Market Size of Europe Data Center Construction Industry

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2023 |

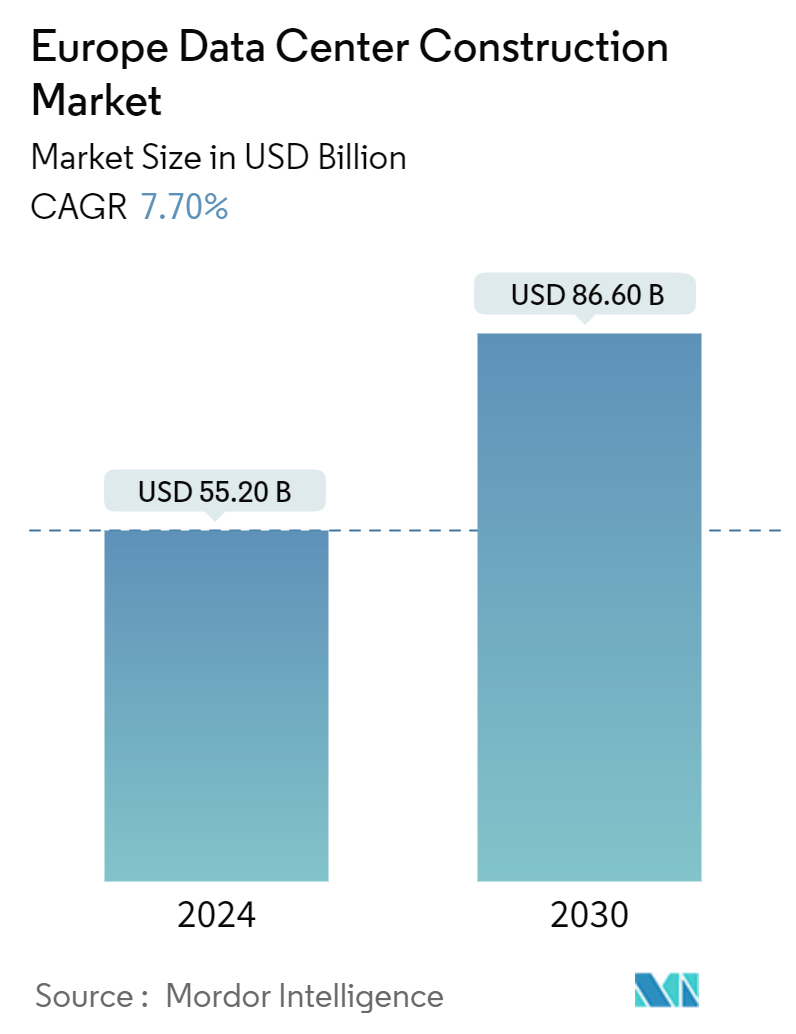

| Market Size (2024) | USD 55.20 Billion |

| Market Size (2030) | USD 86.60 Billion |

| CAGR (2024 - 2030) | 7.70 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Data Center Construction Market Analysis

The Europe Data Center Construction Market size is estimated at USD 55.20 billion in 2024, and is expected to reach USD 86.60 billion by 2030, growing at a CAGR of 7.70% during the forecast period (2024-2030).

The European data center construction market is projected to register a CAGR of 5.3% over the next five years. The market studied has been increasing, with new entrants and data centers being increasingly constructed in the region. The necessity for space and utilities has also expanded to unprecedented levels, with the expansion of businesses driving the need for more data centers in the region.

- Under Construction IT Load Capacity: The upcoming IT load capacity of the European data center construction market is expected to reach above 25,000 MW by 2030.

- Under Construction Raised Floor Space: Europe’s construction of raised floor areas is expected to exceed 80 million sq. ft. by 2030.

- Planned Racks: The region's total number of racks to be installed is expected to reach more than 4 million units by 2030. The United Kingdom is expected to house the maximum number of racks by 2030.

- Planned Submarine Cables: Many under-construction submarine cable projects are under process in Europe. For instance, in May 2024, the IOEMA Project introduced a groundbreaking 1,400 km repeatered submarine fiber optic initiative. This project signifies the first submarine fiber optic cable to land on Germany's North Sea shores in a quarter-century, thus marking a significant milestone. Spanning across the United Kingdom, the Netherlands, Germany, Denmark, and Norway, the IOEMA Project is set to revolutionize data connectivity in Northern Europe, offering enhanced capacity and redundancy.

- The FLAP-D (Frankfurt, London, Amsterdam, Paris, and Dublin) region has become significantly mature and faces limitations related to physical spaces and insufficient energy to power these data centers. Such issues have driven the colocation providers to find new feasible locations, including Oslo, Berlin, Zurich, Milan, Warsaw, and Madrid. These areas are considered potential hotspots for data center construction across the region.

Europe Data Center Construction Industry Segmentation

Data center construction combines physical processes used to construct a data center facility. It chains construction standards with data center operational environment requirements.

The European data center construction market is segmented by tier type (tier 1 and 2, tier 3, and tier 4), end user (banking, financial services and insurance, IT and telecommunications, government and defense, healthcare, and other end users), and geography (Germany, France, United Kingdom, Netherlands, Ireland, Switzerland, Denmark, Sweden, Italy, Russia, Belgium, Poland, Norway, Austria, Spain, and Rest of Europe). The market sizes and forecasts are provided in value (USD) for all the above segments.

| Market Segmentation - By Infrastructure | ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| General Construction |

| Market Segmentation - By Tier Type | |

| Tier 1 and 2 | |

| Tier 3 | |

| Tier 4 |

| Market Segmentation - By End User | |

| Banking, Financial Services, and Insurance | |

| IT and Telecommunications | |

| Government and Defense | |

| Healthcare | |

| Other End Users |

| Market Segmentation - By Geography | |

| Germany | |

| United Kingdom | |

| France | |

| Netherlands | |

| Irelands | |

| Switzerland | |

| Denmark | |

| Sweden | |

| Italy | |

| Poland | |

| Norway | |

| Austria | |

| Spain | |

| Rest of Europe |

Europe Data Center Construction Market Size Summary

The European Data Center Construction Market is experiencing significant growth, driven by the increasing demand for data centers due to the expansion of businesses and the digital economy. The market is characterized by a moderate level of fragmentation, with major players like AECOM, Arup, Caterpillar, SPIE UK, and Schneider Electric SE holding substantial market shares. The FLAP-D regions, including Frankfurt, London, Amsterdam, Paris, and Dublin, have reached maturity, prompting colocation providers to explore new locations such as Oslo, Berlin, Zurich, Milan, Warsaw, and Madrid. The development of smart cities, particularly in Germany, is further fueling the demand for data centers, as increased data consumption necessitates more IT infrastructure. The pandemic has also accelerated the need for data centers, as remote work and online activities surged, highlighting the importance of robust data storage and uptime.

The tier-3 segment dominates the market due to its high redundancy and reliability features, with the United Kingdom hosting the largest number of these facilities. The construction of tier-3 data centers is expected to grow, supported by the increasing adoption of edge and cloud connectivity. Despite challenges such as high land costs in London and power supply issues, the market continues to expand, with numerous projects underway across Europe. Notable developments include CyrusOne's acquisition of an office complex in Frankfurt and Green Mountain's joint venture with KMW to build a new data center campus. These initiatives, along with others, are set to enhance the market landscape, offering opportunities for vendors and contributing to the region's data center infrastructure growth.

Europe Data Center Construction Market Size - Table of Contents

-

1. MARKET SEGMENTATION

-

1.1 Market Segmentation - By Infrastructure

-

1.1.1 Market Segmentation - By Electrical Infrastructure

-

1.1.1.1 Power Distribution Solution

-

1.1.1.1.1 PDU - Basic and Smart - Metered and Switched Solutions

-

1.1.1.1.2 Transfer Switches

-

1.1.1.1.2.1 Static

-

1.1.1.1.2.2 Automatic (ATS)

-

-

1.1.1.1.3 Switchgear

-

1.1.1.1.3.1 Low Voltage

-

1.1.1.1.3.2 Medium Voltage

-

-

1.1.1.1.4 Power Panels and Components

-

1.1.1.1.5 Others

-

-

1.1.1.2 Power Back-up Solutions

-

1.1.1.2.1 UPS

-

1.1.1.2.2 Generators

-

-

1.1.1.3 Service - Design and Consulting, Integration, Support and Maintenance

-

-

1.1.2 Market Segmentation - By Mechanical Infrastructure

-

1.1.2.1 Cooling Systems

-

1.1.2.1.1 Immersion Cooling

-

1.1.2.1.2 Direct-to-Chip Cooling

-

1.1.2.1.3 Rear Door Heat Exchanger

-

1.1.2.1.4 In-row and In-rack Cooling

-

-

1.1.2.2 Racks

-

1.1.2.3 Other Mechanical Infrastructure

-

-

1.1.3 General Construction

-

-

1.2 Market Segmentation - By Tier Type

-

1.2.1 Tier 1 and 2

-

1.2.2 Tier 3

-

1.2.3 Tier 4

-

-

1.3 Market Segmentation - By End User

-

1.3.1 Banking, Financial Services, and Insurance

-

1.3.2 IT and Telecommunications

-

1.3.3 Government and Defense

-

1.3.4 Healthcare

-

1.3.5 Other End Users

-

-

1.4 Market Segmentation - By Geography

-

1.4.1 Germany

-

1.4.2 United Kingdom

-

1.4.3 France

-

1.4.4 Netherlands

-

1.4.5 Irelands

-

1.4.6 Switzerland

-

1.4.7 Denmark

-

1.4.8 Sweden

-

1.4.9 Italy

-

1.4.10 Poland

-

1.4.11 Norway

-

1.4.12 Austria

-

1.4.13 Spain

-

1.4.14 Rest of Europe

-

-

Europe Data Center Construction Market Size FAQs

How big is the Europe Data Center Construction Market?

The Europe Data Center Construction Market size is expected to reach USD 55.20 billion in 2024 and grow at a CAGR of 7.70% to reach USD 86.60 billion by 2030.

What is the current Europe Data Center Construction Market size?

In 2024, the Europe Data Center Construction Market size is expected to reach USD 55.20 billion.