Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

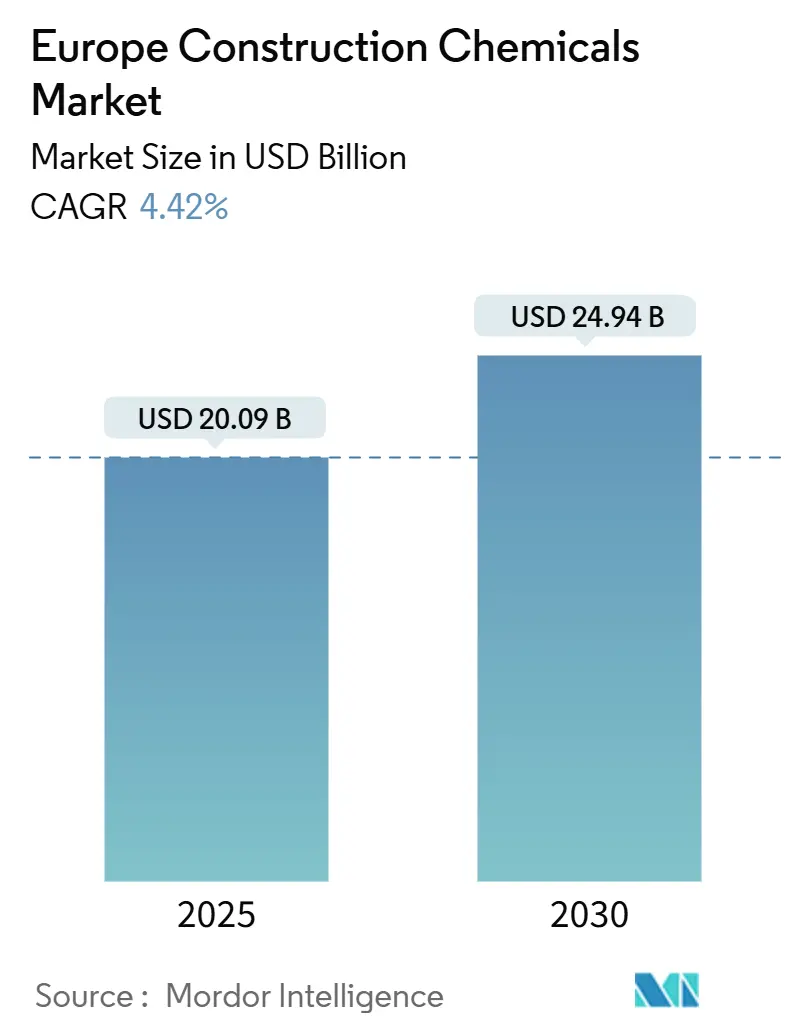

| Market Size (2025) | USD 20.09 Billion |

| Market Size (2030) | USD 24.94 Billion |

| Growth Rate (2025 - 2030) | 4.42% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Construction Chemicals Market Analysis by Mordor Intelligence

The Europe Construction Chemicals Market size is estimated at USD 20.09 billion in 2025, and is expected to reach USD 24.94 billion by 2030, at a CAGR of 4.42% during the forecast period (2025-2030). Expansion continues despite cyclical construction slowdowns because public-sector stimulus under the EU Green Deal, the Energy Performance of Buildings Directive (EPBD), and the Connecting Europe Facility steers spending toward low-carbon materials and infrastructure upgrades. Suppliers that combine specialty formulations with verifiable environmental credentials are more likely to win specifications as project owners adopt mandatory Environmental Product Declarations (EPDs). Consolidation accelerates, illustrated by Saint-Gobain’s USD 1.025 billion acquisition of FOSROC, while leaders such as Sika leverage geographic diversification and specialty product portfolios to protect margins. Raw-material cost volatility, chiefly in epoxy and polyurethane feedstocks, pressures profitability, yet innovation in bio-based, Per- and Polyfluoroalkyl Substances (PFAS)-free, and carbon-negative chemistries creates new revenue streams and improves regulatory resilience across the Europe Construction Chemicals market.

Key Report Takeaways

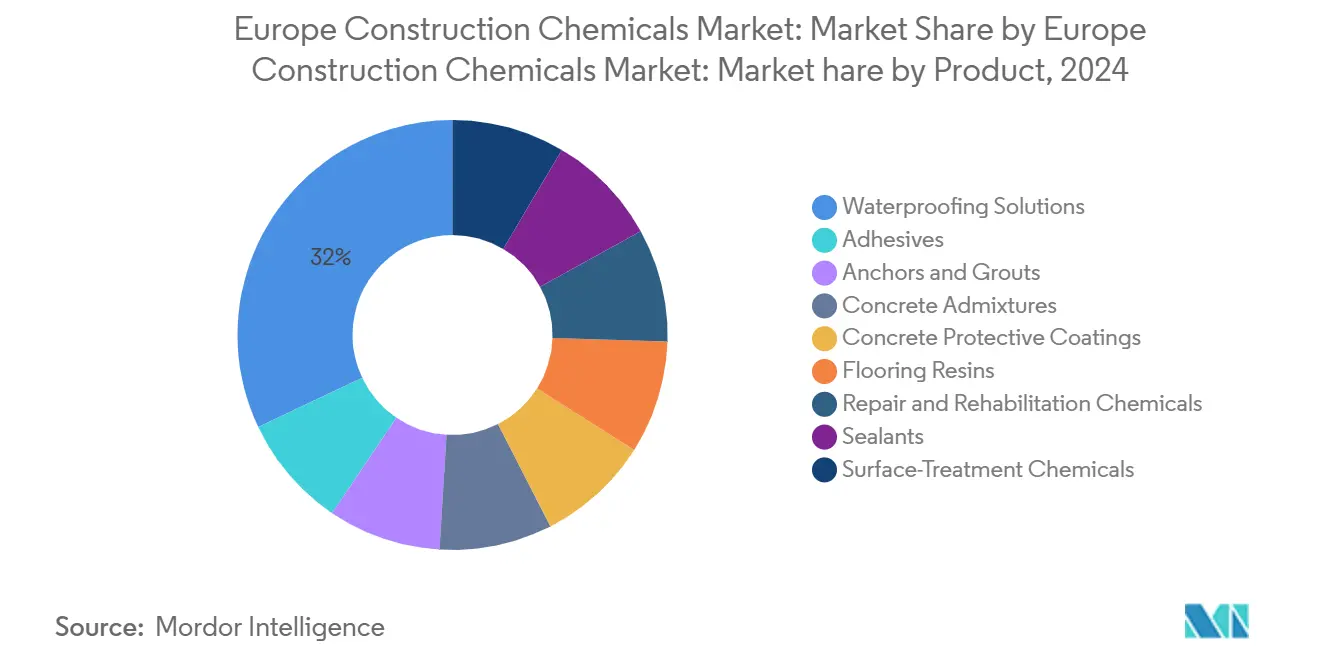

- By product category, waterproofing solutions held 32.07% of the Europe Construction Chemicals market share in 2024. However, the market share of concrete admixtures is expected to increase with the fastest CAGR of 5.24% through 2030.

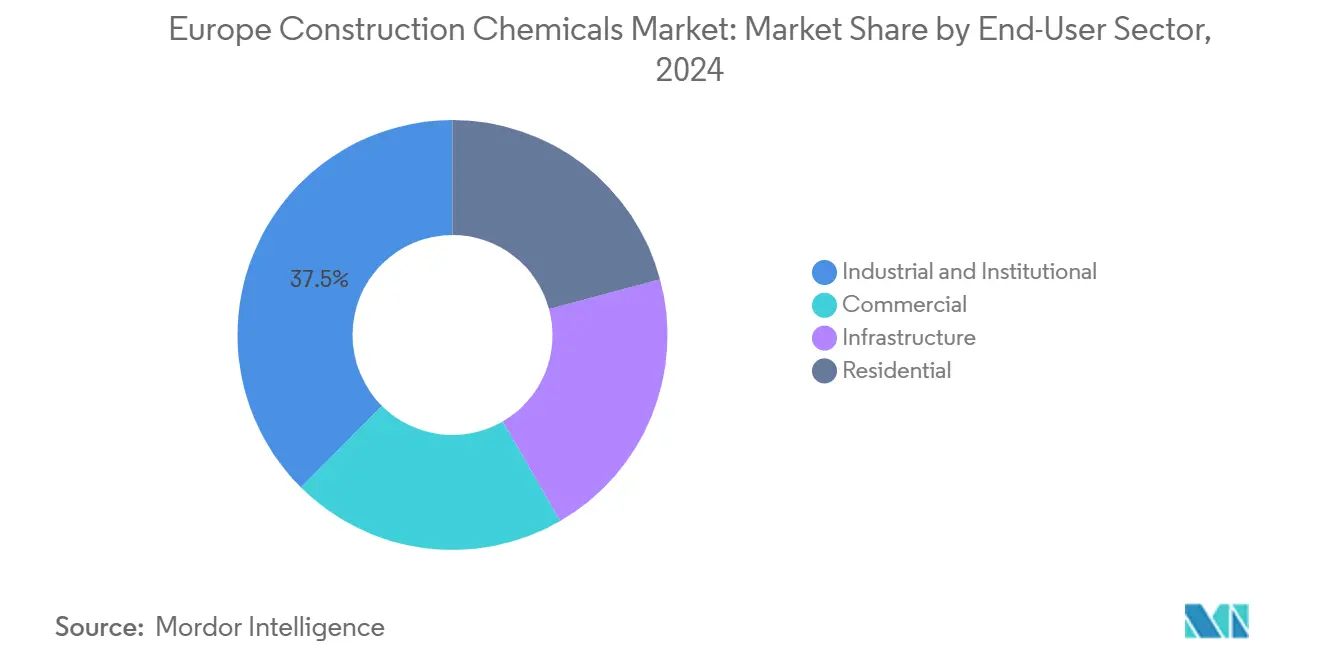

- By end-user sector, industrial and institutional applications accounted for 37.55% of the Europe Construction Chemicals market size in 2024, whereas infrastructure is projected to expand at a 6.94% CAGR through 2030.

- By geography, Germany led with a 14.71% share of the Europe Construction Chemicals market in 2024; Italy records the fastest 5.07% CAGR to 2030.

Europe Construction Chemicals Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal funding accelerates sustainable construction demand | +1.1% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| EU Connecting Europe Facility boosts trans-border infrastructure spend | +1.3% | Cross-border corridors, Central & Eastern Europe priority | Medium term (2-4 years) |

| Stricter EPBD energy-efficiency codes increase demand for high-performance admixtures | +0.8% | EU-wide, phased implementation by member states | Short term (≤ 2 years) |

| Carbon-neutral concrete initiatives adopt novel supplementary cementitious materials | +0.6% | Germany, France, Netherlands leading adoption | Long term (≥ 4 years) |

| Growth of green-hydrogen mega-plants drives specialty grouts for cryogenic tanks | +0.4% | Germany, Netherlands, Denmark hydrogen valleys | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

EU Green Deal funding accelerates sustainable construction demand

The EUR 1 trillion Green Deal investment framework mandates low-carbon renovation across 35 million buildings by 2030, directly increasing volumes for bio-based admixtures, recycled-content waterproofing, and carbon-negative additives that underpin the Europe Construction Chemicals market[1]European Commission, “European Green Deal Investment Plan,” europa.eu. BASF’s bio-based ethyl acrylate launch in late 2024 cut product carbon footprints by 30% while maintaining performance, signaling supplier realignment toward mandatory environmental product declarations under Construction Products Regulation 2024/3110. Financial incentives and green bond eligibility heighten customer preference for products with transparent life-cycle data, creating a premium segment within the Europe Construction Chemicals market. Government renovation subsidies make high-performance sealants, insulation adhesives, and liquid-applied membranes core purchasing priorities for municipal housing operators. As more funding flows from the Social Climate Fund in 2026, market demand for energy-efficient chemistries continues to outpace conventional alternatives, cementing the driver’s medium-term importance.

EU Connecting Europe Facility boosts trans-border infrastructure spend

The EUR 33.7 billion CEF 2021-2027 program channels capital into rail, tunnel, and port projects, thereby increasing demand for specialty chemicals such as high-performance admixtures, rapid-setting mortars, and tunnel waterproofing along corridors like Rail Baltica and the Mediterranean link. Compliance with climate-resilient asset criteria favors carbon-fiber-reinforced systems and self-healing concrete, which extend the structure's lifespan. The Grand Paris Express, co-funded through CEF, alone consumes sizable volumes of spray-applied membranes and low-emission concrete accelerators. Suppliers able to certify multipurpose systems across several national standards secure bid advantages, reinforcing growth momentum for the Europe Construction Chemicals market until the program’s close and anticipated sequel in 2028.

Stricter EPBD energy-efficiency codes increase demand for high-performance admixtures

EPBD revisions require nearly zero-energy performance for new buildings by 2030, prompting architects to adopt thicker insulation, airtight envelopes, and thermal-bridge-eliminating concrete mixes that incorporate advanced admixtures. Germany’s GEG law already enforces tighter U-values, lifting polyurethane foam and thermal-break demand despite a sluggish housing cycle[2]German Federal Ministry for Economic Affairs and Climate Action, “Building Energy Act,” bmwk.de. Retrofit mandates for public buildings increase the consumption of injection grouts and low-viscosity sealers, which improve envelope performance without requiring structural changes. Lifecycle-based EN 15978 assessments drive procurement toward admixtures with audited environmental declarations, giving early-mover suppliers pricing power. Against this backdrop, the Europe Construction Chemicals industry gains both revenue and margin upside from specification-driven product differentiation.

Carbon-neutral concrete initiatives adopt novel supplementary cementitious materials

Cement producers committed to 2050 net-zero pathways are substituting calcined clay, GGBS, and recycled fines, enabling a 47.5% reduction in emissions while meeting EN 206 strength classes. Technologies such as CarbonCure inject recycled CO₂ during batching, improving both compressive strength and reducing the clinker factor simultaneously. The EU Taxonomy classification of low-carbon concrete unlocks green finance, accelerating the adoption of low-carbon concrete across infrastructure and commercial projects. Material passports mandated under Construction Products Regulation (CPR) revisions make embodied-carbon data easily traceable, rewarding suppliers with transparent Supplementary Cementitious Material (SCM) blends. These dynamics strengthen the Europe Construction Chemicals market as novel additives, shrinkage-reducing agents, and performance enhancers become standard in low-carbon mixes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of epoxy, PU, and acrylic feedstocks | -0.70% | EU-wide, particularly affecting import-dependent regions | Short term (≤ 2 years) |

| Stringent VOC and PFAS phase-out regulations restrict solvent-borne chemistries | -0.50% | EU-wide with Denmark leading, phased implementation | Medium term (2-4 years) |

| Shortage of certified applicators for advanced flooring and repair systems | -0.30% | Germany, France, Netherlands most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile prices of epoxy, PU, and acrylic feedstocks

January 2025 spot epoxy resin prices increased by 1.73% as inventories tightened and anti-dumping duties of 10.8%–40.8% were imposed on Asian imports. Polyurethane precursors mirror crude volatility, while energy-intensive acrylic monomer chains face elevated European power costs. Smaller formulators often lack hedging or backward integration, which erodes margins and delays innovation spending. Some customers defer nonessential renovations, marginally dampening volumes in the Europe Construction Chemicals market. Although major producers negotiate long-term contracts, procurement uncertainty is expected to remain a pricing headwind through 2026.

Stringent VOC and PFAS phase-out regulations restrict solvent-borne chemistries

The ECHA draft restriction, covering 10,000 PFAS compounds with thresholds as low as 25 ppb, forces the immediate reformulation of solvent-borne membranes, sealers, and certain superplasticizers. Denmark’s national ban on waterproofing agents, effective in 2026, foreshadows an EU-wide adoption, potentially shrinking usable fluorochemistry options. Simultaneous microplastic rules complicate resin selection, generating R&D costs that disadvantage small players. Suppliers lacking PFAS-free portfolios risk market exit, compressing short-term volumes but ultimately consolidating demand among innovation leaders in the Europe Construction Chemicals market.

Segment Analysis

By Product: Waterproofing solutions lead market consolidation

Waterproofing systems secured a 32.07% Europe Construction Chemicals market share in 2024, underpinned by stringent durability requirements for tunnels, basements, and bridge decks. The segment’s dominance stems from high failure-cost avoidance, which makes end-users favor premium membranes and liquid-applied coatings despite the price premiums. The Europe Construction Chemicals market size for waterproofing grew steadily in 2024 as public-sector renovation grants prioritized moisture-control upgrades. Demand also benefits from rising flood-risk mitigation in riverine regions, encouraging uptake of negative-side slurry mortars and elastomeric overlays. Product innovation focuses on PFAS-free polymers, bio-based asphalt modifiers, and nano-silica-enhanced coatings that maintain adhesion under thermal cycling. SOPREMA’s acquisition strategy combines bitumen, Polymethyl methacrylate (PMMA), and polyurethane technologies, offering system warranties that tighten customer lock-in. Meanwhile, suppliers are accelerating the development of digital detailing tools that integrate with BIM workflows, thereby improving specification compliance and reducing installation errors.

Concrete admixtures represent the fastest-growing product line, with a 5.24% CAGR to 2030, as infrastructure owners demand high-performance mixes that are compatible with low-carbon objectives. High-range water reducers, self-consolidating agents, and shrinkage-compensating additives command premium pricing, lifting the Europe Construction Chemicals market size for admixtures alongside volume growth. Regulatory pressure boosts demand for low-alkali accelerators and chromium-VI-reduced plasticizers, while R&D pipelines focus on nano-clay dispersion technologies that enhance the strength-to-cement ratio. Adhesives and sealants maintain stable demand across curtain-wall, flooring, and façade applications, yet PFAS phase-outs catalyze a wave of silicone and silane-terminated polymer replacements, reshaping competitive positioning inside the Europe Construction Chemicals industry. Flooring resins are gaining traction in data centers and logistics hubs, where static-dissipative and chemical-resistant surfaces are mission-critical. In contrast, anchors and grouts are securing moderate growth in wind-farm foundations and industrial plant retrofits.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Sector: Infrastructure drives growth acceleration

The industrial and institutional segment, while the largest at 37.55% of the Europe Construction Chemicals market share in 2024, expands more slowly due to muted manufacturing PMI trends. Nonetheless, pharmaceutical cleanrooms and semiconductor fabs continue to specify low-VOC flooring resins and antimicrobial coatings. Infrastructure projects are expected to deliver a 6.94% CAGR through 2030, markedly higher than the market average, as EU and national recovery funds flow into rail, road, port, and renewable energy assets. Major corridor schemes such as Rail Baltica and the Brenner Base Tunnel consume specialty admixtures and tunnel gaskets, enlarging the Europe construction chemicals market size for infrastructure-specific solutions. Flood-defense upgrades in the Netherlands and Germany stimulate consumption of sulfate-resistant grouts and shotcrete accelerators.

The residential sector contracted by 7.7% in 2024 and is expected to decline by 3.9% in 2025, reflecting cost-of-living pressures and higher mortgage rates, which are pulling down volumes of commodity tile adhesives and sealants. Commercial construction edges sideways at 0.1% growth but shows hotspots in data center build-outs that require fire-resistant coatings and high-load anchors. Suppliers with balanced exposure to infrastructure and industrial capital expenditure sustain revenue even as housing starts weaken. Diversification into refurbishment chemicals offers resilience because renovation activity benefits from EPBD incentives despite new-build softness, reaffirming infrastructure as the chief growth locomotive within the Europe Construction Chemicals market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany remained the largest territory, accounting for 14.71% of the Europe Construction Chemicals market in 2024 on the back of a EUR 500 billion federally backed infrastructure pipeline stretching to 2035. Transport corridor upgrades and offshore wind grid links sustain demand for crack-bridging membranes and marine-grade grouts, even though total construction spending is projected to decline by 2.5% in 2025. Federal defense-facility hardening creates a niche demand for blast-resistant coatings, shielding suppliers from the residential slump.

Italy exhibits the fastest 5.07% CAGR, fueled by EUR 191.5 billion Recovery and Resilience Plan allocations that prioritize seismic retrofits, digital infrastructure, and energy-efficient public buildings. Northern regions invest in industrial plant modernization, substituting solvent-borne epoxy floors with water-borne polyaspartic alternatives, while Southern regions deploy waterproofing and admixture packages for basic road and hospital upgrades. The rapid drawdown rate of EU funds accelerates tender issuance, translating to front-loaded chemical demand.

France faces transitional headwinds; construction investment declined 3.9% in 2024, yet the Grand Paris Express ensures consistent tunnel-grade admixture consumption and mitigates market contraction. The United Kingdom experiences regulatory divergence post-Brexit, but net-zero building commitments echo EU trends, keeping PFAS-free innovations relevant. Spain’s logistical-park boom supports polyurethane flooring systems, whereas Central and Eastern Europe capture spillover demand as manufacturing reshoring raises new plant construction. Across these diverse trajectories, suppliers that localize service and logistics capabilities align most effectively with the Europe construction chemicals market’s fragmented regional profiles.

Competitive Landscape

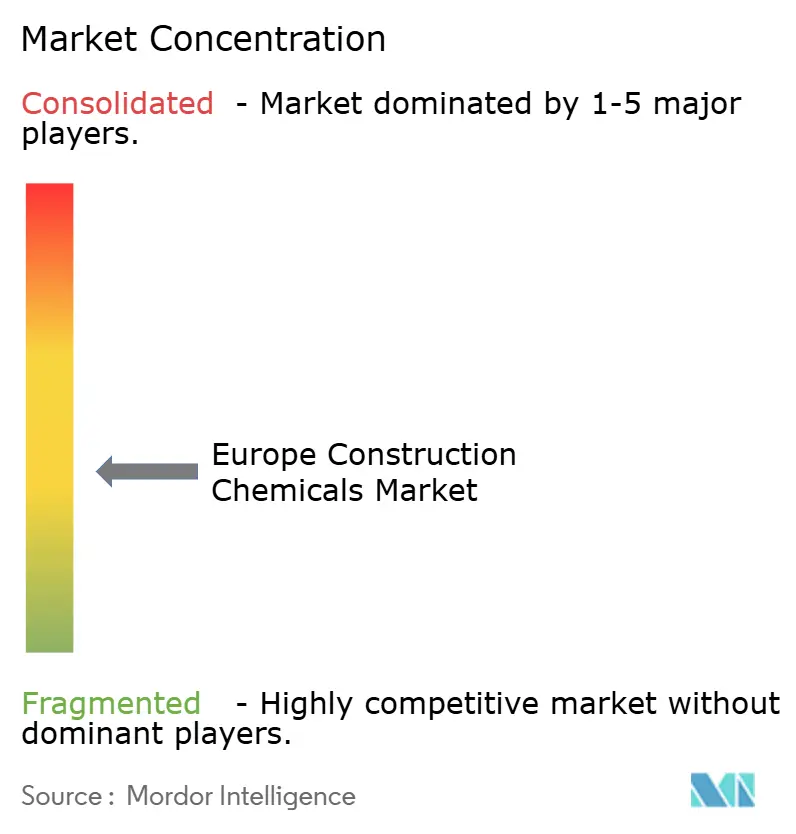

The Europe Construction Chemicals market is moderately fragmented. Technology investment differentiates leaders; BASF’s 2024 move into bio-based ethyl acrylate proves the viability of mass-scale bio-derivatives. Henkel, Arkema, and RPM build proprietary silane-terminated polymer backbones that avoid PFAS liabilities while achieving weather resistance. Smaller regional firms face rising compliance costs and raw material volatility, prompting interest in bolt-on acquisitions from multinationals seeking geographic density or specialty gaps.

Europe Construction Chemicals Industry Leaders

-

MAPEI S.p.A.

-

Saint-Gobain

-

Sika AG

-

Henkel AG and Co. KGaA

-

Arkema

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Sika AG launched SikaTile-150 Moisture Guard Fabric Membrane and SikaTile-250 Fracture Guard UCM globally. SikaTile-150 Moisture Guard Fabric Membrane is a dependable solution for waterproofing showers, tub surrounds, walls, and wet areas.

- June 2025: Cemex Europe, Middle East, and Africa (EMEA) launched a prime family of advanced admixture solutions by harnessing innovative formulations and advanced chemical technologies. These admixtures significantly reduce the carbon footprint of their concrete and cement products.

Europe Construction Chemicals Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, Surface Treatment Chemicals, Waterproofing Solutions are covered as segments by Product. France, Germany, Italy, Russia, Spain, United Kingdom are covered as segments by Country.

By Product

| Adhesives | Hot-Melt |

| Reactive | |

| Solvent-borne | |

| Water-borne | |

| Anchors and Grouts | Cementitious Fixing |

| Resin Fixing | |

| Concrete Admixtures | Accelerator |

| Air-Entraining | |

| Super-plasticizer | |

| Retarder | |

| Shrinkage-Reducer | |

| Viscosity-Modifier | |

| Plasticizer | |

| Other Types | |

| Concrete Protective Coatings | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyurethane | |

| Other Resins | |

| Flooring Resins | Acrylic |

| Epoxy | |

| Polyaspartic | |

| Polyurethane | |

| Other Resins | |

| Repair and Rehabilitation Chemicals | Fiber-Wrapping Systems |

| Injection Grouting | |

| Micro-concrete Mortars | |

| Modified Mortars | |

| Rebar Protectors | |

| Sealants | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| Surface-Treatment Chemicals | Curing Compounds |

| Mold-Release Agents | |

| Other Types | |

| Waterproofing Solutions | Chemicals |

| Membranes |

By End-User Sector

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

By Geography

| France |

| Germany |

| Italy |

| Russia |

| Spain |

| United Kingdom |

| Rest of Europe |

| By Product | Adhesives | Hot-Melt |

| Reactive | ||

| Solvent-borne | ||

| Water-borne | ||

| Anchors and Grouts | Cementitious Fixing | |

| Resin Fixing | ||

| Concrete Admixtures | Accelerator | |

| Air-Entraining | ||

| Super-plasticizer | ||

| Retarder | ||

| Shrinkage-Reducer | ||

| Viscosity-Modifier | ||

| Plasticizer | ||

| Other Types | ||

| Concrete Protective Coatings | Acrylic | |

| Alkyd | ||

| Epoxy | ||

| Polyurethane | ||

| Other Resins | ||

| Flooring Resins | Acrylic | |

| Epoxy | ||

| Polyaspartic | ||

| Polyurethane | ||

| Other Resins | ||

| Repair and Rehabilitation Chemicals | Fiber-Wrapping Systems | |

| Injection Grouting | ||

| Micro-concrete Mortars | ||

| Modified Mortars | ||

| Rebar Protectors | ||

| Sealants | Acrylic | |

| Epoxy | ||

| Polyurethane | ||

| Silicone | ||

| Other Resins | ||

| Surface-Treatment Chemicals | Curing Compounds | |

| Mold-Release Agents | ||

| Other Types | ||

| Waterproofing Solutions | Chemicals | |

| Membranes | ||

| By End-User Sector | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| Residential | ||

| By Geography | France | |

| Germany | ||

| Italy | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- END-USE SECTOR - Construction chemicals consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of construction chemical products such as concrete admixtures, repair and rehabilitation chemicals, flooring resins, waterproofing solutions, anchors and grouts, adhesives and sealants, and surface treatment chemicals is considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF