Market Size of europe dog food Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

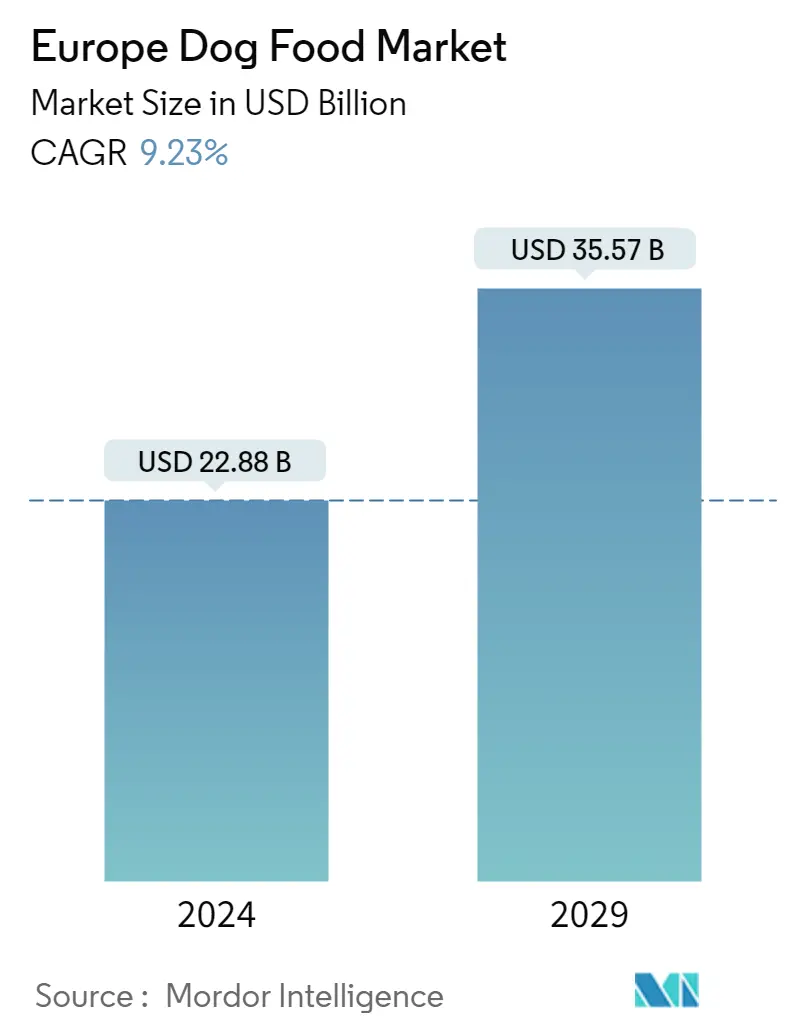

Market Size (2024) | USD 22.88 Billion |

|

|

Market Size (2029) | USD 35.57 Billion |

|

|

Largest Share by Pet Food Product | Food |

|

|

CAGR (2024 - 2029) | 9.23 % |

|

|

Largest Share by Country | United Kingdom |

|

|

Market Concentration | Medium |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

Europe Dog Food Market Analysis

The Europe Dog Food Market size is estimated at USD 22.88 billion in 2024, and is expected to reach USD 35.57 billion by 2029, growing at a CAGR of 9.23% during the forecast period (2024-2029).

22.88 Billion

Market Size in 2024 (USD)

35.57 Billion

Market Size in 2029 (USD)

7.14 %

CAGR (2017-2023)

9.23 %

CAGR (2024-2029)

Largest Market by Product

67.49 %

value share, Food, 2022

The expanding dog ownership rates and availability of wider dog food options with custom-made dry and wet dog foods from various companies have boosted the segment's growth.

Largest Market by Country

16.07 %

value share, United Kingdom, 2022

The high dog owing population, strong distribution networks, wide company presence, and high consumer spending have contributed to its leading position in the region.

Fastest-growing Market by Product

9.91 %

Projected CAGR, Pet Veterinary Diets, 2023-2029

Growing dog health concerns, the prevalence of chronic diseases, and rising demand for specialized pet nutrition are likely to bolster the segment's demand during the forecast period.

Fastest-growing Market by Country

15.61 %

Projected CAGR, Poland, 2023-2029

The increasing adoption of dogs and the growing power of consumers to spend more on premium and nutritional dog foods in the country are driving the growth of the market.

Leading Market Player

19.29 %

market share, Mars Incorporated, 2022

It is the market leader due to its many product launches that are formulated with specialized ingredients and the expansion of its manufacturing facilities in the region.

Food products and treats were dominating the market due to their regular usage, while veterinary diets comprised the fastest-growing segment

- In 2022, the dog food market accounted for 40.8% of the European pet food market. There was a significant increase of 42% compared to 2017, mainly due to the increased number of dog owners and the growing demand for premium products in the region. The dog population grew by 14.2% in 2022 compared to 2017. The major market shares in 2022 were held by the United Kingdom, Germany, and Russia, accounting for 16.1%, 12.5%, and 9.4%, respectively.

- The food product segment is the largest in the dog food market, and it was valued at USD 13.15 billion in 2022. Dry food is the most popular type of dog food, valued at USD 9.88 billion in 2022. Dog owners prefer dry food because of its longer shelf life and lower cost per serving, making it more convenient and economical to purchase in bulk.

- Treats comprise the second-largest segment of dog food, and they were valued at USD 3.54 billion in 2022. Treats are given to dogs with their regular food to provide additional health benefits, such as aiding digestion and promoting healthy skin and coat. They are also commonly used as training rewards.

- Dog veterinary diets were valued at USD 2.05 billion in the market in 2022. This segment is projected to be the fastest growing, registering a CAGR of 8.4% during the forecast period. The increasing prevalence of digestive issues and chronic kidney diseases in dogs has contributed to the growth of this segment.

- The pet nutraceuticals segment grew by 19.1% in 2022 compared to 2017, driven by the increased awareness of healthy diets, particularly due to rising health concerns in dogs. The market is being driven by the increasing dog population, the specific health needs of dogs, and the growing awareness of pet health among dog owners. It is projected to record a CAGR of 7.8% during 2023-2029.

The United Kingdom is the major market in the region, while Poland and Russia are the fastest-growing markets

- The European dog food market is witnessing substantial growth, primarily driven by the rising population of pet dogs in the region. The countries with significant dog populations in Europe include Russia, the United Kingdom, Germany, and Spain. Between 2017 and 2021, the European dog food market experienced an increase of about 28.0%, mainly attributed to the growing number of pet dogs, which rose from 84.9 million in 2017 to 97.0 million in 2022.

- Among European countries, the United Kingdom emerged as the largest dog food market, representing around 16.1% of the total market value, i.e., USD 3.13 billion in 2022. The dominance of the United Kingdom can be primarily attributed to high expenditure on dogs. For instance, the average pet expenditure per dog in the United Kingdom stood at USD 646.2 in 2022, the highest among all European countries.

- Germany held about 12.5% of the European dog food market in 2022. The country had a dog population of about 10.6 million, accounting for around 11.0% of the total European dog population in the same year. With the growing dog population and an increasing trend of pet humanization, the German dog food market is anticipated to register a steady CAGR of 3.5% during the forecast period.

- Although Russia held the largest dog population in the region, it only accounted for 9.4% of the market in 2022. This disparity can be attributed to comparatively lower pet expenditure on dogs in the country. The ongoing Ukraine-Russia War has also had a negative impact on the Russian dog food market.

- However, the increasing dog population and pet humanization are the factors anticipated to drive the market during the forecast period.

Europe Dog Food Industry Segmentation

Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets are covered as segments by Pet Food Product. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel. France, Germany, Italy, Netherlands, Poland, Russia, Spain, United Kingdom are covered as segments by Country.

- In 2022, the dog food market accounted for 40.8% of the European pet food market. There was a significant increase of 42% compared to 2017, mainly due to the increased number of dog owners and the growing demand for premium products in the region. The dog population grew by 14.2% in 2022 compared to 2017. The major market shares in 2022 were held by the United Kingdom, Germany, and Russia, accounting for 16.1%, 12.5%, and 9.4%, respectively.

- The food product segment is the largest in the dog food market, and it was valued at USD 13.15 billion in 2022. Dry food is the most popular type of dog food, valued at USD 9.88 billion in 2022. Dog owners prefer dry food because of its longer shelf life and lower cost per serving, making it more convenient and economical to purchase in bulk.

- Treats comprise the second-largest segment of dog food, and they were valued at USD 3.54 billion in 2022. Treats are given to dogs with their regular food to provide additional health benefits, such as aiding digestion and promoting healthy skin and coat. They are also commonly used as training rewards.

- Dog veterinary diets were valued at USD 2.05 billion in the market in 2022. This segment is projected to be the fastest growing, registering a CAGR of 8.4% during the forecast period. The increasing prevalence of digestive issues and chronic kidney diseases in dogs has contributed to the growth of this segment.

- The pet nutraceuticals segment grew by 19.1% in 2022 compared to 2017, driven by the increased awareness of healthy diets, particularly due to rising health concerns in dogs. The market is being driven by the increasing dog population, the specific health needs of dogs, and the growing awareness of pet health among dog owners. It is projected to record a CAGR of 7.8% during 2023-2029.

| Pet Food Product | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

| Distribution Channel | |

| Convenience Stores | |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

| Country | |

| France | |

| Germany | |

| Italy | |

| Netherlands | |

| Poland | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe |

Europe Dog Food Market Size Summary

The European dog food market is experiencing significant growth, driven by an increasing dog population and a rising demand for premium pet products. The market is characterized by a strong preference for dry dog food due to its cost-effectiveness and convenience. The United Kingdom, Germany, and Russia are key players in this market, with the UK leading in terms of market share, attributed to high pet expenditure. The market is also seeing a shift towards specialized diets, such as veterinary diets, which are gaining popularity due to the growing awareness of dog health issues. The trend of pet humanization is further fueling the market, as pet owners are more inclined to spend on high-quality and nutritious food for their dogs.

The market landscape is moderately consolidated, with major companies like Mars Incorporated, Nestle (Purina), and Colgate-Palmolive Company (Hill's Pet Nutrition Inc.) dominating the scene. The pandemic has accelerated the shift towards online sales channels, with e-commerce platforms like Amazon gaining significant traction in pet food sales. Innovations in pet food products, such as those introduced by Hill's Pet Nutrition and Mars Incorporated, are catering to specific health needs of dogs, enhancing the market's growth prospects. The increasing pet expenditure, driven by the premiumization of pet food and the growing awareness of pet health, is expected to continue supporting the market's expansion in the coming years.

Europe Dog Food Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Pet Food Product

-

1.1.1 Food

-

1.1.1.1 By Sub Product

-

1.1.1.1.1 Dry Pet Food

-

1.1.1.1.1.1 By Sub Dry Pet Food

-

1.1.1.1.1.1.1 Kibbles

-

1.1.1.1.1.1.2 Other Dry Pet Food

-

-

-

1.1.1.1.2 Wet Pet Food

-

-

-

1.1.2 Pet Nutraceuticals/Supplements

-

1.1.2.1 By Sub Product

-

1.1.2.1.1 Milk Bioactives

-

1.1.2.1.2 Omega-3 Fatty Acids

-

1.1.2.1.3 Probiotics

-

1.1.2.1.4 Proteins and Peptides

-

1.1.2.1.5 Vitamins and Minerals

-

1.1.2.1.6 Other Nutraceuticals

-

-

-

1.1.3 Pet Treats

-

1.1.3.1 By Sub Product

-

1.1.3.1.1 Crunchy Treats

-

1.1.3.1.2 Dental Treats

-

1.1.3.1.3 Freeze-dried and Jerky Treats

-

1.1.3.1.4 Soft & Chewy Treats

-

1.1.3.1.5 Other Treats

-

-

-

1.1.4 Pet Veterinary Diets

-

1.1.4.1 By Sub Product

-

1.1.4.1.1 Diabetes

-

1.1.4.1.2 Digestive Sensitivity

-

1.1.4.1.3 Oral Care Diets

-

1.1.4.1.4 Renal

-

1.1.4.1.5 Urinary tract disease

-

1.1.4.1.6 Other Veterinary Diets

-

-

-

-

1.2 Distribution Channel

-

1.2.1 Convenience Stores

-

1.2.2 Online Channel

-

1.2.3 Specialty Stores

-

1.2.4 Supermarkets/Hypermarkets

-

1.2.5 Other Channels

-

-

1.3 Country

-

1.3.1 France

-

1.3.2 Germany

-

1.3.3 Italy

-

1.3.4 Netherlands

-

1.3.5 Poland

-

1.3.6 Russia

-

1.3.7 Spain

-

1.3.8 United Kingdom

-

1.3.9 Rest of Europe

-

-

Europe Dog Food Market Size FAQs

How big is the Europe Dog Food Market?

The Europe Dog Food Market size is expected to reach USD 22.88 billion in 2024 and grow at a CAGR of 9.23% to reach USD 35.57 billion by 2029.

What is the current Europe Dog Food Market size?

In 2024, the Europe Dog Food Market size is expected to reach USD 22.88 billion.