Market Size of Europe Food Packaging Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

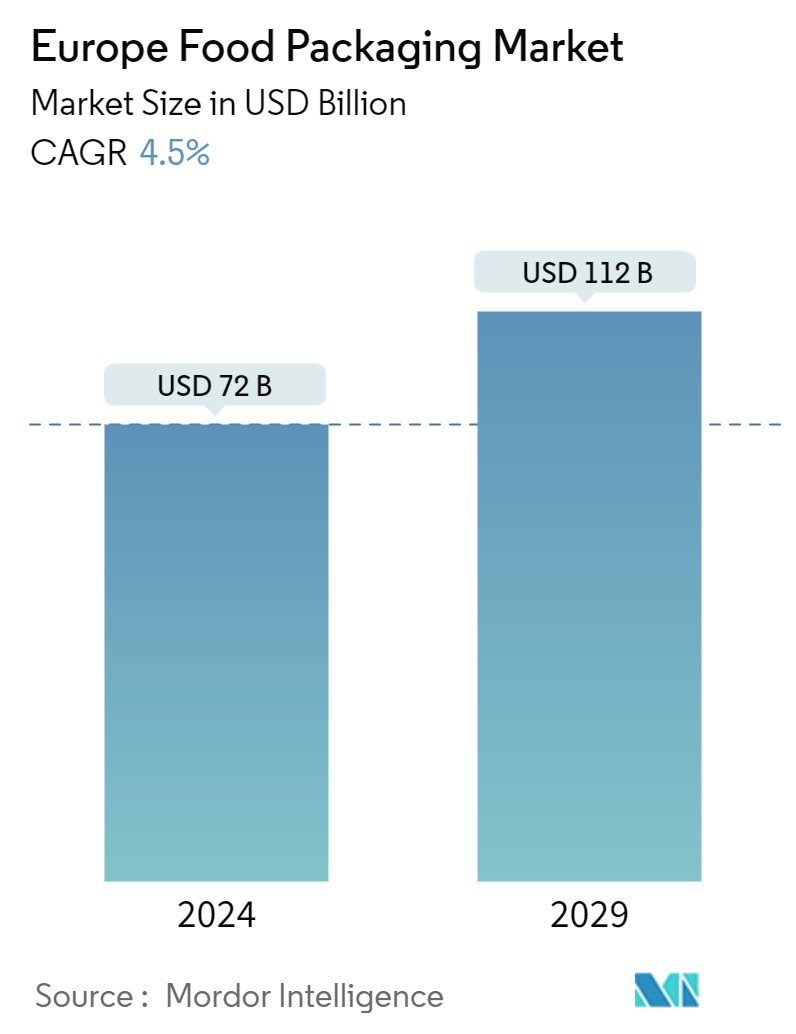

| Market Size (2024) | USD 72 Billion |

| Market Size (2029) | USD 112 Billion |

| CAGR (2024 - 2029) | 4.50 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Food Packaging Market Analysis

The Europe Food Packaging Market size is estimated at USD 72 billion in 2024, and is expected to reach USD 112 billion by 2029, growing at a CAGR of 4.5% during the forecast period (2024-2029).

- Packaging has evolved into a crucial component of everyday life. Its main function is to safeguard food items from external factors and potential harm while maintaining their freshness and flavor. Effective food packaging plays a vital role in preventing spoilage, preserving the advantages of processing, extending shelf life, and enhancing the quality and safety of food products. Innovations in food packaging have a profound influence on various aspects, including food logistics and preservation.

- Food packaging offers several essential advantages, including the mitigation of food contamination, the extension of food shelf-life, and enhanced operational efficiency. As urbanization continues to rise, there is an increasing demand for environmentally friendly packaging solutions and heightened consumer safety considerations, which are expected to drive market growth. Additionally, European nations have experienced robust demand for fresh fruits and vegetables, attributed to a shift toward organic options and the development of packaging that improves shelf life.

- The demand for sustainable packaging solutions across the region's food industry driven by government regulations is expected to drive innovations. In April 2024, the European Parliament approved new initiatives aimed at enhancing the sustainability of packaging and minimizing packaging waste across the European Union. The regulations, which received provisional agreement from the Council, established targets for packaging reduction of 5% by 2030, 10% by 2035, and 15% by 2040. Additionally, EU member states are mandated to specifically decrease the volume of plastic packaging waste. Starting from January 1, 2030, certain types of single-use plastic packaging will be prohibited, including packaging for unprocessed fresh fruits and vegetables, as well as packaging for food and beverages.

- The expansion of fresh food production, coupled with supportive government regulations, enhances the development of the fresh fruits and vegetables industry, subsequently propelling the growth of food packaging in the region. As reported by the CBI Ministry of Foreign Affairs, Europe represents a significant and stable market for a majority of fresh fruits and vegetables. The continuous demand for year-round availability and a diverse selection of produce sustains Europe's reliance on external suppliers. Annually, Europe imports approximately 55 million tonnes of fresh fruits and vegetables. Such factors are expected to drive the demand for suitable packaging solutions.

- The European Environmental Bureau reported that paper-based packaging constitutes the predominant source of packaging waste within the European Union. Furthermore, there is a growing trend in the use of paper-based materials for packaging food and beverages. The food and beverage industry accounts for over two-thirds of the overall packaging market in Europe. The European Parliament and the Council of the EU are evaluating a proposal from the European Commission for a new Packaging and Packaging Waste Regulation (PPWR), which aims to foster various innovations in the market.

- As consumers grow more aware of the significance of a balanced, plant-based diet, the demand for innovative packaging that enhances the shelf life and preserves the quality of fresh produce is increasing. In recent years, investment in European food start-ups has seen a substantial rise. The emergence of home delivery services across Europe considerably affected the food packaging market. The leading countries in Europe regarding platform-to-consumer revenue include the United Kingdom, Germany, France, Spain, and Italy, and this dominance is anticipated to stimulate the need for appropriate packaging solutions.

- Several vendors are also investing significantly to drive the packaging industry's capabilities in the region's food industry. In May 2024, twelve organizations within the European Union were awarded funding to investigate coatings for food packaging that do not contain PFAS. The ZeroF project is receiving co-funding from the Horizon Europe research investment program as well as from the Swiss State Secretariat for Education, Research and Innovation. Commonly referred to as "forever chemicals," PFAS are frequently utilized in coatings that enhance the resistance of food packaging to grease and moisture. Additionally, the rising investments aimed at enhancing food production capabilities across various countries in the region are anticipated to boost market growth.

- The volatility of raw material prices has the potential to hinder market expansion. As reported by European Plastics Converters, the European polymer market faced significant challenges for several months, with the adverse effects of raw material shortages and rising prices severely impacting the production of plastic products within the European Union. Moreover, the market is currently facing significant uncertainties regarding energy, largely attributable to the conflicts between Russia and Ukraine. These circumstances are leading to fluctuations in the supply and pricing of raw materials, as well as disruptions in transportation and logistics, which are exerting pressure on the profit margins of paper packaging manufacturers.

Europe Food Packaging Industry Segmentation

Food packaging refers to materials that enclose, protect, and preserve food products during transportation, storage, and sale. It serves various functions, including maintaining the freshness and quality of the food, expanding shelf life, preventing contamination, and providing important information such as mutational content and expiration dates.

The scope of the study focuses on the market analysis of food packaging in Europe, and market sizing encompasses food packaging product consumption across end-user industries. The study also tracks the key market parameters, underlying growth influencers, and revenue accrued from the market. The scope of the report encompasses market sizing and forecast for segmentation by material (plastic, paper & paperboard, metal, glass), product type (bottles & containers, cartons & pouches, cans, films & wraps, caps & closures), end-user type (fruits & vegetables, meat & poultry, dairy products, bakery & confectionary), and country. The market sizes and forecasts are provided in value (USD) for all the above segments.

| By Material Type | |

| Plastic | |

| Paper & Paperboard | |

| Metal | |

| Glass |

| By Product Type | |

| Bottles & Containers | |

| Cartons & Pouches | |

| Cans | |

| Films & Wraps | |

| Other Product Types |

| By End-user Type | |

| Fruits & Vegetables | |

| Meat & Poultry | |

| Dairy Products | |

| Bakery & Confectionary | |

| Other End-users (Sea Food, Convenience food,Snacks and Side Dishes) |

| By Geography | |

| United Kingdom | |

| Germany | |

| France | |

| Spain | |

| Rest of Europe |

Europe Food Packaging Market Size Summary

The European food packaging market is experiencing significant growth, driven by factors such as increasing urbanization, a shift towards organic food products, and a rising demand for eco-friendly packaging solutions. The market is characterized by its essential role in protecting food products from external influences, preserving freshness, and extending shelf life. This has led to advancements in packaging technologies that enhance food quality and safety. The regulatory framework in Europe supports the agricultural sector, further boosting the demand for fresh food packaging. However, challenges such as fluctuating raw material prices and energy uncertainties due to geopolitical tensions, like the Russia-Ukraine conflict, pose risks to market stability.

The market is also influenced by changing consumer behaviors, such as the rise of online food deliveries and take-outs, which increase the demand for diverse packaging solutions. The focus on sustainable and recyclable packaging is growing, with paper-based packaging gaining popularity due to its environmental benefits and practicality. The sector is witnessing investments and expansions, with companies like Amcor and Huhtamaki enhancing their production capabilities to meet the increasing demand. The market's fragmentation is evident with numerous players engaging in strategic activities like mergers and acquisitions to strengthen their market positions. Overall, the European food packaging market is poised for continued growth, driven by innovation, sustainability, and evolving consumer preferences.

Europe Food Packaging Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industrial Value/Supply Chain Analysis

-

1.3 Industry Attractiveness - Porter Five Forces

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Consumers/Buyers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Assessment of Microeconomic Factors on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Material Type

-

2.1.1 Plastic

-

2.1.2 Paper & Paperboard

-

2.1.3 Metal

-

2.1.4 Glass

-

-

2.2 By Product Type

-

2.2.1 Bottles & Containers

-

2.2.2 Cartons & Pouches

-

2.2.3 Cans

-

2.2.4 Films & Wraps

-

2.2.5 Other Product Types

-

-

2.3 By End-user Type

-

2.3.1 Fruits & Vegetables

-

2.3.2 Meat & Poultry

-

2.3.3 Dairy Products

-

2.3.4 Bakery & Confectionary

-

2.3.5 Other End-users (Sea Food, Convenience food,Snacks and Side Dishes)

-

-

2.4 By Geography

-

2.4.1 United Kingdom

-

2.4.2 Germany

-

2.4.3 France

-

2.4.4 Spain

-

2.4.5 Rest of Europe

-

-

Europe Food Packaging Market Size FAQs

How big is the Europe Food Packaging Market?

The Europe Food Packaging Market size is expected to reach USD 72 billion in 2024 and grow at a CAGR of 4.5% to reach USD 112 billion by 2029.

What is the current Europe Food Packaging Market size?

In 2024, the Europe Food Packaging Market size is expected to reach USD 72 billion.