| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| CAGR | 4.84 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Distribution Transformer Market Analysis

The Europe Distribution Transformer Market is expected to register a CAGR of 4.84% during the forecast period.

The European power infrastructure landscape is undergoing significant transformation driven by the region's ambitious energy transition goals and grid modernization initiatives. According to the International Renewable Energy Agency (IRENA), as of 2022, the European region accounted for more than 21% of the total installed renewable energy capacity globally, highlighting its position as a leader in clean energy adoption. The European Union has demonstrated its commitment to accelerating the clean energy transition through recent policy developments, including the March 2023 provisional agreement to raise the EU's binding renewable target to 42.5% by 2030. This regulatory framework is reshaping the distribution transformer and electrical transformer infrastructure requirements across the region.

The industrial sector's recovery and expansion are creating additional demands on the power distribution equipment and electrical distribution equipment. According to the Federal Statistical Office, German industrial production experienced a notable increase of 2.0% in April 2023, primarily driven by the automotive manufacturing sector. This industrial growth is coinciding with significant investments in grid modernization, as evidenced by Siemens Energy's April 2023 contract to supply electric components for power transmission in three grid connections in the North Sea, representing a substantial EUR 7 billion investment in transmission infrastructure.

The residential and commercial sectors are emerging as key drivers of distribution transformer demand. According to Eurostat, investment in the European residential market accounted for about 5.7% of GDP in 2022, indicating robust construction activity and corresponding infrastructure requirements. This trend is complemented by the increasing adoption of smart grid technologies, as demonstrated by Harmony Energy's February 2023 entry into the French battery storage market with a 100 MW project and EUR 30 million investment in research facilities in Grenoble and Nantes.

The distribution transformer market is witnessing technological evolution with the integration of digital capabilities and smart transformer features. Major industry players are introducing advanced monitoring solutions, as exemplified by GE Grid Solutions' launch of new transformer monitoring technologies at CIGRE Session 2022. These innovations are being driven by the need for greater grid reliability and efficiency, particularly as the power transformer network becomes more complex with the integration of distributed energy resources. The trend towards digitalization is further supported by substantial investments in grid modernization, with European utilities expected to double their annual grid investments to EUR 85 billion by 2025.

Europe Distribution Transformer Market Trends

Rising Renewable Energy Generation

Europe is experiencing a significant transition in its electricity infrastructure modernization and expansion, primarily driven by the increasing integration of renewable energy sources. This aligns with the region's focus on becoming the world's first climate-neutral continent by 2050. According to the International Renewable Energy Agency (IRENA), as of 2022, the European region accounted for more than 21% of the total installed renewable energy capacity globally, with wind and solar representing the majority of this installed capacity. The substantial presence of renewable energy installations necessitates robust distribution transformer infrastructure to manage the intermittent nature of these power sources and ensure stable grid operations.

In March 2023, the European Union strengthened its commitment to renewable energy by raising the binding renewable target for 2030 to a minimum of 42.5%, a significant increase from the previous 32% target. This ambitious goal requires massive scaling-up and acceleration of renewable energy deployment across power generation, industry, buildings, and transport sectors. According to the European Commission, the region invested around EUR 40 billion annually in electricity grids as of 2021, but these investments need to double by 2025 to achieve the EU's Green Deal objectives. The power grid infrastructure represents 18% of all necessary investments required to transform the EU energy system, highlighting the critical role of distribution transformers in facilitating this transition.

The REPowerEU plan, launched in March 2023 as a response to the need for energy independence, aims to increase renewable energy capacity to nearly 1,236 GW by 2030. This massive expansion of renewable energy capacity will require significant investments in grid infrastructure, including grid transformers and power transformers, to effectively integrate and distribute the generated power. Distribution transformers play a crucial role in this transition by enabling the connection of renewable energy sources to the grid, managing voltage levels, and ensuring efficient power distribution to end-users. The transformers must handle the variable nature of renewable energy generation while maintaining grid stability and power quality, making them essential components in Europe's renewable energy infrastructure. Additionally, the integration of electrical transformers and other power distribution equipment is vital to support the evolving energy landscape.

Understand The Key Trends Shaping This Market

Download PDF

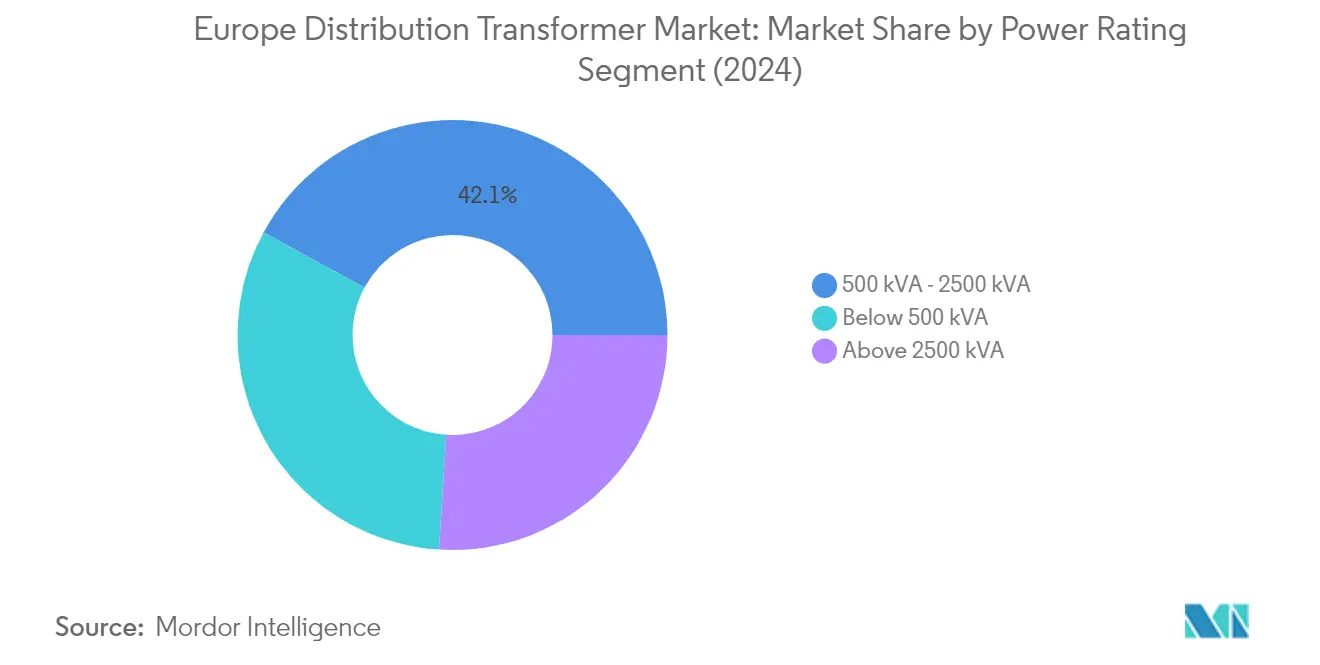

Segment Analysis: By Power Rating

500 kVA - 2500 kVA Segment in Europe Distribution Transformer Market

The 500 kVA - 2500 kVA segment dominates the Europe distribution transformer market, holding approximately 42% market share in 2024. This segment's prominence is primarily driven by its widespread application in various industrial sectors, including textile, automotive, pharmaceutical, metal, power, and food industries. The segment also finds significant usage in the oil and gas industry, covering both offshore and onshore platforms, refineries, and pipelines. The substantial market share can be attributed to the growing investments and expansion plans in manufacturing facilities across Europe, particularly in the automotive sector where companies are increasingly focusing on electric vehicle production facilities. The segment's dominance is further reinforced by the rising demand from data centers and large commercial establishments that require higher power capacity transformers for reliable operations.

Above 2500 kVA Segment in Europe Distribution Transformer Market

The Above 2500 kVA segment is projected to witness the fastest growth in the Europe distribution transformer market during the forecast period 2024-2029, with an expected growth rate of approximately 6%. This accelerated growth is primarily driven by the increasing integration of renewable energy sources into the power grid and the expansion of high-capacity industrial applications. The segment's growth is further supported by Europe's ambitious emission reduction targets and the subsequent need for large-capacity transformers to handle power from renewable sources such as wind farms and solar installations. The modernization and expansion of grid infrastructure, particularly in countries like Germany and the United Kingdom, coupled with the growing number of utility-scale renewable energy projects, are creating substantial demand for high-capacity transformers in this segment.

Remaining Segments in Power Rating Segmentation

The Below 500 kVA segment plays a crucial role in the Europe distribution transformer market, primarily serving residential and small commercial applications. This segment is particularly important in urban development projects and the electrification of residential areas. These transformers are commonly deployed for applications with lower power requirements, such as residential buildings, small commercial complexes, and industrial lighting. The segment's significance is enhanced by the growing trend of distributed energy generation and the increasing adoption of rooftop solar installations in residential areas. The segment also supports various small-scale industrial applications and public infrastructure projects, making it an essential component of the overall market landscape.

Segment Analysis: By Cooling Type

Oil-Cooled Segment in Europe Distribution Transformer Market

The oil-cooled transformer segment dominates the European distribution transformer market, holding approximately 81% market share in 2024. Oil-cooled transformers are predominantly used in outdoor spaces with capacities of 50 MVA and above due to their superior heat absorption and dissipation capabilities. These transformers are particularly vital for handling larger electrical loads and are extensively deployed as pad mounted transformer, power, and industrial transformers. The segment's prominence is driven by several advantages including lower procurement costs (typically 1.5 to 2 times less than dry transformers of similar capacity) and superior heat dissipation properties. The segment is also experiencing the fastest growth trajectory, supported by increasing electricity demand in the European region and the expansion of power grid facilities. Major governments across the region are significantly investing in expanding power grid infrastructure, with companies like German grid firm Amprion announcing plans to invest around EUR 22 billion in its power transmission network over five years, driving the demand for oil-cooled transformers.

Air-Cooled Segment in Europe Distribution Transformer Market

The air-cooled (dry-type) transformer segment plays a crucial role in the European distribution transformer market, particularly in indoor applications and environmentally sensitive areas. These transformers are extensively utilized in various applications ranging from residential buildings to small commercial complexes, offering advantages such as lower maintenance requirements and reduced environmental impact. The segment's growth is primarily driven by the increasing focus on renewable energy integration, particularly in countries like Germany, which aims to generate most of its electricity from renewable sources by 2050. The air-cooled transformers' environmentally friendly characteristics and superior safety features, including lower fire risk and absence of oil leakage concerns, make them particularly attractive for indoor installations in buildings, airports, stadiums, hotels, shopping malls, chemical plants, and refineries.

Segment Analysis: By Phase

Three-Phase Segment in Europe Distribution Transformer Market

The three-phase segment dominates the Europe distribution transformer market, commanding approximately 75% of the total market share in 2024. This segment's prominence is primarily driven by its widespread application in industrial and commercial sectors with heavy load requirements, such as data centers and housing apartments where the cumulative load requirement is high. Three-phase transformers offer significant advantages including better conductor efficiency, lower labor costs for installation and maintenance, and higher power load capabilities. The segment is expected to maintain its market leadership while growing at nearly 5% annually from 2024 to 2029, driven by increasing urbanization, rapid expansion of data centers across major European cities, and growing industrial power requirements. The growth is further supported by the segment's ability to handle applications requiring more than 1,000 kW power requirements, making it essential for large-scale industrial operations and commercial facilities.

Single-Phase Segment in Europe Distribution Transformer Market

The single-phase segment serves as a crucial component in the Europe distribution transformer market, primarily catering to applications with lower power requirements, typically up to 1,000 kW. This segment plays a vital role in residential and light commercial applications, where power demands are relatively modest. Single-phase transformers are particularly valuable in rural electrification projects and areas with dispersed populations due to their compact size and ability to be switched on and off based on load demand. The segment's significance is enhanced by the growing trend of distributed energy resources, especially in residential solar installations and small-scale renewable energy projects. The increasing adoption of smart lighting systems, particularly in countries like Italy where significant investments are being made in public lighting infrastructure, continues to drive demand for single-phase transformers. Additionally, these transformers are essential for various applications including industrial lighting, home inverters, and light commercial loads, making them indispensable for last-mile power distribution.

Segment Analysis: By Application

Power Sector Segment in Europe Distribution Transformer Market

The power sector segment continues to dominate the Europe distribution transformer market, holding approximately 47% market share in 2024. This significant market position is driven by the massive investments in grid modernization and expansion projects across Europe. The segment's growth is further supported by increasing integration of renewable energy sources into power grids, particularly wind and solar power installations. European utilities are actively upgrading their networks with advanced low voltage transformer technologies to handle intermittent renewable power generation and ensure grid stability. The power sector's dominance is also reinforced by various government initiatives promoting clean energy transition and grid resilience. Additionally, the implementation of smart grid technologies and the need to replace aging power infrastructure contribute substantially to the segment's market leadership.

Industrial Segment in Europe Distribution Transformer Market

The industrial segment is projected to exhibit the highest growth rate of approximately 6% during the forecast period 2024-2029. This accelerated growth is primarily attributed to the rapid industrialization and the increasing adoption of automation technologies across European manufacturing facilities. The segment's expansion is further driven by the growing demand for reliable power supply in critical industrial applications, including automotive manufacturing, chemical processing, and data centers. The industrial sector's transition towards energy-efficient operations and the integration of Industry 4.0 technologies are creating additional demand for advanced medium voltage transformer solutions. Moreover, the segment's growth is supported by increasing investments in industrial infrastructure modernization and the establishment of new manufacturing facilities across Europe.

Remaining Segments in Europe Distribution Transformer Market by Application

The telecom and other applications segments, including tramway systems, also play crucial roles in shaping the European distribution transformer market. The telecom segment's growth is primarily driven by the ongoing expansion of 5G infrastructure and the increasing number of data centers across Europe. The deployment of cast resin transformer solutions in telecom applications ensures reliable power supply for critical communication infrastructure. Meanwhile, the other applications segment, which includes tramway systems and electric vehicle charging infrastructure, is gaining prominence due to the increasing focus on sustainable urban transportation solutions and the rapid adoption of electric vehicles across European cities. These segments collectively contribute to the market's diversification and overall growth potential.

Europe Distribution Transformer Market Geography Segment Analysis

Distribution Transformer Market in Germany

Germany dominates the European distribution transformer market, holding approximately 16% market share in 2024. The country's robust power infrastructure and ambitious renewable energy integration targets have positioned it as a key market for distribution transformers. Germany's commitment to transitioning to a low-carbon economy, particularly through its plan to reduce emissions by at least 65% by 2030, has significantly influenced the demand for distribution transformers. The industrial sector, being one of the world's leading industrial economies, drives substantial demand through its diverse manufacturing base spanning automotive, machinery, chemicals, and electronics sectors. The country's focus on grid modernization and the integration of renewable energy sources, particularly wind and solar power, necessitates advanced distribution transformer solutions. Additionally, Germany's emphasis on electric vehicle infrastructure development and the expansion of charging networks creates further opportunities for distribution transformer deployment. The growing manufacturing activities and industrial expansion continue to fuel the need for reliable power distribution systems, making Germany a crucial market for distribution transformer manufacturers.

Distribution Transformer Market in Russia

Russia's distribution transformer market is projected to experience remarkable growth, with an expected CAGR of approximately 17% from 2024 to 2029. The country's power sector transformation and modernization initiatives are driving this substantial growth. Russia's ambitious plans for electric vehicle production and infrastructure development, including the goal of having 1.5 million EVs on Russian roads by 2030, are creating significant opportunities for distribution transformer deployment. The country's focus on developing domestic manufacturing capabilities, particularly in the automotive sector, is expected to boost demand for industrial transformers. Despite global challenges, Russia continues to invest in grid infrastructure and power distribution networks to enhance reliability and efficiency. The country's vast geographical expanse necessitates robust power distribution systems, particularly in remote and developing regions. Furthermore, Russia's efforts to modernize its industrial infrastructure and expand its manufacturing capabilities are creating additional demand for utility transformers. The government's support for domestic production and technological advancement in the power sector is expected to sustain this growth momentum.

Distribution Transformer Market in United Kingdom

The United Kingdom's distribution transformer market is characterized by its strong focus on renewable energy integration and grid modernization initiatives. The country's commitment to achieving net-zero emissions by 2050 and completely decarbonizing the power sector by 2035 drives significant investments in power infrastructure. The UK's ambitious offshore wind energy targets, particularly the goal of achieving 50 GW of offshore wind installed capacity by 2030, necessitate substantial grid infrastructure development. The country's power infrastructure modernization efforts are supported by significant investments from both public and private sectors. The UK's industrial sector continues to drive demand through various applications, including manufacturing, chemicals, automotive, and aerospace industries. The growing adoption of electric vehicles and the corresponding expansion of charging infrastructure create additional demand for distribution transformers. Furthermore, the UK's focus on smart grid development and digital transformation in the power sector necessitates advanced distribution transformer solutions. The country's emphasis on energy efficiency and grid reliability continues to shape the market landscape.

Distribution Transformer Market in France

France's distribution transformer market is driven by its comprehensive energy transition strategy and ambitious renewable energy targets. The country's plan to reduce nuclear energy dependency and increase renewable energy sources creates significant opportunities for distribution transformer deployment. France's diverse industrial sector, encompassing manufacturing, chemicals, automotive, and aerospace industries, continues to drive demand for reliable power distribution solutions. The government's initiatives to promote innovation and competitiveness in the industrial sector, including labor market and tax reforms, contribute to market growth. The country's focus on expanding electric vehicle charging infrastructure and modernizing public transportation systems creates additional demand for distribution transformers. France's commitment to smart grid development and digital transformation in the power sector necessitates advanced distribution transformer solutions. The country's emphasis on energy efficiency and grid reliability, supported by various government initiatives and investments, continues to drive market development. Furthermore, France's strong focus on research and development in the power sector contributes to market innovation and growth.

Distribution Transformer Market in Other Countries

The distribution transformer market in other European countries, including Italy, Spain, Norway, Poland, Sweden, and Turkey, demonstrates diverse growth patterns influenced by their respective energy policies and industrial development strategies. These countries are actively investing in grid modernization and renewable energy integration, driving demand for distribution transformers. The varying industrial landscapes and urbanization rates across these nations create different market opportunities and challenges. Countries like Spain and Italy are particularly focused on solar and wind energy development, while Nordic countries emphasize hydroelectric power and grid interconnection. The growing emphasis on electric vehicle infrastructure and smart city development across these nations contributes to market growth. Additionally, the industrial automation and digitalization trends in these countries necessitate advanced power distribution solutions. The collective effort towards achieving European Union climate goals and energy efficiency targets shapes the market dynamics in these regions. Each country's unique approach to energy transition and grid modernization contributes to the overall European distribution transformer market landscape.

Get Analysis on Important Geographic Markets

Download PDF

Europe Distribution Transformer Industry Overview

Top Companies in Europe Distribution Transformer Market

The European distribution transformer market features prominent players like Siemens Energy, Hitachi Energy, General Electric, Schneider Electric, and Mitsubishi Electric Corporation leading the industry through continuous innovation and strategic initiatives. Companies are increasingly focusing on developing eco-friendly electrical transformers with biodegradable insulation materials and enhanced energy efficiency ratings to meet stringent environmental regulations. The market demonstrates a strong emphasis on digital transformation, with manufacturers incorporating smart monitoring capabilities and IoT integration in their product offerings. Strategic partnerships with utilities and industrial customers, combined with investments in manufacturing facilities across key European markets, highlight the industry's commitment to operational excellence. Companies are also expanding their service portfolios to include preventive maintenance, retrofitting solutions, and end-of-life management, creating comprehensive value propositions for customers.

Market Structure Shows Mixed Competition Dynamics

The European distribution transformer market exhibits a moderately fragmented competitive structure, characterized by the presence of both global conglomerates and specialized regional manufacturers. Global players leverage their extensive R&D capabilities, established brand reputation, and comprehensive product portfolios to maintain market positions, while regional specialists compete through customized solutions and local market expertise. The industry witnesses a balanced mix of multinational corporations with integrated operations and medium-sized companies focusing on specific market segments or geographical regions. Manufacturing capabilities, technical expertise, and after-sales support networks serve as key differentiators in the competitive landscape.

The market demonstrates active merger and acquisition activity, with larger companies acquiring specialized manufacturers to expand technological capabilities and regional presence. Strategic collaborations between manufacturers and technology providers are becoming increasingly common, particularly in developing smart transformer solutions and digital transformation initiatives. Companies are also forming partnerships with utilities and industrial customers to develop customized solutions and secure long-term supply agreements. The competitive dynamics are further influenced by the increasing focus on local manufacturing and supply chain optimization to ensure reliable product delivery and service support.

Innovation and Sustainability Drive Future Success

Success in the European distribution transformer market increasingly depends on companies' ability to align their offerings with the region's energy transition goals and digital transformation initiatives. Manufacturers must invest in developing energy-efficient products, incorporating renewable energy integration capabilities, and enhancing digital features to maintain competitive advantages. Building strong relationships with utilities and industrial customers through collaborative product development and comprehensive service offerings has become crucial for market success. Companies need to demonstrate expertise in specific applications, such as renewable energy integration and grid modernization, while maintaining cost competitiveness through operational efficiency.

Market participants must navigate evolving regulatory requirements, particularly regarding energy efficiency standards and environmental regulations, while maintaining product reliability and cost-effectiveness. New entrants can gain market share by focusing on innovative technologies, such as smart monitoring systems and eco-friendly materials, while established players need to continuously update their product portfolios and manufacturing processes. The ability to provide customized solutions for specific applications, combined with a strong local presence and after-sales support, will become increasingly important for market success. Companies must also develop strategies to address the growing demand for grid modernization and renewable energy integration while maintaining competitive pricing and reliable delivery capabilities.

Europe Distribution Transformer Market Leaders

-

Hitachi ABB Power Grids

-

Eaton Corporation PLC

-

Schneider Electric SE

-

General Electric Company

-

Siemens Energy AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Europe Distribution Transformer Market News

- April 2023: A consortium of Siemens Energy and Spain-based company Dragados Offshore agreed with German-Dutch transmission system operator Tennet to supply electric components for power transmission in three grid connections in the North Sea. The EUR 7 billion contract covers equipment like transformers, switchgear, and converter technologies they will manufacture at their European factories.

- March 2023: Ganz Transformers, the European technology provider for power grids, collaborated with Maschinenfabrik Reinhausen(MR) to manufacture digital transformers with the help of MR's ISM digital platform for intelligent solutions.

Europe Distribution Transformer Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Renewable Energy Generation

- 4.5.1.2 Rising Investments In EV Charging Infrastructure

- 4.5.2 Restraints

- 4.5.2.1 Rising Distributed Generation

- 4.6 Supply Chain Analysis

-

4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Type

- 5.1.1 Oil-filled

- 5.1.2 Dry Type

-

5.2 Capacity

- 5.2.1 Below 500 kVA

- 5.2.2 500 kVA - 2500 kVA

- 5.2.3 Above 2500 kVA

-

5.3 Phase

- 5.3.1 Single Phase

- 5.3.2 Three Phase

-

5.4 Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Rest of Europe

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Hitachi ABB Power Grids

- 6.3.2 Siemens Energy AG

- 6.3.3 Eaton Corporation PLC

- 6.3.4 Schneider Electric SE

- 6.3.5 General Electric Company

- 6.3.6 Westrafo SRL

- 6.3.7 Societa Elettromeccanica Arzignanese S.p.A

- 6.3.8 GBE S.p.A

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developing Greener Alternatives To SF6

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Europe Distribution Transformer Industry Segmentation

Distribution transformers are devices that step down the voltage at substations to deliver electricity to end customers. Distribution transformers provide the final voltage transformation in the electrical grid.

Europe's distribution transformer market is segmented by type, capacity, phase, and geography. By type, the market is segmented into oil-filled and dry types. By capacity, the market is segmented into below 500 kVA, 500 kVA - 2500 kVA, and above 2500 kVA. By phase, the market is segmented into single-phase and three-phase. The report also covers the market size and forecasts for the distribution transformer market across major countries in the region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Type | Oil-filled |

| Dry Type | |

| Capacity | Below 500 kVA |

| 500 kVA - 2500 kVA | |

| Above 2500 kVA | |

| Phase | Single Phase |

| Three Phase | |

| Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Europe Distribution Transformer Market Research FAQs

What is the current Europe Distribution Transformer Market size?

The Europe Distribution Transformer Market is projected to register a CAGR of 4.84% during the forecast period (2025-2030)

Who are the key players in Europe Distribution Transformer Market?

Hitachi ABB Power Grids, Eaton Corporation PLC, Schneider Electric SE, General Electric Company and Siemens Energy AG are the major companies operating in the Europe Distribution Transformer Market.

What years does this Europe Distribution Transformer Market cover?

The report covers the Europe Distribution Transformer Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Distribution Transformer Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Europe Distribution Transformer Market Research

Mordor Intelligence provides a comprehensive analysis of the distribution transformer industry. With decades of expertise in power transformer and electrical transformer research, our detailed report covers a wide range of technologies. These include pad mounted transformer and pole mounted transformer installations, as well as advanced cast resin transformer solutions. The analysis addresses both low voltage transformer and medium voltage transformer segments. It offers detailed insights into the power distribution equipment and electrical distribution equipment markets. Available as an easy-to-download report PDF, our research examines industrial transformer, utility transformer, and commercial transformer applications across Europe.

The report provides stakeholders with crucial insights into smart transformer technologies and grid transformer innovations, focusing on residential transformer deployment trends. Our analysis covers power distribution transformer systems and electric distribution transformer installations, offering comprehensive coverage of secondary transformer applications. The research delivers actionable intelligence for manufacturers, utilities, and investors, supporting strategic decision-making in the evolving European transformer sector. The report PDF download includes detailed technical specifications, regulatory analysis, and future market projections, ensuring stakeholders can effectively navigate this dynamic industry landscape.