Market Size of Europe Frozen Food Packaging Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

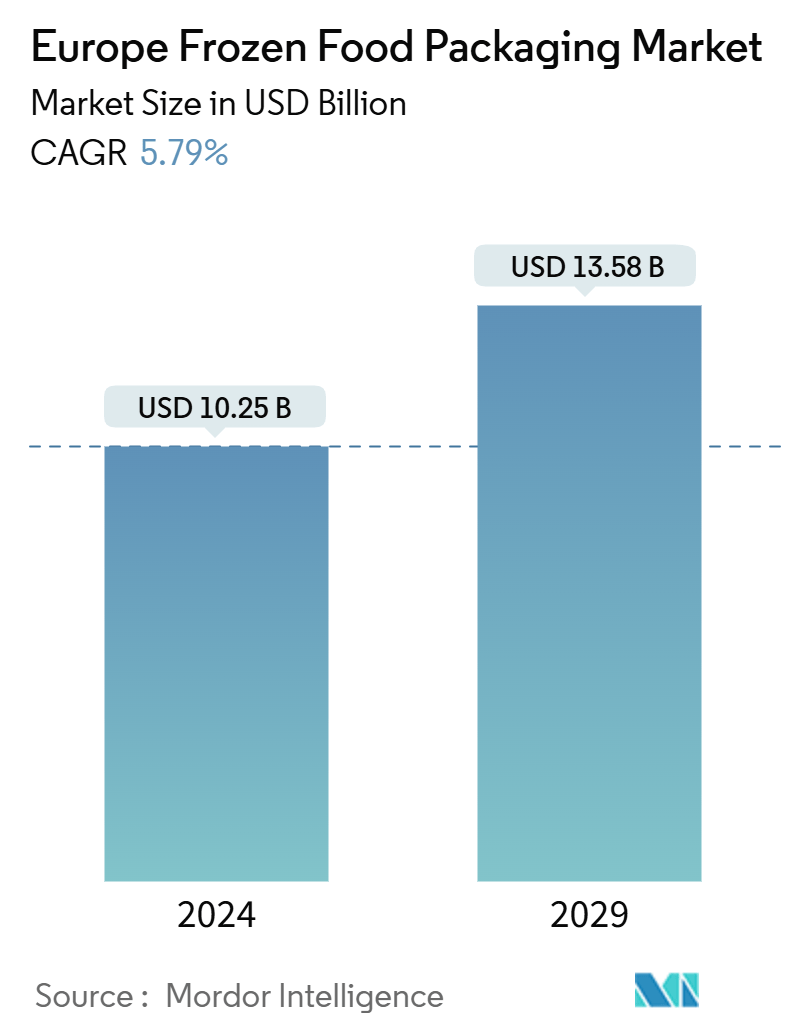

| Market Size (2024) | USD 10.25 Billion |

| Market Size (2029) | USD 13.58 Billion |

| CAGR (2024 - 2029) | 5.79 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Frozen Food Packaging Market Analysis

The Europe Frozen Food Packaging Market size is estimated at USD 10.25 billion in 2024, and is expected to reach USD 13.58 billion by 2029, at a CAGR of 5.79% during the forecast period (2024-2029).

The rapid growth of urbanization and fast-paced lifestyles have shifted consumers' preferences toward frozen food products, which require less time for cooking than traditional home-cooked meals.

- The rise in consumer expectations related to food quality has propelled the demand for frozen food packaging. Also, consumer appreciation of the product quality is another factor driving the market growth. Additionally, with changes in the economy and lifestyles, there is an increased demand for frozen food packaging in Europe. The market is expected to grow lucratively during the forecast period.

- New packaging technologies have also developed recently, making packaging for frozen food products more practical and secure. These technologies include intelligent packaging, active packaging, and engineering science. To reduce environmental pollution and comply with government regulations, companies focus on eco-friendly packaging by employing biodegradable packaging materials that can be recycled, regenerated, and reused.

- Furthermore, convenience is one of the primary factors driving the global increase in frozen food consumption. As a result, leading players are introducing new types and ingredients to cater to consumers' regional tastes. The growing consumer preference for convenience products fuels the increasing demand for frozen products due to their ease of preparation and time savings compared to cooking from scratch.

- Moreover, the frozen snacks food market is expanding rapidly due to the increasing volume of the hectic lifestyle of the working population, which is boosting the frozen snacks market and propelling the demand for the frozen food packaging market.

- However, the European market is anticipated to remain highly regulated, owing to stringent regulations regarding food packaging types and contact materials by agencies such as the European Commission. Frozen food packaging requires robust solutions to maintain food quality and safety across the supply chain by preventing contamination, moisture intrusion, and temperature fluctuations.

Europe Frozen Food Packaging Industry Segmentation

Frozen food packaging encompasses the materials and techniques to safeguard food products stored at freezing temperatures, ensuring their quality, safety, and longevity. This specialized packaging aims to thwart moisture loss, freezer burn, and contamination while maintaining the food's texture, flavor, and nutritional integrity. Commonly, plastics—be it films, trays, bags, or pouches are the go-to materials for frozen food packaging, offering robust barriers against air, light, and moisture. Beyond protection, this packaging prioritizes convenience and portability, aligning with consumer preferences for quick, ready-to-eat meals and snacks.

The Europe Frozen Food Packaging Market is segmented by material (glass, paper, metal, plastic, and other materials), by product (bags, boxes, tubs and cups, trays, pouches, and other product types), by type of food (readymade meals, fruit,s and vegetables, meat, seafood, baked goods and other food types), and by country (United Kingdom, Germany, France, Spain, Italy, Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Material Type | |

| Glass | |

| Paper | |

| Metal | |

| Plastic | |

| Others Material Type |

| By Product Type | |

| Bags | |

| Boxes | |

| Tubs and Cups | |

| Trays | |

| Pouches | |

| Other Product Types |

| By Type of Food | |

| Readymade Meals | |

| Fruits and Vegetables | |

| Meat | |

| Sea Food | |

| Baked Goods | |

| Others Food Types |

| By Country*** | |

| United Kingdom | |

| Germany | |

| France | |

| Spain | |

| Italy |

Europe Frozen Food Packaging Market Size Summary

The European frozen food packaging market is experiencing significant growth, driven by factors such as technological innovation, sustainability concerns, and the demand for customer-friendly packaging. The COVID-19 pandemic has further accelerated this demand due to increased hygiene and safety concerns. The market is characterized by the adoption of new packaging technologies, including active and intelligent packaging, which enhance product protection and extend shelf life. The rising consumer expectations for food quality, coupled with changing lifestyles and increased disposable income, are contributing to the market's expansion. However, the market faces challenges from stringent regulations imposed by the European Commission regarding food packaging materials and the slow growth of the packaged food sector.

The market is moderately fragmented, with several major players focusing on expanding their customer base internationally. Companies are investing in eco-friendly and recyclable packaging solutions to meet consumer preferences and regulatory requirements. The demand for frozen food packaging is particularly driven by millennials, who favor portable and convenient food options. The use of glass packaging is also notable, with a high recycling rate and positive consumer perception regarding its environmental benefits. Despite the challenges posed by the COVID-19 pandemic, the market holds significant growth potential, supported by ongoing investments in innovative packaging solutions and sustainable practices.

Europe Frozen Food Packaging Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Industry Attractiveness - Porter's Five Force Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Buyers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Overview of the Global Frozen Food Packaging Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Material Type

-

2.1.1 Glass

-

2.1.2 Paper

-

2.1.3 Metal

-

2.1.4 Plastic

-

2.1.5 Others Material Type

-

-

2.2 By Product Type

-

2.2.1 Bags

-

2.2.2 Boxes

-

2.2.3 Tubs and Cups

-

2.2.4 Trays

-

2.2.5 Pouches

-

2.2.6 Other Product Types

-

-

2.3 By Type of Food

-

2.3.1 Readymade Meals

-

2.3.2 Fruits and Vegetables

-

2.3.3 Meat

-

2.3.4 Sea Food

-

2.3.5 Baked Goods

-

2.3.6 Others Food Types

-

-

2.4 By Country***

-

2.4.1 United Kingdom

-

2.4.2 Germany

-

2.4.3 France

-

2.4.4 Spain

-

2.4.5 Italy

-

-

Europe Frozen Food Packaging Market Size FAQs

How big is the Europe Frozen Food Packaging Market?

The Europe Frozen Food Packaging Market size is expected to reach USD 10.25 billion in 2024 and grow at a CAGR of 5.79% to reach USD 13.58 billion by 2029.

What is the current Europe Frozen Food Packaging Market size?

In 2024, the Europe Frozen Food Packaging Market size is expected to reach USD 10.25 billion.