Europe Food Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

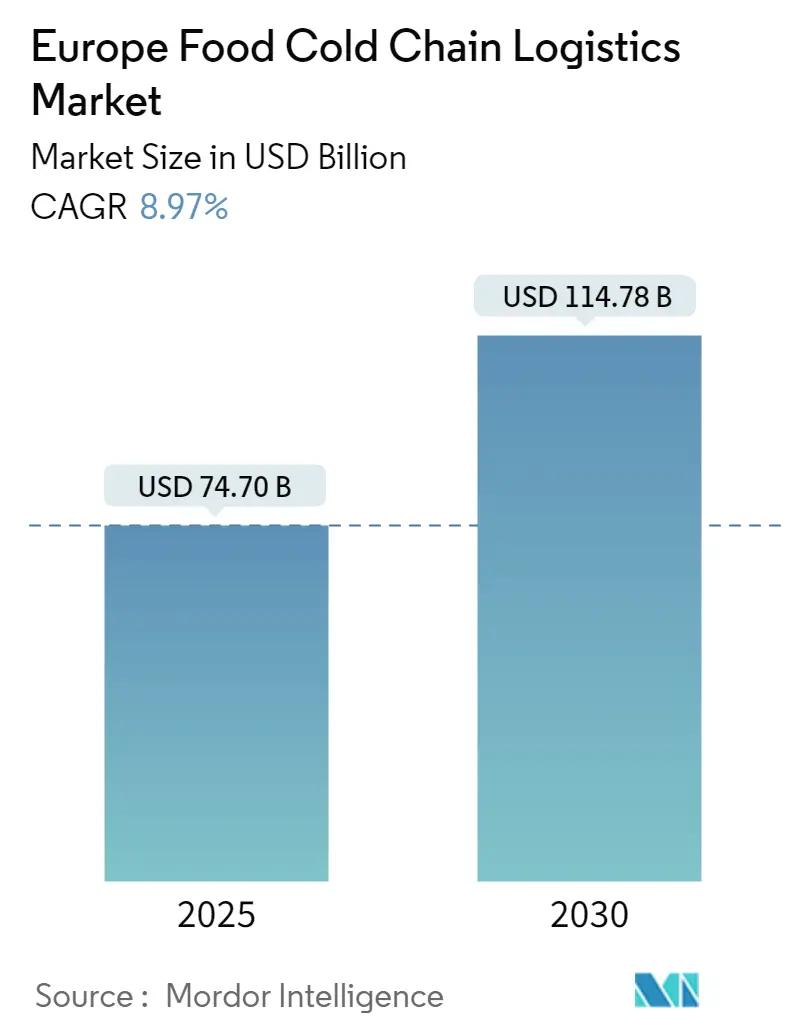

| Market Size (2025) | USD 74.70 Billion |

| Market Size (2030) | USD 114.78 Billion |

| Growth Rate (2025 - 2030) | 8.97% CAGR |

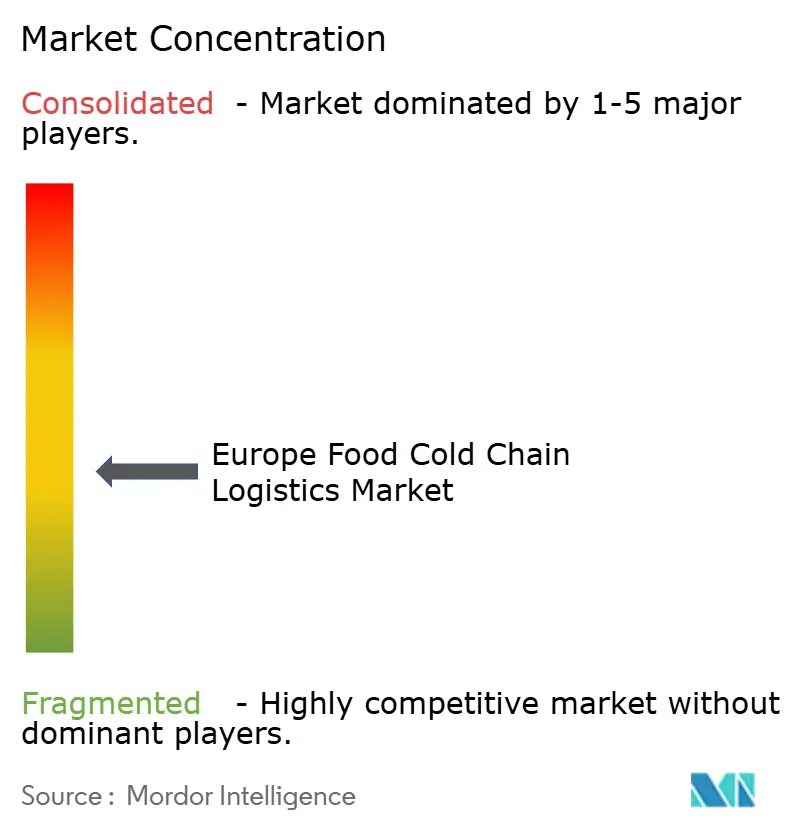

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Food Cold Chain Logistics Market Analysis by Mordor Intelligence

The Europe Food Cold Chain Logistics Market size is estimated at USD 74.70 billion in 2025, and is expected to reach USD 114.78 billion by 2030, at a CAGR of 8.97% during the forecast period (2025-2030).

This sustained growth mirrors a region-wide overhaul of grocery fulfilment models that place temperature-controlled capacity closer to urban shoppers. Regulatory pressure from the EU Green Deal hastens the switch to natural refrigerants, raising capital needs yet lowering lifecycle emissions for compliant operators. Persistent Brexit-related customs checks create new demand for cross-docking hubs at ports such as Calais and Rotterdam, while rising e-commerce volumes compress delivery windows and favour micro-fulfilment centres with multi-temperature zones. Consolidation among pan-European specialists accelerates as private equity groups fund network build-outs, but structural driver shortages and energy price volatility inflate operating costs and test margins.

Key Report Takeaways

- By product type, Frozen Meat & Poultry led with 31.4% of the Europe food cold chain logistics market share in 2024; Ready Meals & Others is projected to expand at a 9.1% CAGR through 2030.

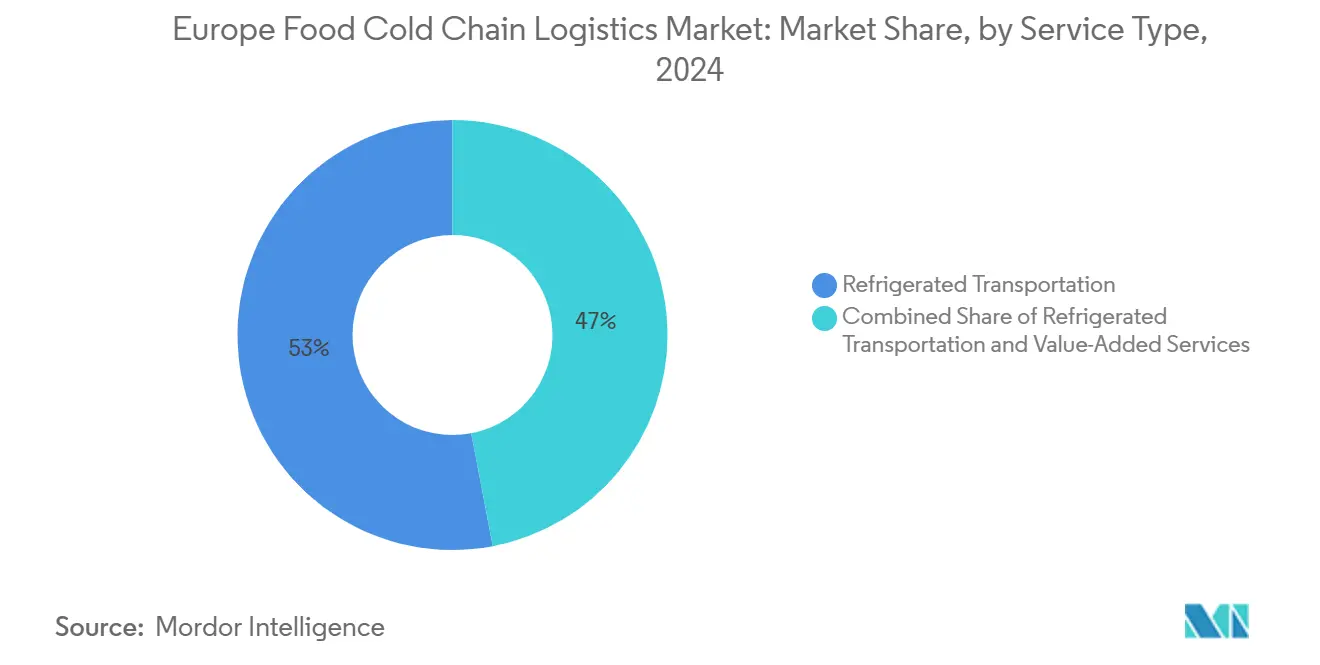

- By service type, Refrigerated Transportation held 53% revenue share of the Europe food cold chain logistics market in 2024, while Value-Added Services records the fastest growth at 8.8% CAGR to 2030.

- By temperature type, the Frozen category accounted for 60.5% share of the Europe food cold chain logistics market size in 2024; the Ambient category is set to rise at a 9.4% CAGR over 2025-2030.

- By geography, Germany remained the region’s primary hub in 2024, while Poland posted the strongest growth momentum among Eastern European markets.

Europe Food Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Europe-wide shift toward omni-channel grocery distribution networks | +2.1% | Western Europe, expanding eastward | Medium term (2-4 years) |

| Mandatory EU Green Deal targets accelerating adoption of natural refrigerants | +1.3% | EU-wide, strongest in Northern Europe | Long term (≥ 4 years) |

| Rapid capacity additions in Iberian Peninsula driven by agri-food export growth | +1.0% | Spain, Portugal | Medium term (2-4 years) |

| Surge in demand for ultra-low-temperature storage for plant-based meat analogues | +0.5% | UK, Germany, Nordics, Netherlands | Short term (≤ 2 years) |

| Post-Brexit customs friction boosting demand for cross-docking cold hubs | +0.9% | UK, France, Netherlands, Belgium | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Europe-wide Shift Toward Omni-Channel Grocery Distribution Networks

European grocers scale click-and-collect and rapid-delivery models that replace single mega-warehouses with dense clusters of micro-fulfilment hubs positioned near city centres. Operators respond by deploying modular buildings with frozen, chilled and ambient zones under one roof, supported by advanced energy-management software that balances refrigeration loads against power-price signals. Robotics adoption in Denmark illustrates the push toward automated pallet handling that compresses order-to-ship cycles without expanding headcount. Success now hinges on securing scarce urban real estate and integrating Internet-of-Things (IoT) sensors that certify temperature compliance in near real time. As these distributed networks mature, third-party logistics providers differentiate through data-driven route optimisation that protects product integrity during same-day deliveries.

Mandatory EU Green Deal Targets Accelerating Natural Refrigerant Adoption

The F-gas phasedown forces warehouse owners to retire high-GWP refrigerants and redesign systems for ammonia or CO₂. Initial capital intensity is high, yet operators report lower electricity use once regenerative heat reclaim and variable-speed compressors are in place. The ICCEE programme illustrates industry commitment by targeting 118 GWh of annual primary-energy savings and EUR 64 million of related investments. Larger companies absorb the expense by refinancing on green-bond markets, while smaller firms face merger pressure as compliance deadlines approach. A scarcity of engineers experienced with natural refrigerants adds wage inflation to project budgets but also seeds a specialised labour pool that bolsters long-run technical resilience.

Rapid Capacity Additions in Iberian Peninsula Driven by Export Growth

Spain and Portugal invest in ripening chambers and multi-temperature depots that preserve produce harvested during Northern Europe’s winter. New rail links from Almería to Rotterdam lower emissions per tonne-kilometre and tap demand from retailers seeking low-carbon supply chains. Solar-powered refrigeration arrays cut daytime grid draw and deliver operating-cost advantages against central European peers. Controlled-atmosphere rooms extend shelf life for berries and stone fruit, allowing Iberian exporters to command premium prices in Scandinavian supermarkets. These regional strengths encourage domestic third-party logistics firms to partner with multinational retailers intent on year-round assortment diversification.

Surge in Demand for Ultra-Low-Temperature Storage for Plant-Based Alternatives

Plant-based meat firms specify –23 °C to –25 °C storage, deeper than traditional frozen ranges. Beyond Burger’s life-cycle study shows refrigerated transport contributes 40% of total warming impact, spotlighting energy efficiency as a reputational risk. Operators carve out dedicated chambers within existing buildings and add doors with higher insulation values to limit thermal ingress during frequent pick-faces. Innovation extends to phase-change pallets that stabilise core temperature during cross-dock transfers and to dual-refrigerant trailers that flex between –25 °C and –18 °C routes. Analysts forecast 25 million t of plant protein demand by 2030, catalysing USD 27 billion of upstream capital projects and anchoring long-term ultra-low-temperature throughput.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continental driver shortage inflating refrigerated road freight spot rates | −1.4% | Pan-European, most severe in Eastern Europe | Medium term (2-4 years) |

| High CAPEX for F-gas phasedown compliance across legacy facilities | −0.8% | EU-wide, highest impact in Southern Europe | Medium term (2-4 years) |

| Power-price volatility in Germany & Italy squeezing 3PL margins | −0.6% | Germany, Italy | Short term (≤ 2 years) |

| Limited availability of Class-A refrigerated warehouse sites near Tier-1 ports (Felixstowe, Antwerp, Hamburg) | −0.5% | UK, Belgium, Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Continental Driver Shortage Inflating Transportation Costs

Europe faces 745,000 unfilled truck-driver slots by 2028, equal to 17% of required capacity. The talent pipeline falters as only 5% of current drivers are under 25 and cross-border routes carry extra administrative burden. IRU data notes 426,000 vacant positions already, pushing wages up and forcing shippers to book capacity weeks earlier than before. Spot-rate premiums on refrigerated lanes have widened relative to ambient lanes due to specialised licence needs and stricter rest-period rules. Modal shift to rail garners interest, yet cold-capable wagons and intermodal plugs are scarce, delaying large-scale migration and keeping road costs elevated.

High CAPEX for F-Gas Phasedown Compliance

EU Regulation 517/2014 tightens quota allocations for high-GWP refrigerants, compelling owners of ageing R-404A or R-507 systems to retrofit or rebuild. Energy now ranks as the second-largest cost item after labour, and although prices have eased since the 2022 spike they remain structurally higher than earlier in the decade. Southern European depots endure efficiency losses because high ambient temperatures erode natural-refrigerant performance, prompting investment in auxiliary adiabatic cooling and variable-speed drives. Studies show 30-40% power savings achievable through comprehensive upgrades, but payback periods stretch when electricity tariffs fluctuate. Mid-sized operators weigh phased refurbishment against outright facility replacement, with financing availability shaping long-term competitiveness.

Segment Analysis

By Product Type: Convenience Formats Reshape Category Priorities

The Europe food cold chain logistics market size for Frozen Meat & Poultry reached the equivalent of 31.4% share in 2024 and remains the largest revenue contributor despite slower incremental growth. Ready Meals & Others posts the highest 9.1% CAGR to 2030, propelled by dual-income households that value heat-and-eat foods compatible with shorter mealtimes. Fish & Seafood maintains resilient demand as aquaculture output scales and retailers promote omega-3 benefits, while Dairy & Ice-cream bookings continue to follow stable consumption patterns tied to established retail promotions. In fruits and vegetables, year-round supply strategies extend cold-chain penetration into previously seasonal categories, stimulating uptake of ethylene-control sachets that preserve freshness during long-haul moves.

Flash-freezing techniques in the Bakery & Confectionery segment allow centralised par-bake production shipped at −18 °C and finished on-site, shifting volume away from daily chilled deliveries. Flash-heat preservation trials for meat products indicate shelf-stable windows of up to 5 days, hinting at future attenuation of cold-chain reliance in selected cuts. Plant-based SKUs, which often blend protein isolates with functional fats, introduce atypical thermal profiles that force operators to recalibrate storage zoning within multi-use chambers. As consumer preferences evolve, agile 3PLs able to match niche temperature regimes widen their service revenue bases across converging product groups.

Note: Segment shares of all individual segments available upon report purchase

By Service Type: Ancillary Offerings Unlock Margin Expansion

Refrigerated Transportation represented 53% of total 2024 revenues in the Europe food cold chain logistics market, underpinned by dense road networks and high outbound frequency demanded by modern grocery retailers. Value-Added Services, including pick-and-pack, blast-freezing, labelling and quality control, deliver the fastest 8.8% CAGR and reposition warehouses as active fulfilment nodes rather than static holding points. Within transport, road commands a 76% modal share, but rail advances at 6.4% CAGR as green-house-gas accounting pushes shippers toward combined transport solutions. Manufacturers adopt the SWS Powerbox to energise containers on rail wagons, mitigating spoilage risk over long corridors[1]SWS Powerbox, “Rail-Powered Reefer Solution,” SWS Powerbox, swspowerbox.com. Airfreight retains a niche for ultra-perishable berries or premium seafood, whereas short-sea movements link Mediterranean producers to island consumers via Ro-Ro vessels fitted with plug-in reefer decks.

For operators, value-added layers defend margins against commoditised storage rates. Services such as product re-work in bonded facilities minimise duty payments on rejected imports, while light manufacturing—dicing vegetables or portioning protein—binds clients through integrated contracts. Digital portals offering real-time inventory visibility and blockchain-validated temperature logs further embed 3PLs within customers’ quality-assurance workflows, creating switching barriers and fostering multi-year engagements.

Note: Segment shares of all individual segments available upon report purchase

By Temperature Type: Ambient Gains Traction Yet Frozen Holds Core Volume

The frozen band (−18 °C to 0 °C) held 60.5% of the Europe food cold chain logistics market share in 2024, anchored by meat, seafood and ice-cream staples. Nevertheless, ambient solutions, powered by retort processing, aseptic filling and high-pressure pasteurisation, register a brisk 9.4% CAGR that reduces reliance on energy-heavy refrigeration. Ready-meals producers reformulate sauces and starch matrices to remain shelf-stable for nine months at 15 °C, enabling distribution through conventional dry channels and freeing consumer freezer space.

Chilled flows (0 °C to 5 °C) grow steadily as retailers expand ranges of ultra-fresh lines with premium positioning. Research shows micro-freezing extends beef freshness to 18 days compared with 4-6 days under standard chilling, prompting some processors to integrate intermittent freeze-thaw cycles that blend microbiological safety with desirable texture retention. EFSA studies on controlled ageing corroborate that microbial loads can be managed within regulatory limits, encouraging adoption of fine-tuned maturation rooms[2]European Food Safety Authority, “Guidance on Meat Ageing,” EFSA Journal, efsa.europa.eu. As technology advances, product developers weigh trade-offs among shelf life, sensory appeal, energy use and packaging waste—choices that ultimately steer volume flows across the three temperature brackets.

Geography Analysis

Germany anchors the Europe food cold chain logistics market with expansive highway and rail corridors that funnel north-south citrus imports and east-west dairy exports. The country’s early embrace of natural refrigerants yields operating-cost savings that compound over time, while Lineage’s new Bremerhaven site adds 40,000 pallet positions with direct quay access that bolsters seaborne integration. Rail-connected depots around Hamburg and the Ruhr accelerate modal shift efforts and chip away at road congestion, aligning with national climate targets. German manufacturers also champion advanced warehouse-management software that synchronises inbound raw-material deliveries with just-in-time production schedules to curtail dwell time.

The United Kingdom remains pivotal despite its smaller landmass because of high grocery e-commerce penetration and elevated automation rates that compensate for post-Brexit labour gaps. Calais-linked buffer facilities manage customs clearance delays, and London-centric micro-fulfilment centres shorten delivery radii for meal-kit providers. UPS’s acquisition of Frigo-Trans and BPL reinforces healthcare cold-chain capabilities, signalling crossover between pharmaceutical and food networks that share temperature-verification standards. Duplicate regulatory frameworks raise administrative overhead, yet early adopters of blockchain traceability convert compliance into marketing claims around provenance and safety.

Southern and Eastern Europe chart divergent but complementary trajectories. France straddles Iberian produce flows to Northern consumers, pairing mature infrastructure in the north with capacity-build programmes around Marseille and Toulouse. Italy’s operators grapple with power-price volatility and therefore fast-track rooftop solar and chilled-water storage to buffer tariff swings. Spain invests heavily in multi-temperature nodes that leverage abundant solar irradiation for cost-effective cooling, providing a launchpad for winter fruit exports. Poland posts the region’s highest growth rate as EUR 252 billion (USD ) of cumulative FDI underwrites modern depots serving cross-border supermarket formats; logistics employment rose 24.6% in 2024 while national unemployment held at 3.0%, securing a robust labour pipeline[3]European Commission, “Foreign Direct Investment Statistics,” Eurostat, ec.europa.eu.

Competitive Landscape

The Europe food cold chain logistics market shows a barbell structure: pan-European giants on one end and local specialists on the other. DSV’s EUR 14.3 billion (approx. USD 16.55 billion) Schenker takeover pushes the Danish firm into the global top tier and is projected to unlock DKK 9.0 billion (approx. USD 1.3 billion) in annual synergies by 2028 through network rationalisation and procurement scale. EQT’s acquisition of Constellation Cold Logistics demonstrates private-equity appetite for asset-heavy platforms that offer stable cash yields and ESG-aligned upgrade potential. Kuehne + Nagel’s EUR 350 million spend in Mantova plus the purchase of Transporte y Distribución Nacional deepens its Southern and Central European footprint, signalling a pivot toward origin-country value-added services that embed the 3PL earlier in the supply chain.

Technology shapes competitive edges. Blockchain-anchored IoT ecosystems document every temperature reading, door open and location ping, reducing insurance premiums and bolstering recall readiness. Predictive maintenance software minimises compressor downtime, while AI-based slotting engines improve pick-face turnover in multi-SKU chambers. Energy-management systems that orchestrate refrigeration duty cycles against hourly grid tariffs trim utility bills by double digits and unlock value beyond simple kilowatt savings.

Regional specialists defend turf through bespoke services—such as seafood ripening in Galicia or halal meat consolidation in the Netherlands—that multinationals find hard to replicate without local talent. Yet fragmented players risk margin squeeze when negotiating power contracts or vehicle procurement, nudging them toward cooperative buying groups or eventual sale. Over the forecast window, capital-intensive sustainability mandates will likely widen capability gaps, favouring well-funded networks able to amortise large-scale upgrades across multi-country portfolios.

Europe Food Cold Chain Logistics Industry Leaders

STEF SA

Americold Logistics, LLC (AGRO Merchants Europe)

DHL Supply Chain (Deutsche Post DHL Group)

Kuehne + Nagel International AG

NewCold Advanced Cold Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kuehne + Nagel acquired Transporte y Distribución Nacional for an undisclosed amount, enhancing its logistics capabilities in the European cold chain segment as part of its strategic expansion strategy.

- May 2025: NewCold opened a USD 275 million cold storage warehouse in Hagerstown, Maryland, marking significant expansion in North American operations while continuing European growth initiatives.

- April 2025: DSV completed the acquisition of Schenker for EUR 14.3 billion (approx. USD 16.55 billion), creating a world-leading logistics player with expected annual synergies of DKK 9.0 billion (approx. USD 1.3 billion) by 2028 and significantly enhanced European road freight capabilities.

- March 2025: Americold announced the acquisition of a Houston warehouse for approximately USD 127 million, adding 35,700 pallet positions to support a major grocery retailer contract and enhance retail segment presence.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe food cold chain logistics market as the revenue earned from transporting and warehousing edible products that must remain chilled (0 - 5 °C) or frozen (-18 - 0 °C) while moving across road, rail, sea, air, and third-party storage networks. According to Mordor Intelligence, this market is valued at about USD 74.70 billion in 2025 and is projected to reach roughly USD 114.78 billion by 2030.

Scope Exclusions: The assessment omits temperature-controlled flows linked to pharmaceuticals, fine chemicals, or any non-food merchandise.

Segmentation Overview

- By Product Type

- Frozen Meat & Poultry

- Fish & Seafood

- Dairy & Ice-cream

- Fruits & Vegetables

- Bakery & Confectionery

- Ready Meals & Others

- By Service Type

- Refrigerated Storage

- Refrigerated Transportation

- Road

- Rail

- Sea

- Air

- Value-Added Services

- By Temperature Type

- Chilled (0–5 °C)

- Frozen (-18–0 °C)

- Ambient

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Nordics

- Poland

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cold-store managers, refrigerated truck operators, grocery e-commerce planners, and food exporters across Germany, Spain, Poland, and the Nordics. These discussions clarified utilization rates, pallet rents, and seasonal surcharges, enabling us to reconcile desk findings with lived realities.

Desk Research

We start by capturing baseline tonnage, trade, and price signals from public datasets, Eurostat Comext codes for agri-food trade, EU Green Deal compliance filings, Transfrigoroute warehouse capacity bulletins, and national road-freight cost indices. Company 10-Ks, prospectuses, and fleet presentations sharpen service-mix splits, while news archives on Dow Jones Factiva and shipment counts sourced through Volza help validate volume flows.

Next, we mine peer-reviewed journals on post-harvest losses, patent families via Questel that flag refrigeration upgrades, and customs duty receipts to triangulate cross-border demand. This list is illustrative; many other references supported data collection, validation, and clarification.

Market-Sizing & Forecasting

We build the baseline through a top-down reconstruction of perishables produced, imported, and exported within Europe. We then corroborate totals with sampled ASP × volume roll-ups from large 3PLs. Key variables, per-capita frozen-food spend, intra-EU HS-02 trade tonnage, diesel spot prices, added cubic-meter cold storage, and online grocery penetration, feed multivariate regressions, complemented by scenario analysis to stress-test energy-price shocks. Bottom-up gaps are filled using density multipliers derived from primary calls.

Data Validation & Update Cycle

Outputs pass anomaly checks against warehouse utilization, FX shifts, and macro indicators, followed by peer review and senior sign-off. Models refresh annually, with interim updates when material events such as F-gas regulation changes or freight strikes occur.

Why Our Europe Food Cold Chain Logistics Baseline Commands Reliability

Published estimates often diverge because firms blend food with pharma, lock in static price decks, or postpone refreshes for years.

Other publicly available numbers range from USD 64.10 billion (2022) to USD 105.50 billion (2024).

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 74.70 B (2025) | Mordor Intelligence | - |

| USD 68.57 B (2024) | Regional Consultancy A | Narrower product list; model updated less frequently |

| USD 64.10 B (2022) | Trade Journal B | Includes pharmaceuticals; uses historic FX rates |

| USD 105.50 B (2024) | Global Consultancy C | Bundles food, pharma, and chemicals, inflating base value |

The comparison shows that by isolating only edible goods, refreshing inputs yearly, and flexing price assumptions within transparent scenarios, Mordor Intelligence offers a balanced, traceable baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the Europe food cold chain logistics market and its forecast growth?

The market is valued at USD 74.70 billion in 2025 and is projected to reach USD 114.78 billion by 2030, registering an 8.97% CAGR.

Which product segment is expanding the quickest in Europe’s food cold chain?

Ready Meals & Others leads with a 9.1% CAGR through 2030, outpacing Frozen Meat & Poultry.

How do EU Green Deal rules affect investment decisions for cold chain operators?

Mandatory natural-refrigerant adoption raises upfront capital needs but delivers long-term energy savings and compliance benefits.

What impact does the truck-driver shortage have on refrigerated transport costs?

With 745,000 positions forecast to remain unfilled by 2028, spot rates for temperature-controlled road freight continue to rise.

Why are ambient solutions gaining share against frozen storage in Europe?

Advances in aseptic processing and high-barrier packaging allow more foods to travel at room temperature, cutting energy use and costs.

Which European country is expected to post the fastest cold chain logistics growth by 2030?

Poland shows the highest momentum, supported by EUR 252 billion of cumulative FDI and expanding modern warehouse capacity.