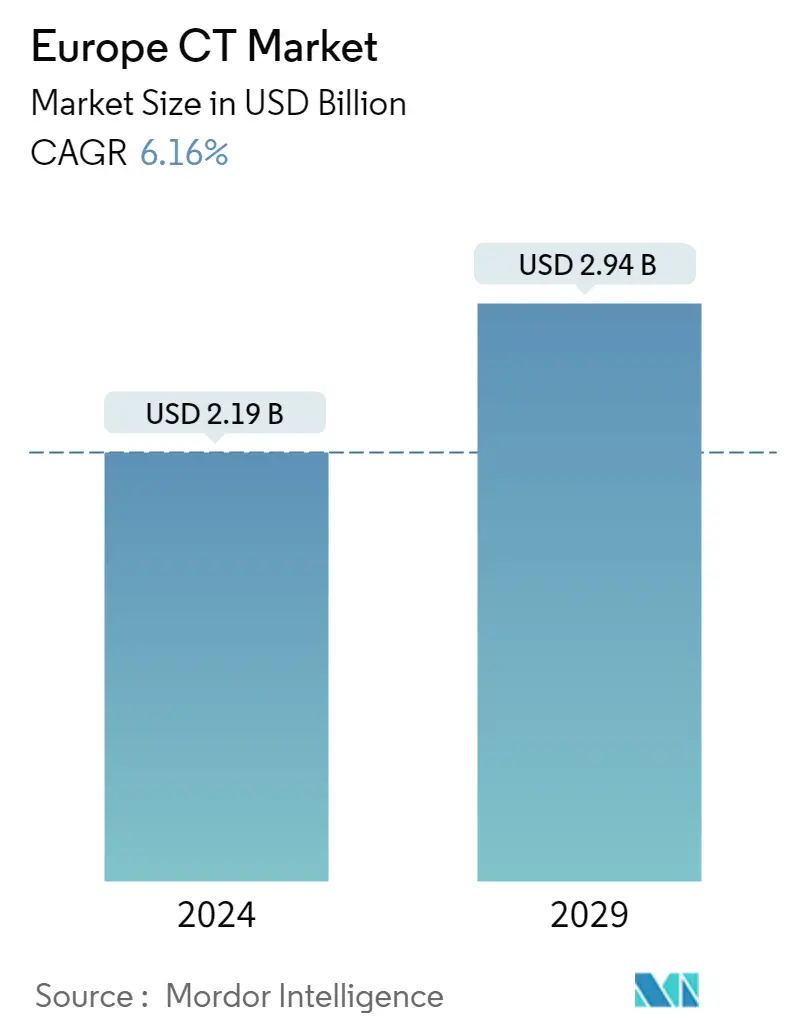

Europe CT Market Size

| Study Period | 2021 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Market Size (2024) | USD 2.19 Billion |

| Market Size (2029) | USD 2.94 Billion |

| CAGR (2024 - 2029) | 6.16 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe CT Market Analysis

The Europe CT Market size is estimated at USD 2.19 billion in 2024, and is expected to reach USD 2.94 billion by 2029, growing at a CAGR of 6.16% during the forecast period (2024-2029).

COVID-19 significantly impacted the growth of the market over the forecast period. As per an NCBI article published in June 2021, CT examination played an important auxiliary role in the diagnosis and subsequent management of COVID-19 patients in Europe. CT scans can reduce the chance of false-negative results in the RT-PCR assay. These findings led to increased demand for CT scans in Europe during COVID-19, thereby having a significant impact on the growth of the market. Furthermore, the demand for CT in Europe is expected to remain stable due to the increased emphasis on chronic disease diagnosis during the post-pandemic period, contributing to the market's growth over the forecast period.

The significant factors for the European computed tomography (CT) market include the rising geriatric population and increase in incidences of chronic diseases, an increase in the shift of medical care toward image-guided interventions, and technological advancements in the region. The burden of chronic diseases is on the rise across Europe, and medical imaging procedures play a crucial role in the accurate diagnosis of these diseases. Chronic diseases, such as heart disease, stroke, cancer, diabetes, obesity, and arthritis, are among the most common, expensive, and preventable of all health problems. As per the data provided in the British Heart Foundation report in August 2022, 6.4 million people are living with a heart or circulatory disease, and 12 infants are diagnosed with a heart defect. Moreover, according to the data published by the World Data Atlas, in 2021, the population aged 65 years and older was 23.6% in Italy, and this target population aged 65 years and older in Italy increased from 11.5 % in 1972 to 23.6 % in 2021, which is growing at an average annual rate of 1.47%. This increase in the aging population in the country is anticipated to suffer from chronic diseases requiring an increased rate of diagnosis, which is anticipated to drive the studied market growth over the forecast period.

Additionally, the rising product launches by various key market players are expected to contribute to the growth of the market. For instance, in November 2021, Siemens Healthcare launched a photon-counting CT scanner called Naeotom Alpha, and this system is cleared for clinical use in Europe.

However, expensive procedures and instruments and a stringent regulatory framework are expected to restrain the growth of the market.

Europe CT Market Trends

This section covers the major market trends shaping the Europe CT Market according to our research experts:

Oncology Segment is Expected to Hold the Largest Market Share in the European CT Market Over the Forecast Period

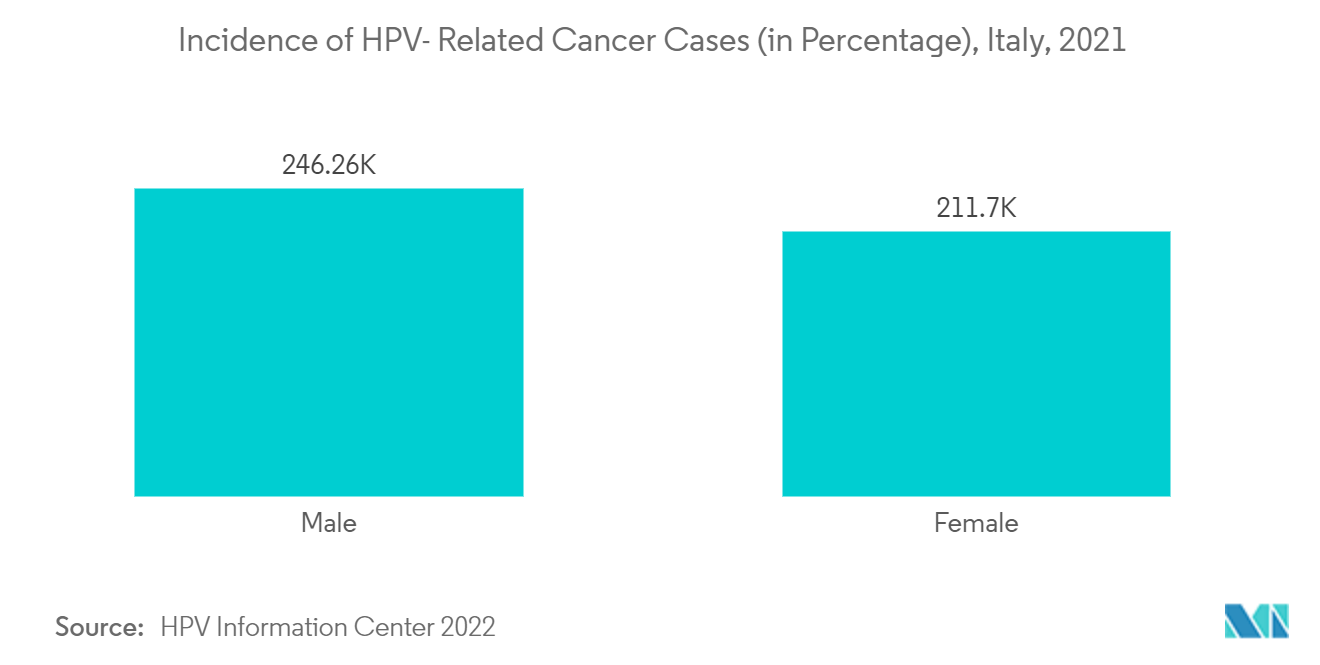

Oncology deals with the diagnosis and treatment of tumors and cancers, and cancer is one of the leading causes of morbidity and mortality. Among both sexes, cervical, anala, oral cavity lung, breast, and colorectal cancers are among the most common cancers. According to the HPV information center fact sheet published in 2022, the crude incidence rate of HPV-related cervical cancer among females was 8.23% in Spain in 2021 and the incidence of oral cavity cancer in males was 13.2% in 2021 in Spain. The cancer burden is increasing in the region, and thus, there is a rise in the usage of imaging modalities for the diagnosis of diseases.

Similarly, the data published by HPV information centers in 2022, mentioned that the incidence of HPV related oral cavity camcers among males was 8.04% in males and 5.38% in males. Additionally, the same source also mentioned that the annual incidence of cervical cancer in Italy was 3,152. Thus, the increasing prevalence of cancer in the European countries are expected to contribute to demand for CT owing to the early and effective diagnosis, thereby contributing to the growth of the studied segment.

Germany is Expected to Hold Significant Market Share in the Market Over the Forecast Period

Germany is expected to dominate the overall market during the forecast period. The market studied is growing in Germany due to the rising frequency of chronic conditions such as cardiovascular disease, the aging population, and favorable government initiatives. For instance, according to estimates from the Global Cancer Observatory updated in March 2021, around 628,519 new cancer cases were identified in Germany in 2021.

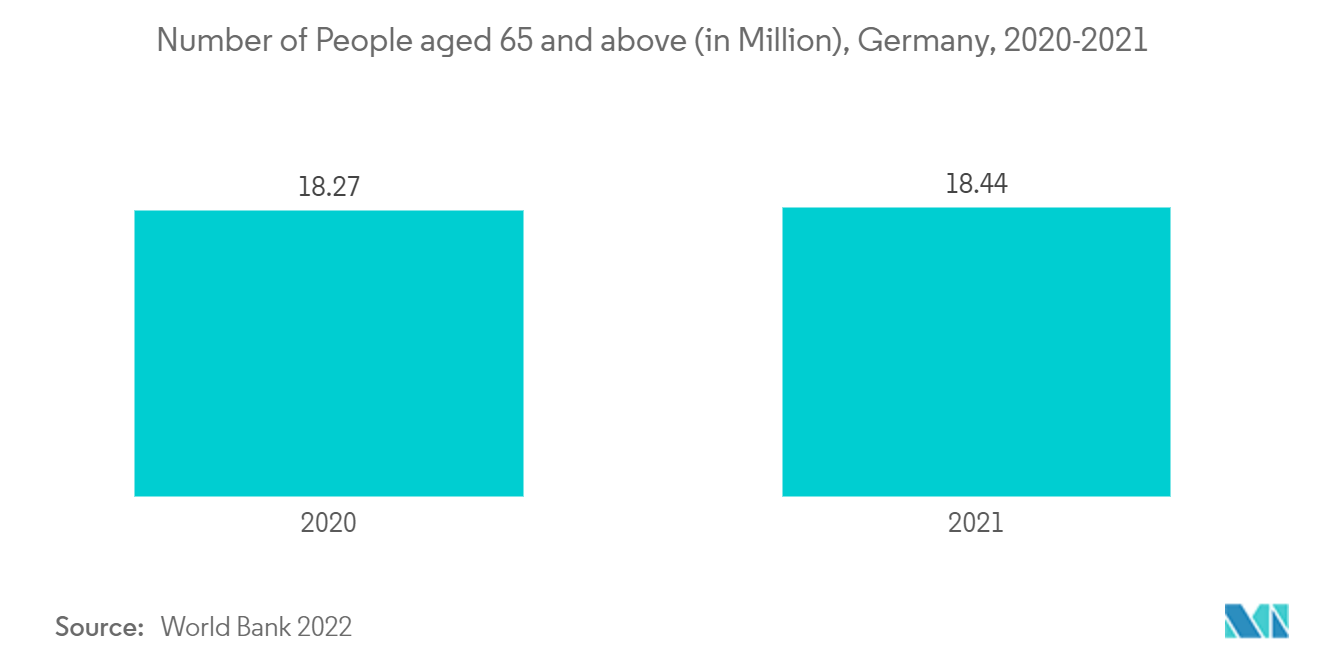

Furthermore, according to the article published by NCBI in August 2022, approximately 29,947 isolated coronary artery bypass grafting procedures, 36,714 isolated heart valve procedures, and 750 assist device implantations were registered in Germany in 2021. According to the same source, the number of solitary heart transplants in Germany has surged to 340 in 2021. In addition, according to the data published by the DSB in December 2022, the number of people aged 67 or older is expected to rise to 20 million by 2030, and the number of people aged 80 or older is expected to reach between 5.8 and 6.7 million by 2030. Chronic diseases such as orthopedic illnesses, heart diseases, and neurological disorders have a higher incidence in the older population and have a greater possibility of affecting the older population. Thus, due to the aforesaid factors, such as rising chronic diseases and increasing demand for effective diagnosis, the market is expected to witness significant growth over the forecast period.

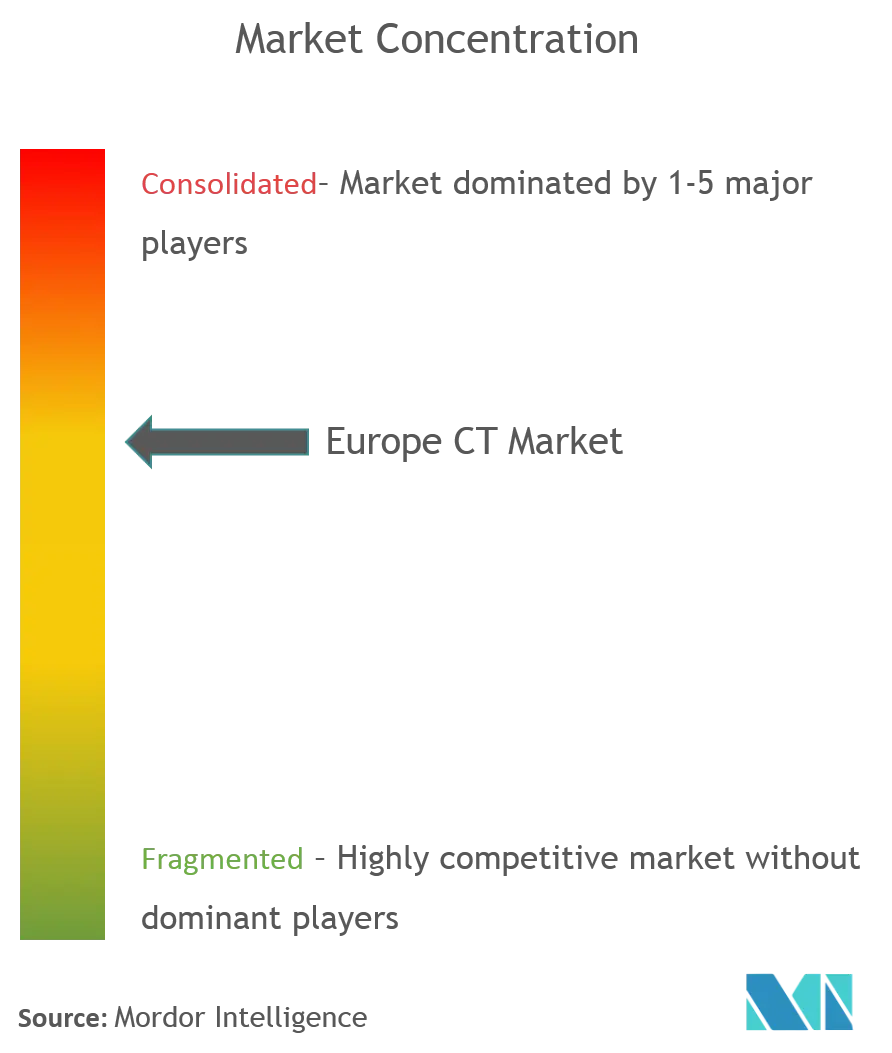

Europe CT Industry Overview

The European CT market is competitive and consists of several players. In terms of market share, a few of the major players are currently dominating the market. Some of the companies that are currently dominating the market are GE Healthcare, Koninklijke Philips NV, Siemens AG, Canon Medical Systems, and Fujifilm Holdings Corporation.

Europe CT Market Leaders

-

GE Healthcare

-

Koninklijke Philips NV

-

Siemens AG

-

Canon Medical Systems

-

Hitachi Medical Systems

*Disclaimer: Major Players sorted in no particular order

Europe CT Market News

- October 2022: GE Healthcare introduced Omni Legend positron emission tomography/ computed tomography platform at the 36th Annual congress of the European Association of Nuclear Medicine in Barcelona, Spain.

- June 2022: Siemens Healthineers launched innovations in SPECT/CT imaging at the European Congress of Radiology in Germany. The company demonstrated the Symbia Prospecta, SPECT/CT system with CE mark clearance that has advanced in imaging technologies.

Europe CT Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Increasing Incidence of Cancer & Chronic Diseases

4.2.2 Advancement in Technology

4.3 Market Restraints

4.3.1 Expensive Procedures and Instruments

4.3.2 Stringent Regulatory Framework

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Value - in USD Million)

5.1 By Type

5.1.1 Low Slice

5.1.2 Medium Slice

5.1.3 High Slice

5.2 By Application

5.2.1 Oncology

5.2.2 Neurology

5.2.3 Cardiovascular

5.2.4 Musculoskeletal

5.2.5 Other Applications

5.3 By End User

5.3.1 Hospitals

5.3.2 Diagnostic Centers

5.3.3 Other End-Users

5.4 Geography

5.4.1 United Kingdom

5.4.2 Germany

5.4.3 France

5.4.4 Spain

5.4.5 Italy

5.4.6 Rest of Europe

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 GE Healthcare

6.1.2 Koninklijke Philips NV

6.1.3 Siemens AG

6.1.4 Canon Medical Systems

6.1.5 Hitachi Medical Systems

6.1.6 Shimadzu Corporation

6.1.7 Samsung Medison

6.1.8 Trivitron Technologies

6.1.9 Fujifilm Holdings Corporation

6.1.10 Carestream Health

6.1.11 Planmeca Group (Planmed OY)

6.1.12 Koning Corporation

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Europe CT Industry Segmentation

As per the scope of the report, computed tomography (CT) is an imaging process that customizes special X-ray equipment to generate a sequence of exhaustive images, or scans, of areas inside the body. Also called computerized axial tomography (CAT) scanning, it is primarily used in cancer diagnosis. The Europe CT market is divided into four regions: Germany, the United Kingdom, France, Spain, Italy, and the rest of Europe. The report offers the value (in USD million) for the above segments.

| By Type | |

| Low Slice | |

| Medium Slice | |

| High Slice |

| By Application | |

| Oncology | |

| Neurology | |

| Cardiovascular | |

| Musculoskeletal | |

| Other Applications |

| By End User | |

| Hospitals | |

| Diagnostic Centers | |

| Other End-Users |

| Geography | |

| United Kingdom | |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe |

Europe CT Market Research FAQs

How big is the Europe CT Market?

The Europe CT Market size is expected to reach USD 2.19 billion in 2024 and grow at a CAGR of 6.16% to reach USD 2.94 billion by 2029.

What is the current Europe CT Market size?

In 2024, the Europe CT Market size is expected to reach USD 2.19 billion.

Who are the key players in Europe CT Market?

GE Healthcare, Koninklijke Philips NV, Siemens AG, Canon Medical Systems and Hitachi Medical Systems are the major companies operating in the Europe CT Market.

What years does this Europe CT Market cover, and what was the market size in 2023?

In 2023, the Europe CT Market size was estimated at USD 2.06 billion. The report covers the Europe CT Market historical market size for years: 2021, 2022 and 2023. The report also forecasts the Europe CT Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Europe CT Industry Report

Statistics for the 2024 Europe CT market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Europe CT analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.