Report Takeaways

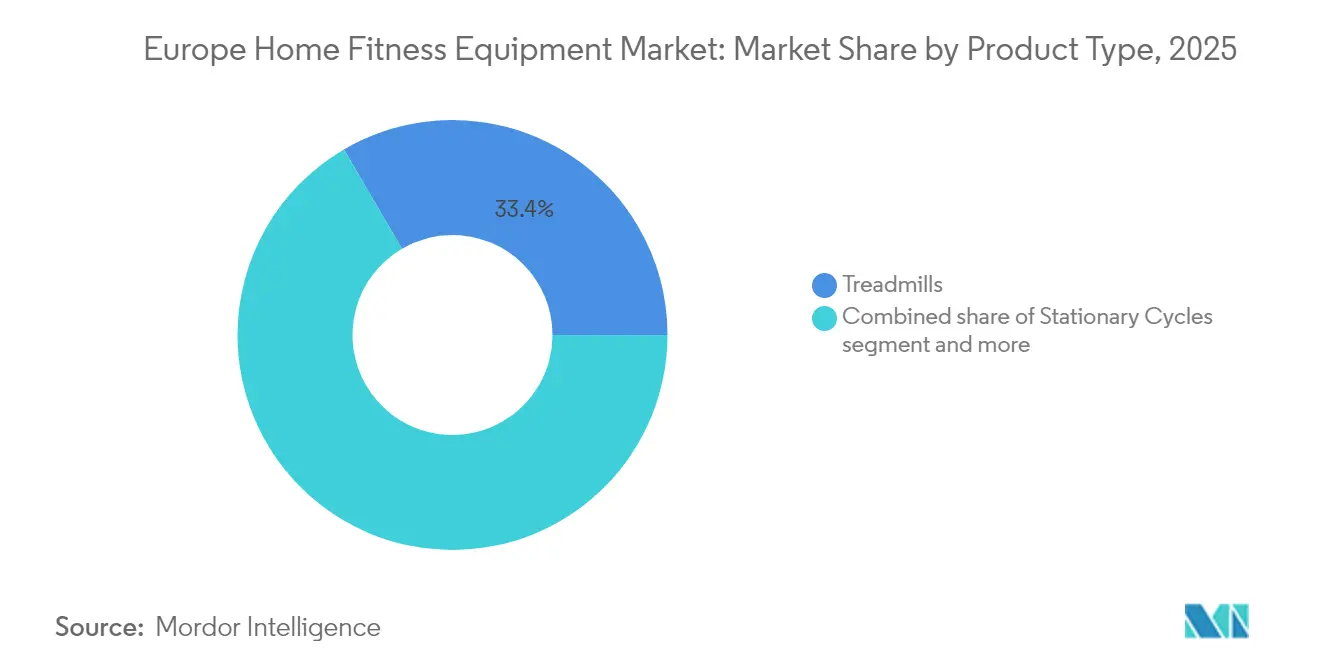

- By product type, treadmills led with a 33.42% revenue share in 2025, while stationary cycles are forecast to expand at a 4.98% CAGR through 2031.

- By category, conventional equipment commanded 61.05% of 2025 turnover, yet smart and connected variants are growing fastest at 6.80% CAGR.

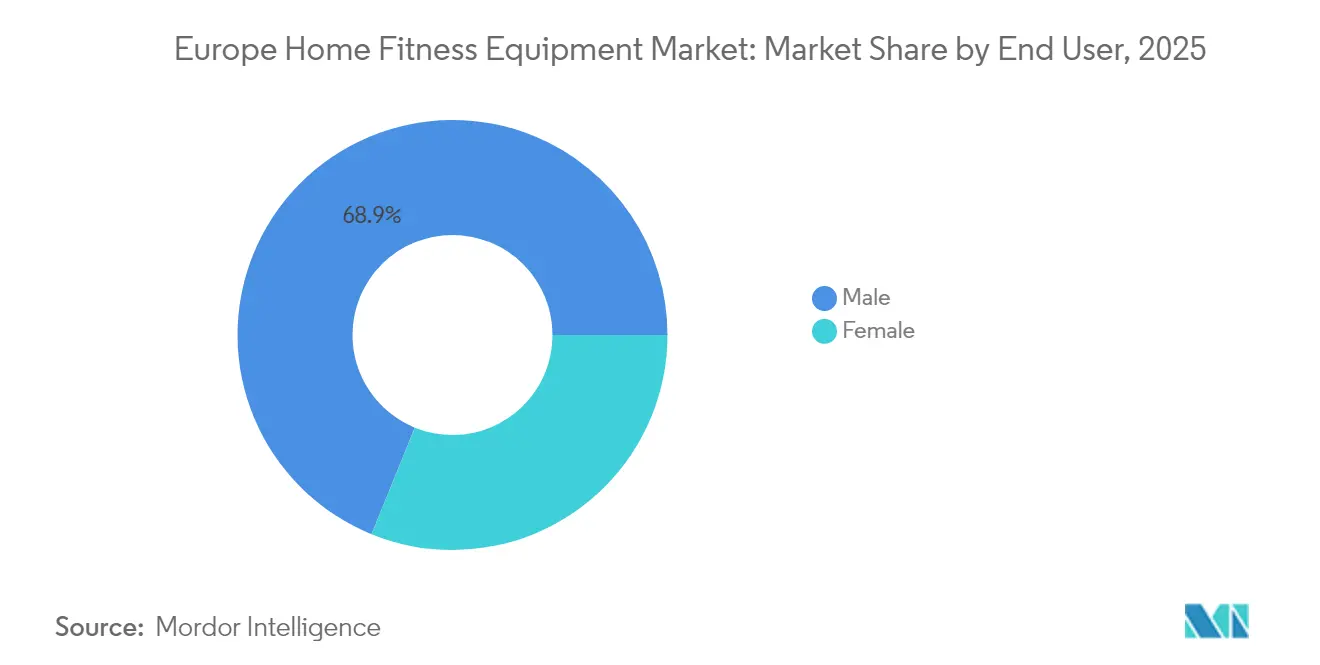

- By end user, male buyers contributed 68.85% of 2025 demand; the female segment is accelerating at a 6.02% CAGR.

- By distribution, offline retail captured 52.35% of 2025 sales, but online channels are rising at a 5.75% CAGR.

- By geography, Germany held 27.20% of 2025 revenue, while Italy is projected to post the fastest 5.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Home Fitness Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obesity and a health-awareness wave | +1.2% | Regional, with the highest prevalence in the United Kingdom, Germany, Spain | Long term (≥ 4 years) |

| Rapid product innovation in smart/connected gear | +1.0% | Germany, France, the United Kingdom, Netherlands | Medium term (2-4 years) |

| Expansion of e-commerce and D2C logistics | +0.8% | Germany, France, the United Kingdom, Italy, Spain | Short term (≤ 2 years) |

| Persistent hybrid (home + gym) workout habits | +0.7% | Germany, the United Kingdom, France, the Netherlands, Belgium | Medium term (2-4 years) |

| EU "Green Deal" spurring demand for energy-efficient equipment | +0.5% | EU-wide, strongest in Germany, the Netherlands, and Sweden | Long term (≥ 4 years) |

| Employer-subsidised home-fitness programmes for remote staff | +0.4% | Germany, the United Kingdom, France, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising obesity and health-awareness wave

In 2024, the World Health Organization's European Regional Obesity Report revealed that 59% of European adults grappled with obesity, a notable rise of 7 percentage points since 2015. Alarmingly, the report also highlighted that 1 in 3 children were affected. In response to this growing concern, national health systems are pivoting their focus towards preventive care. This includes subsidized fitness programs, which, in turn, are driving up demand for home fitness equipment. The WHO's monitoring framework for Health-Enhancing Physical Activity indicated a significant leap in policy achievement across the European Union: 81.8% in 2024, a jump from 64.7% in 2015. This underscores a steadfast governmental commitment to promoting active living. Despite these efforts, cardiovascular diseases continue to dominate, accounting for 45% of regional deaths. This grim statistic has fueled public health campaigns advocating for daily exercise. As clinical evidence mounts and fitness equipment becomes more accessible, even the most sedentary individuals find it easier to embark on strength and cardio training at home. Recognizing the importance of wellness, employers are weaving these metrics into corporate health plans, creating a scenario where owning fitness equipment becomes a tangible indicator of employee engagement.

Rapid product innovation in smart/connected gear

In the first half of 2024, Technogym's Checkup platform, leveraging AI for movement assessments and corrective exercise prescriptions, drove a 11.3% year-on-year revenue surge to EUR 406.3 million (USD 440 million). This underscores the premium pricing potential of software differentiation. Echelon Fitness, in October 2024, unveiled its Strength Home system: a foldable unit boasting a 24-inch HD touchscreen and digital resistance from 5 to 110 pounds, priced at USD 2,999.99. The launch targets urban residents without dedicated workout spaces. Despite Peloton reporting 2.9 million paid connected-fitness subscribers in its Q1 fiscal 2025 results, the company faced a 1.6% year-on-year revenue dip to USD 586 million. This trend suggests hardware saturation is nudging brands towards content monetization. In January 2025, Tonal Systems rolled out a B2B initiative, embedding its electromagnetic resistance units in hotels, physical therapy centers, and private gyms. This move diversifies its revenue channels beyond direct consumer sales. Equipment firmware now integrates biometric sensors, monitoring heart rate, cadence, and power output, for real-time coaching adjustments. However, this advancement amplifies data privacy responsibilities under the General Data Protection Regulation. As a result, manufacturers are channeling investments into fortified cloud systems and clear consent processes.

Expansion of e-commerce and D2C logistics

According to Eurostat, European e-commerce saw a 2.1% uptick in 2023. Notably, fitness equipment sales surged, as consumers, emboldened by pandemic-era trial periods, grew more comfortable purchasing high-ticket items online[2]Source: Eurostat, “E-commerce Statistics,” ec.europa.eu. In a strategic move, Decathlon unveiled "Decathlon Pulse" in January 2025, a dedicated mergers-and-acquisitions arm. This initiative underscores Decathlon's ambition to onboard digital-native brands, seamlessly weaving them into its omnichannel distribution framework. By adopting direct-to-consumer models, manufacturers are reaping margins of 30% to 40%, savings that typically benefit retail intermediaries. Moreover, these models empower manufacturers to gather invaluable first-party data, shedding light on usage patterns, churn triggers, and potential upsell avenues. Peloton's decision to shutter its Chicago factory in May 2024, pivoting to contract manufacturing in Taiwan, highlights a calculated balance between vertical integration and capital efficiency. Premium brands now consider white-glove delivery and in-home assembly as essential services. Given that treadmills and rowing machines can weigh between 100 to 150 kilograms and often need technical setup, this service has become paramount. Furthermore, the rise of augmented-reality apps, which allow buyers to visualize equipment in their homes, has led to a notable dip in return rates. Historically, these rates hovered around 15% for large fitness items shipped through parcel carriers.

Persistent hybrid (home + gym) workout habits

In Germany, gym memberships thrive alongside strong sales of home fitness equipment, indicating that consumers see these two avenues as complementary. Similarly, in 2023, gym-goers in the UK opted for home equipment on days when traveling to the gym felt time-consuming or when the facility was too crowded. This trend is especially evident among professionals aged 30 to 50, who value time efficiency and are open to investing in both gym memberships and home equipment. In April 2025, Decathlon teamed up with Freeletics, offering a 3-month complimentary subscription with equipment purchases. With a goal of rolling out over 100 co-branded products by the end of 2026, this partnership capitalizes on the growing preference for seamless transitions between home workouts and gym sessions. Basic-Fit, in March 2024, bolstered its network by acquiring RSG Spain, adding 42 clubs to its existing 1,575 locations and 4.25 million members. This move underscores the gym sector's belief that the rise in home equipment sales won't undermine gym memberships but will instead broaden the market. The enduring popularity of hybrid workout routines sheds light on the forecasted 5.05% CAGR growth of stationary cycles through 2030, a rate surpassing that of bulkier treadmills, thanks to their space efficiency and suitability for quick interval sessions.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront equipment cost | -0.9% | Italy, Spain, Poland, Belgium | Short term (≤ 2 years) |

| Limited living space in dense urban housing | -0.6% | Germany, France, the United Kingdom, Netherlands | Medium term (2-4 years) |

| Subscription-fatigue toward digital content fees | -0.5% | The United Kingdom, Germany, and France | Short term (≤ 2 years) |

| GDPR-driven data-privacy compliance costs | -0.3% | Europe-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront equipment cost

Mid-tier treadmills and rowing machines are moderately priced, while premium connected variants from Peloton and Technogym command high prices. This pricing dynamic poses a challenge for households in Italy, Spain, Poland, and Belgium, where median disposable incomes lag behind their Western European counterparts. Nautilus Inc. filed for Chapter 11 bankruptcy in March 2024, a move spurred by a 28.5% drop in cardio-equipment sales. This highlights the fragility of demand, especially when consumers see little distinction between premium and budget offerings. In January 2025, Decathlon rolled out the Compact Run 100 treadmill, priced for the mass market, targeting first-time buyers who value functionality over connectivity. While financing options like installment plans and lease-to-own structures are on the rise, eurozone interest rates remain high. As of December 2024, the European Central Bank's deposit facility rate stood at 3.00%, inflating the effective cost of credit[3]Source: European Central Bank, “Key Interest Rates,” ecb.europa.eu. Although the price-performance gap between traditional and smart equipment is shrinking due to declining component costs, concerns about ongoing subscription fees for connected devices heighten the total cost of ownership worries. Retailers have observed a 25% to 30% drop in conversion rates when checkout pages feature subscription prompts alongside hardware prices, underscoring the friction caused by bundling transparency.

Limited living space in dense urban housing

Seventy percent of Europeans live in urban areas. Over the past decade, as housing costs have risen, average dwelling sizes in these areas have shrunk. In cities like Paris, Berlin, and Amsterdam, treadmills take up a notable 1.5 to 2.0 square meters of floor space in apartments that typically average 70 to 90 square meters. Echelon's Strength Home system, launched in October 2024, folds down to a compact 30 centimeters, allowing it to be conveniently stored in closets or behind furniture. While treadmills accounted for 33.92% of 2024 revenue, rowing machines and stationary cycles, easily stored vertically or wheeled away, are capturing a growing market share. This trend explains the forecasted 5.05% CAGR growth for cycles through 2030. In multi-family buildings, noise transmission through shared walls and floors restricts equipment use, especially for high-impact activities like running. This challenge has led manufacturers to invest in technologies that dampen vibrations and design quieter motors. As cities grapple with rising costs, the emergence of micro-apartments, units under 40 square meters, has paved the way for ultra-compact fitness solutions. Modalities like resistance bands, suspension trainers, and bodyweight-focused systems, though not traditional equipment, are vying for the same discretionary budget.

Segment Analysis

By Product Type: Cycles Gain on Treadmills' Dominant Share

Stationary cycles are projected to grow at a 4.98% CAGR from 2026 to 2031, surpassing the broader market's 4.67% growth. Their compact size and affordability attract first-time buyers, particularly in space-constrained urban apartments. Treadmills, contributing 33.42% of 2025's revenue, are popular for walking, jogging, and running. However, their 1.5 to 2.0 square-meter footprint and noise issues limit adoption in multi-family housing. Decathlon's January 2025 launch of the Compact Run 100 treadmill addresses these challenges with a foldable design, though its mass-market focus suggests price competition over advanced features. Rowing machines are gaining popularity for full-body cardio with minimal joint impact, with brands like Hydrow and WaterRower emphasizing natural resistance mechanisms. Elliptical machines, while offering low-impact motion for rehabilitation and older users, face limited market penetration due to their bulkier frames and higher price points.

In Nautilus Inc.'s final pre-bankruptcy quarter, strength training equipment, dumbbells, resistance bands, cable systems, and electromagnetic units like Tonal, which saw a 7.4% sales increase, contrasting with a 28.5% decline in cardio equipment sales. This shift highlights growing consumer interest in functional fitness and muscle preservation. Echelon's October 2024 launch of the Strength Home, priced at USD 2,999.99, targets this trend with a compact design and digital resistance range of 5 to 110 pounds. Other fitness products like yoga mats, foam rollers, and suspension trainers remain fragmented across specialty retailers and lack the recurring-revenue potential of connected equipment, relegating them to a supplementary role. The European Union's Ecodesign for Sustainable Products Regulation, effective September 2026, will mandate durability and reparability disclosures, favoring mechanical products like rowing machines and free weights over electronic treadmills and cycles, which face higher compliance costs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Smart Equipment Narrows Conventional's Lead

From 2026 to 2031, smart and connected equipment is projected to grow at a 6.80% CAGR, outpacing conventional variants by nearly 2 percentage points. Manufacturers are enhancing hardware with AI-driven coaching, biometric tracking, and gamified challenges, justifying premium pricing and recurring subscriptions. While conventional equipment captured 61.05% of 2025 revenue, appealing to cost-conscious buyers and subscription skeptics, its growth faces challenges from commoditization and thin margins. Technogym's Checkup platform, leveraging AI for movement assessments and corrective exercise prescriptions, drove an 11.3% year-on-year revenue surge to EUR 406.3 million (USD 440 million) in H1 2024, underscoring the value of software differentiation. Peloton's 2.9 million paid connected-fitness subscribers provide a recurring revenue buffer against hardware losses, yet a 1.6% year-on-year dip in Q1 fiscal 2025 revenue to USD 586 million signals a plateau in subscriber growth.

Smart equipment faces additional compliance costs due to the General Data Protection Regulation, with mid-sized firms incurring an annual burden of EUR 50,000 to EUR 200,000 (USD 54,000 to USD 216,000) for consent, encryption, and data localization mandates. This creates a competitive edge for incumbents with seasoned legal teams. Decathlon's April 2025 alliance with Freeletics, offering a 3-month complimentary subscription with equipment buys and aiming for over 100 co-branded products by end-2026, showcases mass-market retailers' strategy of tapping into the connected segment via content ecosystems. Tonal's January 2025 shift to a B2B approach, installing electromagnetic resistance units in hotels and physical-therapy centers, broadens its revenue avenues and mitigates subscription-churn hurdles. While conventional equipment's straightforwardness, free from firmware updates, cloud dependencies, and recurring fees, ensures its lasting appeal, the lack of usage analytics curtails manufacturers' potential for product design optimization and upselling services.

By End User: Female Segment Accelerates

Forecasts indicate that the female segment will expand at a 6.02% CAGR from 2026 to 2031, outpacing the male segment's more gradual growth. This shift comes as manufacturers roll out lower-impact modalities, personalized coaching, and community features, all of which align closely with women's fitness preferences. In 2025, male users represented a dominant 68.85% of revenue, a testament to their historical stronghold in strength training and high-intensity cardio. However, this dominance is waning as brands increasingly acknowledge the significant purchasing power of female consumers. Peloton, for instance, has tailored its content library with female instructors and cycling classes focused on prenatal and postnatal fitness. This strategy has successfully built a dedicated female subscriber base, even as Peloton's total subscriber count held steady at 2.9 million in Q1 fiscal 2025. Meanwhile, Echelon's Strength Home system, introduced in October 2024, starts with a digital resistance of 5 pounds, catering to beginners and those in rehabilitation, demographics that lean female.

Female buyers, drawn to rowing machines and stationary cycles for their cardiovascular benefits, prefer these options for full-body workouts without the bulkiness of heavy resistance training. Responding to this trend, Decathlon launched its Training Rower 900 and Training Bike 900 in January 2025, featuring sleek designs and competitive pricing against premium brands. The emergence of online fitness communities, be it Facebook groups, Instagram challenges, or Strava leaderboards, has underscored the importance of social accountability, a motivator that research highlights as particularly influential for female exercisers. Brands that weave community elements like live leaderboards and group challenges into their platforms are witnessing heightened engagement and reduced churn rates among female users. The male segment's tempered growth can be attributed to market saturation among early adopters and a prevailing preference for gym-based training, where the allure of heavy free weights and specialized machines outshines home alternatives.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Online Gains on Offline's Installed Base

Online retail stores are projected to grow at a 5.75% CAGR from 2026 to 2031, narrowing the gap with offline channels, which accounted for 52.35% of 2025 revenue. This shift is driven by direct-to-consumer brands bypassing traditional showrooms to boost margins and gather customer data. Offline retail outlets, including specialty fitness chains, department stores, and sporting goods shops, benefit from tactile product evaluation and instant fulfillment but face challenges like fixed costs and limited product assortments, reducing their competitiveness against digital-first brands. Peloton's May 2024 closure of its Chicago manufacturing facility and shift to contract manufacturing in Taiwan reflects a strategic move toward leaner, online-focused operations. Decathlon's January 2025 launch of 'Decathlon Pulse,' a mergers-and-acquisitions initiative, highlights its intent to acquire digital-first brands and integrate them into its omnichannel framework.

European e-commerce grew 2.1% in 2023, with fitness equipment sales outpacing others as consumers gained confidence in purchasing high-ticket items online after pandemic-era trials. White-glove delivery and in-home assembly have become essential for premium brands, as items like treadmills and rowing machines, weighing 100 to 150 kilograms, require technical setup, increasing delivery costs. Augmented-reality apps that visualize equipment in buyers' homes have reduced return rates, which previously reached 15% for large fitness items shipped via parcel carriers. Fitshop's October 2024 acquisition of Kettler and HOI brands from Trisport AG expanded its footprint to 67 branches across 9 European countries, with EUR 124 million (USD 134 million) in revenue. This move illustrates how omnichannel players are consolidating offline assets to complement online reach. The tension between online convenience and offline experience is driving hybrid models, where showrooms allow product trials but fulfill orders through central warehouses, balancing inventory efficiency with tactile engagement.

Geography Analysis

In 2025, Germany holds 27.20% of revenue, driven by a mature fitness culture with 11.7 million gym memberships and a EUR 5.88 billion (USD 6.4 billion) fitness market in 2023. High disposable income, strong e-commerce, and government wellness subsidies of up to EUR 600 (USD 650) per employee annually support demand. Technogym's H1 2024 revenue of EUR 406.3 million (USD 440 million), up 11.3% year-on-year, highlights growth in German-speaking markets with rising connected equipment adoption. Italy is projected to grow fastest at a 5.13% CAGR (2026–2031), driven by a younger workforce and obesity-focused health campaigns, as 1 in 3 children face obesity per the WHO's 2024 report. France sees steady mid-tier equipment demand, though subscription fatigue and urban space constraints limit growth.

The UK’s strong gym membership base in 2023 aligns with robust home-equipment sales, showing complementary usage. EGYM’s April 2024 acquisition of Hussle integrated 1,500 UK gyms into its Wellpass platform. Spain’s EUR 2.5 billion (USD 2.7 billion) fitness market and 5.6 million gym members in 2023 face lower disposable income challenges, but Basic-Fit’s March 2024 acquisition of RSG Spain, adding 42 clubs, signals long-term growth confidence. The Netherlands, Poland, Belgium, and Sweden, though smaller markets, show rising adoption due to increasing disposable incomes and e-commerce. Poland’s growing middle class and Belgium’s urbanization favor compact, budget-friendly equipment. Sweden’s EUR 120 (USD 130) per tonne CO₂ tax drives low-carbon material use and logistics optimization. The EU’s Ecodesign Regulation, effective September 2026, will mandate durability and reparability disclosures, pushing manufacturers to adapt or risk exclusion.

Smaller markets like Austria, Denmark, Finland, Ireland, and Portugal show varied demand influenced by income, housing, and fitness culture. Austria benefits from cross-border e-commerce with Germany. Denmark’s high income supports premium equipment, while Finland’s sauna culture favors complementary equipment. Ireland’s economic growth expands its market, though reliance on imports raises costs. Portugal’s lower income limits premium growth, but retailers like Decathlon gain share with budget options. Fragmentation complicates logistics, favoring omnichannel players with retail footprints.

Competitive Landscape

In the Europe home fitness equipment market, Technogym, Peloton, ICON Health & Fitness, Johnson Health Tech, and Nautilus Inc. are key players. However, no single entity dominates, leaving room for newcomers to innovate, especially those merging hardware with unique content or catering to overlooked segments. Technogym reported a robust H1 2024 revenue of EUR 406.3 million (USD 440 million), marking an 11.3% year-on-year increase. This success underscores its prowess in fostering connected ecosystems and nurturing ties with commercial gyms, bolstering its brand among home consumers. In a notable shift, Peloton closed its Chicago manufacturing in May 2024, laying off 400 employees. This move indicates a strategic transition from vertical integration to a leaner model, emphasizing online sales and subscription revenues over traditional hardware profits. Nautilus Inc. filed for Chapter 11 bankruptcy in March 2024, largely due to a 28.5% drop in cardio-equipment sales. The company accepted a USD 37.5 million stalking-horse bid from Johnson Health Tech, highlighting the industry's divide: brand strength and scale can determine success in a market with low consumer switching costs. Meanwhile, Decathlon, a mass-market retailer, is forging content alliances to rival premium brands. Its April 2025 deal with Freeletics aims for over 100 co-branded products by the close of 2026, all without the hefty investment in proprietary software.

New entrants are capitalizing on the subscription fatigue of established players. By integrating perpetual content libraries directly into hardware sales, they're eliminating recurring fees, making their offerings attractive to budget-conscious consumers. Tonal is diversifying its revenue approach. In January 2025, it shifted to a business-to-business model, placing its electromagnetic resistance units in hotels and physical therapy centers, thus avoiding the churn seen in direct consumer sales. The General Data Protection Regulation (GDPR) poses challenges for newcomers with its stringent consent, encryption, and data-localization rules. While these hurdles favor established players with robust legal and cloud infrastructures, they also present a chance for brands emphasizing on-device processing to reduce compliance costs.

The market is witnessing a wave of consolidation. Fitshop's October 2024 takeover of Kettler and HOI brands bolstered its presence to 67 branches in 9 European nations, raking in EUR 124 million (USD 134 million) in revenue. Similarly, LifeFit Group's March 2025 acquisition of FIT/One added 210 clubs in Germany and Austria, contributing an impressive EUR 245 million (USD 265 million) in last twelve months revenue. The focus is shifting from merely innovating hardware to creating an entire ecosystem. Brands that master content, cultivate community, and harness customer data stand to gain significantly, enjoying higher lifetime values and shielding themselves from market commoditization.

Europe Home Fitness Equipment Industry Leaders

Peloton Interactive, Inc.

Technogym S.p.A.

ICON Health & Fitness

Johnson Health Tech

Nautilus Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Decathlon and Freeletics announced a 5-year strategic partnership to co-develop 100-plus fitness products by end-2026, bundling a 3-month free Freeletics subscription with equipment purchases to compete against premium connected brands. The agreement targets corporate wellness programs and aims to integrate guided workouts seamlessly with Decathlon's mass-market hardware.

- March 2025: LifeFit Group acquired FIT/One, adding 210 clubs across Germany and Austria with EUR 245 million (USD 265 million) in LTM revenue, consolidating its position as a leading European gym operator and signaling confidence that home equipment will complement rather than cannibalize memberships.

- January 2025: Decathlon unveiled a new home gym range, including the Compact Run 100 treadmill, Training Rower 900, and Training Bike 900, emphasizing space-efficient designs to address urban housing constraints and targeting first-time buyers with mass-market pricing.

Europe Home Fitness Equipment Market Report Scope

Fitness equipment products like training benches, treadmills, stationary bicycles, and dumbbell sets, among others bought to perform an exercise at home, are altogether called home fitness equipment. Europe's home fitness equipment market is segmented by product type, distribution channel, and geography. By product type, the market studied is segmented into treadmills, elliptical machines, stationary cycles, rowing machines, strength training equipment, and other product types. By distribution channel, the market studied is segmented into offline retail stores, online retail stores, and direct selling. By geography, the report provides a detailed regional analysis, which includes Spain, the United Kingdom, Germany, Italy, France, Russia, and the rest of Europe. For each segment, the market sizing and forecasts have been done based on value (in USD million).

Product Type

| Treadmills |

| Elliptical Machines |

| Stationary Cycles |

| Rowing Machines |

| Strength Training Equipment |

| Other Product Types |

Category

| Conventional |

| Smart/Connected Equipment |

End User

| Male |

| Female |

Distribution Channel

| Offline Retail Stores |

| Online Retail Stores |

Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| Product Type | Treadmills |

| Elliptical Machines | |

| Stationary Cycles | |

| Rowing Machines | |

| Strength Training Equipment | |

| Other Product Types | |

| Category | Conventional |

| Smart/Connected Equipment | |

| End User | Male |

| Female | |

| Distribution Channel | Offline Retail Stores |

| Online Retail Stores | |

| Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the European home fitness equipment market in 2026?

The European home fitness equipment market size is USD 3.46 billion in 2026, with a forecast CAGR of 4.67% to 2031.

Which product category is growing fastest?

Smart and connected equipment posts the highest 6.80% CAGR, outpacing conventional hardware by almost two percentage points.

Which country contributes the largest revenue?

Germany leads with 27.20% of 2025 sales, supported by 11.7 million gym memberships and strong wellness subsidies.

What restrains adoption in urban areas?

Limited living space and noise constraints make bulky treadmills less attractive, shifting demand toward compact cycles and folding strength stations.

How are manufacturers tackling subscription fatigue?

Some vendors bundle perpetual content libraries with the hardware price, while others pair short free trials with discounted renewals to ease billing resistance.