Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

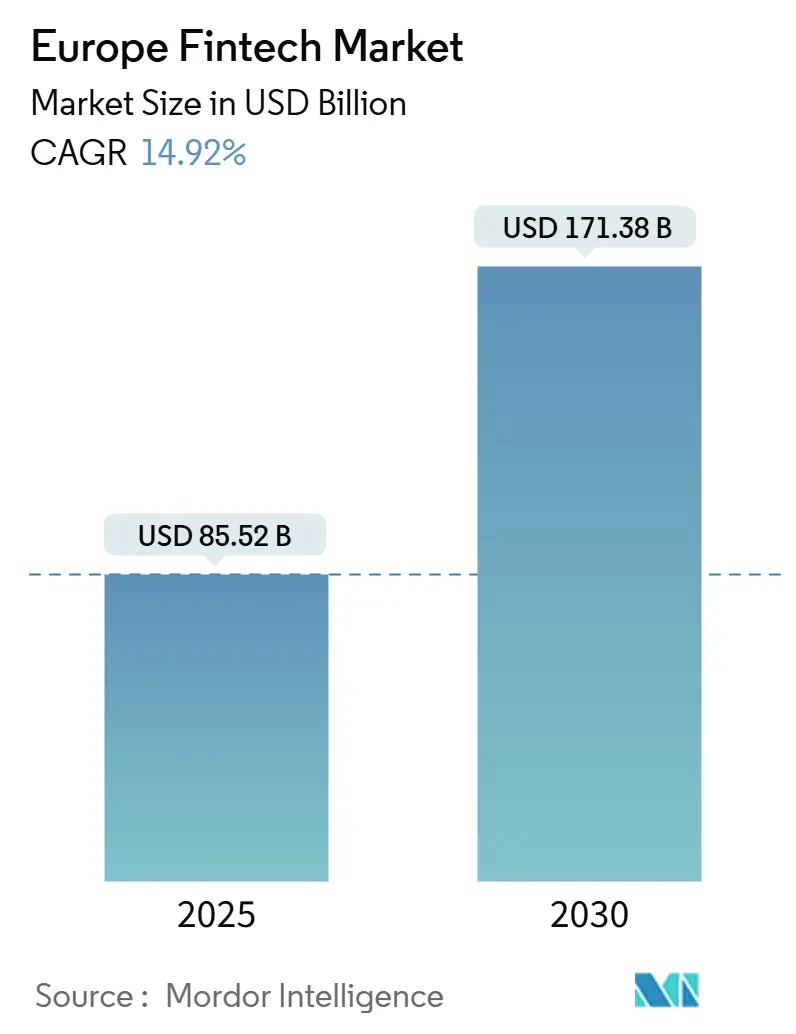

| Market Size (2025) | USD 85.52 Billion |

| Market Size (2030) | USD 171.38 Billion |

| Growth Rate (2025 - 2030) | 14.92% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Fintech Market Analysis by Mordor Intelligence

Europe fintech market size stands at USD 85.52 billion in 2025 and is forecasted to advance to USD 171.38 billion by 2030, translating into a brisk 14.92% CAGR. The accelerated expansion is tied to rising mobile‐first banking habits, tighter European Union mandates on instant payments, and the growing conviction among incumbents that partnering with digital specialists is more economical than building new technology alone. Europe fintech market participants are also profiting from a steady migration of retail and small-business transactions from cash and cards toward account-to-account rails, a shift reinforced by the January 2025 enactment of the Instant Payments Regulation. Demand for embedded finance is widening the addressable base beyond pure consumer payments into B2B working-capital, trade, and treasury use cases, while open-banking APIs move from compliance projects to genuine product-revenue engines. A supportive climate policy agenda and the digital-euro pilot are further catalyzing wallet, identity, and reg-tech spending, ensuring that the Europe fintech market keeps outpacing traditional banking growth over the medium term.

Key Report Takeaways

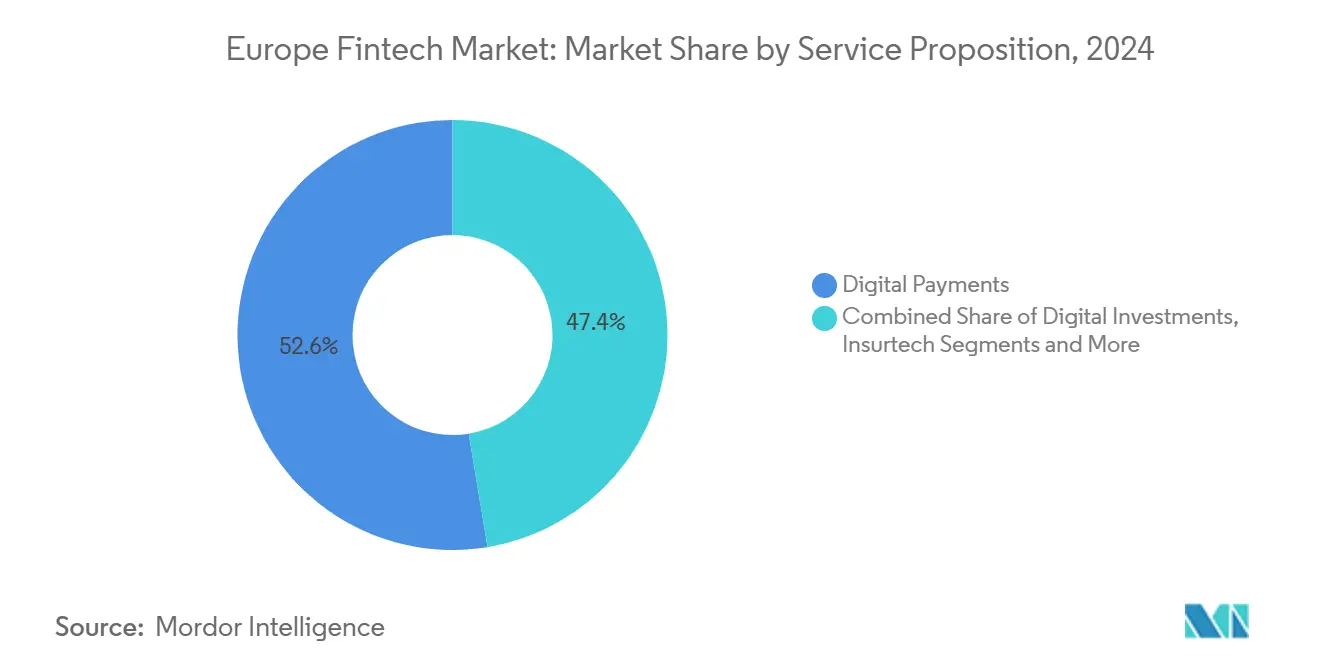

- By service proposition, digital payments led with 52.6% revenue share of Europe fintech market in 2024, whereas Insurtech is projected to log the fastest 16.62% CAGR through 2030.

- By end-user, retail users commanded 67.8% of Europe fintech market share in 2024; the business cohort is set to rise at a 15.83% CAGR out to 2030.

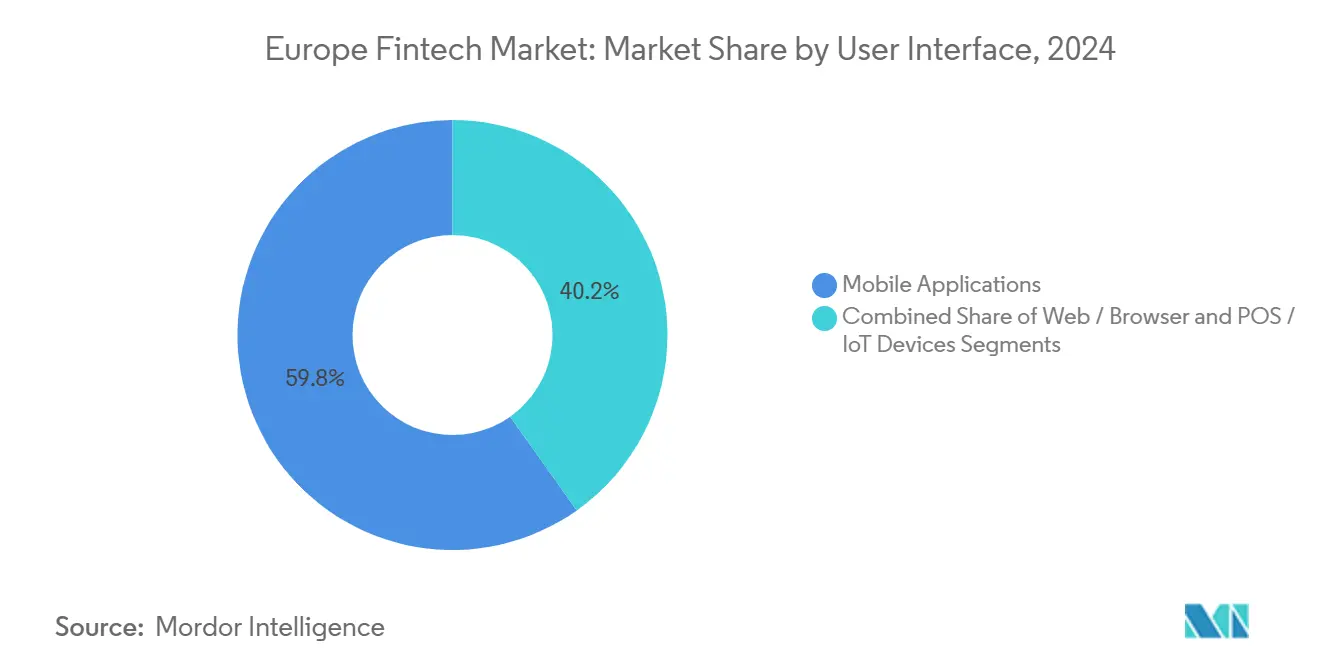

- By user interface, mobile applications captured 59.8% of Europe fintech market size in 2024 and are on course for a 17.91% CAGR between 2025-2030.

- By geography, the United Kingdom accounted for 21.57% of Europe fintech market share in 2024, while the Nordics are heading for a 16.27% CAGR over the same horizon.

Europe Fintech Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of account-to-account instant payments | +3.2% | Benelux, Nordics, Germany | Medium term (2–4 years) |

| Embedded payments uptake among European SMEs | +2.8% | UK, Germany, France, Southern Europe | Medium term (2–4 years) |

| Open-banking API maturation unlocking data revenues | +2.4% | UK, France, Germany, Nordics | Long term (≥ 4 years) |

| Rapid uptake of Buy-Now-Pay-Later in e-commerce | +2.1% | UK, Germany, Nordics, Southern Europe | Short term (≤ 2 years) |

| Digital-euro pilots driving wallet and ID investments | +1.8% | Eurozone, notably Germany, France, Italy | Long term (≥ 4 years) |

| Climate-aligned fintech innovation under EU rules | +1.5% | EU-wide, strongest in Nordics, France, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Account-to-Account Instant Payments Enabled by PSD2 and SEPA Infrastructure

EU law now obliges every payment provider to deliver euro transfers in under 10 seconds at parity pricing with conventional credit transfers, making instant settlement a utility rather than a premium add-on. Fintech platforms with direct clearing‐house connectivity can sidestep card interchange, price aggressively, and monetize data flows created by real-time balances. Nordic wallet mergers, such as Vipps MobilePay, and the forthcoming pan-European Wero scheme widen consumer reach while reducing reliance on global card networks. Banks that still run on legacy batch systems are facing cost pressure to modernize core payments engines or outsource to cloud-native vendors. As instant payments become the default, treasury teams will demand richer liquidity analytics, a field where specialist providers already bundle real-time cash forecasting with multicurrency pooling. Regulatory certainty combined with user familiarity therefore cements instant account-to-account transfer as the bedrock of long-run Europe fintech market adoption.

Acceleration of Embedded Payments Adoption Among European SMEs and Mid-Market Enterprises

Software vendors serving retail, hospitality, logistics, and professional-services niches are weaving invoicing, settlement, and short-term working-capital into their core workflows. For small and midsize enterprises, this integration lowers reconciliation effort and unlocks transaction data that can underpin risk-based credit lines. In Germany and the UK, municipal regulations that digitize tax filing and e-invoicing amplify the appeal of single-screen finance. Payment facilitators that supply white-label APIs now price on net-revenue share, helping independent software companies open new profit streams without the burden of acquiring licenses. The pan-EU SME finance guarantee program likewise encourages banks to distribute lending through embedded partners, sustaining double-digit volume growth even under conservative venture-funding conditions. Because the feature set lives inside operational software, churn is low, fortifying recurring revenue visibility for the vendors that power Europe fintech market pipelines[1]European Investment Bank, “EFSI SME Window,” eib.org.

Maturation of Open-Banking API Ecosystems Unlocking Data-Driven Revenue Streams

The second iteration of the Payment Services Directive created the legal foundation for secure access to payment-account data, yet early deployments were limited to compliance check-boxes. By 2025, leading banks expose premium endpoints—credit risk insights, categorized merchant data, and variable recurring payments—that third parties pay for at tiered usage fees. Fintechs use this intelligence to craft dynamic affordability scores and personalized wealth dashboards, shifting monetization from pure transaction fees to subscription and analytics royalties. National clearing houses in France and the Netherlands already publish standardized performance dashboards, allowing TPPs to benchmark latency and uptime across host banks. The next regulatory wave, PSD3, is expected to enshrine similar rules for savings, insurance, and pensions, further expanding accessible data domains. These structural tailwinds underpin sustained API call growth, reinforcing the data-network effect that anchors long-term revenue capture across the Europe fintech market.

Rapid Uptake of Buy-Now-Pay-Later Solutions Across Regional E-commerce Channels

BNPL adoption moves beyond fashion and electronics into groceries, travel, and subscriptions, helped by the continent-wide surge in debit card preference and prudent credit attitudes among younger adults. Providers now offer capped late-fee structures, interest-bearing installment plans, and fraud-score APIs to merchants, embedding risk controls that pre-empt the incoming Consumer Credit Directive update. Retailers benefit from observable basket-size uplift and repeat purchase frequency, bolstering merchant willingness to absorb MDRs. Top-tier e-commerce platforms have begun rolling out native BNPL widgets supported by white-label financing partners, shortening integration cycles from months to days. Regulators insist on transparent disclosures, prompting providers to upgrade dashboards that let users track multiple installment plans in one view. The interplay of strict consumer safeguards and merchant ROI keeps the service on a solid growth path inside the Europe fintech market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged venture-capital slowdown for scale-ups | -2.1% | UK, Germany, France, rest of Europe | Medium term (2–4 years) |

| Fragmented national licensing hindering expansion | -1.8% | EU-wide, smaller fintech hubs | Long term (≥ 4 years) |

| Rising cloud-sovereignty compliance costs | -1.4% | Germany, France, other EU states | Medium term (2–4 years) |

| Stricter bank-capital rules curbing partner lending | -1.2% | UK, Germany, France, Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Prolonged Venture-Capital Slowdown Creating Funding Gaps for Scale-Ups

Tighter monetary policy and a pivot toward profitability have reduced the pool of follow-on capital available to series-B-plus fintechs. Median cheque sizes fell 29% from 2023 to 2024, forcing growth-stage players to trim headcount, delay expansion, or seek strategic investors. Public-market comparables re-rated sharply, driving internal rate-of-return targets higher for private funds and sharpening due-diligence scrutiny. Government agencies such as the European Investment Fund injected counter-cyclical capital, yet disbursement timelines and ticket sizes rarely match hyper-growth aspirations. As a result, founders prioritize monetization of existing cohorts and rigorously benchmark unit economics before adding new geographies. While healthier in the long run, this discipline temporarily subtracts velocity from the Europe fintech market.

Fragmented National Licensing Regimes Hindering Cross-Border Expansion

Passporting under the single market still requires local establishment for deposit-taking, insurance intermediation, and certain lending activities, particularly in smaller member states that apply gold-plating on top of EU directives. Fintechs must therefore juggle divergent capital requirements, reporting taxonomies, and customer-onboarding rules, driving legal and compliance spend disproportionately higher than revenue in early expansion years. New entrants often select the Netherlands, Lithuania, or Ireland as a first license base owing to faster authorization timelines, yet they later confront incremental approvals in adjacent markets that erode the time-to-scale advantage. The Digital Finance Package advocates a single-point-of-contact rule, but implementation will not conclude before 2027. Until harmonization arrives, overlapping supervision remains a structural drag on the Europe fintech market[2]European Banking Authority, “Single Rulebook Interactive,” eba.europa.eu.

Segment Analysis

By Service Proposition: Insurtech Disrupts Traditional Models

Europe fintech market size for Digital Payments stood at 52.6% of the total market size. The segment’s momentum reflects rapid consumer migration from cash to contactless payments, accelerated yet again by mandatory instant‐payment cost parity. Although high penetration levels in the Nordics and the Netherlands suggest maturity, room for wallet-based value-added services such as micro-savings and installment financing sustains double-digit topline expansion. Payment processors leverage ISO 20022 data richness to upsell reconciliation dashboards and fraud analytics to merchants. Cross-border settlement remains a lucrative niche, with specialist providers offering multicurrency wallets and local payment method orchestration to digital exporters.

Insurtech commands the highest 16.62% CAGR forecast, positioning it as a catalyst for margin expansion inside the Europe fintech market. Usage-based motor policies, AI-enabled claims triage, and embedded micro-insurance sold through travel and electronics retailers are reshaping distribution economics. Traditional carriers partner with cloud-native policy-administration vendors to shrink product launch cycles from months to weeks. ESG-linked covers—parametric flood protection, renewable energy warranty—align with EU taxonomy disclosures, inserting new premium pools into the Europe fintech industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Businesses Drive Innovation Demand

Retail users held a 67.8% share of the market in 2024; habitual mobile wallet usage and a culturally ingrained preference for debit cards underpin this dominance. Loyalty integrations that let consumers earn real-time rewards strengthen daily engagement metrics, ensuring that super-apps lock in high net-promoter scores. The digital euro sandbox draws retail participation from early adopters eager for fee-free peer-to-peer settlement, reinforcing wallet network effects. Challenger banks complement payment features with budgeting tools and fractional-share trading to increase share-of-wallet.

The business cohort, while smaller, is projected to grow at 15.83% CAGR during the forecast period. Treasury portals that bundle multicurrency accounts, on-demand FX hedging, and credit-line assignment are winning over mid-market exporters challenged by post-Brexit trade complexity. SaaS enterprise-resource-planning suites embed supplier financing, transforming payable days outstanding into a revenue lever for platform owners. Regulatory mandates on e-invoicing and real-time VAT reporting force SMEs to digitize invoice flows, indirectly lifting payment-initiation volumes. These momentum drivers assure a rising proportional contribution from business users to the European fintech market revenues.

By User Interface: Mobile Applications Lead Multi-Channel Strategy

Europe fintech market size attributed to mobile applications reached a 59.8% share of the total market size in 2024. Rapid 5G rollout, biometric onboarding, and device-level security chips ease regulatory know-your-customer (KYC) compliance while delivering frictionless user journeys. Feature velocity is high: in-app ESG product scoring, AI-chat account support, and QR-code instant transfers launch in sprints rather than quarterly releases. Nordic issuers report that 94% of daily banking logins originate from mobiles, cementing the channel’s primacy for engagement.

Web and browser interfaces retain relevance for corporate dashboards, portfolio analytics, and complex lending applications. Responsive design ensures parity of features, yet larger screen real estate enables data-dense reporting essential to financial controllers. POS and IoT endpoints, the smallest slice today, are evolving fastest as connected cars, voice assistants, and wearables incorporate tokenized payment credentials. Retailers pilot frictionless checkout lanes where shelf sensors auto-populate baskets and debit customer wallets upon exit. Each new endpoint feeds incremental transaction flows back into the Europe fintech market, reinforcing the omnichannel ecosystem.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United Kingdom held a 21.57% share of Europe fintech market in 2024. A nimble regulatory sandbox, robust venture capital networks, and talent clusters around London Shoreditch continue to attract overseas startups seeking a single English-language launch pad. FCA initiatives such as variable recurring payments extend open-banking utility and provide incumbents with programmable payment use cases that lower merchant costs[3]Financial Conduct Authority, “FCA Business Plan 2025-30,” fca.org.uk.

Germany and France combined represented a significant share of Europe fintech market in 2024, driven by strong industrial B2B demand and supportive public-bank innovation programs. Berlin hosts over 700 fintech firms, many oriented toward supply-chain finance to serve the Mittelstand. France’s Tibi plan channels institutional capital into late-stage scale-ups, filling the domestic funding gap. Both nations champion sovereign-cloud requirements that push providers to localize data centers, indirectly benefiting regional infrastructure players.

Nordic countries—Sweden, Denmark, Finland, and Norway—collectively recorded the highest projected 16.27% CAGR for 2025-2030. Cash usage has fallen below 4% of payment volume, enabling regulators to mandate fully digital tax and welfare disbursement. National digital-ID schemes such as BankID and MitID reduce onboarding abandonment rates, a competitive advantage that heightens foreign fintech interest in local partnerships. Southern states, notably Italy and Spain, accelerate on the back of EU Recovery and Resilience funds earmarked for SME digitization, while Benelux remains a favored hub for passporting due to multilingual talent and regulator proximity.

Competitive Landscape

Europe fintech market competition balances scale economies in payments with fragmentation in niche verticals. Adyen leverages direct acquiring licenses in 50-plus jurisdictions to court enterprise merchants that wish to consolidate gateways. Klarna moves beyond deferred payments into deposit accounts and loyalty engagement, monetizing a 100 million consumer base. Revolut’s 50 million-plus users receive trading, insurance, and soon mortgage options, proving that super-app economics travel outside Asia. Incumbent banks respond by acquiring or investing in banking-as-a-service platforms such as Solaris to rejuvenate product roadmaps.

Consolidation quickens: Shift4’s USD 2.5 billion purchase of Global Blue delivers global tax-free shopping rails to an acquirer seeking European volume density. Private equity firms accumulate infrastructure assets with recurring revenue and high regulatory switching costs, exemplified by Montagu’s takeover of Multifonds. Horizontal expansion is complemented by vertical specialization; Pleo concentrates on expense management for SMEs, Qonto targets freelancers with automation-focused current accounts, and Tide scales bookkeeping-as-a-service. Artificial-intelligence deployment distinguishes winners through superior fraud-signal accuracy and customer-service productivity, driving margin divergence across the Europe fintech market.

White-space growth resides in intersectional propositions: climate-linked hardware leasing, embedded factoring for e-commerce supply chains, and patient payment plans blended into healthcare booking portals. Traditional core banking software refresh cycles offer further entry points as institutions retire mainframes in favor of cloud-native cores. Vendors that prove low migration risk and high regulatory compliance win multi-year contracts, solidifying market position before the next funding wave re-ignites scale-up capital flow.

Europe Fintech Industry Leaders

-

Adyen N.V.

-

Klarna Bank AB

-

Revolut Ltd

-

Checkout.com Group

-

Wise plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Mollie launched services in Sweden, supporting local payment methods such as Swish to address the eighth-largest European e-commerce market.

- February 2025: Shift4 agreed to acquire Swiss paytech Global Blue for USD 2.5 billion, one of the year’s largest cross-Atlantic fintech deals.

- February 2025: Solaris raised EUR 140 million in Series G funding, with SBI Group taking majority ownership to back European banking-as-a-service expansion.

- January 2025: The Instant Payments Regulation came into force, obliging EU payment service providers to offer real-time euro transfers at no surcharge, accelerating A2A adoption across the Europe fintech market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European fintech market as all fee or interest income earned within Europe by regulated providers of digital payments, lending and financing, investment platforms, insurtech offerings, and neobanking services that reach users through mobile apps, browser interfaces, or connected devices.

Scope exclusion: pure-play decentralized crypto exchanges that do not support fiat settlement are kept outside the frame.

Segmentation Overview

- By Service Proposition

- Digital Payments

- Digital Lending and Financing

- Digital Investments

- Insurtech

- Neobanking

- By End-User

- Retail

- Businesses

- By User Interface

- Mobile Applications

- Web / Browser

- POS / IoT Devices

- By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Discussions with payment processors, challenger banks, reg-tech architects, venture investors, and former supervisors across the UK, Germany, France, Spain, and the Nordics guided elasticity assumptions, pricing drifts, and user-migration timelines. Surveys of small merchants and retail savers provided adoption rates for account-to-account rails and in-app wallets, letting us reconcile desk findings with customer reality and fine-tune country weights.

Desk Research

We begin with official macro and industry datasets such as Eurostat household digital-payment penetration, European Central Bank instant-payments volumes, Bank for International Settlements Red Book transaction flows, and European Banking Authority PSD2 compliance filings, which anchor channel mix and pricing ratios. Trade groups like the European Fintech Association, plus national statistics from BaFin, ACPR, and the FCA, enrich fee take-rates and license cohorts. Company filings, IPO prospectuses, and investor decks supply benchmark unit economics that feed our margin curves. Where public data fade, Mordor analysts reference paid resources including D&B Hoovers for revenue splits, Dow Jones Factiva for deal pipelines, and Volza for cross-border remittance flows. The examples above are illustrative; many other sources help us verify, cross-check, and clarify data points throughout the build.

Market-Sizing & Forecasting

A top-down reconstruction converts transaction values, balance sheets, and funding pools into service-level revenues, which are then validated through selective bottom-up checks such as sampled average revenue per user times active user bases. Key variables like mobile banking users, instant SEPA share of transfers, venture funding inflows, PSD2 API call volumes, digital-wallet penetration, and average merchant service charges drive both history and forecasts. Multivariate regression, layered with scenario analysis for regulatory or rate shocks, projects each driver through 2030. Where supplier or channel data remain incomplete, gaps are bridged using banker interviews and regional analogs before final triangulation.

Data Validation & Update Cycle

Outputs pass variance scans against independent payment and lending indicators, followed by senior analyst peer review. We refresh every twelve months, with interim revisions triggered by material events such as new ECB directives or megadeals; just before release, an analyst reruns the model so clients receive the latest vetted view.

Why Mordor's Europe Fintech Baseline Commands Reliability

Published estimates often diverge because analysts define services differently, apply distinct growth levers, or lock in outdated exchange rates.

Key gap drivers include whether unlicensed crypto venues are counted, the extent to which cross-border remittance fees are captured, and how quickly analysts refresh post-PSD2 adoption curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 85.52 B (2025) | Mordor Intelligence | |

| USD 96.50 B (2024) | Global Consultancy A | Includes non-regulated crypto venues and assumes uniform EU spread without country granularity |

| USD 89.30 B (2024) | Industry Data Firm B | Omits early-stage neobanks, applies flat 10% growth path across segments |

| USD 62.63 B (2024) | Regional Research House C | Excludes payment-gateway fees and cross-border remittances, relies heavily on funding data proxies |

These contrasts show that Mordor Intelligence, by selecting only regulated activities, layering market-specific variables, and updating annually, delivers a balanced and transparent baseline that decision-makers can trace back to reproducible steps and reliable inputs.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected growth rate of the Europe fintech market between 2025 and 2030?

The market is forecast to grow at a 14.92% CAGR, more than doubling revenue from USD 85.52 billion in 2025 to USD 171.38 billion by 2030.

Which service proposition will show the fastest expansion?

Insurtech is expected to log the highest 16.62% CAGR as carriers adopt AI-driven underwriting and embedded-insurance sales.

How significant are mobile applications in regional fintech adoption?

Mobile apps accounted for 59.8% of 2024 revenue and are poised to expand at a 17.91% CAGR, underscoring their primacy in everyday financial engagement.

Why are instant payments important for European businesses?

EU regulation mandates real-time euro transfers at no extra cost, allowing merchants and SMEs to manage liquidity with greater precision and lower card-processing fees.

What obstacles do fintech’s face when scaling across European borders?

Fragmented licensing rules require separate authorizations in many jurisdictions, increasing compliance costs and slowing time to market.

How has venture-capital availability altered fintech strategies?

Funding scarcity forces scale-ups to focus on profitability, disciplined customer acquisition, and product lines that deliver near-term cash flow rather than growth at all costs.

Page last updated on: