Europe Electric Wheelchair Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

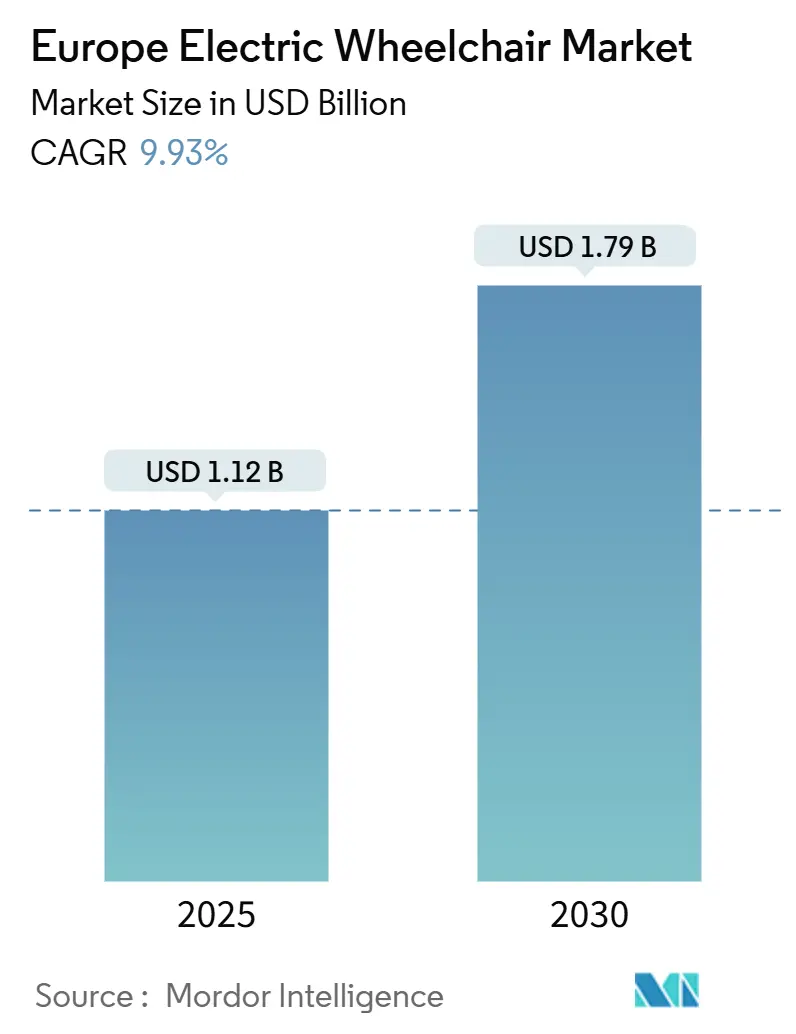

| Market Size (2025) | USD 1.12 Billion |

| Market Size (2030) | USD 1.79 Billion |

| Growth Rate (2025 - 2030) | 9.93% CAGR |

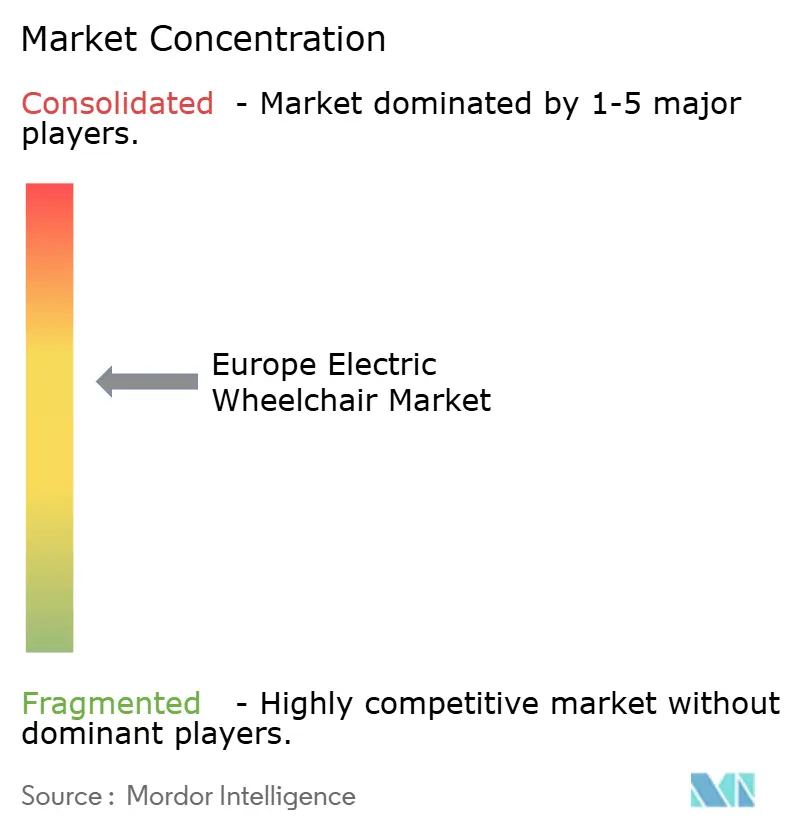

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Electric Wheelchair Market Analysis by Mordor Intelligence

The European electric wheelchair market size is estimated to be USD 1.12 billion in 2025 and is expected to reach USD 1.79 billion by 2030, growing at a CAGR of 9.93% during the forecast period (2025-2030). The European electric wheelchair market benefits from structural demographic aging, cohesive reimbursement frameworks, and battery innovation that reduces device weight while extending range, positioning powered mobility as a cost-effective substitute for institutional care. Demand accelerates as national accessibility mandates tighten, corporate fleet programs gain prominence in ESG, and second-life electric-vehicle batteries lower ownership costs. Meanwhile, the EU Battery Regulation 2023/1542 requires a redesign of the supply chain, creating both short-term compliance costs and long-term competitive advantages for manufacturers with traceable component sourcing. Spain drives incremental volume as the Recovery and Resilience Plan spending modernizes long-term care infrastructure, while Germany secures absolute leadership through comprehensive statutory coverage and dense service infrastructure. In parallel, AI-enabled predictive maintenance and tele-rehab connectivity reshape post-sale economics, allowing providers to monetize uptime guarantees and remote clinical insights.

Key Report Takeaways

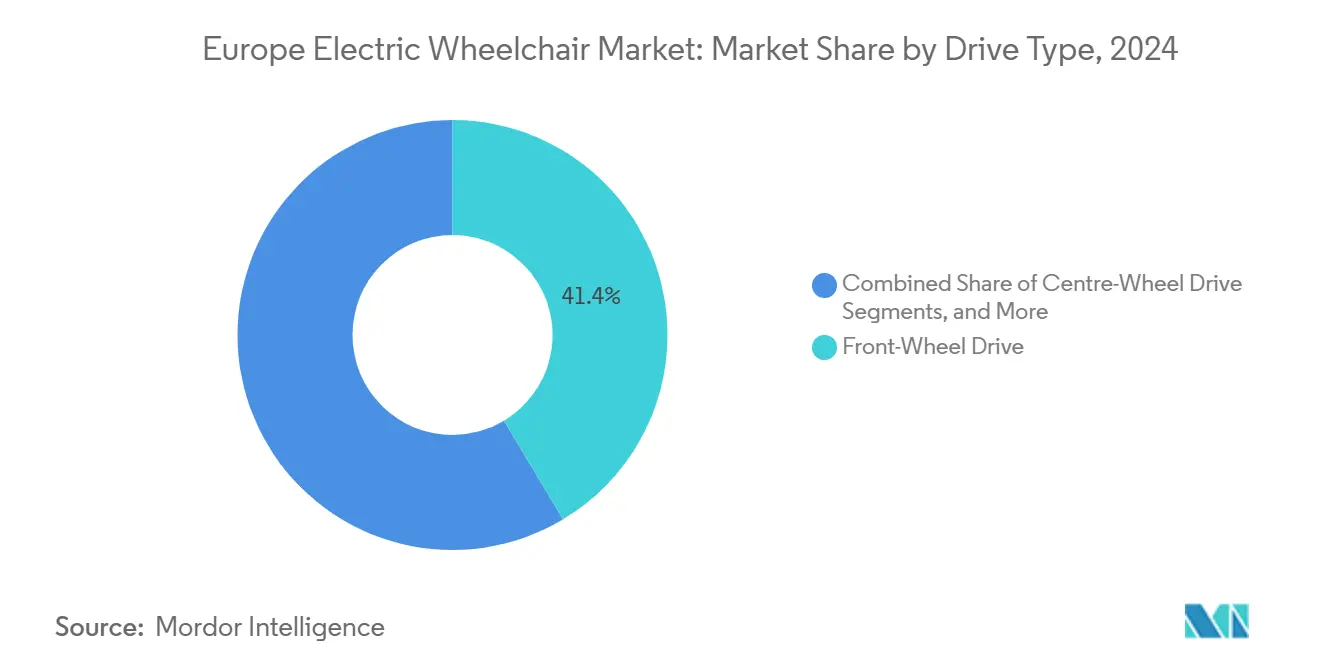

- By drive type, front-wheel drive accounted for 41.35% of the European electric wheelchair market share in 2024; center-wheel drive is advancing at a 9.94% CAGR through 2030.

- By end user, personal/homecare held 67.73% of the European electric wheelchair market share in 2024, while the same segment is expected to expand at a 9.98% CAGR to 2030.

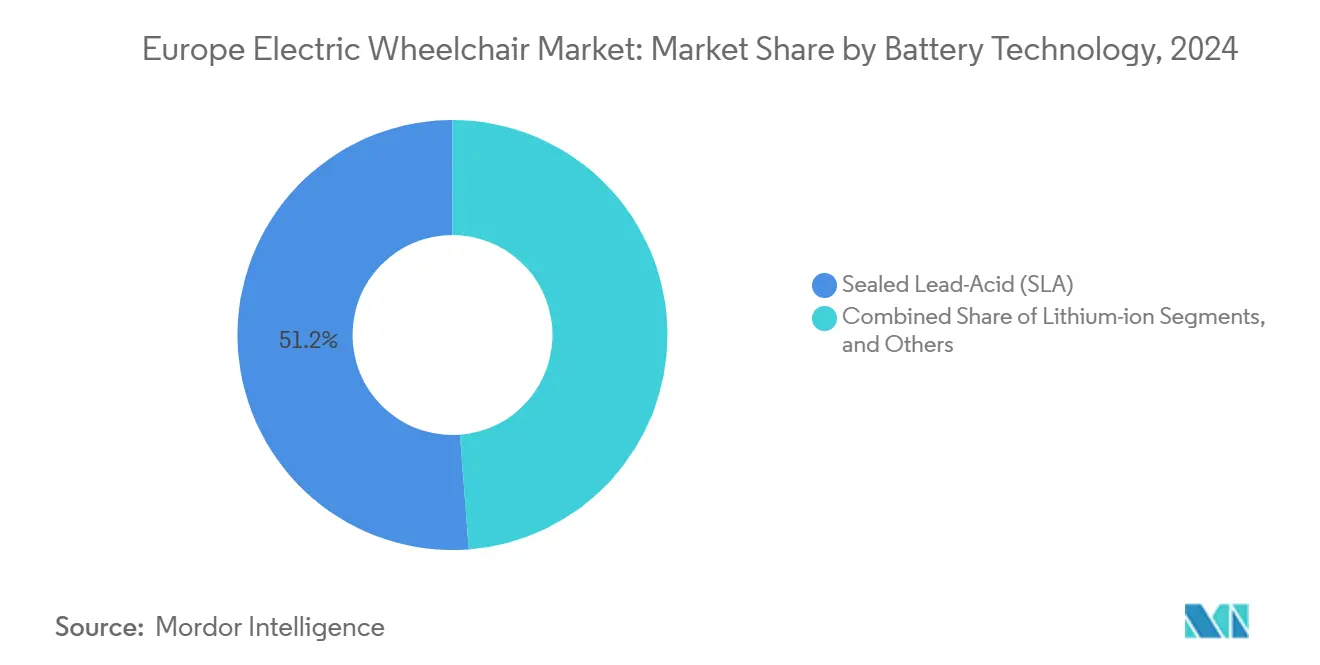

- By battery technology, sealed lead-acid accounted for 51.24% share of the European electric wheelchair market size in 2024, and lithium-ion is projected to grow at 10.07% CAGR toward 2030.

- By distribution channel, dealers/offline retail controlled a 63.45% share of the European electric wheelchair market size in 2024; online/e-commerce platforms posted the fastest growth rate of 10.03% through 2030.

- By country, Germany led with 27.83% of the European electric wheelchair market share in 2024, whereas Spain recorded the highest 9.96% CAGR to 2030 under the national Recovery and Resilience Plan.

Europe Electric Wheelchair Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Population Prevalence | +2.8% | Global, with highest concentration in Germany, Italy, and Eastern Europe | Long term (≥ 4 years) |

| EU Reimbursement Regulations | +2.1% | EU-wide, with varying national implementation timelines | Medium term (2-4 years) |

| Advances In Lithium-Ion Batteries | +1.9% | Global, with early adoption in Northern and Western Europe | Medium term (2-4 years) |

| AI-Based Predictive Maintenance | +1.4% | Asia Pacific core, spill-over to Northern Europe and urban centers | Long term (≥ 4 years) |

| Second-Life EV Batteries | +1.2% | EU-wide, with pilot programs in Germany, Netherlands, and Nordics | Long term (≥ 4 years) |

| Corporate Inclusive-Mobility Fleet Demand | +0.9% | Western Europe, concentrated in corporate headquarters regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Higher Chronic-Disease Prevalence

As the proportion of elderly citizens in Europe continues to grow significantly, the electric wheelchair market on the continent is witnessing notable expansion, driving structural demand for powered mobility devices [1]“Ageing Europe—Statistics on Population Developments,” Eurostat,ec. europa.eu . Chronic conditions like diabetes and musculoskeletal disorders affect a significant portion of the European population, resulting in a notable percentage of seniors relying on wheelchairs. Germany leads in overall demand due to its large elderly population, while Eastern European countries are experiencing the fastest aging rates, creating opportunities for early market entrants. Healthcare systems are increasingly adopting aging-in-place policies, shifting reimbursement budgets from long-term care facilities to durable equipment that supports independent living at home. WHO estimates indicate that the use of electric wheelchairs among seniors remains relatively low but shows growth potential, implying a substantial unmet need as demographic pressure intensifies [2]“Assistive Technology Factsheet,” World Health Organization, who.int .

EU Reimbursement & Accessibility Regulations

By the mid-2020s, the European Accessibility Act mandates a barrier-free design across transport, digital banking, and commerce. This requires institutions to offer suitable powered mobility aids for both staff and customers. In Northern Europe, complementary national payor systems provide substantial coverage for prescribed devices. In contrast, Southern and Eastern countries offer only partial coverage, limiting device uptake. By the latter half of the decade, harmonized digital product passports aim to streamline cross-border conformity assessments, reducing transaction friction for both manufacturers and hospitals. However, differing implementation deadlines compel suppliers to uphold multi-country reimbursement strategies and localized tender approaches. Over time, standardized evidence requirements tend to benefit incumbents with established clinical dossiers and quality systems aligned with ISO 13485.

Advances in Lithium-Ion Batteries & Lightweight Alloys

Lithium-ion packs, offering significantly higher energy density compared to sealed lead-acid units, reduce overall chair weight considerably and extend daily range. These advantages appeal to both independent users and busy hospital fleets. Meanwhile, carbon-fiber frames and aerospace-grade aluminum further lighten the chassis, all while adhering to ISO 7176 rollover and crash standards. As cell prices decline—due to passenger-EV gigafactories—the premium becomes justifiable for mid-tier chairs, broadening the market's reach. Battery management electronics relay real-time health data to cloud dashboards, enabling service partners to anticipate failures and schedule swaps, thereby minimizing downtime. In Northern Europe, providers are testing subscription models that incorporate battery analytics, achieving notable reductions in lifetime costs for institutional fleets.

AI-Based Predictive Maintenance & Tele-Rehab Integration

IoT-embedded motors, gyros, and powertrains transmit operating parameters that machine-learning algorithms analyze to schedule predictive service. Pilot trials in Denmark and Sweden cut unscheduled breakdowns by two-fifths, freeing scarce clinical technicians for higher-value tasks. Tele-rehab portals overlay wheelchair mobility metrics onto electronic health records, enabling physiotherapists to fine-tune home-exercise regimens. Data-rich ecosystems appeal to payors because remote assessments avoid transportation costs and reduce hospital readmissions. Yet, roll-out depends on reliable 4G/5G coverage and digital literacy among elderly users; public-funded digital-skills programs therefore become indirect growth catalysts. Manufacturers that offer open APIs gain an edge as hospitals seek vendor-agnostic analytics hubs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Cost | -1.8% | Southern and Eastern Europe, with gaps in rural coverage | Medium term (2-4 years) |

| Infrastructure & Service-Network Gaps | -1.2% | Rural regions across all EU countries, most acute in Eastern Europe | Long term (≥ 4 years) |

| EU Battery Regulation 2024/1542 Compliance Costs | -0.9% | EU-wide, with highest impact on smaller manufacturers | Short term (≤ 2 years) |

| Surging Refurbished-Chair Marketplaces | -0.7% | Western Europe, concentrated in online marketplaces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Cost & Patchy Reimbursement

Advanced chairs span fairly, creating affordability hurdles where public coverage lags [3]“Health at a Glance: Europe 2024,” Organisation for Economic Co-operation and Development, oecd.org . Northern payors reimburse most of it, but Southern systems cap funding to basic models, forcing many households to self-finance or defer purchase entirely. Lengthy prior-authorization cycles extend patient wait times, often exceeding three months in Italy and Greece, intensifying inequity between regions. Private insurance rarely fills the gap, resulting in an economic stratification that contradicts the common EU objectives for health access. Fiscal pressure following pandemic-era spending makes rapid reimbursement harmonization unlikely, maintaining divergent national uptake curves until at least 2029.

Infrastructure & Service-Network Gaps in Rural EU

Rural municipalities face lengthy repair lead times, a stark contrast to the prompt same-day support available in metro areas. This disparity not only compromises the quality of life for rural residents but also curtails their social participation. In Eastern Europe, many older homes grapple with restricted charging access. Here, retrofitting efforts lag behind essential energy-efficiency upgrades. A shortage of certified technicians poses challenges, making it difficult to meet the Regulation’s mandates on battery swaps and recycling quotas. This shortfall jeopardizes product availability, especially in remote areas. While EU structural funds aim to bolster broadband and e-mobility infrastructure, many of these grants are still mired in the feasibility stage, delaying their full impact for the foreseeable future. Vendors that strategically invest in mobile service vans and cloud diagnostics stand poised to cultivate customer loyalty, especially as public-sector capacity upgrades loom on the horizon.

Segment Analysis

By Drive Type: Centre-Wheel Maneuverability Gains Traction

Front-wheel systems dominated the European electric wheelchair market share at 41.35% in 2024, due to their familiarity in hospital procurement and competitive price points. However, centre-wheel platforms are posting a 9.94% CAGR as clinicians prioritize tight turning radii that suit narrow corridors and small apartments, a trend echoed in Spain’s long-term-care retrofit program. Rear-wheel designs remain relevant for outdoor users seeking top speed and curb-climb capacity, while standing wheelchairs serve spinal cord and pediatric therapy protocols. Hybrid all-wheel variants are found in premium segments, where adventure-sport enthusiasts highly value adaptive terrain handling.

Centre-wheel adoption accelerates as multi-motor control units become cheaper, narrowing the cost gap with front-wheel chairs to one-fifth. Clinical trials across German university hospitals report faster obstacle clearance for centre-wheel users, an outcome that influences payor formularies and procurement kits. Manufacturers integrate modular drive modules that let providers convert frame architecture post-purchase, extending fleet life and boosting residual value. As EU tender documents increasingly impose maneuverability benchmarks, suppliers with centre-wheel portfolios secure higher bid scores, reinforcing the segment’s momentum across the European electric wheelchair market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Personal-Care Demand Steers Home-Centric Design

Personal/homecare captured 67.73% of the European electric wheelchair market share in 2024, the consequence of aging-in-place strategies that channel public funds toward community settings. This category also outpaces other verticals at a 9.98% CAGR through 2030, driven by Spain’s resilience plan, which earmarks budgets for telecare and domiciliary support for powered mobility. Hospital and clinic demand remains steady as infection-control-compliant frames and sealed electronics become routine line items in acute-care tenders. Rehabilitation centers serve as innovation incubators, featuring adjustable seating and sensor-laden platforms that feed therapy dashboards, while sports organizations develop a niche premium line for adaptive athletics.

At home, lithium-ion penetration grows faster because users value weight savings that facilitate self-transfer and car loading, thereby supporting independent living. Customizable joystick algorithms enable fine-tuned acceleration curves tailored to residential layouts, helping personal users avoid wall impacts. Meanwhile, long-term care facilities standardize their fleets to simplify training and spare management, increasingly adopting leasing models that swap units every three years. Tele-rehab compatibility is now a purchasing criterion in most municipal home-care tenders, reinforcing a software-defined product mindset among suppliers competing in the European electric wheelchair market.

By Battery Technology: Lithium-Ion Leapfrogs Legacy Lead-Acid

Sealed lead-acid packs retained 51.24% of the European electric wheelchair market share in 2024, primarily due to their competitive pricing and widespread recycling streams. Yet, lithium-ion units are growing at a rate of 10.07% annually, as their range, weight, and charge cycle superiority convince payers and users alike. The EU Battery Regulation 2023/1542 tilts the playing field by mandating performance labeling and removability, criteria that are easier to meet with modular lithium units. Nickel-metal hydride and early solid-state chemistries remain in pilot phases for extreme-temperature applications, such as Nordic outdoor sports.

In recent years, the European market for lithium-ion electric wheelchairs has experienced significant growth. Projections indicate continued expansion in the coming years, driven by inflows from second-life EV cells that help reduce material costs. Battery passports not only validate the origin of these batteries but also boost their residual value in the refurbished market. Meanwhile, advanced BMS chips are paving the way for revenue through subscription monitoring. As the EU tightens recycling quotas in the near future, disposal fees for lead-acid batteries are expected to increase substantially. This shift diminishes the traditional cost advantage of lead-acid batteries, accelerating the move towards lithium across institutional fleets.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Hybrid Paths Blend Digital & Clinical Support

Dealer/offline retail networks held a 63.45% share of the European electric wheelchair market in 2024, reflecting the need for mandatory face-to-face clinical assessments and device fittings. Online channels, however, are projected to post a 10.03% CAGR to 2030 as video-based consultation, augmented-reality measurement apps, and integrated insurance portals mature. Institutional procurement remains steady but is shifting toward framework agreements that emphasize lifetime service costs rather than acquisition prices.

E-commerce excels in price transparency, offering a wider range of choices for digitally savvy caregivers who cross-shop across the EU single market. Some manufacturers deploy click-to-clinic models where users configure chairs online and finalize fittings at partner centers, blending convenience with safety. Meanwhile, dealers diversify into subscription service packs, bundling predictive-maintenance telemetry and battery leasing. The hybrid blend is expected to generate one-fifth of incremental volume by 2030, indicating multichannel coexistence rather than outright channel displacement in the European electric wheelchair market.

Geography Analysis

Western and Northern Europe form the demand core, led by Germany’s 27.83% share in 2024, underpinned by statutory health insurance that reimburses complete prescribed devices and a nationwide network of numerous certified mobility retailers. France and Italy maintain a steady pull through standardized procurement, while cross-border mobility within the Schengen zone accelerates secondary sales of refurbished units. Spain outperforms the regional CAGR average at 9.96%, driven by Recovery and Resilience Plan outlays that modernize long-term care infrastructure and subsidize digital health integration. Nordic countries, although small in population, excel in the adoption of premium bright chairs due to their high per-capita healthcare spending and universal broadband coverage.

In the United Kingdom, straying from EU medical device regulations has resulted in unclear labeling and inadequate post-market surveillance. Yet, due to the NHS's procurement strength, suppliers on the continent still find a robust demand, bolstered by mutual recognition clauses. Eastern European nations, notably Poland, Romania, and the Baltic states, are experiencing significant growth, driven by EU cohesion funds allocated to hospital upgrades and rural access initiatives. Yet, a lack of service networks means rural patients face prolonged repair downtimes, stalling adoption until technician numbers grow. Furthermore, the EU Battery Regulation's infrastructure mandates exacerbate the rural-urban divide, with certified recycling points predominantly located in major cities.

Cross-border e-commerce now accounts for a notable share of personal-use imports, driven by both price differences and device customizations not available locally. Manufacturers storing spare parts centrally in Benelux have significantly reduced cross-country shipping times, boosting user satisfaction. Looking ahead, aligning reimbursement codes with the digital product passport could smooth out remaining regulatory bumps, setting the stage for a unified demand cycle in the European electric wheelchair market, which transcends national borders.

Competitive Landscape

The European electric wheelchair industry exhibits moderate concentration, with the top five companies jointly controlling approximately three-fifths of unit shipments, leaving a significant opportunity for specialized entrants to emerge. Permobil leads the premium clinical segments through its M-series platform, known for its programmable seating and cloud analytics. In contrast, Sunrise Medical dominates mid-range institutional fleets with its Quickie line, acclaimed for its reliability. Invacare leverages vertical integration across batteries, motors, and seating, helping to shield margins against raw material inflation. Ottobock diversifies from prosthetics into powered chairs, capitalizing on cross-selling opportunities in rehabilitation clinics, while Pride Mobility remains strong in consumer-focused SKUs distributed via pan-European dealer networks.

Competition now hinges on software roadmaps as much as it does on mechanical engineering. Leaders embed over-the-air firmware updates that refine joystick sensitivity, unlock subscription telemetry, and offer pay-per-use feature packs. Smaller firms target niche users, such as bariatric or pediatric populations, where large players’ modular chassis may be oversized or cost-prohibitive. Compliance mastery also constitutes a barrier; battery passport serialization and MDR Class IIa audits require capital that start-ups often lack. In response, larger OEMs launch white-label programs that enable innovators to piggyback under established CE certificates, thereby accelerating ecosystem expansion.

Strategic M&A focuses on AI analytics and lightweight material start-ups, rather than horizontal consolidation of wheelchair brands. Venture capital inflows favor tele-rehab platforms that integrate wheelchair mobility data, creating acquisition targets for OEMs seeking end-to-end care offerings. Service footprint remains a differentiator: companies operating mobile repair fleets gain churn protection through rapid onsite fixes, a perk especially valued in rural EU regions. Overall, margin resilience rests on balancing hardware commoditization with data-driven recurring revenue—an equation incumbents appear better positioned to solve within the European electric wheelchair market.

Europe Electric Wheelchair Industry Leaders

Pride Mobility Products

MEYRA GmbH

Invacare Corporation

Hoveround Corporation

Ottobock SE & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Ottobock (UK) has launched the Juvo B7 power wheelchair, offering mid- and front-wheel drive variants designed for users with complex positioning requirements.

- May 2024: Küschall, a subsidiary of Invacare, introduced the Champion SL folding manual wheelchair, emphasizing travel convenience and high-performance frame rigidity.

Europe Electric Wheelchair Market Report Scope

Electric wheelchairs, commonly referred to as power or motorized wheelchairs, are wheeled seating devices driven by electric motors. They cater to individuals unable to manually operate traditional wheelchairs, such as those with mobility challenges and seniors residing in retirement homes, assisted living facilities, or their own homes.

The European Electric Wheelchair Market is segmented by product, portability, age, end-use, and country. Based on the product, the market is segmented into Front Wheel, Middle Wheel, Rear Wheel, and Others. Based on end use, the market is segmented into Personal, Hospital, and Sport Conditioning. Based on the country, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe. For each segment, market sizing and forecasting have been conducted based on value (USD) and Volume (Units).

| Front-Wheel Drive |

| Centre-Wheel Drive |

| Rear-Wheel Drive |

| Standing / Standing-Up |

| All-Wheel / Hybrid Drive |

| Personal / Homecare |

| Hospitals & Clinics |

| Rehabilitation Centres |

| Sports & Adventure Conditioning |

| Long-Term Care Facilities |

| Sealed Lead-Acid (SLA) |

| Lithium-ion |

| Others |

| Dealer / Offline Retail |

| Online / E-commerce |

| Institutional Procurement |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Drive Type | Front-Wheel Drive |

| Centre-Wheel Drive | |

| Rear-Wheel Drive | |

| Standing / Standing-Up | |

| All-Wheel / Hybrid Drive | |

| By End User | Personal / Homecare |

| Hospitals & Clinics | |

| Rehabilitation Centres | |

| Sports & Adventure Conditioning | |

| Long-Term Care Facilities | |

| By Battery Technology | Sealed Lead-Acid (SLA) |

| Lithium-ion | |

| Others | |

| By Distribution Channel | Dealer / Offline Retail |

| Online / E-commerce | |

| Institutional Procurement | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe electric wheelchair market in 2025 and how fast is it expanding?

It reached USD 1.12 billion in 2025 and is projected to grow at a 9.93% CAGR to 2030.

Which country is registering the quickest sales growth?

Spain posts the region’s highest 9.96% CAGR through 2030, supported by Recovery and Resilience Plan healthcare funding.

What drive configuration currently dominates demand?

Front-wheel chairs lead with 41.35% share, though centre-wheel platforms are gaining fastest at 9.94% CAGR.

Which battery technology is displacing sealed lead-acid units?

Lithium-ion packs are advancing at a 10.07% CAGR thanks to lighter weight, longer range, and Regulation 2023/1542 compliance.

What remains the single biggest adoption barrier?

High up-front prices and uneven reimbursement, especially across Southern and Eastern Europe, continue to hinder broad uptake.

How are manufacturers creating post-sale value?

They bundle AI-driven predictive maintenance and tele-rehab data services, cutting downtime and generating recurring revenue.