Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

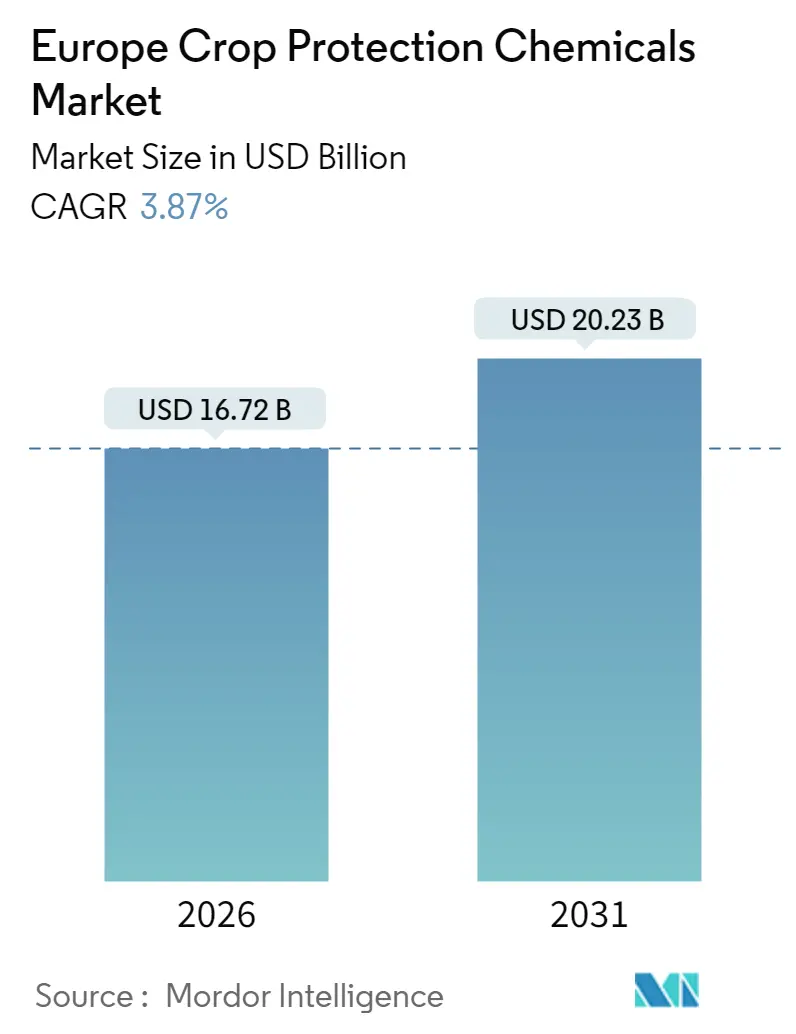

| Market Size (2026) | USD 16.72 Billion |

| Market Size (2031) | USD 20.23 Billion |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Crop Protection Chemicals Market Analysis by Mordor Intelligence

The Europe crop protection chemicals market was valued at USD 16.1 billion in 2025 and estimated to grow from USD 16.72 billion in 2026 to reach USD 20.23 billion by 2031, at a CAGR of 3.87% during the forecast period (2026-2031). Sustained regulatory pressure, climate-driven pest incidence, and the premiumization of low-risk formulations together underpin this steady expansion. Farmers across the region continue to invest in integrated pest management (IPM) tools, and digital advisory platforms that balance profitability with compliance. Large manufacturers are reshaping portfolios toward biostimulant–pesticide co-formulations, while distributors integrate artificial-intelligence (AI) decision support into service packages. At the same time, price-sensitive segments in Eastern Europe adopt cost-effective generics, anchoring a two-tiered demand structure within the Europe crop protection chemicals market. Competitive intensity remains high as rising Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) costs elevate scale advantages for the top players, yet novel entrants armed with RNA interference (RNAi) and microbial solutions introduce disruptive possibilities.

Key Report Takeaways

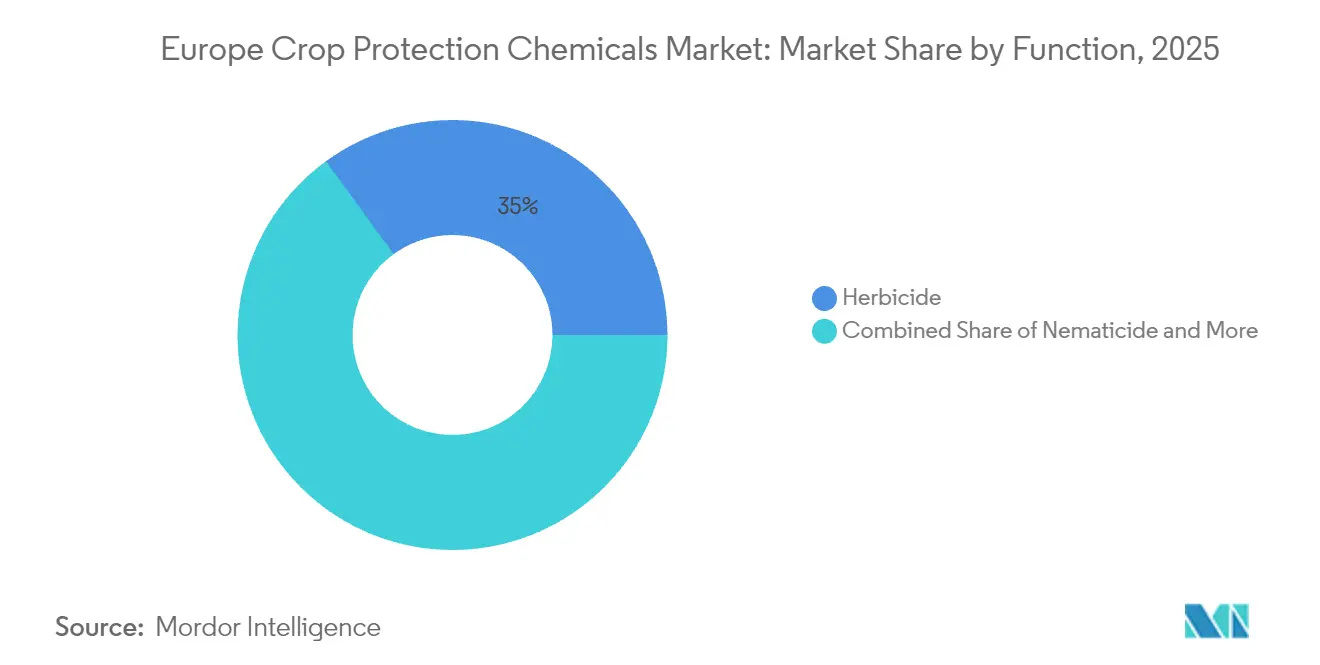

- By function, herbicides led with 35.01% of Europe crop protection chemicals market share in 2025, while insecticides posted the fastest 4.45% CAGR through 2031.

- By application mode, foliar treatments accounted for 47.12% of the Europe crop protection chemicals market size in 2025; seed treatment methods are poised to grow at 4.12% CAGR to 2031.

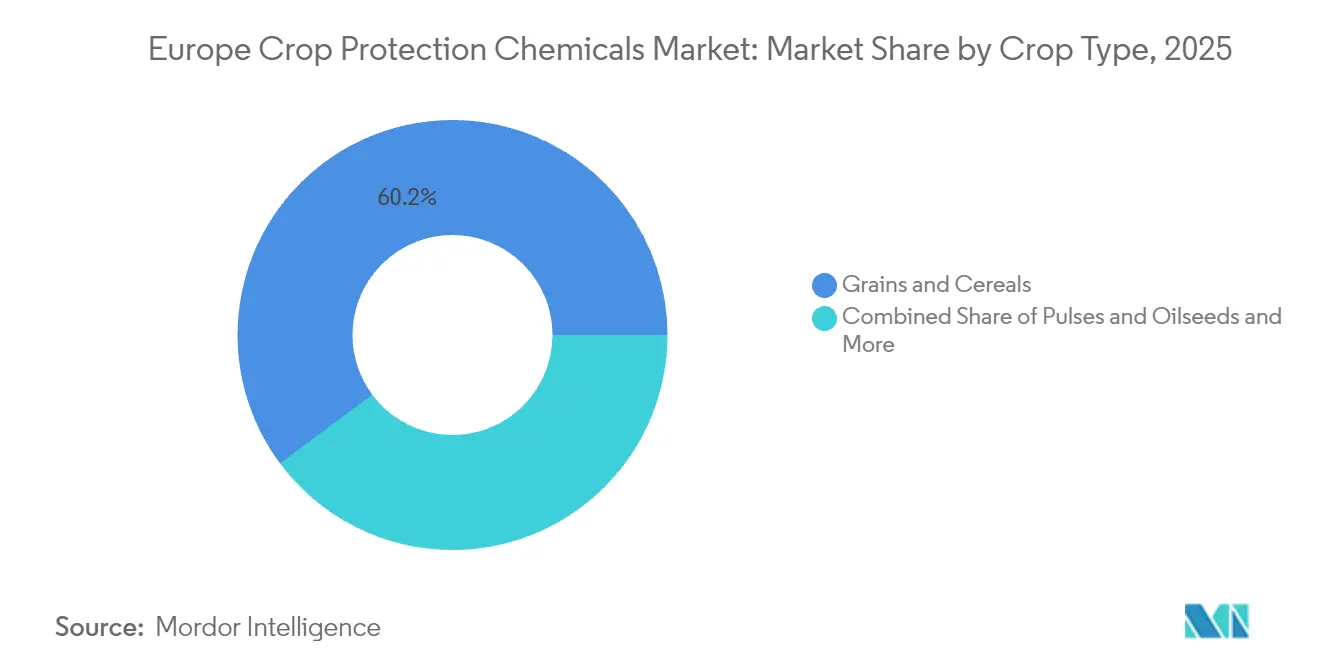

- By crop type, grains and cereals represented 60.18% of overall demand in 2025; turf and ornamental applications are expanding at a 4.25% CAGR through 2031.

- By country, Germany held a 21.12% revenue share in 2025; France is projected to register the highest 5.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Crop Protection Chemicals Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Integrated Pest Management adoption | +0.8% | EU-wide, strongest in Netherlands and Denmark | Medium term (2-4 years) |

| Surge in conservation-tillage practices | +0.7% | France, Germany, Spain, and Poland | Long term (≥ 4 years) |

| Climate-change-driven pest pressure | +0.6% | Southern Europe primary, spreading northward | Short term (≤ 2 years) |

| Rapid biostimulant-pesticide co-formulation launches | +0.5% | Germany, France, Italy leading adoption | Medium term (2-4 years) |

| AI-based prescription spraying platforms | +0.4% | Western Europe, pilot programs in Eastern Europe | Long term (≥ 4 years) |

| Rising cereal acreage in Eastern Europe | +0.3% | Poland, Romania, Ukraine (pre-conflict areas) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Integrated Pest Management Adoption

Integrated pest management adoption is rising, shifting farmer purchasing criteria from bulk volume toward targeted efficacy. The European Food Safety Authority (EFSA) recorded a 23% increase in IPM implementation during 2024, with Dutch commercial growers achieving 89% adoption.[1]Source: European Food Safety Authority, “Integrated Pest Management Adoption in Europe,” EFSA.EUROPA.EU This shift increases demand for monitoring devices, selective chemistries, and biological control agents that command 15–30% price premiums. Digital scouting and sensor networks reduce active ingredient use by up to 40%, allowing suppliers to transition from volume-driven to service-oriented revenue models within the Europe crop protection chemicals market.

Surge in Conservation-Tillage Practices

Conservation tillage, including no-till and strip-till, now covers 19% of the European Union’s arable land, up from 14% in 2023, according to the Joint Research Centre of the European Commission.[2]Source: European Commission Joint Research Centre, “Adoption of Conservation Tillage in the EU,” EUROPA.EU Farmers adopt these practices to reduce soil erosion, retain moisture, and lower diesel costs, though increased weed pressure boosts herbicide demand. Equipment upgrades like high-residue disc drills and herbicide-tolerant crops drive sales of selective chemistries and precision spraying services.

Climate-Change-Driven Pest Pressure

Warmer temperatures foster invasive pests such as the brown marmorated stink bug, now present in 15 European countries.[3]Source: European and Mediterranean Plant Protection Organization, “Invasive Alien Plants Database,” EPPO.INT Emergency authorizations for restricted actives during 2024 to combat fall armyworm in Spain and Portugal unlocked sales of USD 3.0 billion equivalent across the region. Suppliers with versatile portfolios and agile regulatory teams captured new demand pockets, offsetting volume declines from usage caps.

Rapid Biostimulant Pesticide Co-formulation Launches

Co-formulated products that merge plant nutrition with pest control comprised 40% of new European registrations in 2024. These hybrids meet dual agronomic goals, yield resilience and pest suppression, while easing regulatory hurdles under the European Union Fertilizing Products Regulation. Early movers realize scarcity pricing and brand loyalty advantages, reinforcing margin expansion in the Europe crop protection chemicals market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast-track bans on key actives (e.g., glyphosate) | -0.9% | EU-wide, varying implementation timelines | Short term (≤ 2 years) |

| Escalating registration costs under REACH | -0.6% | EU-27, affecting all market participants | Medium term (2-4 years) |

| Counterfeit pesticide penetration via gray imports | -0.4% | Eastern Europe and Southern borders | Short term (≤ 2 years) |

| Growing vegan/organic consumer lobby | -0.3% | Western Europe, urban centers primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fast-track Bans on Key Actives (e.g., Glyphosate)

Accelerated reviews of legacy molecules, exemplified by the 2024 glyphosate phase-out debate, inject investment uncertainty. Sudden neonicotinoid seed-treatment bans removed USD 1.3 billion in annual sales, forcing reformulation cycles and inventory write-downs. Diversified portfolios cushion impact yet smaller firms reliant on single actives face market exit in the Europe crop protection chemicals market. This regulatory volatility favors companies with diversified product portfolios but penalizes firms dependent on specific active ingredients, creating market share redistribution opportunities for agile competitors.

Escalating Registration Costs Under REACH

The European Chemicals Agency (ECHA) calculates that full dossiers now cost EUR 8–15 million (USD 8.6–16.1 million) per active ingredient. These outlays promote consolidation as only large multinationals sustain multi-product compliance pipelines. Product rationalization trims farmer choice and cements oligopolistic dynamics. These escalating costs force portfolio rationalization as companies discontinue marginally profitable products, reducing farmer choice while concentrating market power among players with sufficient scale to absorb regulatory expenses.

Segment Analysis

By Function: Weed Control Dominates a Diversifying Portfolio

Advanced weed resistance management drives herbicide innovation as traditional active ingredients face regulatory restrictions. Herbicides command 35.01% market share in 2025, yet insecticides demonstrate superior growth dynamics with 4.45% CAGR through 2031, reflecting climate-driven pest pressure and precision application adoption. The herbicide segment confronts dual pressures from glyphosate phase-out timelines and evolved weed resistance that renders established chemistries ineffective across 40% of European agricultural land. Fungicides maintain steady demand driven by climate-induced disease pressure, while molluscicides and nematicides serve specialized market niches with limited growth potential.

Regulatory compliance under the Sustainable Use Regulation creates opportunities for companies developing novel modes of action. The European Medicines Agency's expedited review process for low-risk substances provides competitive advantages for firms investing in RNA interference technologies and microbial-based solutions. Precision application technologies enable herbicide manufacturers to maintain market share despite volume restrictions by optimizing efficacy through targeted delivery systems that reduce environmental exposure while preserving weed control effectiveness.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application Mode: Foliar Dominance Meets Seed-Treatment Momentum

Foliar applications capture 47.12% market share in 2025, reflecting established farmer practices and equipment infrastructure, while seed treatment technologies accelerate at 4.12% CAGR through precision agriculture adoption. The dominance of foliar methods stems from versatility across crop types and growth stages, enabling farmers to respond reactively to pest pressure rather than implementing preventive strategies. Chemigation systems gain traction in water-scarce regions where irrigation infrastructure enables simultaneous nutrient and pesticide delivery, reducing labor costs and improving application uniformity.

Seed treatment innovations drive the fastest growth through systemic protection that reduces environmental exposure while providing season-long pest control. Fumigation applications remain concentrated in high-value crops and soil sterilization, while soil treatment methods face regulatory scrutiny due to groundwater contamination concerns. The European Food Safety Authority's 2024 guidance on application method risk assessment favors enclosed systems and precision delivery technologies that minimize off-target exposure.

By Crop Type: Broad-Acre Grains Anchor Demand, Specialty Crops Drive Value

Grains and cereals represent 60.18% of crop protection applications in 2025, driven by extensive cultivation across European agricultural landscapes and intensive production systems that require comprehensive pest management programs. Turf and ornamental segments demonstrate 4.25% CAGR growth through urbanization trends and climate-resilient landscaping demands that prioritize aesthetic standards over cost considerations. Commercial crops including sugar beet, rapeseed, and cotton face specific regulatory challenges as neonicotinoid restrictions eliminate established pest control strategies.

Fruits and vegetables command premium pricing due to cosmetic quality standards and intensive production systems, yet regulatory restrictions on residue levels create compliance challenges that favor integrated pest management approaches. The European Commission's 2024 Maximum Residue Limit revisions reduced allowable pesticide concentrations by an average of 30% across high-value crops, forcing growers toward precision application technologies. Pulses and oilseeds benefit from crop rotation incentives under the Common Agricultural Policy, creating demand for specialized herbicides that enable sustainable farming systems.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany maintains 21.12% market share in 2025 through intensive agricultural systems and advanced technology adoption, while France demonstrates 5.75% CAGR leadership driven by precision agriculture investments and sustainable farming transitions. Western Europe exhibits a mature profile characterized by premium positioning, stringent application protocols, and early adoption of AI agronomy tools. Germany’s high pesticide expenditure per hectare underpins stable revenues for suppliers that offer compliance documentation and stewardship training. French policy incentives coupled with farmer cooperatives fast-track precision machinery uptake, allowing manufacturers to bundle products with data services.

The Netherlands leverages controlled-environment agriculture to trial microbial and pheromone solutions before broader rollout. Southern Europe pairs Mediterranean climatic stress with specialty crop economics. Italian and Spanish growers demand fungicides tailored to high-sugar fruits, while value perceptions support bio-fungicide premiums. Water scarcity elevates the appeal of chemigation and drought-tolerant crop varieties, enlarging niche sub-markets. Portugal and Greece deploy European Union structural funds to modernize irrigation and digital infrastructure, opening fresh opportunities for variable-rate technology providers. Eastern Europe remains the volume frontier. Expanding cereal acreage in Poland, Romania, and Czech Republic anchors herbicide growth, though purchasing power favors off-patent formulations. Uptake of satellite-guided scouting accelerates as mobile connectivity improves. Ukraine’s partial crop recovery amid rebuilding efforts represents latent demand, subject to geopolitical stabilization. Across these geographies, distributors that tailor product and service mix to distinct regulatory, agronomic, and economic conditions strengthen competitive positioning within the Europe crop protection chemicals market.

Competitive Landscape

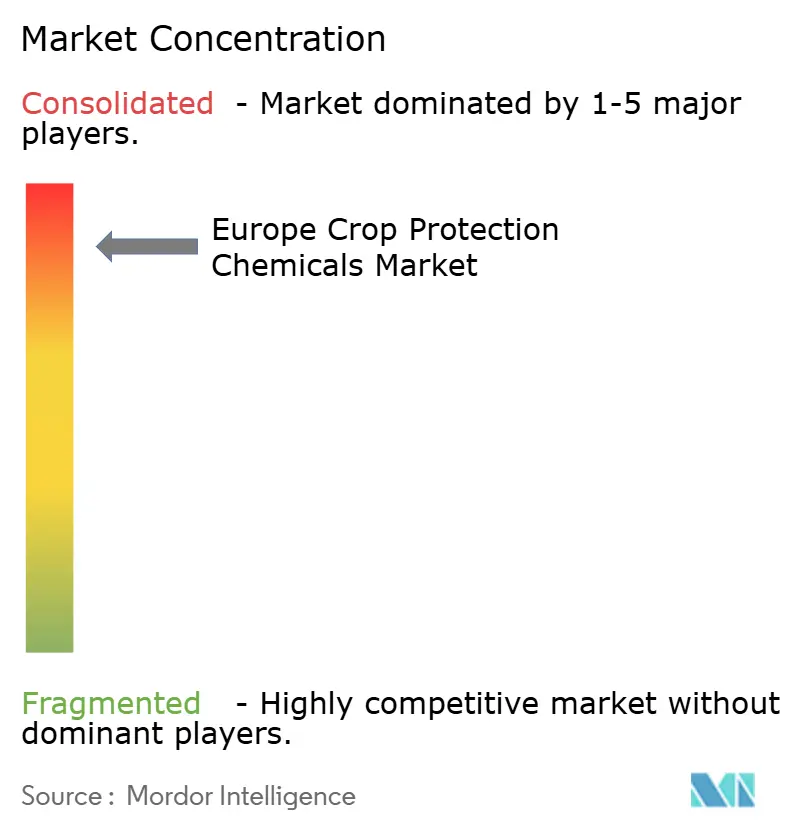

The top five companies, Bayer AG, Syngenta Group, BASF SE, Corteva Inc., and UPL Limited, controlled 74% of 2024 sales, reflecting significant concentration in the Europe crop protection chemicals market. Scale affords these leaders multinational regulatory teams, advanced discovery platforms, and life-cycle stewardship programs that smaller firms struggle to replicate. BASF’s 2024 clearance for RNAi insect control established a technological edge, and Corteva’s region-wide IPM platform launch illustrated a pivot to outcome-based services.

White-space entrants focus on RNA-based sprays, and AI decision-support ecosystems. Patent data from the European Patent Office show a 45% surge in protection filings during 2024. Startups leverage shorter approval cycles and farmer demand for residue-free produce. Nevertheless, REACH compliance capital requirements and tender-based distributor relationships remain formidable barriers.

Established players counter by forming licensing pacts or minority investments, ensuring access to disruptive pipelines while retaining distribution scale throughout the Europe crop protection chemicals market. Mergers and strategic alliances are anticipated to persist as regulation tightens and R&D costs escalate. Firms with balanced portfolios spanning chemistry and digital agronomy will likely secure share gains, whereas mono-line providers face progressive marginalization.

Europe Crop Protection Chemicals Industry Leaders

BASF SE

Bayer AG

Nufarm Ltd

Syngenta Group

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Bayer has applied for registration of its novel herbicide icafolin in the European Union, following submissions in Brazil, the U.S., and Canada. Icafolin offers a new mode of action for post-emergence weed control and supports regenerative agriculture practices

- March 2025: FMC Corporation and Bayer have partnered to introduce Isoflex active herbicide technology to European markets. This collaboration aims to offer farmers a new solution for controlling key grass and broadleaf weeds in cereal crops.

- August 2024: Adama announced the renewal of its fungicides Folpet and Capitan for continued use in Europe. These products had been widely used in cereal and grape farming to manage fungal diseases effectively. The renewal ensured regulatory compliance and reinforced Adama’s commitment to sustainable crop protection.

Europe Crop Protection Chemicals Market Report Scope

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type. France, Germany, Italy, Netherlands, Russia, Spain, Ukraine, United Kingdom are covered as segments by Country.Function

| Fungicide |

| Herbicide |

| Insecticide |

| Molluscicide |

| Nematicide |

Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

Country

| France |

| Germany |

| Italy |

| Netherlands |

| Russia |

| Spain |

| Ukraine |

| United Kingdom |

| Rest of Europe |

| Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental | |

| Country | France |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Ukraine | |

| United Kingdom | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF