Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

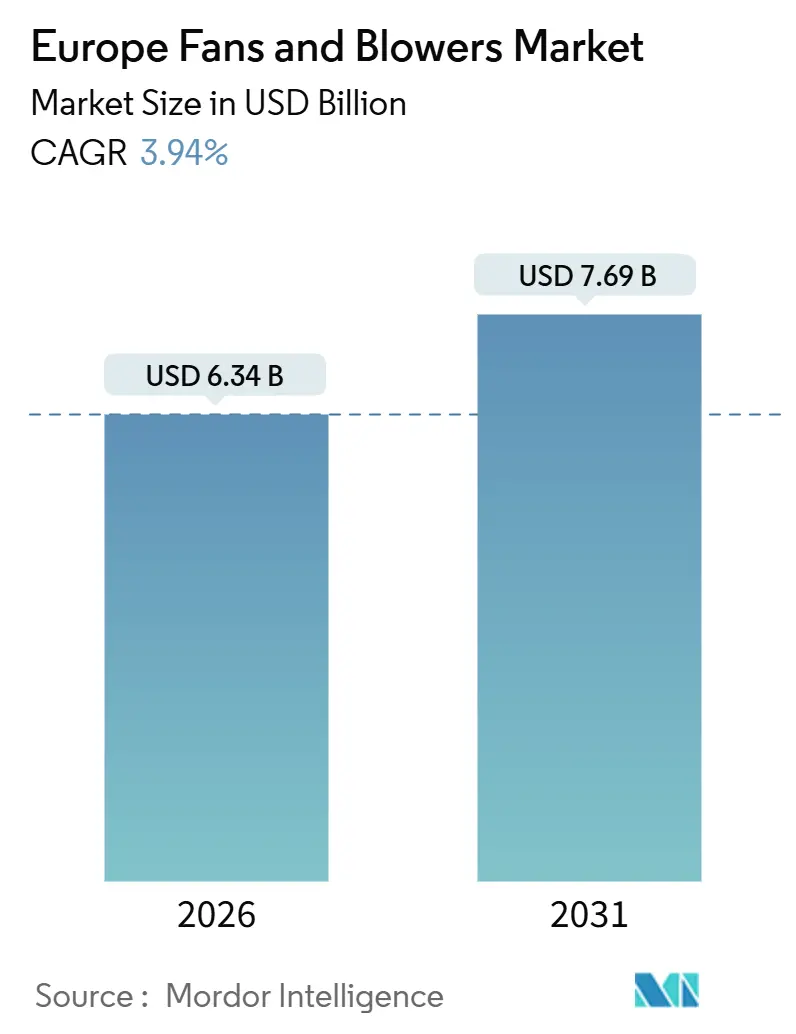

| Market Size (2026) | USD 6.34 Billion |

| Market Size (2031) | USD 7.69 Billion |

| Growth Rate (2026 - 2031) | 3.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Fans And Blowers Market Analysis by Mordor Intelligence

The Europe Fans And Blowers Market size is estimated at USD 6.34 billion in 2026, and is expected to reach USD 7.69 billion by 2031, at a CAGR of 3.94% during the forecast period (2026-2031).

Stricter Ecodesign efficiency rules support demand, the ongoing data-center build-out, and a fast-moving wave of commercial-building retrofits that favor electronically commutated (EC) motors. Centrifugal technology still dominates heavy-industry orders, yet axial designs are winning share in low-pressure ventilation because they couple variable-speed control with quieter operation. End-user spending is tilting toward lifecycle-cost optimization, a trend reinforced by IoT-ready sensors that cut unplanned downtime and document energy savings. Competitive intensity is rising as Asian producers undercut prices by 20-30%, prompting European brands to differentiate with predictive-maintenance analytics and additive-manufactured impellers. Private-equity interest remains high after Samsung Electronics and Chart Industries acquired FläktGroup and Howden, respectively, signaling that conglomerates see ventilation hardware as an anchor for connected-building and hydrogen infrastructure platforms.

Key Report Takeaways

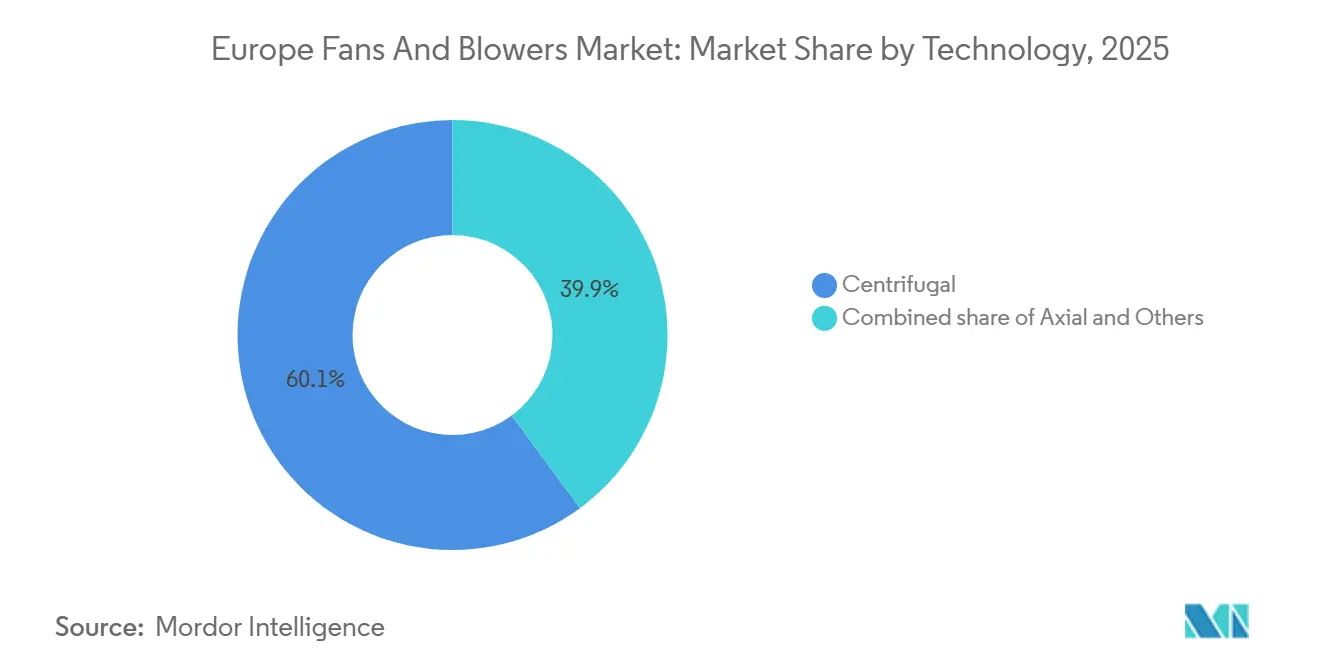

- By technology, centrifugal fans led with 60.1 of % European fans and blowers market share in 2025, while axial fans are projected to advance at a 4.9% CAGR through 2031.

- By pressure range, low-pressure units below 15 kPa captured 55.5% revenue share in 2025 and are expanding at 5.4% CAGR to 2031.

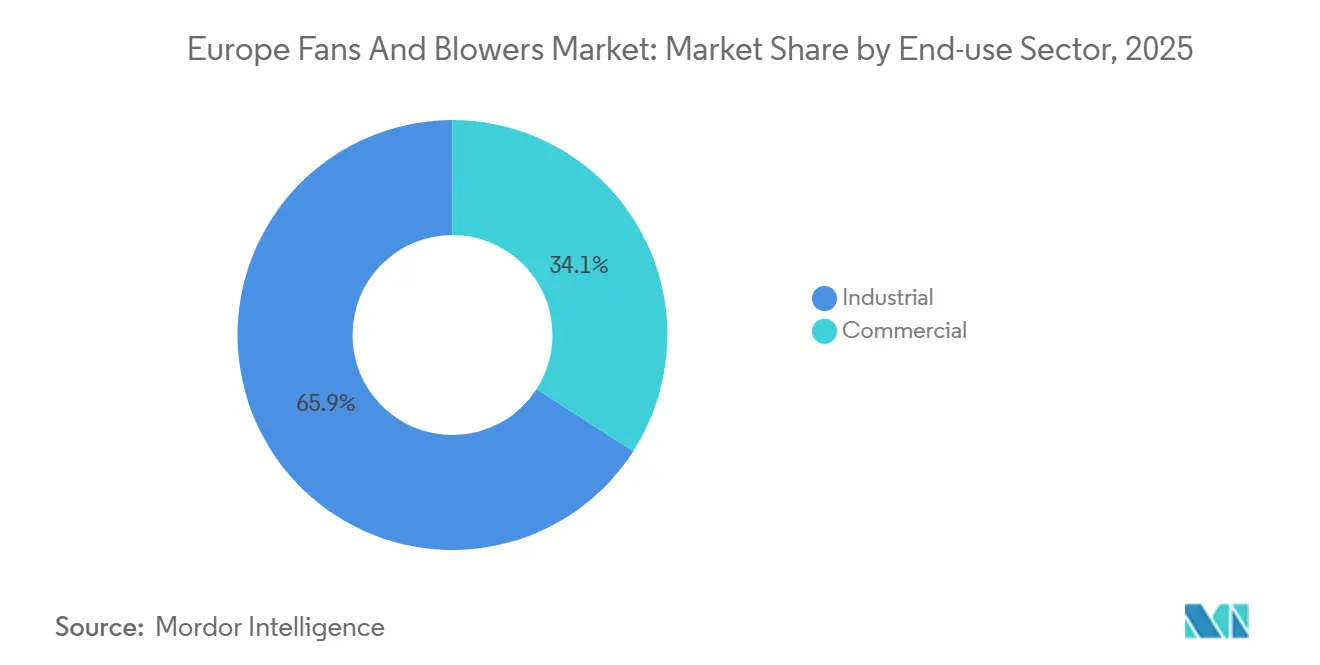

- By end-use sector, industrial facilities accounted for 65.9% of 2025 sales, while commercial buildings are growing fastest at 5.0% CAGR through 2031.

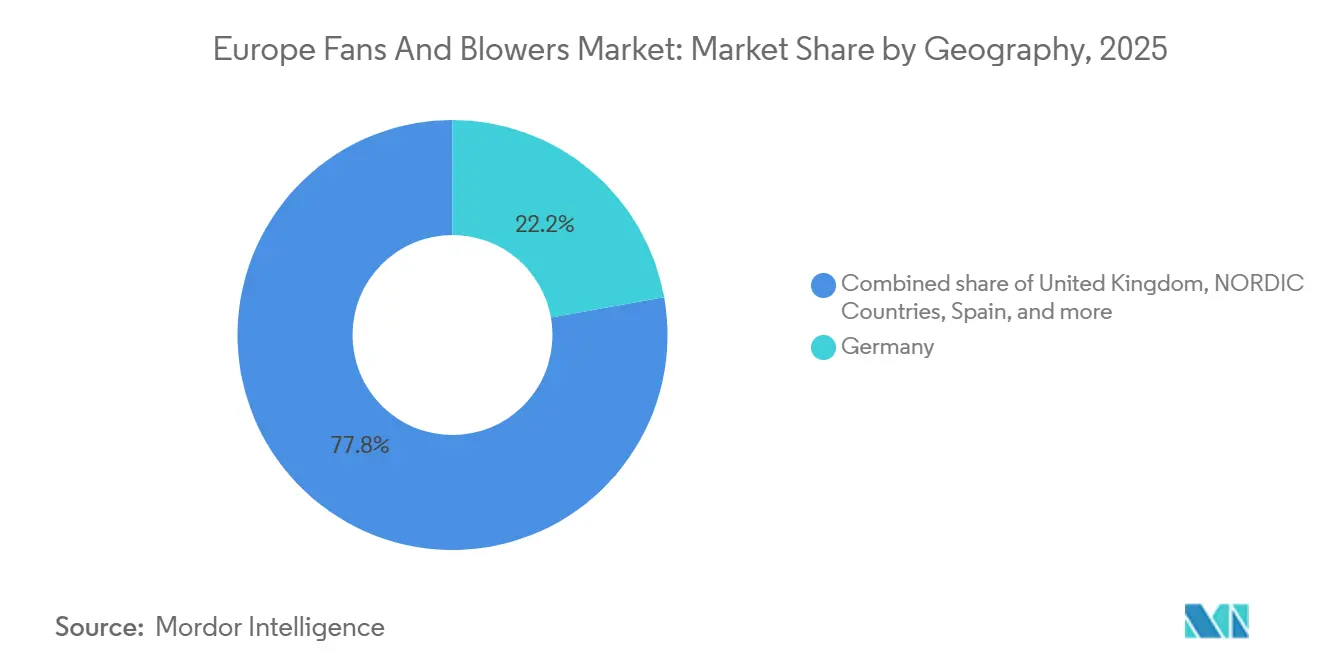

- By geography, Germany contributed 22.2% of 2025 revenue, whereas the Nordics are poised for the quickest climb at 4.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Fans And Blowers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Ecodesign energy-efficiency mandates for fan systems | 1.2% | EU-wide, strongest enforcement in Germany, France, Netherlands | Medium term (2-4 years) |

| Rapid capacity build-out of European data centers | 0.9% | Germany, Netherlands, Nordics, Spain | Short term (≤ 2 years) |

| HVAC green-building retrofits in commercial real estate | 0.8% | Western Europe core (UK, Germany, France), expanding to Southern Europe | Medium term (2-4 years) |

| Expansion of hygienic air-handling demand in F&B and pharma | 0.6% | Denmark, Ireland, Belgium, Germany, Switzerland (pharma hubs); France, Netherlands (F&B clusters) | Medium term (2-4 years) |

| Integration of IoT sensors enabling predictive maintenance | 0.5% | Germany, Nordics, UK (early adopters), gradual spread to CEE | Long term (≥ 4 years) |

| Additive-manufactured impeller designs boosting replacement cycle | 0.3% | Germany, UK, France (aerospace and automotive clusters with AM capabilities) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Ecodesign Energy-Efficiency Mandates for Fan Systems

Commission Regulation 2024/1834 replaces voluntary schemes with binding minimum energy-efficiency indexes from July 2026. The rule covers fans between 125 W and 500 kW, instantly outlawing single-speed AC induction motors in most commercial HVAC and light-industrial settings.[1]European Commission, “Commission Regulation 2024/1834,” europa.eu Germany’s economic ministry projects an 8 TWh cut in EU electricity use by 2030, roughly equal to the output of a mid-sized coal plant. Manufacturers gain a staggered path, Tier 1 in 2026 and Tier 2 in 2029, which softens tooling-cost shocks but shortens the replacement cycle for installed units. Contractors have begun stockpiling compliant inventory, as evidenced by Systemair’s 11.1% organic sales jump in Western Europe during Q2 2025/26. The regulation, therefore, pulls forward retrofit budgets and lifts demand for EC-motor axial fans that comfortably meet the new index thresholds.

Rapid Capacity Build-Out of European Data Centers

Hyperscale and colocation operators commissioned 742 MW in 2024 and have 1.7 GW under construction, with a further 2.5 GW in planning.[2]JLL, “2024 EMEA Data Center Outlook,” jll.com Spain has emerged as a hot spot after Amazon Web Services committed EUR 15.7 billion for its Aragon campus. Frankfurt and London jointly exceed 1.7 GW of live capacity, and both markets carry pipelines above 500 MW. Rack densities are climbing from 8 kW in 2020 to 15 kW and higher for AI workloads, forcing operators to specify low-pressure axial arrays that modulate airflow in real time and meet stringent acoustic rules. Germany’s Section 71a of the Building Energy Act requires digital monitoring for HVAC systems above 290 kW, further steering buyers toward IoT-ready fan platforms.

HVAC Green-Building Retrofits in Commercial Real Estate

The EU renovation wave targets 35 million structures by 2030, mandating Energy Performance Certificate class D or better for all buildings undergoing major works. Part L changes in the United Kingdom set a 27% carbon-cut baseline for new non-domestic buildings, and policymakers are now consulting on retrofit equivalence. Landlords, therefore, replace pre-2010 air-handling units with EC-motor fans that achieve specific fan power below 1.5 W/L·s. Trane Technologies deepened its retrofit toolkit by taking a majority stake in Danish district-energy specialist Vartech in September 2024.

Integration of IoT Sensors Enabling Predictive Maintenance

Section 71a in Germany sets a legal floor for digital monitoring, and early adopters show tangible gains. Samotics’ SAM4 Health detects fan bearing faults 4-8 weeks ahead of failure, yielding 30-40% downtime cuts in pilot industrial sites. Research in 2024 proved that hybrid LoRa-5G sensor networks can hit 95% fault-detection accuracy with sub-200 ms latency, suitable for real-time control.[3]IEEE, “Hybrid LoRa-5G Sensor Networks for HVAC Fault Detection,” ieee.org ebm-papst now embeds Bluetooth Low Energy modules in its RadiCal and AxiBlade lines, letting facility teams pull performance data from a phone without hard-wiring into the building-management system. Adoption remains concentrated in Germany, the Nordics, and the UK because integration depends on planned outages.

Restraints Impact Analysis

| Restrain | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile steel & aluminum prices inflating BOM costs | -0.6% | EU-wide, acute in Germany, Italy, Spain (manufacturing hubs) | Short term (≤ 2 years) |

| Price pressure from low-cost Asian imports | -0.4% | Western Europe (Germany, France, UK), limited in Nordics | Medium term (2-4 years) |

| Supply risks for rare-earth magnets in high-efficiency motors | -0.4% | EU-wide, particularly affecting Germany, France, Italy (motor manufacturing centers) | Medium term (2-4 years) |

| Urban noise-emission limits curbing large-fan installations | -0.3% | Dense urban centers: London, Paris, Berlin, Amsterdam, Milan, Barcelona | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel & Aluminum Prices Inflating BOM Costs

North-west European hot-rolled coil traded between EUR 550 and EUR 720 per t in 2024, with 15% quarter-on-quarter swings driven by energy costs and anti-dumping measures.[4] EUROFER, “European Steel Association Annual Report 2025,” eurofer.eu Aluminum billet fluctuated between USD 2,400 and USD 2,800 per t as smelters curtailed output amid high electricity prices. Fan housings, impellers, and motor frames account for up to 45% of centrifugal unit cost, leaving suppliers exposed when fixed-price contracts collide with raw-material spikes. EBM-Papst’s revenue fell 13.1% in fiscal 2024/25 as legacy quotes failed to absorb input-cost inflation. Steel demand is likely to stabilize alongside a mild construction rebound in 2026, yet aluminum volatility will linger until the Carbon Border Adjustment Mechanism reaches full force.

Price Pressure from Low-Cost Asian Imports

Chinese vendors now provide CE-marked axial fans at 20-30% lower prices, and regional distributors face fewer procurement hurdles as e-commerce simplifies cross-border sourcing. European suppliers counter with extended warranties, local service, and IoT analytics, propositions that resonate with pharmaceutical and data-center customers but less so with price-sensitive commercial buyers. The EU’s Carbon Border Adjustment Mechanism may narrow the gap for steel-intensive centrifugal models, yet aluminum-rich axial units see limited tariff exposure. Systemair acknowledged that specification-grade projects underpin growth while commodity segments lose share to imports.

Segment Analysis

By Technology: EC Motors Propel Axial Gains

Centrifugal fans held 60.1% of 2025 revenue, underpinned by process industries that need high static pressures beyond 70 kPa for material handling and thermal control. Axial designs, however, are advancing at 4.9% CAGR because EC motors cut energy use by as much as 70% compared with single-speed induction units and meet Ecodesign thresholds coming into force in 2026. The Europe fans and blowers market size attached to axial products is expanding fastest within data-center cooling and commercial-HVAC retrofits, where footprint, noise, and variable-speed capability outweigh peak-pressure requirements.

Centrifugal technology will keep its foothold in medium- and high-pressure slots because backward-curved and radial wheels handle particulate-laden flows and corrosive gases. Yet low-pressure ventilation, currently 55.5% of total demand, now gravitates toward axial arrays controlled through building-management software, chipping away at centrifugal share below 15 kPa. The trend parallels a broader shift toward distributed air paths in data halls and office retrofits, replacing legacy high-static central plants with modular fan walls that scale rack by rack.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Pressure Range: Low-Pressure Segment Leads on Dual Fronts

Low-pressure units below 15 kPa secured 55.5% of 2025 revenue and show the highest 5.4% CAGR as building-code revisions tighten specific fan-power ceilings and noise thresholds. The Europe fans and blowers market share that low-pressure products command stems from ventilation retrofits across office, retail, and public buildings, plus the surge in hyperscale data centers, where low static pressure and high volumetric flow best match hot-aisle containment.

Medium-pressure equipment covering 15-70 kPa maintains roughly 30% of the European fans and blowers market size, tracking the overall 3.94% CAGR because industrial capital spending remains cautious. High-pressure models above 70 kPa, used in forced-draft boilers and mining shafts, hover near 15% share and face sub-3% growth due to coal-plant retirements and steel output cuts. The resulting portfolio mix underscores a structural pivot: regulatory and acoustic constraints favor many small, quiet, energy-sipping fans rather than one large, high-static machine.

By End-Use Sector: Commercial Acceleration Amid Industrial Stagnation

Industrial users generated 65.9% of 2025 sales, dominated by power, chemicals, metals, and heavy manufacturing that rely on rugged centrifugal blowers. Pharmaceutical and food plants buck the industrial sluggishness as Novo Nordisk, Eli Lilly, and Pfizer equip new cleanrooms with stainless-steel, HEPA-ready systems that command premium prices.

Commercial buildings, conversely, log the swiftest 5.0% CAGR. Owners retrofit air-handling units to hit Energy Performance Certificate targets without lengthy shutdowns, favoring modular EC-motor axial fans that slot into existing shafts. Trane Technologies’ investment in Vartech exemplifies how OEMs bundle ventilation with heat pumps and district-energy links to capture turnkey retrofit contracts. Shorter 15-year replacement cycles and clear payback calculations ensure that commercial demand grows faster than heavy industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany contributed 22.2% of 2025 revenue thanks to its dense network of automotive, chemical, and machinery plants that specify high-pressure centrifugal blowers for paint booths, fume extraction, and pneumatic conveying. Factory orders dipped 5.4% year-on-year in 2024, tempering near-term expansion, yet the installed base guarantees a steady retrofit stream tied to Ecodesign compliance. The United Kingdom, France, Italy, and Spain collectively form about 40% of the European fans and blowers market size. UK Part L updates and France’s RE2020 standard lift commercial-building retrofits, while Spain’s hyperscale boom, anchored by AWS and Meta, drives low-pressure axial uptake.

The Nordics, though smaller in absolute terms, post the fastest 4.8% CAGR. Denmark’s climate-neutrality goal for 2045 and Sweden’s target of net-zero by 2045 give teeth to efficiency incentives, and district-heating upgrades bundle high-efficiency fans with heat pumps. Novo Nordisk’s EUR 2.3 billion Kalundborg expansion and Microsoft’s Stockholm data-center cluster illustrate how pharmaceutical and hyperscaler investment pushes specification criteria toward lifecycle performance and sensor readiness.

The Netherlands remains Europe’s densest data-center hub, with Digital Realty’s 27 MW AMS11 site relying on variable-speed axial arrays. Central and Eastern Europe contributes roughly 15% of revenue and records near-average growth, held back by looser code enforcement and limited hyperscale presence. Cohesion-fund grants for public-building efficiency are, however, seeding early replacement projects in Poland and the Czech Republic.

Note: Segment shares of all individual segments available upon report purchase

Competitive Landscape

The Europe fans and blowers market features moderate fragmentation; the top five suppliers, ebm-papst, Howden, FläktGroup, Systemair, and Greenheck, control an estimated 35-40% combined share. Conglomerates are entering through acquisitions: Samsung Electronics closed a EUR 1.5 billion buyout of FläktGroup in November 2025 to embed ventilation into smart-building ecosystems. Chart Industries finalized its USD 4.5 billion takeover of Howden in May 2024, bundling cryogenic and hydrogen gear with industrial fans. Schneider Electric paid USD 850 million for UK-based Motivair in October 2024 to deepen thermal-management services for hyperscale data centers.

Strategic playbooks now diverge. Premium brands such as ebm-papst and Systemair embed IoT sensors and cloud dashboards, justifying 15-25% price premiums in uptime-critical niches like pharma and AI data halls. Mid-tier suppliers focus on quick customization and 48-hour delivery for commercial HVAC contractors. Emerging white-space lies in rare-earth-free motor designs; start-ups such as Niron Magnetics develop iron-nitride magnets to sidestep neodymium supply risks highlighted by the EU Critical Raw Materials Act.

Margin pressure from Chinese entrants remains acute for commodity axial models. European brands counter through local service footprints, extended warranties, and additive-manufactured impellers that shave weight and raise aerodynamic efficiency, though these gains resonate mainly with operators who monetize uptime and energy savings.

Europe Fans And Blowers Industry Leaders

ebm-papst Group

Howden Group Ltd

FläktGroup Holding GmbH

Systemair AB

Greenheck Fan Corp.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: ebm-papst Mulfingen GmbH & Co. KGaA & Co. KG, a global frontrunner in air technology solutions, unveiled its cutting-edge, energy-efficient fans and blowers tailored for the bus and coach sector at Busworld 2025.

- August 2025: EBM-Papst designed RadiPac EC centrifugal fans for cleanroom filter-fan units. The five-blade impeller minimizes flow losses, delivering air volumes up to 2,330 m³/h with sufficient pressure for recirculated air. Advanced EC technology and the latest impeller design ensure over 60% efficiency.

- June 2025: UK-based industrial fan manufacturer, Fans & Blowers Limited, has successfully acquired B.O.B. Stevenson Limited, a notable name in the industrial fan sector. This move marks a pivotal moment in the storied journeys of both companies.

Europe Fans And Blowers Market Report Scope

Fans and blowers, both mechanical devices, serve the purpose of moving air or gas. Their primary distinction lies in the pressure they generate: fans, designed for general ventilation, move large volumes of air at low pressure. In contrast, blowers produce a higher, more directed pressure, making them suitable for targeted airflow or for pushing air through resistances such as ducts.

The Europe fans and blowers market is segmented by technology, pressure range, end-use sector, and geography. By technology, the market is segmented into centrifugal, axial, and others. By pressure range, the market is segmented into low (below 15 kPa), medium (15 to 70 kPa, and high (above 70 kPa. By end-use sector, the market is segmented into industrial (power generation, oil and gas, iron and steel, chemical and petrochemical, mining and metals, construction and cement, HVAC and cleanrooms, and others) and commercial. The report also covers market size and forecasts for the European fans and blowers market across major countries. For each segment, the market size and forecasts have been done based on revenue (USD).

By Technology

| Centrifugal |

| Axial |

| Others |

By Pressure Range

| Low (Below 15 kPa) |

| Medium (15 to 70 kPa) |

| High (Above 70 kPa) |

By End-use Sector

| Industrial | Power Generation |

| Oil and Gas | |

| Iron and Steel | |

| Chemical and Petrochemical | |

| Mining and Metals | |

| Construction and Cement | |

| HVAC and Cleanrooms | |

| Others | |

| Commercial |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDIC Countries |

| Netherlands |

| Rest of Europe |

| By Technology | Centrifugal | |

| Axial | ||

| Others | ||

| By Pressure Range | Low (Below 15 kPa) | |

| Medium (15 to 70 kPa) | ||

| High (Above 70 kPa) | ||

| By End-use Sector | Industrial | Power Generation |

| Oil and Gas | ||

| Iron and Steel | ||

| Chemical and Petrochemical | ||

| Mining and Metals | ||

| Construction and Cement | ||

| HVAC and Cleanrooms | ||

| Others | ||

| Commercial | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Netherlands | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Europe fans and blowers market?

The market stood at USD 6.34 billion in 2026 and is projected to reach USD 7.69 billion by 2031.

How fast is the market expected to grow through 2031?

Revenue is forecast to advance at a 3.94% CAGR between 2026 and 2031.

Which technology category is expanding quickest?

Axial fans powered by electronically commutated motors are growing at 4.9% CAGR on the back of data-center and commercial-HVAC demand.

Why are low-pressure fans gaining share?

Tight building-code limits on specific fan power and a shift toward distributed ventilation make low-pressure, variable-speed units the most energy-efficient option.

Which region is expected to record the fastest growth?

The Nordic countries are forecast to log a 4.8% CAGR, driven by aggressive decarbonization goals and data-center investment.

How are European suppliers responding to low-cost Asian imports?

They focus on lifecycle-cost value, IoT-enabled predictive maintenance, local service networks, and advanced impeller designs to justify premium pricing.