Europe Fluoropolymer Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

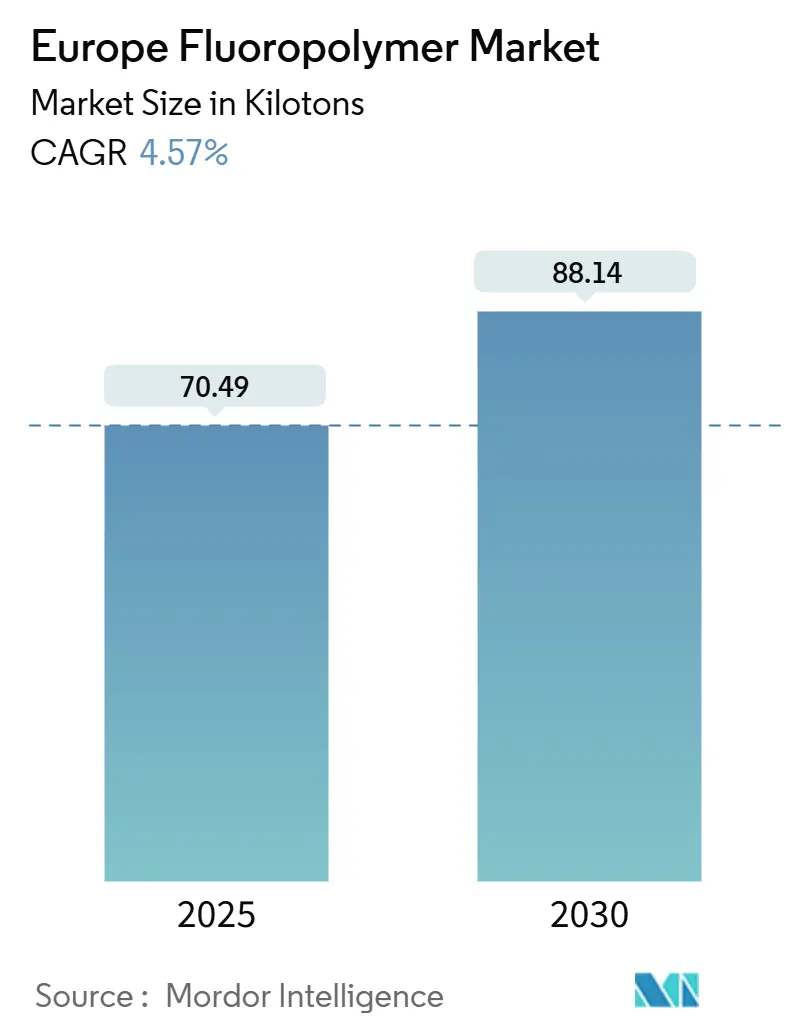

| Market Volume (2025) | 70.49 kilotons |

| Market Volume (2030) | 88.14 kilotons |

| Growth Rate (2025 - 2030) | 4.57% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Fluoropolymer Market Analysis by Mordor Intelligence

The Europe Fluoropolymer Market size is estimated at 70.49 kilotons in 2025, and is expected to reach 88.14 kilotons by 2030, at a CAGR of 4.57% during the forecast period (2025-2030). The Europe fluoropolymer market is gaining volume from electric-vehicle batteries, green-hydrogen electrolyzers, and 5G infrastructure, even as PFAS regulations tighten across the region. Demand resilience stems from the material’s unmatched chemical inertness, dielectric stability, and wide service temperature range, which are indispensable in automotive fuel systems, semiconductor tools, and renewable energy equipment. Producers continue to shift portfolios toward PVDF, FEP, and ETFE grades that qualify for essential-use exemptions, while securing alternative synthesis routes to cut emissions. Supply risk, however, persists because fluorspar feedstock availability remains volatile and because the European Chemicals Agency’s broad PFAS definition may slow permitting for new capacity. Competitive dynamics favor vertically integrated suppliers that can cross-license technology, back-integrate into raw materials, and co-develop next-generation solutions with Tier-1 end-users.

Key Report Takeaways

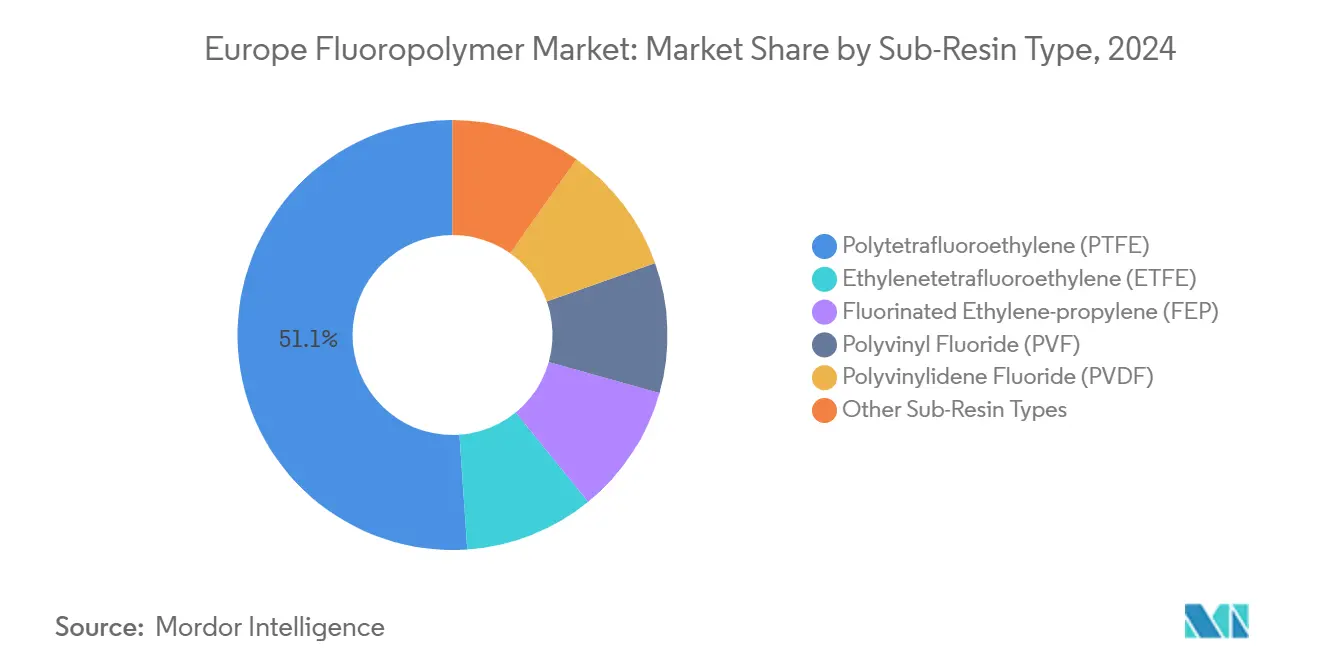

- By sub-resin, Polytetrafluoroethylene (PTFE) led with 51.10% of the Europe Fluoropolymer market share in 2024, while Polyvinylidene Fluoride (PVDF) is projected to post the fastest 8.89% CAGR through 2030.

- By end-user industry, industrial and machinery applications accounted for 56.10% of the Europe Fluoropolymer market size in 2024; automotive is advancing at an 8.86% CAGR to 2030.

- By geography, Germany held 24.31% revenue share of the Europe Fluoropolymer market in 2024; France is forecast to expand at a 6.53% CAGR through 2030.

Europe Fluoropolymer Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU auto-emission norms propel PTFE use in fuel systems | +1.2% | Germany, France, Italy | Medium term (2-4 years) |

| PVDF binders gain share in EV Li-ion batteries | +1.8% | Germany, France, Nordic regions | Long term (≥ 4 years) |

| 5G roll-out lifts FEP/PTFE in high-frequency cables | +0.9% | Germany, UK, France | Short term (≤ 2 years) |

| Aerospace lightweighting boosts ETFE/FEP wire insulation | +0.6% | France, Germany, UK | Medium term (2-4 years) |

| Green-hydrogen electrolyzers need PVDF/PFA gaskets | +0.7% | Germany, Netherlands, Nordic regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Auto-Emission Norms Propel PTFE Use in Fuel Systems

Euro 7 regulations mandate lower evaporative losses, spurring automakers to specify PTFE-lined hoses, gaskets, and vapor-control components that withstand biofuels and hydrogen blends. German OEMs adopt these parts to reduce warranty claims, while commercial-vehicle makers target longer service intervals. The Europe Fluoropolymer market benefits because PTFE meets permeability, temperature, and chemical-resistance thresholds that alternative elastomers cannot match[1]Chemours, “Applications of PTFE and PVDF in Automotive and Battery Markets,” chemours.com.

PVDF Binders Gain Share in EV Li-ion Batteries

European gigafactories require high-purity PVDF to bind cathode powders without compromising energy density or cycle life. Battery-grade PVDF commands premium pricing as manufacturers minimize the presence of trace metals that can trigger capacity fade. The France-based Nafion expansion assures local supply, and German cell makers secure multi-year contracts to hedge against Asian sourcing risks. The Europe Fluoropolymer market thus captures outsized growth from mobility electrification.

5G Roll-out Lifts FEP/PTFE in High-Frequency Cables

Telecom operators installing 28 GHz links favor FEP and PTFE dielectrics to curb insertion loss and moisture ingress. Cable makers leverage FEP’s processability for thin-wall extrusion, while PTFE remains the low-loss benchmark in critical antenna feed lines. Rapid deployment cycles unlock retrofit demand as legacy 4G sites are upgraded, allowing the Europe Fluoropolymer market to diversify beyond traditional industrial segments.

Aerospace Lightweighting Boosts ETFE/FEP Wire Insulation

Airbus and its supply chain are pursuing mass reductions in wiring harnesses, which directly translate into fuel savings. ETFE and FEP enable thinner insulation walls without sacrificing cut-through or flame resistance. Radiation stability is another advantage for high-altitude avionics cabling. As next-generation aircraft incorporate more electric subsystems, fluoropolymer-insulated wires proliferate across airframes, sustaining volume growth for the Europe Fluoropolymer market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PFAS regulatory clampdown across EU | -1.4% | EU-wide, notably Germany and Netherlands | Medium term (2-4 years) |

| Volatile fluorspar feedstock prices | -0.8% | Global supply chain, affects EU producers | Short term (≤ 2 years) |

| EU fluorine-gas supply tightness | -0.6% | Germany, France, Italy production centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PFAS Regulatory Clampdown Across EU

The proposed universal PFAS restriction forces manufacturers to assess substance authorizations, reformulate products, and invest in abatement technology. Compliance costs rise as analytical testing protocols become stricter. Some member states introduce accelerated timelines, increasing uncertainty for investment decisions. Although essential-use exemptions remain on the table, the Europe Fluoropolymer market must navigate a patchwork of national measures that could dampen near-term demand[2]European Chemicals Agency, “Universal PFAS Restriction Proposal,” echa.europa.eu.

Volatile Fluorspar Feedstock Prices

Supply disruptions in China and logistical bottlenecks in Mexico led to a more than 5% increase in fluorspar prices in late 2024. European converters, dependent on imports, absorbed margin pressure because downstream buyers resisted pass-through pricing. Inventories rose, tying up working capital and reducing production flexibility. Persistent volatility threatens capacity-utilization rates across the Europe Fluoropolymer market.

Segment Analysis

By Sub-Resin Type: PTFE Dominance Faces PVDF Challenge

PTFE held 51.10% of the Europe Fluoropolymer market share in 2024, underscoring its entrenched role in chemical-processing gaskets, semiconductor wet benches, and high-temperature seals. PVDF, however, is recording an 8.89% CAGR, driven by cathode-binder demand in European battery plants as they gear up for a combined output of more than 400 GWh by 2030. The Europe Fluoropolymer market size for PVDF is forecast to widen as green hydrogen electrolyzers and photovoltaic backsheets also specify the resin. FEP maintains steady cable and wire insulation volumes, while ETFE, valued for mechanical toughness, expands in aerospace wiring harnesses and architectural membranes.

Regulatory pressure diverges the outlook: PTFE producers invest in emissions-capture systems to safeguard essential-use exemptions, whereas PVDF gains positive visibility amid battery-chain incentives. Specialty copolymers address niche needs in the semiconductor and aerospace industries where conventional grades fall short. European formulators also explore melt-processable resins with partial fluorination chemistry to reduce the overall PFAS load. Such innovations buttress the Europe Fluoropolymer market against substitution risk while aligning with climate and circular-economy objectives.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Industrial Machinery Leads Amid Automotive Surge

Industrial and machinery applications accounted for 56.10% of the Europe Fluoropolymer market size in 2024 thanks to entrenched usage in pump linings, valve seats and semiconductor fabrication tools. Many of these uses fall under essential-service classifications, insulating them from blanket PFAS bans. Automotive demand, however, is growing fastest at an 8.86% CAGR as Euro 7 fuel-system parts, EV battery modules and power-electronics cooling circuits all specify fluoropolymers. That trajectory is pivotal because unit volumes are high and OEM homologation cycles lock in material choices for multiple model years.

Aerospace volumes fluctuate with build rates but remain strategically important for high-margin applications, such as wire insulation and sealing rings. Building and construction usage faces restrictions on architectural membranes in exterior facades, yet chemical-resistant coatings for industrial roofs continue to gain traction. Electronics uses benefit from advanced packaging and 5G antenna upgrades, while flexible-packaging volumes shrink following the EU ban on PFAS food-contact coatings. Overall, diverse demand pillars support the Europe Fluoropolymer market even as some legacy outlets contract.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Germany anchors the Europe Fluoropolymer market with a 24.31% share in 2024, underpinned by its automotive OEM base, chemical complexes along the Rhine, and world-class semiconductor fabs. German producers leverage co-location advantages to supply PTFE fuel-system liners and PVDF binder slurry directly to Tier-1 suppliers. The country’s hydrogen strategy further increases the need for PVDF gaskets in electrolyzers and fuel-cell stacks. Technical universities collaborate with industry consortia to optimize the recycling of fluoropolymers and capture emissions.

France, posting a 6.53% CAGR, benefits from Chemours’ Nafion expansion and an aerospace cluster centered on Toulouse. Wire-insulation demand scales with Airbus ramp-ups, while chemical midstream players develop low-emission PVDF synthesis that reduces HF venting by up to 35%. French policy also channels grants into circular-economy pilot plants, enhancing local feedstock resilience as green-hydrogen hubs grow in Dunkirk and Normandy, PVDF and PFA components secure long-term offtake.

Italy’s market remains steady as industrial-equipment repairs and small-engine production absorb PTFE and FEP parts, but high energy costs and tighter PFAS disposal rules temper growth. The United Kingdom navigates post-Brexit regulatory divergence while maintaining demand for ETFE and FEP in aerospace and data-center cabling. Eastern European states are capturing automotive supply-chain relocation, which is lifting regional PVDF and PTFE consumption. Nordic countries lead electrolyzer deployments, driving demand for PVDF gaskets and membranes.

Competitive Landscape

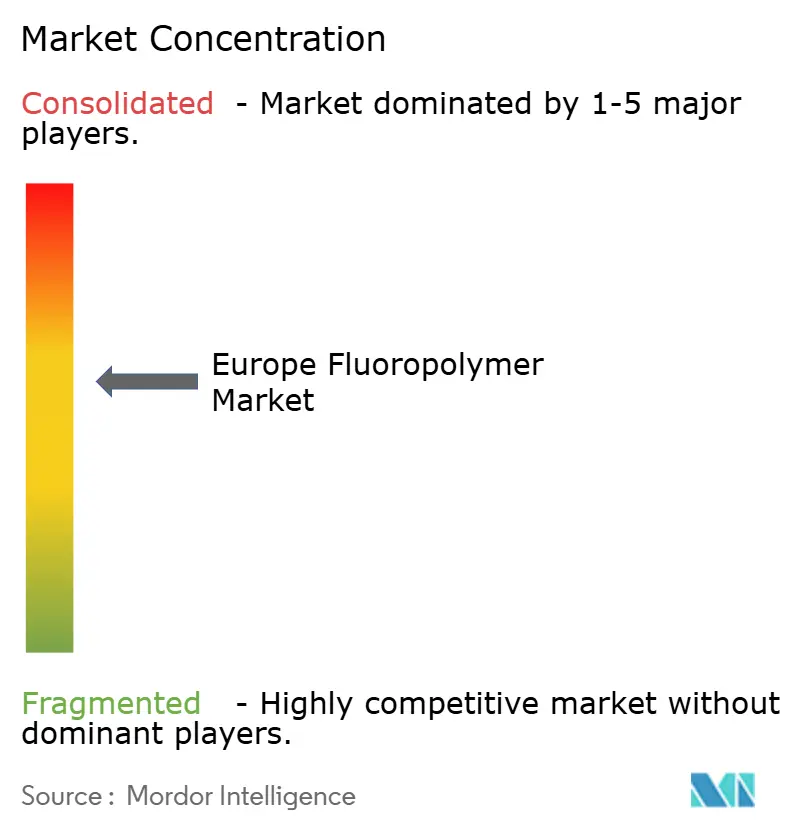

The Europe Fluoropolymer market is moderately concentrated. 3M, Arkema, and Chemours collectively control significant volume through captive fluorspar mines, integrated HF plants, and proprietary polymerization know-how. These firms co-develop application-specific grades with automotive, energy, and electronics customers, securing multi-year contracts that support capital expenditure (Capex) recovery. Overall, sustained R&D spending, back-integration, and customer co-creation position market leaders to manage the twin challenges of regulation and shifting demand within the Europe fluoropolymer market.

Europe Fluoropolymer Industry Leaders

-

3M

-

AGC Inc.

-

Arkema

-

Syensqo

-

The Chemours Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Syensqo signed multi-year contracts to supply its battery-grade Solef Polyvinylidene Fluoride (PVDF) to automotive OEMs and battery manufacturers. Deliveries will come from Syensqo's advanced plant in Tavaux, France, leveraging its suspension PVDF technology.

- June 2024: AGC Chemicals Europe, Ltd., a subsidiary of AGC Inc., supplied Fluon ETFE FILM for the Allianz Arena's facade in Munich, Germany. This film is resistant to heat, chemicals, and various weather conditions, enabling the Allianz Arena's facade to remain intact and functional after years of exposure.

Europe Fluoropolymer Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Ethylenetetrafluoroethylene (ETFE), Fluorinated Ethylene-propylene (FEP), Polytetrafluoroethylene (PTFE), Polyvinylfluoride (PVF), Polyvinylidene Fluoride (PVDF) are covered as segments by Sub Resin Type. France, Germany, Italy, Russia, United Kingdom are covered as segments by Country.| Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) |

| Polytetrafluoroethylene (PTFE) |

| Polyvinyl Fluoride (PVF) |

| Polyvinylidene Fluoride (PVDF) |

| Other Sub-Resin Types |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| France |

| Germany |

| Italy |

| Russia |

| United Kingdom |

| Rest of Europe |

| By Sub-Resin Type | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | |

| Polytetrafluoroethylene (PTFE) | |

| Polyvinyl Fluoride (PVF) | |

| Polyvinylidene Fluoride (PVDF) | |

| Other Sub-Resin Types | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | France |

| Germany | |

| Italy | |

| Russia | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the fluoropolymers market.

- Resin - Under the scope of the study, virgin fluoropolymer resins like Polytetrafluoroethylene, Polyvinylidene Fluoride, Polyvinylfluoride, Fluorinated Ethylene-propylene, Ethylenetetrafluoroethylene, etc. in the primary forms are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms