Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 8.53 Billion |

| Market Size (2030) | USD 11.51 Billion |

| Growth Rate (2025 - 2030) | 6.18% CAGR |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Diabetes Care Devices Market Analysis by Mordor Intelligence

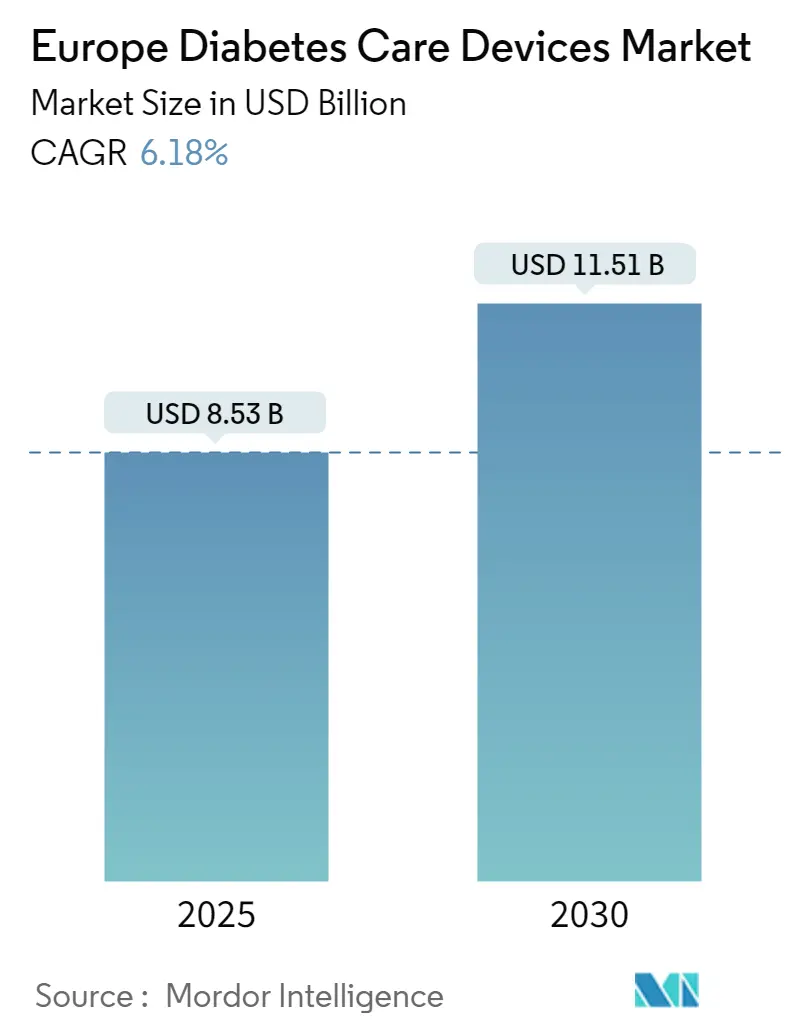

The Europe diabetes care devices market size is valued at USD 8.53 billion in 2025 and is forecast to reach USD 11.51 billion by 2030, advancing at a 6.18% CAGR. Strong demand for real-time glucose data, wider adoption of connected insulin delivery systems, and supportive reimbursement measures combine to sustain growth momentum. Expanded coverage for continuous glucose monitoring (CGM) across major European health systems is broadening the treated population, while hospital-at-home pilots are accelerating the shift from inpatient to remote diabetes management. Manufacturers are prioritizing all-in-one CGM sensors and patch pumps that minimize training time and improve adherence, and artificial-intelligence-driven dose-adjustment software is moving from pilot studies to routine practice. Competitive intensity is rising as incumbent leaders pursue scale-driven mergers and nimble entrants focus on non-invasive monitoring, creating a balanced landscape that rewards both manufacturing depth and innovation speed.

Key Report Takeaways

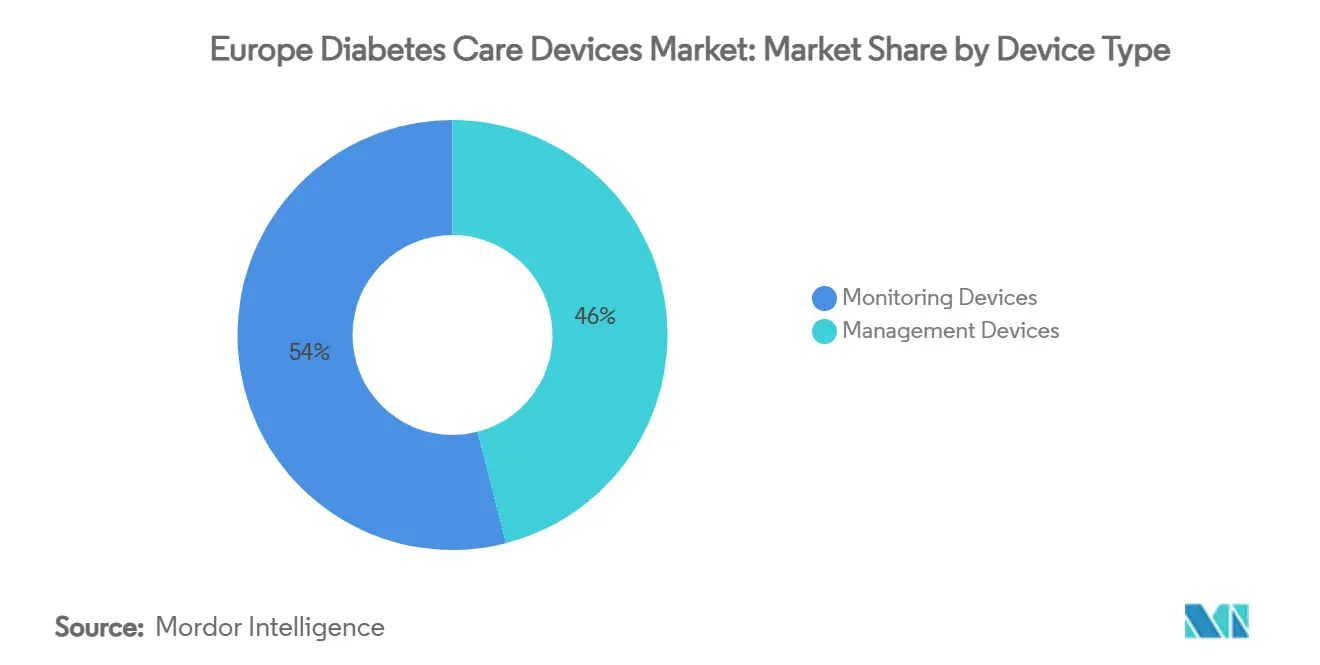

- By device type, monitoring devices led with 54.01% of Europe diabetes care devices market share in 2024, while management devices are projected to expand at a 7.07% CAGR through 2030.

- By patient type, the type-2 diabetes segment accounted for 81.35% of the Europe diabetes care devices market size in 2024 and is set to grow at 7.34% CAGR to 2030.

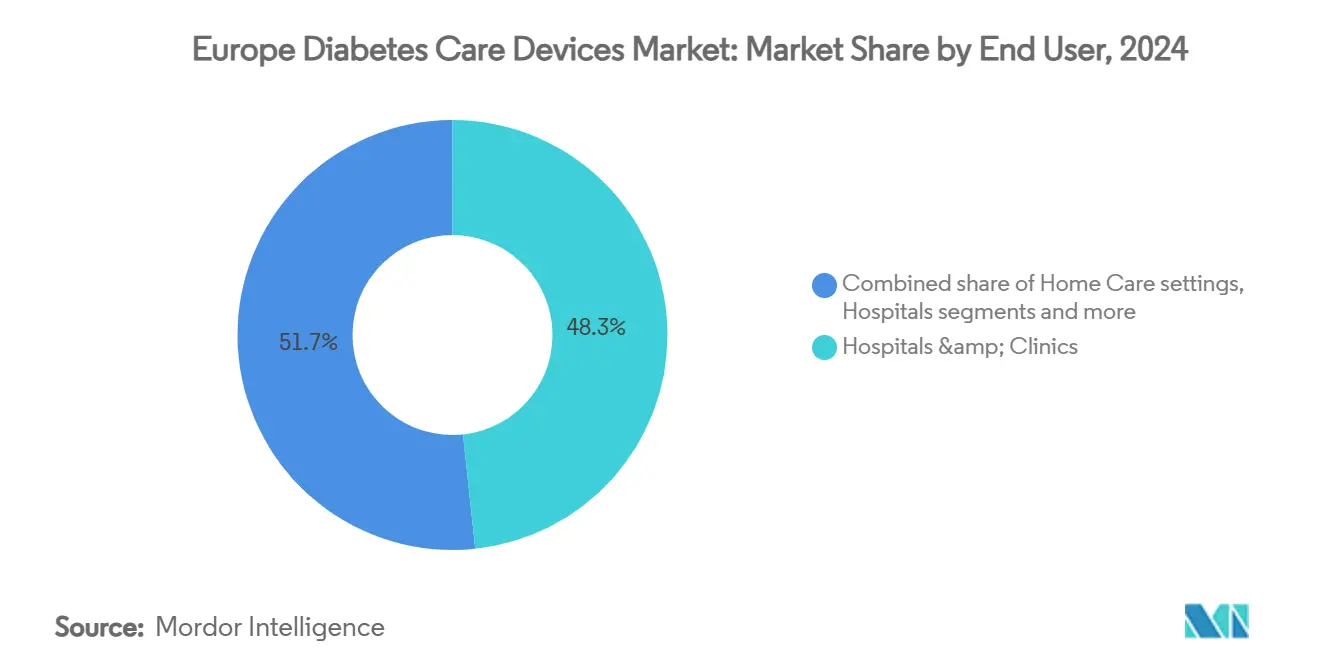

- By end-user, hospitals and clinics held 48.31% of Europe diabetes care devices market share in 2024; home-care settings represent the fastest trajectory at an 8.97% CAGR between 2025 and 2030.

- By distribution channel, retail pharmacies commanded 54% of the Europe diabetes care devices market size in 2024, whereas online pharmacies are forecast to register the quickest rise at an 8.34% CAGR during the same period.

Europe Diabetes Care Devices Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Reimbursement Reforms Boosting CGM Uptake in Germany & Nordics | +2.1% | Germany, Nordic countries | Medium term (2-4 years) |

| EU MDR Fast-Track for Class IIb "Smart Pens" Accelerating Product Launches | +1.2% | Europe | Short term (≤ 2 years) |

| Tender-Driven Consolidation of Test-Strip Pricing in Southern Europe | +0.8% | Spain, Italy, Portugal, Greece | Medium term (2-4 years) |

| Pediatric T1D Prevalence Surge in CEE Fueling Patch-Pump Demand | +0.7% | Central and Eastern Europe | Long term (≥ 4 years) |

| Hospital-at-Home Pilots in UK & France Driving Remote Monitoring Kits | +1.1% | United Kingdom, France | Medium term (2-4 years) |

| AI-based Decision Support Mandates in Spain Increasing Smart Pen Sales | +0.6% | Spain, with spillover to other EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Reimbursement Reforms Boosting CGM Uptake in Germany & Nordics

Statutory insurance in Germany broadened CGM coverage to all insulin-dependent patients at the start of 2024, instantly eliminating the primary cost barrier. Denmark, Sweden, and Norway mirrored the move, creating a unified northern cluster where reimbursement now favors sensor-based monitoring over test strips. The resulting surge in prescriptions is encouraging suppliers to localize sensor assembly to secure tender points and shorten lead times. Healthcare providers are revising clinical pathways so that CGM initiation happens within four weeks of insulin therapy commencement, tightening links between primary care and diabetology clinics. Manufacturers expect device utilization rates to climb steadily over the next three years as physician familiarity increases and patient self-management apps integrate national e-health records. Reimbursement certainty is therefore translating into higher volumes, more predictable revenue, and stronger negotiating power for compliant suppliers

EU MDR Fast-Track for Class IIb “Smart Pens” Accelerating Product Launches

The 2024 introduction of a twelve-to-fifteen-month fast-track review for connected insulin pens under the EU Medical Device Regulation slashed average time-to-market by roughly one-third. Leading developers rapidly submitted Bluetooth-enabled pens that capture dose data, flag omissions, and transmit information to physicians’ dashboards. Early approvals have prompted a queue of follow-on filings, signaling that the regulatory bottleneck is unlikely to return soon. Marketing teams are capitalizing on the compressed timeline by aligning European launches with global brand campaigns, thereby maximizing initial uptake. National formularies that previously hesitated to reimburse premium pens are reassessing cost–benefit models because real-world adherence gains are now easier to quantify. Collectively, these factors make Europe the launchpad for next-generation insulin-delivery hardware. .

Tender-Driven Consolidation of Test-Strip Pricing in Southern Europe

Public healthcare systems in Spain, Italy, Portugal, and Greece shifted to centralized tenders for blood-glucose test strips in 2024. Spain achieved a 35% price cut, and the other three markets applied comparable targets, forcing manufacturers to prioritize lean production and logistics savings over premium features. The lower unit cost has already driven a measurable uptick in test-strip consumption among patients who remain outside CGM eligibility. At the same time, the squeeze has triggered mergers between mid-tier strip suppliers seeking scale efficiencies. Over the next procurement cycle, price transparency is expected to narrow the gap between national and regional formularies, giving multi-country bidders a strategic edge in volume allocation. Southern Europe therefore represents both a margin challenge and a volume opportunity for the Europe diabetes care devices market .

Hospital-at-Home Pilots in the UK & France Driving Remote Monitoring Kits

The United Kingdom’s National Health Service expanded its “virtual ward” initiative to include insulin-treated diabetes in 2024, while France integrated diabetes monitoring within its “Hospitalisation à Domicile” network. Both programs package real-time CGM sensors, connected insulin pens, and teleconsultation portals into a turnkey kit delivered to patients within 48 hours of discharge. Early data show 25% fewer diabetes-related readmissions, underpinning further scale-up through 2026. Suppliers benefit from bulk-purchase agreements that guarantee minimum volumes and simplify post-market surveillance. As virtual ward templates migrate to additional EU members, remote monitoring is cementing itself as a core pillar of chronic-care policy, further enlarging the Europe diabetes care devices market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Divergent VAT Rates on Devices vs. Consumables Distorting SMBG Economics | -0.7% | European Union | Medium term (2-4 years) |

| Data-Residency Rules Limiting Cloud CGM Platforms in DACH Region | -0.9% | Germany, Austria, Switzerland | Medium term (2-4 years) |

| Fragmented HTA Processes Delaying Insulin Pump Funding in Italy & Spain | -0.5% | Italy, Spain | Short term (≤ 2 years) |

| Sensor Waste-Disposal Regulations Raising Cost of Ownership in Benelux | -0.3% | Belgium, Netherlands, Luxembourg | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Divergent VAT Rates on Devices vs. Consumables Distorting SMBG Economics

Reduced VAT on glucose meters but full VAT on test strips in several EU states inflates lifetime costs for self-monitoring of blood glucose. Patients may defer testing or stretch strip use, undermining glycemic control. Manufacturers are lobbying for harmonized medical-device VAT schemes, yet legislative progress remains slow. In the interim, low-priced strip bundles and subscription models aim to preserve testing frequency. Until tax parity is achieved, the economics of strip-based monitoring will limit growth potential for the segment inside the Europe diabetes care devices market[2]Source: European Commission, “Medical Device Regulation Fast-Track Guidance,” europa.eu.

Data-Residency Rules Limiting Cloud CGM Platforms in the DACH Region

Germany, Austria, and Switzerland require personal health data to remain on domestic servers. CGM suppliers have had to build country-specific hosting, adding 25-30% to operating costs and delaying advanced cloud features such as predictive analytics. Smaller vendors often defer or cancel launches, narrowing choice for clinicians and patients. Efforts to align European cloud standards are underway, but any relaxation is unlikely before 2027. The immediate effect is slower penetration of fully cloud-connected CGM in one of Europe’s most affluent diabetes markets .

Segment Analysis

By Device Type: Monitoring Dominates; Management Gains Pace

The monitoring segment captured 54.01% of the Europe diabetes care devices market in 2024, reflecting the primacy of accurate glucose data in day-to-day therapy. CGM systems now account for a majority of monitoring revenue because they deliver painless, continuous readings and integrate seamlessly with smartphones and hospital dashboards. CGM penetration accelerated once reimbursement expanded beyond type-1 to all insulin-treated patients. Suppliers are differentiating through sensor wear time, calibration-free operation, and direct-to-watch connectivity, signalling a gradual fade-out of fingerstick meters for regular measurement.

Management devices represent a smaller revenue pool but are forecast to progress at a 7.07% CAGR to 2030. Automated insulin delivery systems that combine CGM input with closed-loop algorithms epitomize this momentum. The result is a tighter convergence of traditionally separate hardware categories into unified ecosystems capable of autonomous glucose control. As algorithm accuracy improves, payers increasingly view advanced pump-sensor systems as an investment that offsets future complication costs. Consequently, management devices will narrow the gap with monitoring tools and may even surpass them in value toward the end of the decade, reshaping the competitive centre of gravity within the Europe diabetes care devices market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Patient Type: Type-2 Scale Drives Design Priorities

Type-2 diabetes patients accounted for 81.35% of the Europe diabetes care devices market size in 2024, underscoring a paradigm shift from type-1-centric engineering to broader metabolic-health use cases. Simplicity, discreet form factors, and low training overhead guide product roadmaps aimed at this cohort. Connected sensors that pair with diet-tracking apps appeal to type-2 users keen on lifestyle feedback rather than intensive insulin titration. As national guidelines now encourage CGM even for basal-insulin regimens, device makers are rolling out value-priced sensors that maintain core accuracy while omitting premium bells and whistles.

Type-1 diabetes retains outsized influence on breakthrough innovation. Hybrid closed-loop systems were perfected in the paediatric type-1 population before scaling to adult users and, more recently, to select type-2 subgroups[1]Source: NHS Fife, “Clinical Governance Committee Papers,” nhsfife.org . Meanwhile, gestational diabetes is beginning to attract tailored solutions that emphasise rapid onboarding and per-trimester subscription models. Collectively, patient-type diversification broadens the Europe diabetes care devices market and mitigates reliance on any single therapy pathway.

By End-User: Hospitals Anchor; Home-Care Accelerates

Hospitals and clinics held 48.31% of Europe diabetes care devices market share in 2024 thanks to their central role in diagnosis, device initiation, and intensive treatment. Multi-disciplinary diabetes centres inside hospital systems facilitate instant data transfer from bedside monitors to electronic health records, enabling closed-loop care pathways. Institutional procurement remains a stable volume channel for suppliers, particularly for in-patient CGM used during steroid therapy or post-operative glycaemic control.

Home-care settings, however, are poised for the fastest expansion at an 8.97% CAGR. Hospital-at-home programs, community nursing networks, and direct-to-patient sensor subscriptions are eroding historical barriers between inpatient and outpatient technology access. User-friendly insertion tools, integrated video tutorials, and automated re-ordering of consumables make self-management more feasible than ever. For payers, every avoided admission underlines the economic logic of home-centred device provision, further enlarging the Europe diabetes care devices market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Retail Dominance and Online Momentum

Retail pharmacies captured 54% of the Europe diabetes care devices market size in 2024, leveraging deep in-store advisory capabilities and established reimbursement workflows. Many leading chains now dedicate specialist staff to sensor placement and smart-pen training, moving beyond simple dispensing toward holistic disease-state services. Integration with pharmacy benefit platforms allows rapid eligibility checks and instant co-payment calculation at the counter, smoothing the patient journey.

Online pharmacies and direct-to-consumer e-commerce recorded an 8.34% CAGR and are on track to gain share as prescription-to-home workflows become commonplace. Remote consultation laws passed in several EU states during the pandemic remain in force, legitimising virtual prescribing. Suppliers, in turn, are tailoring packaging for courier networks, adding tamper-proof seals and interactive onboarding QR codes. As broadband access expands and digital literacy rises, online channels will convert convenience-driven trial orders into high-retention subscription plans, multiplying their contribution to the Europe diabetes care devices market.

Geography Analysis

Germany captured 25.54% Europe diabetes care devices market share in 2024, giving it the largest single-country stake in the Europe diabetes care devices market. The expansion of statutory health insurance to cover continuous glucose monitoring for all insulin-dependent patients removed previous therapy-type restrictions and created a surge in demand. Roughly 1.2 million Germans on insulin therapy now represent an immediate addressable base for connected pens and closed-loop systems. German centers that piloted automated insulin delivery reported measurable improvements in glycemic outcomes, further reinforcing physician advocacy for these devices. Nevertheless, strict data residency requirements in the DACH region are forcing manufacturers to fund localized cloud infrastructure, lifting operating costs by 25-30% and tempering near-term margin expansion.

France held 9.67% of the Europe diabetes care devices market size in 2024, benefiting from a centralized reimbursement model that quickly funnels innovative devices into the hospital-at-home channel. The “Hospitalisation à Domicile” program integrates continuous glucose monitoring and connected insulin delivery, creating alternative distribution pathways and driving consistent uptake across metropolitan areas. In the United Kingdom, the NHS virtual ward initiative now spans more than 50 trusts and places diabetes monitoring at the core of remote-care pilots, yet budget overruns such as the GBP 2.5 million annual overspend in NHS Fife illustrate funding pressure despite strong clinical results .

Southern Europe presents a contrasting picture: Spain is mandating AI-based decision support in public hospitals while tender-driven strip procurement has reduced testing costs by 35%, and Italy’s regulator AIFA still requires 18-24 months of post-market real-world evidence, slowing roll-outs. Central and Eastern European countries are grappling with annual pediatric Type 1 prevalence growth of 3-4%, prompting Poland, Czech Republic, and Hungary to prioritize patch pumps that fit smaller body sizes. Collectively, these divergent policy landscapes mean that while the Europe diabetes care devices market continues to grow, manufacturers must orchestrate highly localized market access strategies to capture incremental demand efficiently.

Competitive Landscape

The competitive structure is moderately concentrated: Abbott, Medtronic, Dexcom, Roche, and Novo Nordisk together hold roughly 65% of overall revenue. Abbott consistently reinvests double-digit percentages of device revenue into sensor R&D and reported more than 20% diabetes-care sales growth in 2024, driven by expanded Libre sensor reimbursement. Medtronic counters with single-platform simplicity, having unified pump, sensor, and app into an all-in-one ecosystem; CE-mark clearance for its disposable sensor in 2024 opened immediate market access in multiple EU states . Dexcom focuses on iterative sensor miniaturisation, backed by sustained R&D outlays disclosed in SEC filings, and maintains strong clinical-specialist engagement programs.

Strategic consolidation remains active. Novo Nordisk’s USD 11 billion purchase of fill-finish facilities in Belgium, Italy, and the United States secures supply resilience and underscores a long-term commitment to combination therapy solutions that pair devices with injectable insulin. Cardiovascular supply-chain giant Cardinal Health expanded its European diabetes footprint by acquiring an established sensor-distribution group, reflecting distributor appetite for margin-protective vertical integration. Meanwhile, start-ups rooted in university spin-outs target multi-month implantable sensors and photonic glucose spectroscopy. Though still in pre-regulatory stages, such entrants inject competitive tension by promising fewer consumables and lower lifetime cost.

Artificial intelligence is the new differentiator. Incumbent platforms now embed predictive alerts that model glucose 30–60 minutes ahead, aiming to reduce nocturnal hypoglycaemia and post-meal excursions. Partnerships between device firms and cloud-analytics providers accelerate algorithm updates, turning data ownership into a strategic resource. Vendors able to balance regulatory compliance with agile software iteration are staking claims to premium reimbursement tiers. Over time, AI-driven clinical decision support is likely to raise the performance bar for all participants, compelling late adopters either to license algorithms or cede share within the Europe diabetes care devices market.

Europe Diabetes Care Devices Industry Leaders

-

Roche Diabetes Care

-

Medtronic PLC

-

Novo Nordisk A/S

-

Dexcom Inc.

-

Abbott

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- Feburary 2025: Novo Nordisk acquired three fill-finish sites from Catalent for USD 11 billion to expand global diabetes-therapy manufacturing capacity

- June 2022: Cequr, the leader in wearable diabetes technology, released its newest and most innovative insulin delivery device, the Insulin Pen 2.0TM. The pen is small enough to be always worn on the user's body, and it also features a built-in blood glucose meter so that users can track their blood sugar throughout the day.

Europe Diabetes Care Devices Market Report Scope

Diabetes care devices are the hardware, equipment, and software used by diabetes patients to regulate blood glucose levels, prevent diabetes complications, lessen the burden of diabetes, and enhance the quality of life. The europe diabetes care devices market is segmented into monitoring devices, management devices and geography. The report offers the value (in usd) and volume (in units) for the above segments.

By Device Type

| Monitoring Devices | Self-Monitoring Blood Glucose | Glucometer Devices |

| Test Strips | ||

| Lancets | ||

| Continuous Glucose Monitoring | Sensors | |

| Durables | ||

| Management Devices | Insulin Pumps | Insulin Pump Device |

| Insulin Pump Reservoir | ||

| Infusion Set | ||

| Insulin Syringes | ||

| Insulin Pens | ||

| Jet Injectors | ||

By Patient Type

| Type-1 Diabetes |

| Type-2 Diabetes |

| Gestational & Others |

By End-user

| Hospitals & Clinics |

| Home-care Settings |

| Ambulatory Surgical Centres |

| Pharmacies & Retail Chains |

By Distribution Channel

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Direct-to-Consumer E-commerce |

By Country

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Rest of Europe |

| By Device Type | Monitoring Devices | Self-Monitoring Blood Glucose | Glucometer Devices |

| Test Strips | |||

| Lancets | |||

| Continuous Glucose Monitoring | Sensors | ||

| Durables | |||

| Management Devices | Insulin Pumps | Insulin Pump Device | |

| Insulin Pump Reservoir | |||

| Infusion Set | |||

| Insulin Syringes | |||

| Insulin Pens | |||

| Jet Injectors | |||

| By Patient Type | Type-1 Diabetes | ||

| Type-2 Diabetes | |||

| Gestational & Others | |||

| By End-user | Hospitals & Clinics | ||

| Home-care Settings | |||

| Ambulatory Surgical Centres | |||

| Pharmacies & Retail Chains | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Online Pharmacies | |||

| Direct-to-Consumer E-commerce | |||

| By Country | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Europe Diabetes Care Devices Market?

The Europe Diabetes Care Devices Market size is expected to reach USD 8.53 billion in 2025 and grow at a CAGR of 6.18% to reach USD 11.51 billion by 2030.

What is the current Europe Diabetes Care Devices Market size?

In 2025, the Europe Diabetes Care Devices Market size is expected to reach USD 8.53 billion.

Who are the key players in Europe Diabetes Care Devices Market?

Roche Diabetes Care, Medtronic PLC, Novo Nordisk A/S, Dexcom Inc. and Abbott are the major companies operating in the Europe Diabetes Care Devices Market.

What years does this Europe Diabetes Care Devices Market cover, and what was the market size in 2024?

In 2024, the Europe Diabetes Care Devices Market size was estimated at USD 8.00 billion. The report covers the Europe Diabetes Care Devices Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Diabetes Care Devices Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: