Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

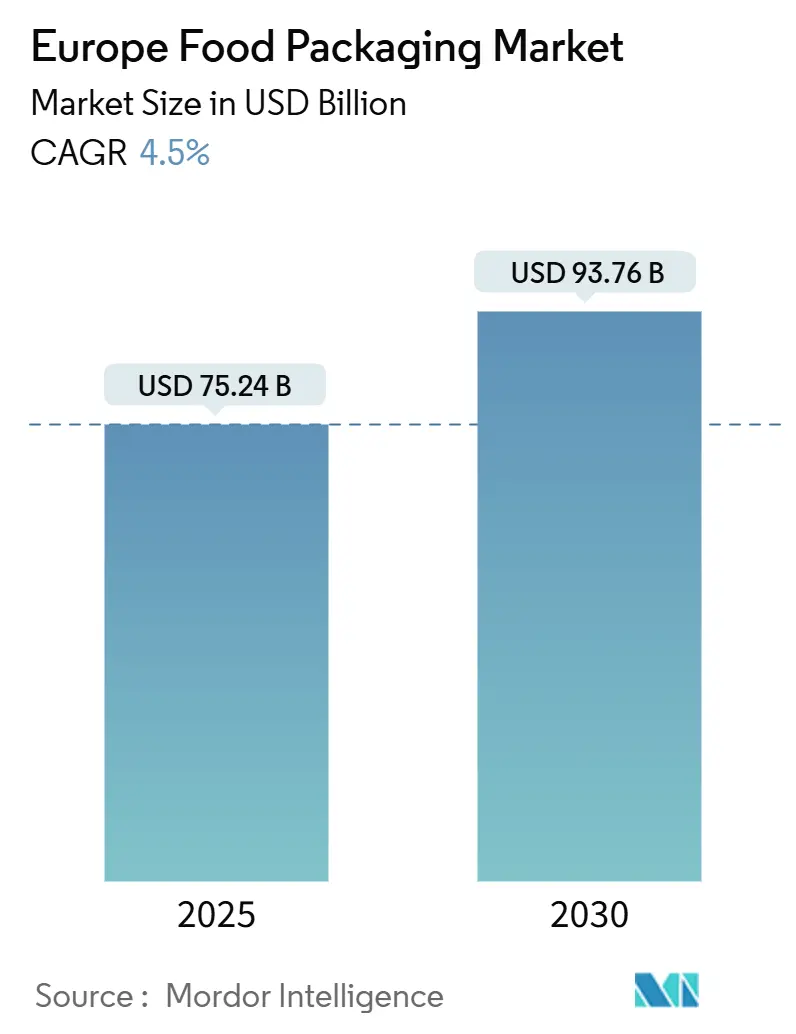

| Market Size (2025) | USD 75.24 Billion |

| Market Size (2030) | USD 93.76 Billion |

| Growth Rate (2025 - 2030) | 4.50% CAGR |

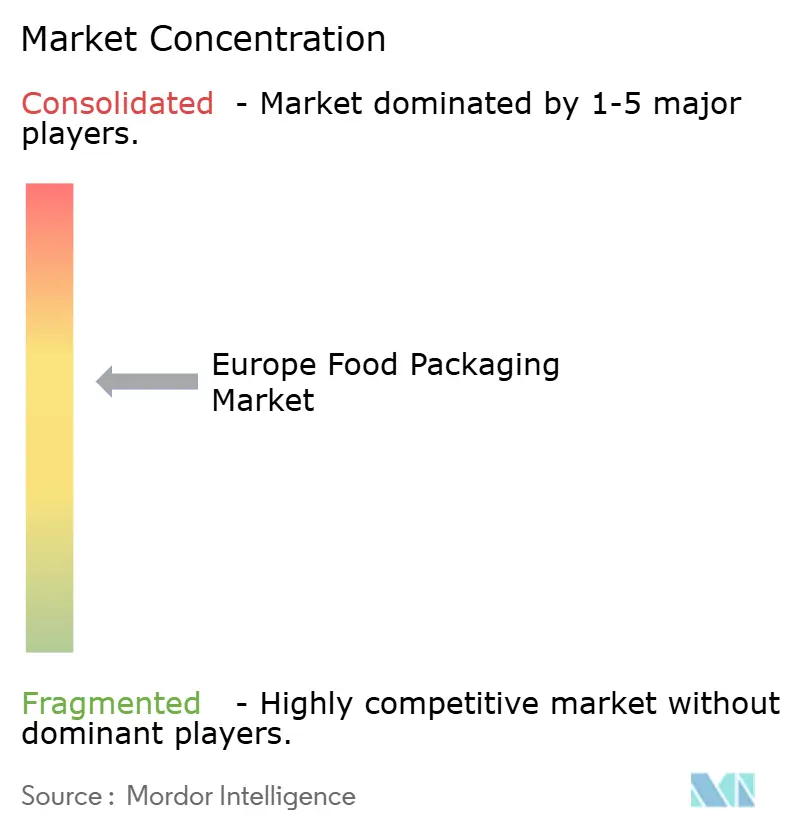

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Food Packaging Market Analysis by Mordor Intelligence

Europe food packaging market size stood at USD 75.24 billion in 2025 and is forecast to touch USD 93.76 billion by 2030, expanding at a 4.50% CAGR over 2025-2030. Robust demand for recyclable barrier materials, rising e-commerce grocery volumes, and a widening cold-chain footprint across Central and Eastern Europe are anchoring this trajectory. The EU Packaging and Packaging Waste Regulation (PPWR) is accelerating capital flows into recycling infrastructure and post-consumer resin (PCR) sourcing, allowing brand owners to meet the 30% recycled-content target for plastic beverage bottles by 2030.[1]European Commission, “Packaging and Packaging Waste,” europa.eu At the same time, rapid urbanization and smaller household sizes are spurring single-portion and convenience formats that rely on high-barrier films. Cold-chain expansion, exemplified by automated mega-warehouses in Poland and Hungary, is cementing demand for temperature-resistant packs that combine modified-atmosphere (MAP) and active-antimicrobial technologies. However, volatile polymer and aluminum prices continue to squeeze converters’ gross margins, encouraging vertical integration and recycled-content hedging strategies.

Key Report Takeaways

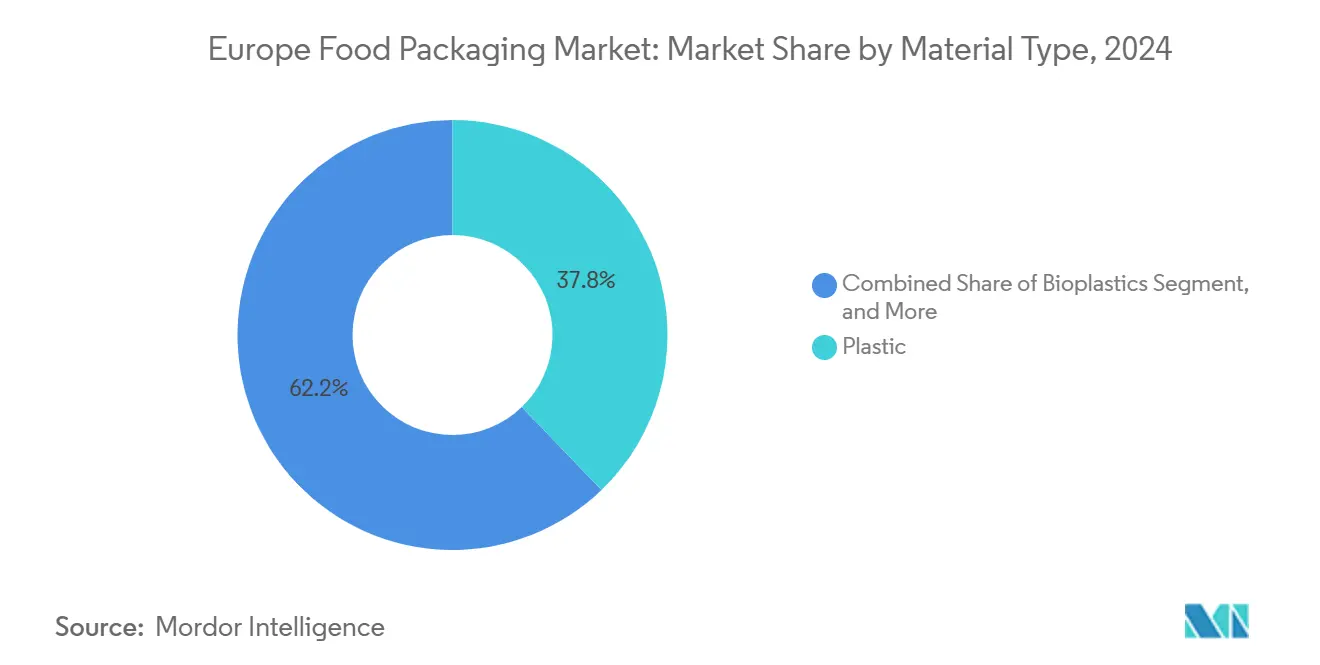

- By material, plastics retained 37.82% of Europe food packaging market share in 2024 while bioplastics are projected to post a 7.54% CAGR through 2030.

- By product type, bottles and containers held 31.22% revenue share of the Europe food packaging market size in 2024, whereas films and wraps are set to rise at a 6.65% CAGR to 2030.

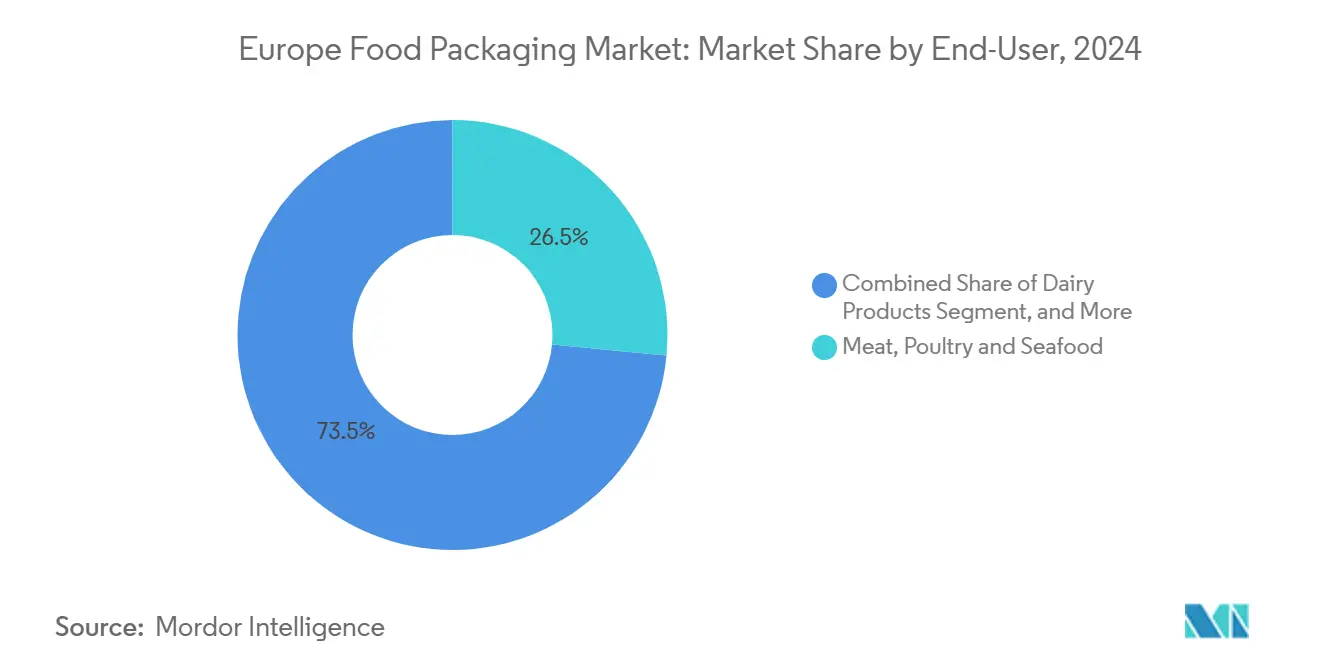

- By end-user, meat, poultry, and seafood applications led with 26.52% share of the Europe food packaging market size in 2024, while ready meals and convenience foods will accelerate at a 6.34% CAGR between 2025-2030.

- By packaging technology, modified-atmosphere systems commanded 28.92% of Europe food packaging market share in 2024; active and intelligent formats exhibit the fastest 7.88% CAGR through 2030.

- By country, Germany accounted for the largest national share in 2024, whereas Poland is predicted to log the highest mid-single-digit CAGR to 2030.

- Amcor, Mondi, Smurfit WestRock, Sealed Air, and Huhtamäki jointly controlled nearly 35% of 2024 revenue, reflecting a moderately consolidated landscape in Europe food packaging market.

Europe Food Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of food-service and take-away formats | +0.8% | Western Europe core, expanding to CEE | Short term (≤ 2 years) |

| E-commerce grocery boom accelerating secondary packaging demand | +0.7% | Germany, UK, France lead, spreading EU-wide | Medium term (2-4 years) |

| EU food-safety rules boosting high-barrier solutions | +0.6% | EU-27 uniform application | Long term (≥ 4 years) |

| Sustainability push toward recyclable and paper-based formats | +0.9% | Nordic countries lead, EU-wide adoption | Medium term (2-4 years) |

| Cold-chain expansion in CEE heightening demand for temperature-resistant packs | +0.5% | Poland, Hungary, Czech Republic focus | Medium term (2-4 years) |

| Demographic shift toward smaller households driving single-portion packs | +0.4% | Germany, Netherlands, Denmark highest impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid growth of food-service and take-away formats

Take-away meals jumped 28% year over year in Germany during 2024, powered by platform aggregators and workplace mobility shifts. Operators seek multi-compartment and leakproof packs that remain compliant with the Single-Use Plastics (SUP) Directive’s reuse stipulations. Reusable container schemes, despite incurring operating costs 15-20% higher than disposables, are rolling out in quick-service chains to mitigate levy exposure. Packaging suppliers are responding with dishwasher-durable PP and molded-fiber solutions fitted with scannable tracking codes for reverse logistics. For small independents, hybrid paper-plastic packs that achieve recyclability without dishwashing present a pragmatic bridge solution. Demand concentration remains strongest in the top-25 EU cities, yet smaller Central European capitals are posting double-digit volume growth, indicating wider market penetration ahead.

E-commerce grocery boom accelerating secondary packaging demand

Online grocery penetration hit 8.3% of European food retail in 2024, reshaping packaging specifications for ship-to-home fulfillment. Temperature swings during last-mile delivery require insulation liners and moisture barriers that traditional shelf-ready packs never encountered. Flexible films with integrated air pouches now dominate fresh produce shipments because they offer protective cushioning at one-tenth the grammage of rigid plastics, trimming freight weight and carbon score alike. Grocers simultaneously wrestle with the PPWR’s source-reduction targets, prompting pack-design algorithms that cut void space by 12-15% per parcel. Reverse logistics for ice packs and insulation is emerging as a service niche for logistics firms in Germany and the Netherlands. As cold-chain parcel density rises, packaging converters positioned with rapid-response prototyping and mixed-material competence are winning multi-year supply contracts.

EU food-safety rules boosting high-barrier solutions

EFSA cleared 23 new active-packaging substances in 2024, widening the toolbox for oxygen, ethylene, and moisture scavengers that stretch shelf life by up to 40% in high-protein foods. Retailers are mandating these high-barrier packs to minimize markdowns from spoilage as inventory transit times lengthen inside regional distribution hubs. Advanced metallized PET and EVOH co-extrusions now appear routinely in chilled ready meals and premium cheeses. Breadth of adoption, however, varies by price segment; discount grocers favor simpler MAP while premium chains absorb the incremental 3-5 ¢ per pack for active layers. Compliance verification is tightening, requiring converters to supply migration test data under EU Regulation 10/2011. Companies with in-house barrier-film extrusion and analytical labs thus gain a speed-to-market edge.

Sustainability push toward recyclable and paper-based formats

Paperboard recycling already exceeds 75% across the bloc, but upcoming PPWR amendments seek 85% by 2030, catalyzing adoption of aqueous-coated fiber wraps for dry snacks and confectionery. Nordic mills have commercialized dispersion-barrier cartons that tolerate light oils, unlocking cereals and frozen bakery niches formerly served by PE-lined solutions. Nevertheless, moisture-sensitive applications still rely on ultra-thin PE or bio-based PLA tie layers, complicating fiber recovery. R&D labs are piloting enzymatic delamination to detach coatings at pulp plants, an advance that could lower recycling yields’ energy footprint by 8-10%. Large brands are publicly committing to “design for fiber” roadmaps to align with forthcoming extended producer responsibility (EPR) modulated fees that reward mono-material designs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polymer and aluminium feedstock prices | -0.9% | Global impact, EU manufacturing concentrated | Short term (≤ 2 years) |

| EU Single-Use Plastics (SUP) Directive compliance costs | -0.7% | EU-27 uniform application | Medium term (2-4 years) |

| Skilled-labour shortages in packaging-machinery operations | -0.4% | Germany, Netherlands highest impact | Long term (≥ 4 years) |

| Climate-linked uncertainty in bioplastic feedstock supply | -0.3% | Southern Europe agricultural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile polymer and aluminum feedstock prices

Virgin LDPE and PP contract prices swung 15-20% quarter-to-quarter through 2024, tied to energy cost spikes and Middle-East cracker turnarounds, eroding converters’ margin visibility. Aluminum ingot rose 18% over H1 2024 before retreating in Q3, compelling can-sheet rollers to renegotiate annual supply agreements. Mid-tier converters with limited hedging facilities are adopting dual-sourcing strategies and raising PCR content to buffer fluctuations. Nonetheless, recycled resin trades at a 10-15% premium to virgin in high-purity grades, limiting immediate savings. Film extruders are experimenting with mass-balance PP blends that permit incremental PCR incorporation without sacrificing seal integrity, aiming to protect brand owners from future cost shocks.

EU Single-Use Plastics Directive compliance costs

The SUP Directive’s widened product list now covers certain lids, caps, and stirrers, forcing SMEs to divert EUR 2 million (USD 2.314 million ) per plant toward tooling conversion and certification, according to industry association. Tooling lead times of up to 10 months prolong revenue disruption, nudging family-owned converters to consider strategic alliances or outright exits. National transpositions vary: France enforces a deposit on take-away cups; Germany imposes mandatory reusable options for outlets exceeding 80 m². Such divergence adds layer-on-layer complexity for pan-European food-service chains that standardize SKUs. Early-mover converters specializing in molded fiber or reusable PP lines report order backlogs extending into 2026, underscoring a supply-demand mismatch that will linger through the compliance horizon.

Segment Analysis

By Material Type: Bioplastics Scale Yet Battle Feedstock Risk

Plastic retained a 37.82% stake in Europe food packaging market share in 2024, supported by entrenched extrusion assets and continuously improving PCR streams. Bioplastics, while only a mid-single-digit slice of Europe food packaging market size, will post the highest 7.54% CAGR thanks to regulatory credits and retailer carbon pledges. The spread of closed-loop recycling hubs has stabilized rPET and rHDPE supply, enabling converters to hit 30% PCR thresholds without mechanical-property penalties. In parallel, fiber-based packs upgraded with water-borne dispersion coatings are cannibalizing thin-wall PP yogurt cups, reflecting advances that narrow the moisture barrier gap.

Growth prospects for bioplastics hinge on overcoming agricultural supply shocks and certification fragmentation. Southern Europe drought episodes curbed PLA resin output by low single digits in 2024, awakening interest in non-crop-based PHA and bacterial-cellulose films. Producers are lobbying for a harmonized “compostable at home” mark to reassure consumers and unlock municipal collection scale. Should EU Eco-design rules grant higher EPR rebates to compostables, the delta between bio- and petro-based solutions could compress, accelerating substitution.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Films and Wraps Leverage E-Grocery Logistics

Bottles and containers commanded 31.22% of 2024 revenue, anchored by beverage and dairy stalwarts. Films and wraps, however, will outpace all formats at 6.65% CAGR as they underpin the protective secondary layer demanded by online grocery fulfilment. Retailers favor multi-layer PE-PA structures that pair puncture resistance with peel-and-reseal convenience, elevating customer unboxing satisfaction scores. Trays and lids are evolving into mono-PET platforms to harvest recycle-ready credentials, while caps and closures integrate tethered designs to meet SUP rules and curb litter.

Advanced films adopting antimicrobial or antioxidant additives are migrating from premium meats into mainstream produce, extending shelf life by up to 5 days and shrinking shrinkage rates. Lightweighted shrink films allow pallet stabilization with 15% less material, contributing to PPWR reduction mandates. As corrugated e-commerce boxes slim down, wrapped primary packs shoulder greater cushioning duties, reinforcing the indispensability of flexible materials.

By End-User: Convenience Lifestyles Fuel Ready-Meal Momentum

Meat, poultry, and seafood preserved their 26.52% lion’s share of Europe food packaging market size in 2024, underpinned by stringent cold-chain standards and protein popularity. Yet ready meals and convenience foods will expand fastest at 6.34% CAGR as time-pressed urban consumers swap scratch cooking for microwaveable dishes. MAP trays blended with PP-EVOH maintain integrity through dual-oven cycles, delivering shelf life above 10 days without additives. Dairy packaging, historically rigid, is adopting thin-wall thermoformed PET pots paired with snap-fit paperboard over-sleeves to signal eco-wins without compromising mechanical protection.

Portion-controlled snack kits serving one to two people deliver premium per-gram margins and foster repeat purchases. Modified-atmosphere adoption in sushi and salads jumped double digits in 2024, evidencing retailers’ appetite for high-margin fresh aisles that depend on airtight, clear-barrier PET lidding. Government food-loss targets are reinforcing this shift by promoting pack formats that align quantity with consumption behavior.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Packaging Technology: Active and Intelligent Converge Around Shelf-Life

Modified-atmosphere technology remained the top choice with 28.92% revenue share in 2024 owing to its broad applicability and proven ROI. Europe food packaging market size for active and intelligent formats, though smaller, is forecast to clock the tallest 7.88% CAGR as EFSA clears new oxygen scavengers and smart ink sensors. QR-code freshness indicators printed in-line enable distributors to triage near-expiry stock in real time, cutting waste and bolstering ESG metrics. Aseptic filling retains a stronghold in beverages and soups but faces cost pressure from ambient-stable retort pouches that slash logistics energy by eliminating chilled storage.

Vacuum skin packaging (VSP) continues to gain in premium red meat, delivering enhanced visual appeal while providing leakproof presentation. Edible films made from whey protein or seaweed derivatives are entering pilot trials for cheese slices and snack bars, foreshadowing a dissipation of the pack itself into consumable form over the long haul.

Geography Analysis

Germany accounted for the largest national slice of Europe food packaging market in 2024, benefiting from a mature recycling infrastructure that achieved a 67% packaging recovery rate. Domestic converters leverage dual systems and deposit schemes to secure steady PCR feedstock, buffering virgin-resin price shocks. France maintains leadership in premium and AOC-certified foods, driving sophisticated barrier requirements, particularly in wine, cheese, and pâtisserie categories. Italy’s flex-pack specialists are pioneering low-solvent gravure inks that reduce VOC emissions, aligning with stringent Lombardy air-quality ordinances.

The United Kingdom’s post-Brexit deviation from EU rules offers an experimental sandbox where graphene-enhanced barrier films gained regulatory clearance in late 2024, granting early-mover rights to local innovators. Spain’s fruit-export corridors rely heavily on MAP liners to reach Scandinavian buyers, underpinning a healthy replacement cycle for vented crates and breathable bags.

Central and Eastern Europe represent the fastest-climbing sub-region: Poland alone is projected to outpace the continental average by 150 basis points as supermarkets scale and frozen food exports proliferate.[2]NewCold, “Automated Cold Storage Facility Poland,” newcold.comHungary and Czechia mirror this upswing, propelled by tax incentives for cold-storage investment. Nordic countries, meanwhile, register the highest per-capita use of fiber-based packs, with Sweden and Finland recording 85% collection rates for paper packaging in 2024. Tabularizing these contrasts shows a continent of micro-markets, each demanding tailored compliance, material, and branding strategies.

Competitive Landscape

The market is moderately consolidated: the top five players Amcor, Mondi, Smurfit WestRock, Sealed Air, and Huhtamäki collectively controlled around 35% revenue in 2024, a level that grants scale purchasing power yet leaves white-space for nimble regional firms. Amcor’s USD 55 million buyout of Moda Systems brought digital-printing agility suitable for micro-runs and personalized SKUs, a core demand in direct-to-consumer food channels.[3]Amcor, “Amcor Acquires Moda Systems,” amcor.com Smurfit WestRock’s 2024 merger forged the world’s largest corrugated supplier, enabling cross-Atlantic know-how transfer in lightweight containerboard.

Sustainability credentials are a competitive battleground. Huhtamäki’s EUR 45 million (USD 52.04 million) fiber-molding expansion caters to quick-service chains coping with SUP restrictions on EPS and PS. Sealed Air’s launch of antimicrobial pouches, cleared by EFSA, extended red-meat shelf life by up to 40%, winning supply contracts with pan-EU retailers. Mid-cap innovators specializing in mono-material laminates and enzymatic de-inking report double-digit growth and are prime acquisition targets as incumbents bolster technology stacks.

Patent filings for active packaging climbed 28% in 2024, signaling ongoing R&D dynamism despite margin pressure. Players unable to finance innovation are forming joint ventures with academia to share risk while keeping a foot in premium niches. Overall, competition blends scale efficiency, regulatory fluency, and sustainability positioning.

Europe Food Packaging Industry Leaders

Amcor plc

Mondi plc

Smurfit WestRock

Tetra Laval International S.A.

Huhtamäki Oyj

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Smurfit WestRock finalized its merger, yielding USD 8.5 billion in combined European sales and reinforcing corrugated capacity for e-commerce.

- October 2024: Amcor acquired Moda Systems, integrating digital presses that slash changeover time and ink waste.

- August 2024: Sealed Air unveiled an active-antimicrobial pouch range in Europe, gaining EFSA nod for beef and poultry applications.

- July 2024: Constantia Flexibles won a European Packaging Award for its recycle-ready barrier laminate used in cheese blocks.

Europe Food Packaging Market Report Scope

The scope of the study focuses on the market analysis of food packaging in Europe, and market sizing encompasses food packaging product consumption across end-user industries. The study also tracks the key market parameters, underlying growth influencers, and revenue accrued from the market. The scope of the report encompasses market sizing and forecast for segmentation by material (plastic, glass), product type (bottles & containers, cartons & pouches, cans, films & wraps, caps & closures), end-user type (fruits & vegetables, meat & poultry, dairy products, bakery & confectionary), and country. The market sizes and forecasts are provided in value (USD) for all the above segments.

By Material Type

| Plastic |

| Paper and Paperboard |

| Metal |

| Glass |

| Bioplastics |

By Product Type

| Bottles and Containers |

| Cartons and Pouches |

| Cans |

| Films and Wraps |

| Trays, Caps and Closures |

By End-user

| Fruits and Vegetables |

| Meat, Poultry and Seafood |

| Dairy Products |

| Bakery and Confectionery |

| Ready Meals and Convenience Food |

By Packaging Technology

| Modified-Atmosphere Packaging (MAP) |

| Aseptic Packaging |

| Vacuum Skin Packaging |

| Active and Intelligent Packaging |

| Edible and Biodegradable Films |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Material Type | Plastic |

| Paper and Paperboard | |

| Metal | |

| Glass | |

| Bioplastics | |

| By Product Type | Bottles and Containers |

| Cartons and Pouches | |

| Cans | |

| Films and Wraps | |

| Trays, Caps and Closures | |

| By End-user | Fruits and Vegetables |

| Meat, Poultry and Seafood | |

| Dairy Products | |

| Bakery and Confectionery | |

| Ready Meals and Convenience Food | |

| By Packaging Technology | Modified-Atmosphere Packaging (MAP) |

| Aseptic Packaging | |

| Vacuum Skin Packaging | |

| Active and Intelligent Packaging | |

| Edible and Biodegradable Films | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Europe food packaging market in 2025?

It is valued at USD 75.24 billion and is projected to reach USD 93.76 billion by 2030.

What CAGR is expected for Europe’s food packaging between 2025 and 2030?

The market is forecast to grow at 4.50% annually during the period.

Which packaging material grows fastest in Europe?

Bioplastics lead with a 7.54% CAGR, propelled by regulatory incentives and brand sustainability goals.

Why are films and wraps gaining popularity?

E-commerce grocery expansion requires lightweight, protective secondary packaging, boosting films and wraps at a 6.65% CAGR.

Which technology shows highest growth momentum?

Active and intelligent packaging systems are advancing at 7.88% CAGR due to stricter food-safety and shelf-life demands.

What key regulation shapes packaging strategies in Europe?

The EU Packaging and Packaging Waste Regulation mandates 30% recycled content in plastic bottles by 2030 and tightens recyclability criteria across all formats.