Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 46.12 Billion |

| Market Size (2031) | USD 90.89 Billion |

| Growth Rate (2026 - 2031) | 14.53% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Electric Motors For Electric Vehicle Market Analysis by Mordor Intelligence

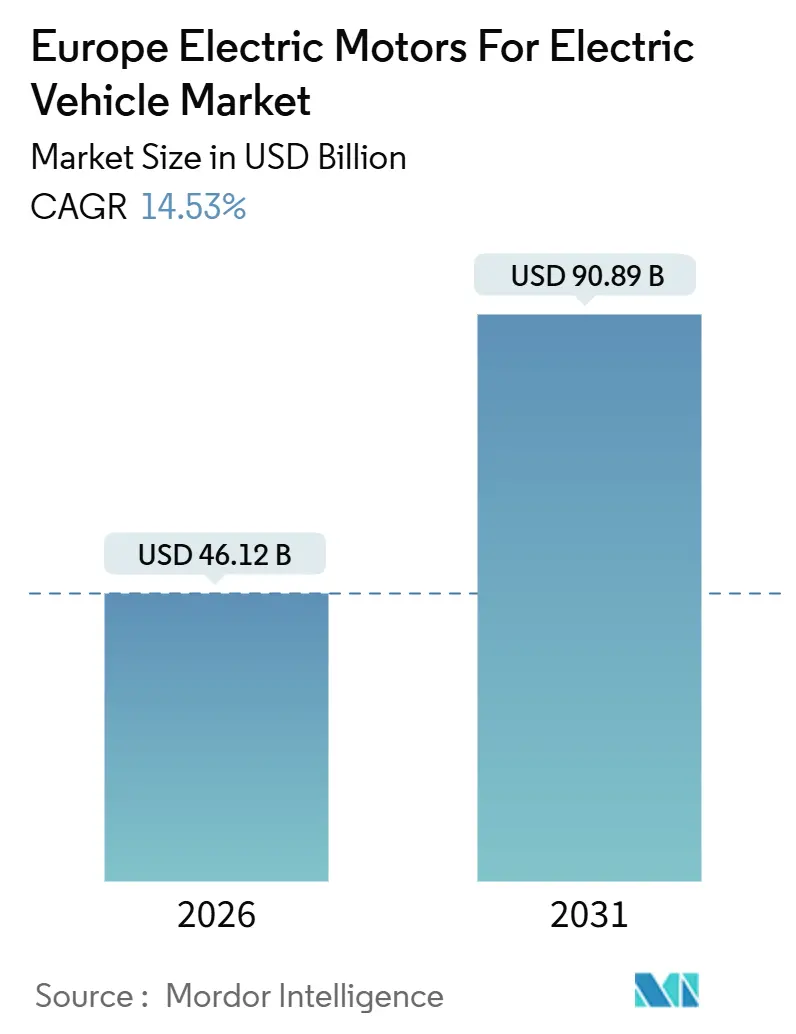

The European electric motor for the electric vehicle market stood at USD 46.12 billion in 2026 and is projected to reach USD 90.89 billion by 2031, advancing at a 14.53% CAGR during the forecast period. Tighter European Union fleet–average CO₂ limits, rapid battery cost deflation, and platform-level standardization by leading automakers are accelerating electric-motor demand at a pace that outstrips pure consumer-driven adoption. Persistent price swings in rare-earth materials are nudging OEMs to evaluate magnet-free motor designs; however, power-density requirements mean that permanent-magnet synchronous motors still dominate the volume. Rising investments in integrated e-drive production lines, especially those co-locating motor, inverter, and gearbox manufacturing, are compressing time-to-market and lowering landed costs. Germany currently leads regional revenue, but the expansion of Eastern Europe and government incentives in Spain and Poland are reshaping the supply chain footprint across the continent[1]“Regulation (EU) 2025/1214 on CO₂ Emission Performance Standards,” European Commission, europa.eu.

Key Report Takeaways

- By motor type, permanent-magnet synchronous motors held 58.71% of the European electric motor market share for the electric vehicle market in 2025, while switched-reluctance motors are forecast to climb at a 16.97% CAGR through 2031.

- By vehicle type, battery electric vehicles commanded 72.88% of the European electric motor market share for the electric vehicle market in 2025. In contrast, fuel-cell electric cars are expected to post the fastest growth rate of 19.81% through 2031.

- By application, passenger cars accounted for 64.78% of the European electric motor market share for the electric vehicle market in 2025, and off-road electric equipment is projected to expand at a 15.36% CAGR to 2031.

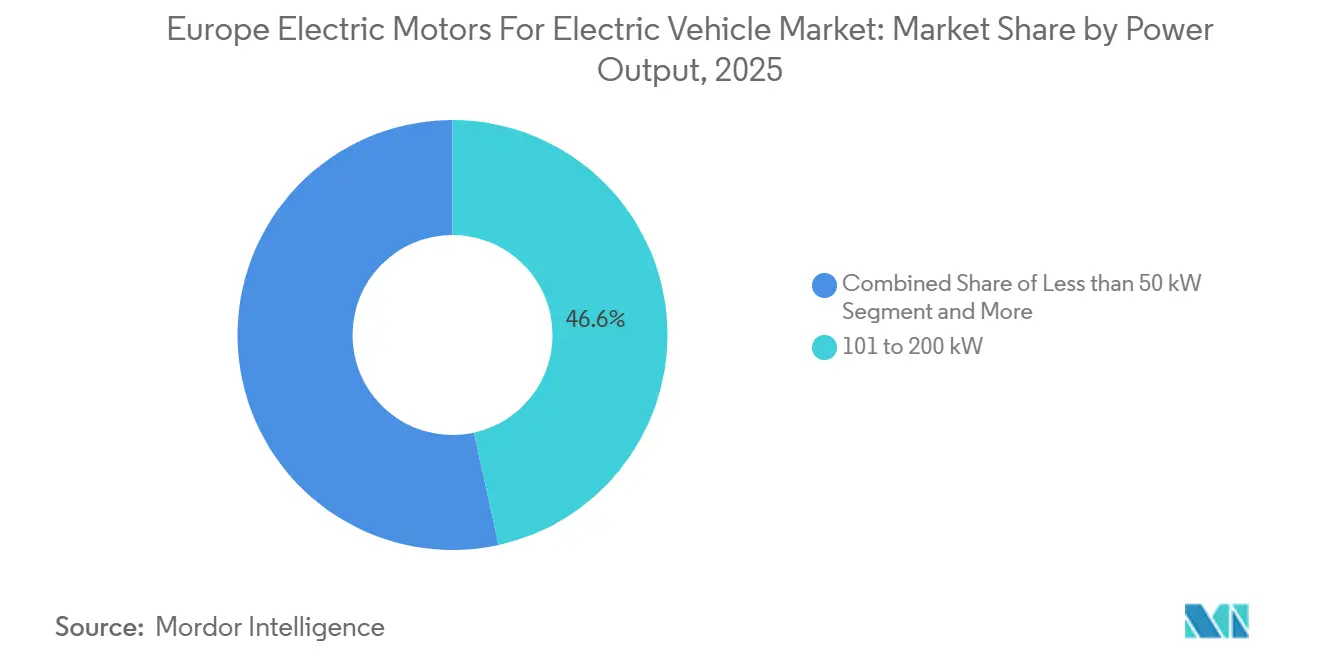

- By power output, the 101-to-200 kW bracket captured 46.56% of the European electric motor market share for the electric vehicle market in 2025, while motors above 400 kW are expected to advance at a 17.33% CAGR through 2031.

- By cooling method, liquid-cooled designs represented 62.76% of the European electric motor market share for the electric vehicle market in 2025 and are projected to track an 18.76% CAGR to 2031.

- By country, Germany led the European electric motor for the electric vehicle market with a 27.33% share in 2025; however, Poland is on track for the fastest growth, with a 16.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Electric Motors For Electric Vehicle Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU CO₂ Fleet-Average Targets | +3.2% | Germany, France, Italy, Spain, Netherlands, Belgium | Short term (≤ 2 years) |

| Decline in Battery USD/kWh | +2.8% | Germany, United Kingdom, France, Poland, Czech Republic | Medium term (2-4 years) |

| OEM Electrification Road-Maps | +2.5% | Germany, France, Spain, Italy, United Kingdom | Medium term (2-4 years) |

| Spain's 2024 PERTE VEC 2 Program | +1.8% | Spain, Portugal | Long term (≥ 4 years) |

| Demand from Retrofit E-Powertrains | +1.5% | United Kingdom, France, Germany, Italy, Netherlands | Short term (≤ 2 years) |

| AI-Driven Motor-Inverter Co-Design | +1.2% | Germany, Sweden, France, Austria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter EU CO₂ Fleet-Average Targets for 2025 and 2030

The European Union’s Regulation 2025/1214 lowered the 2025 fleet-average limit to 93.6 g CO₂/km till 2029 and set a 49.5 g CO₂/km ceiling for 2034, pairing steep non-compliance fines with the expiration of the super-credit mechanism at the end of 2025[2]"CO2 emissions performance of new passenger cars in Europe", European Environment Agency, eea.europa.eu. Automakers now accelerate BEV launches, irrespective of short-term profitability, because every percentage-point gap in the electric-vehicle mix can trigger hundreds of millions of euros in penalties. Platform production is therefore being front-loaded at factories in Zwickau, Emden, and Tychy, with suppliers scaling hairpin stator and rotor lines accordingly. The regulation effectively ties motor demand to statutory ceilings rather than consumer preference, pushing European electric motors for the electric vehicle market onto a policy-driven growth path.

Rapid Decline in Battery USD/kWh Enabling Affordable BEVs

Average pack prices slid from USD 153/kWh in 2022 to USD 111/kWh in 2024 and are on track to fall below USD 80/kWh by 2026. Crossing this threshold enables B- and C-segment BEVs to reach purchase-price parity with internal-combustion cars without subsidies, thereby expanding the potential motor customer base by tens of millions of vehicles. Renault’s 2025 R5 E-Tech launch at EUR 25,000 illustrates how lower battery costs free pricing headroom to specify higher-efficiency, 110 kW permanent-magnet motors. Component suppliers, meanwhile, have trimmed assembly labor per motor by nearly one-third, thanks to copper hairpin winding and integrated inverters. Yet the shift toward lithium-iron-phosphate batteries—with their lower energy density—requires motors to deliver better efficiency across a broader torque band, highlighting the delicate balance between cost, range, and rare-earth demand.

OEM Electrification Road-Maps and Platform Shifts

Volkswagen’s MEB, Stellantis’s STLA-Medium, and BMW’s Neue Klasse platforms standardize motor mountings, thermal interfaces, and inverter packaging to unlock economies of scale. For example, integrating silicon-carbide MOSFETs directly inside the motor housing has trimmed high-voltage cabling by more than a meter while increasing power density by roughly 30%. Design consolidation shifts the competitive advantage from bespoke motor geometry to manufacturing scale and thermal-management expertise, prompting Tier 1 suppliers to invest in multi-gigawatt lines across Germany, Spain, and Austria. Platform commonality also simplifies over-the-air updates that tweak torque curves within the same hardware envelope, converting software into a fresh battleground for differentiation. As more models ride on shared architectures, the European electric motors for the electric vehicle market reinforce its volume-driven cost curve and vertically integrate critical sub-assemblies.

Spain’s 2024 PERTE VEC 2 Program Anchoring New E-Drive Supply Chains

The EUR 3 billion program launched in 2024 channels public funds into Valencian and Aragonese clusters, subsidizing hairpin stator, rotor assembly, and coil laser-welding equipment. Vitesco and Schaeffler have already commissioned a combined nameplate capacity shortening logistics corridor to Iberian and southern French vehicle plants. Mandatory private co-investment ensures a long-term commitment, while a parallel workforce re-skilling initiative covers 12,000 technicians across Spain. Lead times for specialized insertion machinery nevertheless stretch to 18 months, creating a temporary bottleneck that slows complete capacity ramp-up until 2028. Even so, the initiative positions Spain as a pivotal production node and boosts regional resilience against supply-chain shocks.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility and Supply-Chain Risk | -1.5% | Germany, France, Italy, Spain, Poland, Czech Republic | Medium term (2-4 years) |

| High CAPEX | -1.3% | Germany, Spain, France, United Kingdom, Poland | Short term (≤ 2 years) |

| Grid Connection Queues | -0.9% | United Kingdom, Germany, Netherlands, Belgium | Short term (≤ 2 years) |

| Talent Shortage | -0.8% | Germany, France, Austria, Sweden, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rare-Earth Magnet Price Volatility and Supply-Chain Risk

Neodymium-praseodymium oxide peaked near USD 68,000 per metric ton in early 2025 before sliding to USD 54,000 by year-end, a 26% swing that destabilized quarterly gross margins for many Tier 1 suppliers. Forward contracts can cushion some volatility but carry hefty premiums, further squeezing profit. Substituting ferrite magnets reduces power density by up to 20%, necessitating design changes that few OEMs are willing to accept for mainstream passenger cars. Recycling initiatives in Saxony aim to recover 2,000 metric tons annually by 2028; however, this covers less than 5% of the projected European demand. Until domestic extraction or large-scale recycling becomes a viable option, magnet pricing remains a structural headwind.

High CAPEX for Advanced Hair-Pin Winding and Liquid-Cooling Lines

Transitioning from round-wire to hairpin stators requires an investment of EUR 8-12 million in automated insertion and laser-welding equipment per production line, while adding liquid-cooling capability pushes the investment past EUR 15 million for mid-volume facilities. Payback periods often exceed 24 months, a stretch for smaller Tier 2 firms. Once installed, these capital-intensive lines become geographically “sticky,” making relocation to lower-cost countries economically unviable over a 10-year depreciation cycle. The hurdle effectively raises barriers to entry and favors incumbents with stronger balance sheets, slowing the diffusion of next-generation winding technologies.

Segment Analysis

By Motor Type: PMSM Dominance Faces SRM Challenge

Permanent Magnet Synchronous Motors (PMSMs) commanded 58.71% of the European electric motor market share for the electric vehicle market in 2025, as their power density allows automakers to meet interior-space targets without resizing vehicle subframes. Induction motors are often used in dual-motor all-wheel-drive configurations, where their lower cost offsets the penalties associated with partial-load efficiency. BLDC units maintained a foothold in two- and three-wheelers due to their simplicity and compatibility with air cooling. At the same time, brushed DC motors have largely been replaced by BLDC units in mainstream automotive use. SRM volume is rising quickly—forecasted to increase at a 16.97% CAGR through 2031, because magnet-free designs hedge against rare-earth volatility.

SRM gains come with engineering trade-offs: higher torque ripple and acoustic noise demand sophisticated control algorithms that in turn require costlier silicon-carbide inverters. Nevertheless, suppliers unveiled 150 kW SRM prototypes that achieve over 90% rated-load efficiency, significantly narrowing the gap with PMSM. Induction motor adoption remains steady where battery packs exceed 75 kWh, as the impact on range is less severe. Overall, technology mix shifts will continue, yet PMSM remains the anchor of the European electric motors for the electric vehicle market through 2031.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: BEV Leadership, FCEV Momentum

BEVs absorbed 72.88% of the European electric motor market share for the electric vehicle market in 2025 on the strength of Volkswagen ID models, Stellantis platforms, and Tesla’s sustained Model Y sales. FCEVs are expanding at a 19.81% CAGR through 2031, lifted by hydrogen-refueling corridors that reached 250 stations across Germany, France, and the Netherlands. The PHEV share is eroding under stricter real-world CO₂ testing, prompting OEMs to reallocate their R&D budgets toward full-electric architectures. HEVs still serve regions with patchy charging networks but generate lower motor revenue because power ratings often stay below 50 kW.

FCEV motor design diverges from BEV norms: dual 180 kW liquid-cooled PMSMs compensate for the fuel-cell response lag in heavy-duty trucks, thereby increasing the average motor content per vehicle. BEVs continue to drive volume, but FCEV growth adds incremental upside and diversifies the demand profile within the European electric vehicle market.

By Application: Passenger Cars Lead, Off-Road Surges

Passenger cars accounted for 64.78% of the European electric motor market share for the electric vehicle market in 2025, mirroring Europe’s car-centric mobility patterns and the concentration of BEV releases in the C- and D-segments. Off-road and industrial EVs—such as electric excavators, wheel loaders, and port equipment—are projected to grow at a 15.36% CAGR through 2031, as urban construction and harbor authorities impose zero-tailpipe emissions mandates. E-commerce fleet electrification pledges propel the share of commercial vans and medium trucks. Two-wheelers and three-wheelers clustered in southern urban centers.

Harsh operating conditions in off-road segments favor ruggedized induction motors with IP67 enclosures, while passenger-car motors prioritize compactness and efficiency. Commercial-vehicle stop-start cycles create thermal spikes, driving adoption of active cooling even for sub-100 kW units. These nuanced duty-cycle differences make application segmentation a key lens through which to forecast the European electric motor market size across sub-verticals for the electric vehicle market.

By Power Output: Mid-Range Dominates, High-Power Accelerates

Motors rated 101-200 kW captured 46.56% of the European electric motor market share for the electric vehicle market in 2025, as they meet acceleration benchmarks for mainstream C-segment cars without incurring the premium costs associated with vehicles of this class. Units above 400 kW, essential for heavy-duty trucks and articulated buses, are the fastest-growing slice at a 17.33% CAGR through 2031, albeit from a smaller base. The 51-100 kW bracket serves entry-level BEVs and urban delivery vans, where cost sensitivities dictate air-cooled architectures.

Thermal management becomes the primary design constraint beyond 250 kW, necessitating the use of oil-spray or direct liquid-cooled stator windings to prevent magnet demagnetization. Silicon-carbide inverters now unlock peak efficiencies of 98% or higher, even at 550 kW, enabling OEMs to maintain range without oversizing battery packs. These high-power advances expand the upper boundary of Europe's electric motors for the electric vehicle market size as commercial applications electrify.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Cooling Method: Liquid Cooling Ascends

Liquid-cooled motors held 62.76% of the European electric motor market share for the electric vehicle market in 2025 and are on track for an 18.76% CAGR through 2031, a trajectory tied to rising continuous power demands above 150 kW. Air-cooled designs retain 37.24% share, focusing on vehicles below 100 kW where bill-of-materials savings of USD 400-600 per unit remain decisive. Above 150 kW, air cooling necessitates oversized stators, which add up to 6 kg of copper and steel, thereby nullifying any weight advantages.

Liquid cooling’s complexity introduces a leak risk and parasitic power draw of roughly 150-200 W; yet, the 20-25% volume reduction it permits frees valuable packaging space for larger battery packs. Southern Europe’s high ambient temperatures further tilt the balance toward liquid-cooled systems, reinforcing a structural shift already underway in the European electric motor market for electric vehicles.

Geography Analysis

Germany accounted for 27.33% of the European electric motor market share for the electric vehicle market in 2025, leveraging Volkswagen’s Zwickau and Emden plants, BMW’s Munich R&D center, and a dense supplier base that enables rapid prototyping and validation cycles. Proximity between engineering and production shortens development timelines by as much as nine months, making Germany a vital hub in the European electric motor market for electric vehicles. Poland is emerging as the fastest-growing geography with a 16.27% CAGR through 2031, driven by Stellantis’s Tychy electrification, LG Energy Solution’s cell capacity ramp-up, and lower labor costs that compress landed cost per motor by double-digit percentages. France follows, anchored by Renault’s vertically integrated ElectriCity complex, which co-locates battery, motor, and final assembly under one roof, significantly reducing logistics buffers.

The United Kingdom retained a significant portion of volume despite post-Brexit tariff uncertainty, due to high localization at Nissan Sunderland and the presence of supply-chain clusters in the Northeast. Italy benefits from Stellantis' investments in Melfi and Mirafiori, while Spain leverages PERTE VEC 2 subsidies to attract new motor component lines. A “rest-of-Europe” cohort—comprising the Czech Republic, Hungary, Romania, and Slovakia — primarily serves just-in-sequence shipments into German vehicle plants.

Germany’s dominance is underpinned by workforce expertise and infrastructure maturity, yet rising wage costs are encouraging suppliers to diversify eastward. Poland’s grid, which is still reliant on coal for more than 60% of its generation, pushes industrial electricity prices above German averages, partly eroding its labor-cost advantage. France’s integrated supply chain reduces working-capital requirements, bolstering project cash flow and making it an attractive blueprint for other countries. Spain’s ramp-up timeline means its full capacity effect will not materialize until the next decade. Still, early indicators suggest a durable southward shift in the European electric motor market for electric vehicles.

Competitive Landscape

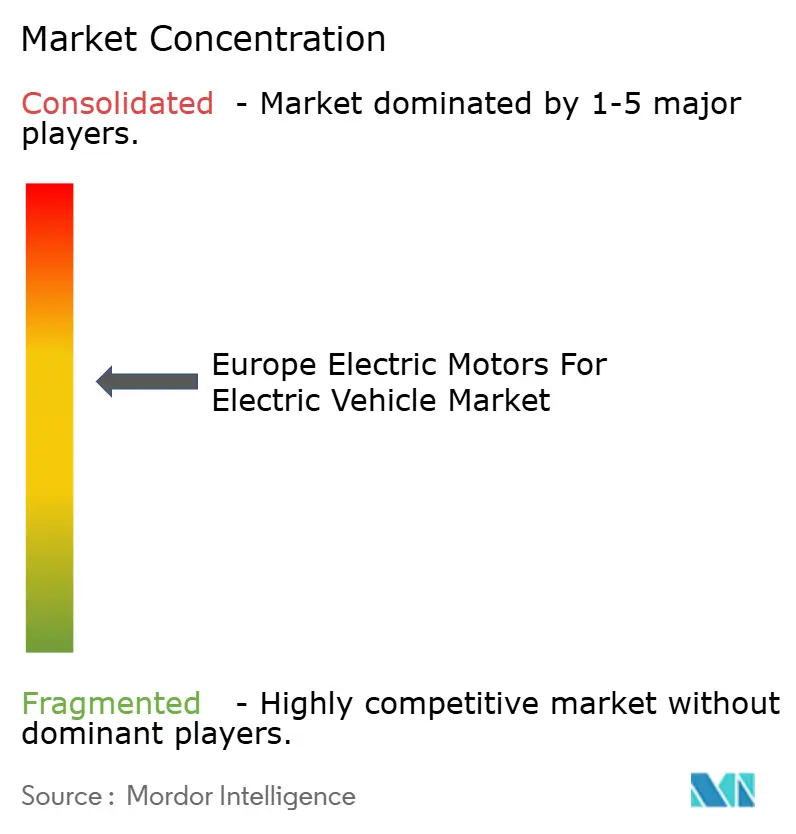

The European electric motor market for electric vehicles exhibits moderate concentration, with Robert Bosch GmbH, Siemens AG, ZF Friedrichshafen AG, Valeo SA, and Nidec Corporation collectively accounting for the majority of the 2025 revenue. Tier 1 integrators increasingly bundle inverter and gearbox functions into a single e-drive, capturing more value per unit and tightening supplier-OEM collaboration. YASA’s axial-flux motor, adopted by Mercedes-Benz AMG models in 2025, delivers significantly higher torque density than radial-flux designs, signaling that topology innovation remains a potent disruptor.

In-wheel motor specialists, such as Elaphe and Protean, target urban vehicles where eliminating half-shafts offsets the added unsprung mass; however, adoption remains niche due to ride-quality penalties at higher speeds. Retrofit-kit providers have carved out a high-margin aftermarket for commercial vans, serving fleet operators who are keen to comply with low-emission zone mandates without purchasing new vehicles. Intellectual property filings underscore the innovation race: the European Patent Office logged 347 electric motor control applications in 2025, reflecting intensified R&D competition.

Regulatory shifts also shape strategy. The EU’s Ecodesign for Sustainable Products Regulation, effective in 2026, requires detailed disassembly roadmaps and verification of recycled content, favoring suppliers with robust reverse logistics and recycling partnerships. Rare-earth price volatility is prompting larger players to integrate vertically into magnet production, while smaller entrants diversify into switched-reluctance architectures to minimize their exposure. These dynamics collectively sustain a competitive yet consolidating landscape across the European electric motor market for electric vehicles.

Europe Electric Motors For Electric Vehicle Industry Leaders

-

Robert Bosch GmbH

-

Siemens AG

-

Valeo SA

-

ZF Friedrichshafen AG

-

Nidec Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: BMW Group Plant Steyr started series production of Gen-6 e-motors for Neue Klasse models, shipping the fully electric drivetrain across BMW’s global network.

- February 2025: Renault Group, Valeo, Siemens eAutomotive, and Valeo announced that they signed a memorandum of understanding to form a strategic partnership for designing, manufacturing, and co-development of automotive electric motors for electric vehicles in France.

- January 2025: Nissan has introduced the latest evolution of its e-POWER drivetrain in Europe, offering an electric-drive experience that eliminates the need for plug-in charging.

Europe Electric Motors For Electric Vehicle Market Report Scope

An electric vehicle is a vehicle that is either partially or fully powered by electricity and is propelled by one or more electric motors, using only the energy stored in batteries. The vehicle's electric motor is powered by a massive traction battery pack that must be connected to a wall outlet or charging equipment, commonly known as electric vehicle supply equipment (EVSE).

The electric motors for the electric vehicle market are segmented by motor type, vehicle type, application, power output, cooling method, and country. By motor type, the market is segmented into DC Brushed Motors, DC Brushless Motors (BLDC), Induction Motors (AC), Permanent Magnet Synchronous Motors (PMSM), and Switched Reluctance Motors (SRM). By vehicle type, the market is segmented into Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (HEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Fuel Cell Electric Vehicles (FCEVs). By application, the market is segmented into Two-Wheelers, Three-Wheelers, Passenger Cars, Commercial Vehicles, and Off-Road / Industrial EVs. By power output, the market is segmented into Less than 50 kW, 51 to 100 kW, 101 to 200 kW, 201 to 400 kW, and Above 400 kW. By cooling method, the market is segmented into Air-Cooled Motors and Liquid-Cooled Motors. By country, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe. The market forecasts are provided in terms of value (USD) and volume (Units).

By Motor Type

| DC Brushed Motors |

| DC Brushless Motors (BLDC) |

| Induction Motors (AC) |

| Permanent Magnet Synchronous Motors (PMSM) |

| Switched Reluctance Motors (SRM) |

By Vehicle Type

| Battery Electric Vehicles (BEVs) |

| Hybrid Electric Vehicles (HEVs) |

| Plug-in Hybrid Electric Vehicles (PHEVs) |

| Fuel Cell Electric Vehicles (FCEVs) |

By Application

| Two-Wheelers |

| Three-Wheelers |

| Passenger Cars |

| Commercial Vehicles |

| Off-Road / Industrial EVs |

By Power Output

| Less than 50 kW |

| 51 to 100 kW |

| 101 to 200 kW |

| 201 to 400 kW |

| Above 400 kW |

By Cooling Method

| Air-Cooled Motors |

| Liquid-Cooled Motors |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Motor Type | DC Brushed Motors |

| DC Brushless Motors (BLDC) | |

| Induction Motors (AC) | |

| Permanent Magnet Synchronous Motors (PMSM) | |

| Switched Reluctance Motors (SRM) | |

| By Vehicle Type | Battery Electric Vehicles (BEVs) |

| Hybrid Electric Vehicles (HEVs) | |

| Plug-in Hybrid Electric Vehicles (PHEVs) | |

| Fuel Cell Electric Vehicles (FCEVs) | |

| By Application | Two-Wheelers |

| Three-Wheelers | |

| Passenger Cars | |

| Commercial Vehicles | |

| Off-Road / Industrial EVs | |

| By Power Output | Less than 50 kW |

| 51 to 100 kW | |

| 101 to 200 kW | |

| 201 to 400 kW | |

| Above 400 kW | |

| By Cooling Method | Air-Cooled Motors |

| Liquid-Cooled Motors | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What was the Europe electric motors for electric vehicle market size in 2026?

The market reached USD 46.12 billion in 2026 and is projected to rise to USD 90.89 billion by 2031.

Which motor technology currently leads adoption?

Permanent-magnet synchronous motors held 58.71% of 2025 installations, making them the dominant technology in the region.

Which country is growing fastest for electric-motor production?

Poland shows the highest 2026-2031 CAGR at 16.27% due to new OEM platforms and battery-cell capacity additions.

Why are liquid-cooled motors gaining share?

Rising continuous power requirements above 150 kW favor liquid cooling because it removes heat more efficiently, allowing smaller, lighter designs that improve vehicle packaging.

How does rare-earth price volatility impact suppliers?

Swings in neodymium-praseodymium oxide prices can compress quarterly gross margins by several hundred basis points, prompting forward-contracting and exploration of magnet-free architectures.