| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 302.23 Billion |

| Market Size (2030) | USD 354.29 Billion |

| CAGR (2025 - 2030) | 3.23 % |

| Market Concentration | Low |

Major Players_-_Copy.webp "Europe Contract Logistics Market Major Players")

*Disclaimer: Major Players sorted in no particular order |

Europe Contract Logistics Market Analysis

The Europe Contract Logistics Market size is estimated at USD 302.23 billion in 2025, and is expected to reach USD 354.29 billion by 2030, at a CAGR of 3.23% during the forecast period (2025-2030).

The European contract logistics landscape is experiencing a gradual recovery amid evolving macroeconomic conditions. As prices stabilize and wages increase, European consumers are regaining purchasing power, which is expected to stimulate domestic demand across various sectors. The logistics services sector maintains its crucial position in the European economy, accounting for approximately 11-12% of the region's GDP. Advanced European economies are projected to see growth rates of 0.7% in the immediate term, with expectations of improvement through 2024 and 2025. The inflation trajectory shows signs of moderation, driven by declining energy prices and improving supply chain management conditions, with projections indicating an average of 5.8% in advanced European economies.

The industry is witnessing significant infrastructure developments and strategic expansions across key markets. Major logistics providers are strengthening their presence through substantial investments in modern facilities. For instance, in June 2023, GXO announced plans to expand its German operations with a new 587,000-square-foot warehouse in Dormagen, featuring cutting-edge warehousing solutions. This development represents a broader trend of logistics companies investing in advanced facilities to enhance their service capabilities and market presence. The focus on technological integration and automation in these new facilities reflects the industry's commitment to improving operational efficiency and service quality.

Cross-border collaboration and strategic partnerships are emerging as key trends shaping the market landscape. A notable example is the July 2023 strategic partnership between Geopost and JD Logistics, aimed at enhancing global logistics solutions capabilities by combining JDL's warehousing network with Geopost's delivery infrastructure. This collaboration exemplifies the industry's move toward creating seamless international express services, particularly strengthening logistics connections between China and Europe. Such partnerships are revolutionizing both C2C and B2C shipping solutions, introducing comprehensive end-to-end shipment tracking and enhanced customer support services.

The market is experiencing a significant shift toward sustainable and technologically advanced operations. Companies are increasingly investing in green logistics solutions and digital transformation initiatives to meet evolving customer expectations and regulatory requirements. The integration of advanced technologies such as automated mobile robots (AMRs) and sophisticated warehouse management systems is becoming more prevalent across European logistics operations. This technological evolution is particularly evident in major logistics hubs, where companies are implementing state-of-the-art digital tracking systems and automated solutions to optimize their operations and improve service delivery efficiency.

Europe Contract Logistics Market Trends

Growth in Manufacturing and Automotive Sector

The European manufacturing sector is showing strong signs of recovery in 2024, particularly evident in Germany's manufacturing sector, which demonstrated improvement with the HCOB final Purchasing Managers' Index (PMI) rising to 45.4 from April's 42.5. This positive momentum is further reinforced by the new orders index for German manufacturing, which rose by more than seven points in February 2024, signaling a potential turnaround in the sector. The automotive industry, a key manufacturing subsector, has shown remarkable resilience with a 7% growth in Europe in 2023, supported by easing supply chain disruptions and diminishing threats of energy rationing.

The sector's growth is being propelled by significant investments and technological advancements. The UK government's announcement of a GBP 4.5 billion (USD 5.72 billion) funding boost for eight key manufacturing sectors, including aerospace, automotive, and life sciences, demonstrates strong institutional support. According to MAKE UK, 71% of manufacturers invested or planned to invest in technology in 2023, with 59% expecting a positive impact on business performance. This technological transformation, particularly investments in automation, robotics, and AI, has helped improve productivity, efficiency, and reduce costs while minimizing environmental impact. In April 2024, Germany's automotive production reached 399,500 passenger cars, marking a substantial 26% year-over-year increase, while exports grew by 308,000 units, also representing a 26% rise.

Understand The Key Trends Shaping This Market

Download PDF

Growth in E-commerce Industry

The e-commerce sector continues to be a major catalyst for contract logistics growth, driven by evolving consumer expectations for faster and more reliable delivery services. In 2023, UK households are projected to spend approximately GBP 120 billion (USD 152.54 billion) on e-commerce, growing at an annual rate of 8.8%. This surge in online shopping has transformed the retail landscape, with e-commerce emerging as the UK's most popular retail channel over the past decade. The trend has created unprecedented demand for specialized warehousing services, particularly in order processing capabilities.

The industry's response to this growth is evident in recent strategic investments and technological adaptations. In November 2023, EV Cargo demonstrated this trend by investing in technology-driven supply chain services and building a distribution network with a world-leading control tower system. These investments are crucial as contract logistics providers help e-commerce companies reduce inventory, lower distribution costs, and facilitate new product launches. The sector's evolution is particularly beneficial for businesses of all sizes, offering advantages such as improved business manageability, advanced technology solutions, risk mitigation, and scalability. Contract logistics providers are increasingly focusing on specialized services for various sectors, including consumer electronics, telecommunications devices, and computer equipment, helping businesses optimize their logistics management and enhance their market presence.

Increasing Trend Towards Outsourcing

The European contract logistics market demonstrates significant growth potential, with current outsourcing penetration at approximately 20%, notably higher than the global average of 10-15%. This relatively low penetration rate, particularly in certain regions and industries, represents a substantial opportunity for expansion as businesses increasingly recognize the benefits of logistics outsourcing their operations. Transportation and storage services are experiencing particularly high outsourcing rates, driven by companies seeking to optimize their operations and focus on core business activities.

The trend towards outsourcing is particularly pronounced in the e-commerce sector, where companies are leveraging third-party logistics providers' expertise to manage complex supply chain operations. These providers offer crucial services such as customs handling, value-added tax (VAT) services, and flexible delivery options, enabling businesses to expand into new markets efficiently. The sophistication of modern contract logistics services extends beyond basic warehousing and transportation, encompassing advanced technology solutions, risk management, and scalable infrastructure that allows businesses to adapt quickly to market changes and consumer demands. This comprehensive service offering has become increasingly attractive to businesses looking to enhance their operational efficiency while maintaining competitive advantages in their respective markets.

Segment Analysis: By Type

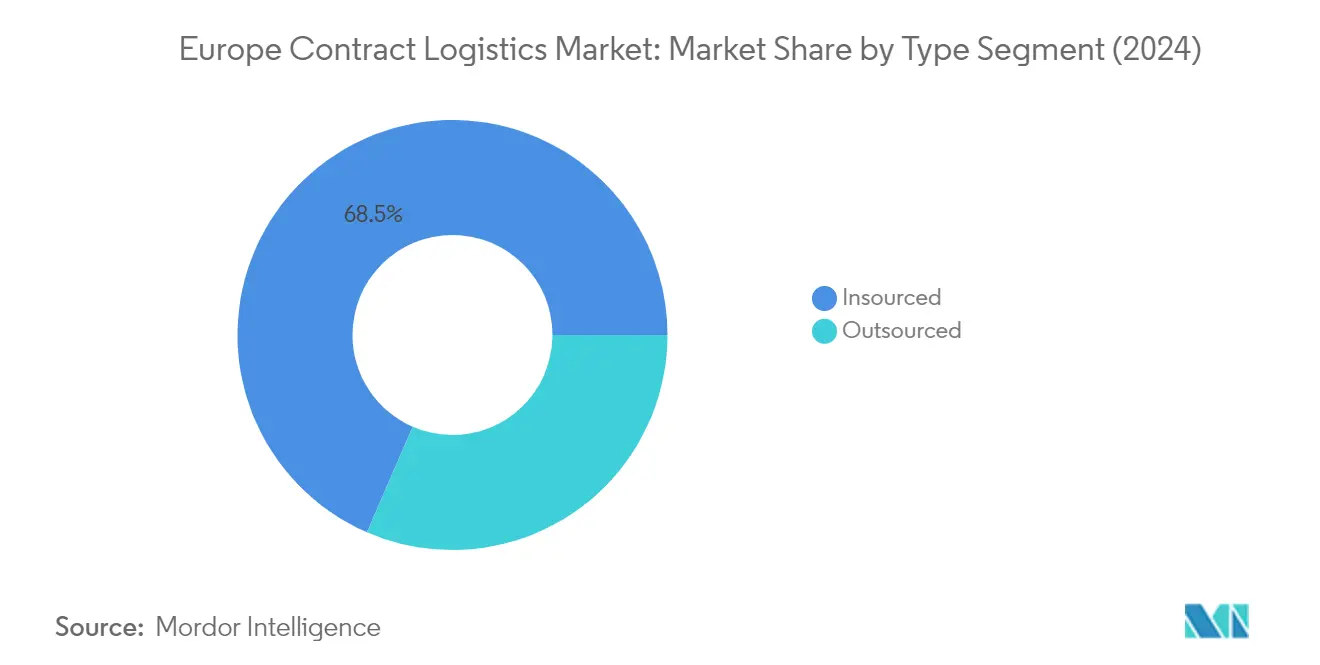

Insourced Segment in Europe Contract Logistics Market

The insourced segment dominates the European contract logistics market, commanding approximately 69% market share in 2024. This significant market position is driven by well-established European players in the automotive and manufacturing sectors who are increasingly integrating vertically and employing insourcing of contract logistics services to maximize profit and reduce business dependencies. For instance, in 2024, major automotive manufacturers are prioritizing insourcing and localizing as key strategies for maintaining flexibility and efficiency amidst growth. The segment's dominance is further strengthened by the increasing need for on-site logistics in major end-user industries like automotive and manufacturing, particularly for transporting spare parts, equipment, and finished goods within plants or factories. Despite the high capital investment, space requirements, and larger workforce needed for establishing an insourced contract logistics network, large enterprises continue to prefer this model for greater control over their supply chain operations.

Outsourced Segment in Europe Contract Logistics Market

The outsourced segment is projected to exhibit the fastest growth in the European contract logistics market from 2024 to 2029. This growth trajectory is supported by several key market developments, including GXO Logistics' strategic expansion in Germany with a new 387,000-square-foot warehouse in Dormagen, and Yusen Logistics' establishment of new contract logistics centers across Europe. The segment's accelerated growth is primarily driven by increasing supply chain complexity, rising demand for specialized logistics expertise, and the need for cost-effective solutions among small and medium enterprises. Companies are increasingly recognizing the benefits of outsourcing their logistics operations, including access to advanced technologies, specialized expertise, and flexible scaling options without significant capital investments. This trend is particularly evident in sectors like e-commerce, retail, and healthcare, where businesses are focusing on their core competencies while leveraging third-party logistics expertise for supply chain operations, including third-party logistics (3PL) and fulfillment services.

Segment Analysis: By End User

Consumer Goods & Retail Segment in Europe Contract Logistics Market

The consumer goods and retail segment has emerged as a dominant force in Europe's contract logistics market, commanding approximately 23% market share in 2024, with a value of USD 66.17 billion. This segment's leadership position is driven by the rapid evolution of e-commerce trends and increasing demands for faster delivery across Europe. The segment is also experiencing the highest growth trajectory, projected to expand at around 4% CAGR from 2024 to 2029, fueled by the rising adoption of omnichannel retailing strategies and sophisticated warehousing services. The growth is particularly evident in major European retail hubs such as Germany, the UK, and France, where retailers are increasingly outsourcing their logistics operations to optimize supply chain efficiency. The segment's robust performance is further supported by the integration of advanced technologies such as warehouse automation, robotics, and digital supply chain solutions, enabling more efficient inventory management and order fulfillment services processes.

Remaining Segments in Europe Contract Logistics Market

The European contract logistics market encompasses several other vital segments including food and beverage, industrial machinery and automotive, construction, and chemicals, each serving distinct industry needs. The food and beverage segment has shown significant strength, particularly in temperature-controlled logistics and specialized warehousing solutions. The industrial machinery and automotive segment continues to be crucial, especially in manufacturing-heavy regions like Germany and Eastern Europe, with increasing focus on just-in-time delivery systems. The construction segment's dynamics are closely tied to infrastructure development and urban expansion projects across Europe, while the chemicals segment maintains its importance through specialized handling requirements and safety protocols. Each of these segments contributes uniquely to the market's diversity, with varying requirements for storage, transportation, and value-added services, reflecting the complex nature of Europe's industrial and commercial landscape.

Europe Contract Logistics Market Geography Segment Analysis

Contract Logistics Market in Germany

Germany dominates the European contract logistics landscape, commanding approximately 24% of the market share in 2024. The country's central location in Europe, coupled with its highly skilled logistics services, provides ideal conditions for international shippers to succeed in European markets. Germany's strategic position offers easy access to the EU's 500 million consumers, making it an attractive hub for logistics operations. The country's robust infrastructure, including modern highways, advanced warehousing facilities, and efficient transportation networks, continues to attract major logistics providers. The automotive sector, a key driver of logistics demand, has shown resilience despite recent challenges, with production facilities maintaining steady operations. Major logistics companies are expanding their presence in the country, with several new warehouse developments and technological implementations enhancing operational capabilities. The integration of automation and digitalization in logistics operations has further strengthened Germany's position as a leading logistics hub, with companies investing in smart warehousing solutions and innovative delivery systems.

Contract Logistics Market in Sweden

Sweden's contract logistics market is experiencing remarkable growth, projected to expand at approximately 5% annually from 2024 to 2029. As the largest logistics market in Scandinavia, Sweden continues to attract significant investments from multinational corporations and logistics providers. The country's strategic position as a gateway to Northern Europe has made it a preferred location for centralized distribution services serving the Nordic region. Sweden's robust infrastructure, including major cargo airports such as Stockholm Arlanda and Gothenburg Landvetter, facilitates efficient logistics operations. The presence of global brands like H&M, Ikea, and Ericsson has created a sophisticated logistics ecosystem that demands high-quality logistics services. The country's commitment to sustainability has driven innovation in green logistics solutions, with companies implementing eco-friendly practices in their operations. Advanced technology adoption, including automation and digitalization, has enhanced operational efficiency across the logistics value chain. The market's growth is further supported by Sweden's stable economic environment and strong focus on research and development in logistics technologies.

Contract Logistics Market in United Kingdom

The United Kingdom maintains its position as a crucial hub for contract logistics operations in Europe, driven by its sophisticated infrastructure and innovative logistics solutions. The country's logistics sector has demonstrated remarkable resilience, adapting to post-Brexit challenges through enhanced technological integration and operational efficiency. Major logistics providers are investing in new facilities, particularly in key locations such as the Midlands and Greater London, where occupancy rates exceed 90%. The rise of e-commerce has catalyzed significant changes in the UK's logistics landscape, with companies implementing advanced warehouse automation and robotics solutions. The market has seen substantial investments in sustainable logistics practices, with providers increasingly adopting electric vehicles and eco-friendly warehouse operations. The UK's strong focus on last-mile delivery solutions and urban logistics has led to the development of innovative distribution models. The integration of artificial intelligence and machine learning in logistics operations has enhanced predictive capabilities and operational efficiency, positioning the UK at the forefront of logistics innovation.

Contract Logistics Market in France

France's contract logistics sector continues to evolve, characterized by significant technological advancement and strategic infrastructure development. The country's position as a key gateway between Northern and Southern Europe makes it an essential logistics hub. Major logistics clusters around Paris and Lyon serve as crucial nodes in the European supply chain management network. The market has witnessed substantial investments in automation and robotics, particularly in warehouse operations, enhancing operational efficiency and service quality. French logistics providers have been at the forefront of implementing sustainable practices, with a strong focus on reducing carbon emissions and promoting green logistics solutions. The country's robust transportation infrastructure, including an extensive network of highways and railways, facilitates efficient logistics operations. Innovation in urban logistics solutions has become a key focus area, with providers developing specialized solutions for city-center deliveries. The market's growth is further supported by France's strong manufacturing base and diverse industrial sectors, creating consistent demand for sophisticated logistics services.

Contract Logistics Market in Other Countries

The contract logistics landscape across other European countries presents a diverse and dynamic market environment. Countries like Italy, Spain, Poland, and Belgium each contribute uniquely to the European logistics ecosystem, leveraging their geographical advantages and specialized capabilities. The Netherlands, with its strategic location and world-class port infrastructure, serves as a crucial gateway for European logistics operations. Eastern European countries, particularly Poland and the Czech Republic, have emerged as important logistics hubs, offering cost-effective solutions and modern infrastructure. The Benelux region continues to play a vital role in European distribution networks, while Nordic countries demonstrate strong potential in sustainable logistics solutions. Southern European nations like Spain and Italy leverage their strategic Mediterranean positions to facilitate trade flows. These markets are characterized by increasing adoption of advanced technologies, growing e-commerce capabilities, and enhanced focus on sustainable logistics solutions, collectively contributing to the robust European logistics network.

Get Analysis on Important Geographic Markets

Download PDF

Europe Contract Logistics Industry Overview

Top Companies in Europe Contract Logistics Market

The European contract logistics landscape is characterized by major players like DHL, Kuehne + Nagel, GXO Logistics, CEVA Logistics, DSV, and DB Schenker leading significant market transformations. These companies are heavily investing in digital transformation initiatives, incorporating artificial intelligence, IoT, and blockchain technologies to enhance operational efficiency and visibility in logistics management. The industry is witnessing a strong push toward sustainable logistics practices, with companies adopting electric vehicles and eco-friendly warehouse solutions. Strategic partnerships and collaborations, particularly in technology integration and cross-border operations, have become increasingly common. Companies are expanding their value-added services beyond traditional logistics, offering comprehensive supply chain services including inventory management, order fulfillment, and reverse logistics capabilities.

Consolidated Market with Strong Global Players

The European contract logistics market exhibits a consolidated structure dominated by large global logistics conglomerates with extensive networks and comprehensive service portfolios. These major players leverage their scale and resources to maintain competitive advantages through advanced technology implementations and extensive geographic coverage. The market has witnessed significant merger and acquisition activities, with larger companies acquiring specialized regional players to enhance their service offerings and expand their market presence. Companies like GXO Logistics and XPO have been particularly active in strategic acquisitions to strengthen their positions in key European markets.

The competitive dynamics are further shaped by the presence of strong regional specialists who maintain significant market share in specific geographic areas or industry verticals. These regional players often compete effectively by offering specialized services and maintaining strong local customer relationships. The market has seen increased collaboration between global and local players, creating strategic alliances to combine international reach with local expertise. This trend has led to a complex competitive landscape where success depends on balancing scale advantages with specialized service capabilities.

Innovation and Sustainability Drive Future Success

Success in the European contract logistics market increasingly depends on companies' ability to innovate while maintaining operational efficiency and sustainability. Market leaders are focusing on developing integrated digital platforms that provide end-to-end supply chain visibility and real-time analytics capabilities. The adoption of automation and robotics in warehousing operations has become a critical differentiator, with companies investing heavily in these technologies to improve efficiency and reduce operational costs. Customer-centric innovation, particularly in last-mile delivery solutions and value-added services, has emerged as a key factor in maintaining competitive advantage.

For new entrants and smaller players, success lies in identifying and serving niche markets or specialized industry sectors where they can build expertise and strong customer relationships. The increasing focus on sustainability presents opportunities for companies to differentiate themselves through green logistics solutions and environmental certifications. Regulatory changes, particularly regarding environmental standards and cross-border operations, are reshaping competitive dynamics and creating new opportunities for specialized service providers. The ability to adapt to changing customer needs while maintaining cost efficiency and service quality will remain crucial for both established players and new entrants in the market. The role of third-party logistics and 4PL providers is becoming increasingly significant as companies seek to optimize their logistics management strategies.

Europe Contract Logistics Market Leaders

-

Deutsche Post DHL Group

-

Kuehne + Nagel International AG

-

DB Schenker

-

CEVA Logistics

-

SNCF Logistics/Geodis

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Europe Contract Logistics Market News

- May 2024: Omoda and Jaecoo UK, brands under China's Chery Automobile Co., have inked a multi-year warehousing deal with DHL Supply Chain, marking their foray into the UK market. Under this agreement, DHL will manage aftermarket services for both brands, housing spare parts, accessories, and notably, batteries for their electric and hybrid vehicle lines.

- September 2023: JLR and DHL, in a continuation of their 15-year partnership, have inked a three-year transport contract extension. The highlight of this renewal is DHL's bold commitment to transition its entire UK core fleet, operating within JLR, to alternative fuels by April 2024. Not to be outdone, JLR is also making the shift to alternative fuels in its UK fleet. These combined efforts are projected to slash carbon emissions by an impressive 84%, equating to a yearly reduction of over 8,000 tonnes of CO2e. This joint move towards alternative fuels underscores the shared environmental aspirations of both entities. Aligned with its Reimagine strategy, JLR is targeting a 46% reduction in CO2e emissions across its SBTi scope 1 and 2, and an even more ambitious 54% reduction in its SBTi scope 3 emissions by 2030. These milestones pave the way for JLR's ultimate goal: achieving carbon neutrality by 2039.

Europe Contract Logistics Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2. RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

-

4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increased Outsourcing of Services

- 4.2.1.2 Increasing Demand For Contract Logistics In Italy, France, And Poland

- 4.2.2 Restraints

- 4.2.2.1 Increasing Competition In The European Contract Logistics Market

- 4.2.2.2 Regulatory Compliance

- 4.2.3 Opportunities

- 4.2.3.1 Pooled Warehousing

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Government Regulations and Initiatives

- 4.6 Technological Trends

- 4.7 Insights into the E-commerce Industry in the Region (Domestic and Cross-border)

- 4.8 Insights into Contract Logistics in the Context of After-sales/Reverse Logistics

- 4.9 Brief on Different Services Provided by Contract Logistics Players (Integrated Warehousing and Transportation, Supply Chain Services, and Other Value-added Services)

- 4.10 Spotlight on Freight Transportation Costs/Freight Rates

- 4.11 Insights into Effects of Brexit on the European Logistics Industry

- 4.12 Impact of COVID-19 on the Market

5. MARKET SEGMENTATION

-

5.1 By End User

- 5.1.1 Industrial Machinery and Automotive

- 5.1.2 Food and Beverage

- 5.1.3 Construction

- 5.1.4 Chemicals

- 5.1.5 Other Consumer Goods

- 5.1.6 Other End Users

-

5.2 By Country

- 5.2.1 Germany

- 5.2.2 United Kingdom

- 5.2.3 Netherlands

- 5.2.4 France

- 5.2.5 Italy

- 5.2.6 Spain

- 5.2.7 Poland

- 5.2.8 Belgium

- 5.2.9 Sweden

- 5.2.10 Rest of the Europe

6. COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

-

6.2 Company Profiles (including Merger and Acquisition, Joint Ventures, Collaborations, and Agreements)

- 6.2.1 Deutsche Post DHL Group

- 6.2.2 XPO Logistics

- 6.2.3 Schenker AG (DB Schenker)

- 6.2.4 CEVA Logistics

- 6.2.5 SNCF Logistics/Geodis

- 6.2.6 DSV AS

- 6.2.7 Neovia Logistics Services

- 6.2.8 GEFCO SA

- 6.2.9 United Parcel Service Inc. (UPS Supply Chain Solutions)

- 6.2.10 Rhenus SE & Co. KG

- 6.2.11 Bertelsmann SE & Co. KGaA (Arvato)

- 6.2.12 FIEGE Logistik Stiftung & Co. KG*

-

6.3 Other Companies (Key Information/Overview)

- 6.3.1 Expeditors International, United Parcel Service Inc., Bollore Logistics, Hellmann Worldwide Logistics GmbH & Co. KG, Agility Logistics Pvt. Ltd, H. Essers NV, Wincanton PLC*

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

8. APPENDIX

- 8.1 GDP Distribution by Activity for Key Countries

- 8.2 Insights into Capital Flows

- 8.3 External Trade Statistics - Export and Import by Product

- 8.4 Insights into Key Export Destinations of Europe

- 8.5 Insights into Key Import Origins of Europe

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Europe Contract Logistics Industry Segmentation

Contract logistics refers to a long-term partnership that includes a variety of services, from the transportation of goods or replacement parts to the delivery of goods to the ultimate customer.

The report provides a complete background analysis of the European contract logistics market, including an assessment of the economy, a market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles are covered in the report. The report also covers the impact of COVID-19 on the market.

The report covers the European Logistic Companies, and it is segmented by End User (Industrial Machinery and Automotive, Food and Beverage, Construction, Chemicals, Other Consumer Goods, and Other End Users), and Country (Germany, the United Kingdom, the Netherlands, France, Italy, Spain, Poland, Belgium, Sweden, and Rest of Europe). The report offers the market size in value terms in USD for all the abovementioned segments.

| By End User | Industrial Machinery and Automotive |

| Food and Beverage | |

| Construction | |

| Chemicals | |

| Other Consumer Goods | |

| Other End Users | |

| By Country | Germany |

| United Kingdom | |

| Netherlands | |

| France | |

| Italy | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of the Europe |

Need A Different Region or Segment?

Customize Now

Europe Contract Logistics Market Research FAQs

How big is the Europe Contract Logistics Market?

The Europe Contract Logistics Market size is expected to reach USD 302.23 billion in 2025 and grow at a CAGR of 3.23% to reach USD 354.29 billion by 2030.

What is the current Europe Contract Logistics Market size?

In 2025, the Europe Contract Logistics Market size is expected to reach USD 302.23 billion.

Who are the key players in Europe Contract Logistics Market?

Deutsche Post DHL Group, Kuehne + Nagel International AG, DB Schenker, CEVA Logistics and SNCF Logistics/Geodis are the major companies operating in the Europe Contract Logistics Market.

What years does this Europe Contract Logistics Market cover, and what was the market size in 2024?

In 2024, the Europe Contract Logistics Market size was estimated at USD 292.47 billion. The report covers the Europe Contract Logistics Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Contract Logistics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Europe Contract Logistics Market Research

Mordor Intelligence provides a comprehensive analysis of the contract logistics industry. We leverage extensive expertise in supply chain management and logistics services. Our research covers the full range of 3PL (Third-Party Logistics) and 4PL (Fourth-Party Logistics) services. This includes freight forwarding, warehousing services, and integrated logistics solutions. The report, available as a PDF download, offers detailed insights into logistics management practices and transportation management systems across Europe.

Stakeholders gain from our thorough analysis of inventory management trends, distribution services, and logistics solutions. The report explores key aspects of logistics outsourcing, contract warehousing, and fulfillment services. It also covers dedicated contract carriage operations. Our research aids decision-makers in understanding supply chain services dynamics. This enables them to optimize their contract distribution strategies and enhance operational efficiency through improved third party logistics implementation.