Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

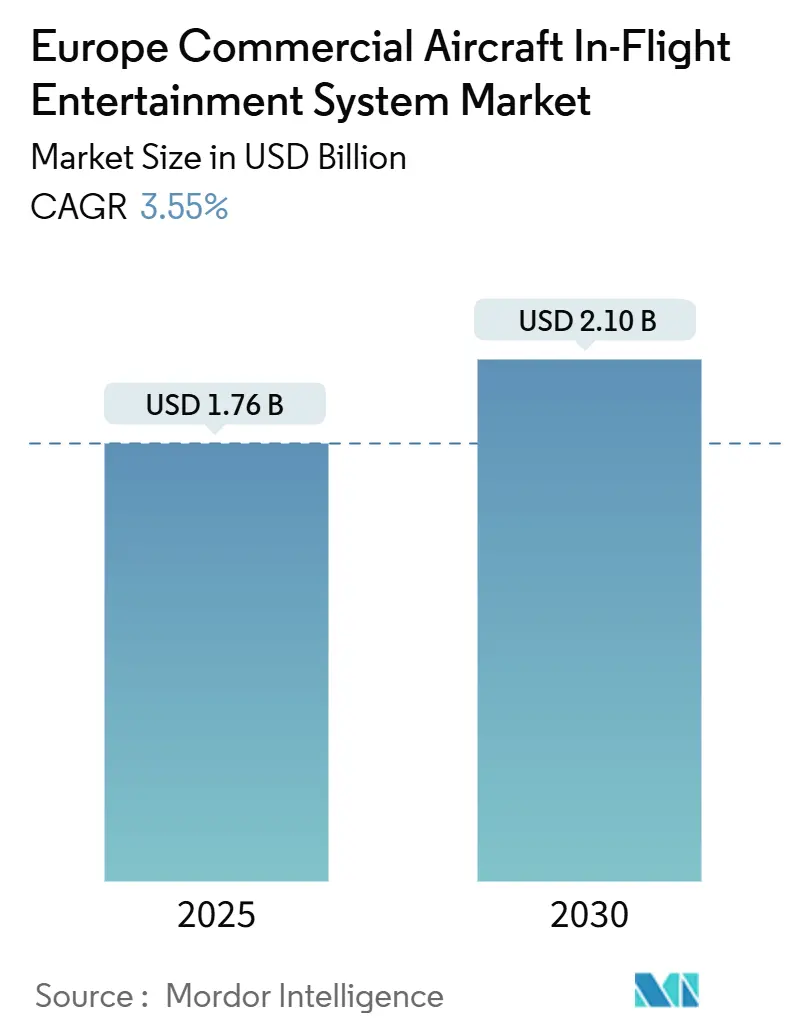

| Market Size (2025) | USD 1.76 Billion |

| Market Size (2030) | USD 2.10 Billion |

| Growth Rate (2025 - 2030) | 3.55% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Commercial Aircraft In-Flight Entertainment System Market Analysis by Mordor Intelligence

The European commercial aircraft in-flight entertainment (IFE) system market size is USD 1.76 million in 2025 and is projected to reach USD 2.10 million in 2030, reflecting a 3.55% CAGR. This performance highlights a mature regional aviation ecosystem, where incremental technology upgrades, rather than capacity increases, drive demand for cabin-based digital services. Airlines now weigh carbon savings, cybersecurity compliance, and retrofit lead times when selecting solutions, pushing suppliers to deliver lighter architectures, hybrid seat-back plus wireless options, and certification-ready hardware. Competitive advantages accrue to vendors with multi-orbit satellite partnerships, pan-European maintenance stations, and proven EASA relationships.

Key Report Takeaways

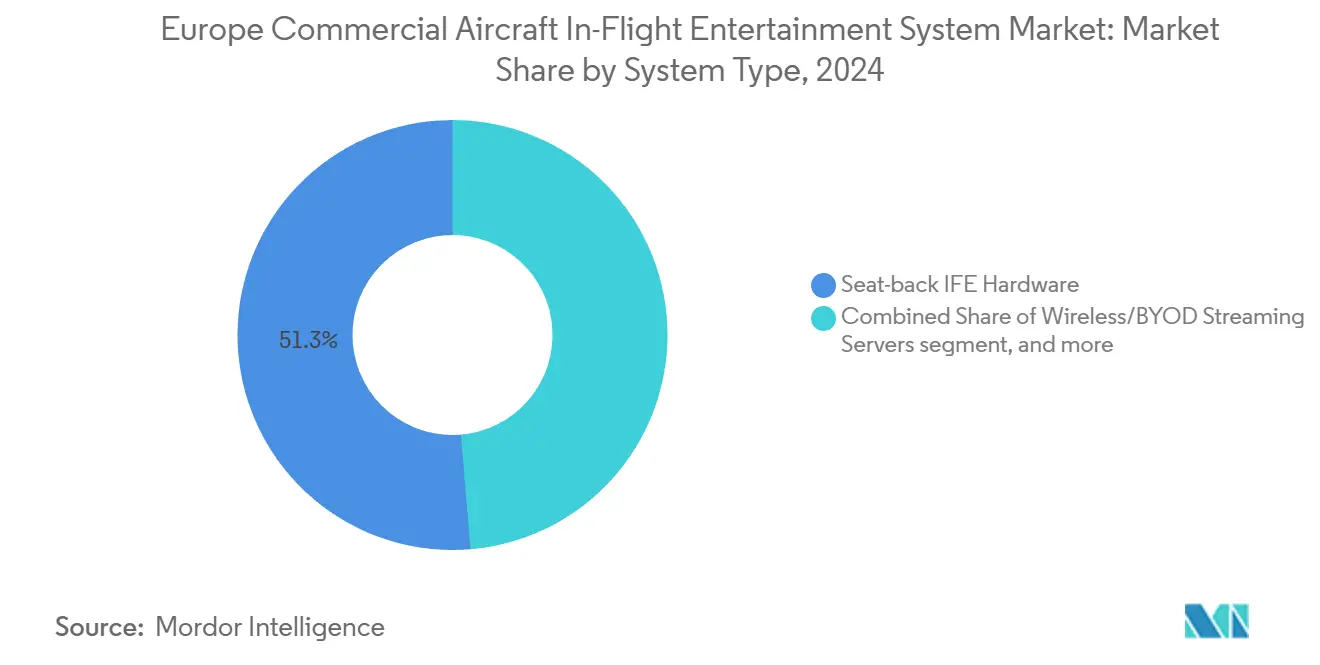

- By system type, seat-back hardware held 51.34% of the European commercial aircraft IFE system market size in 2024; however, wireless and BYOD architectures are expected to expand at a 2.45% CAGR through 2030.

- By aircraft type, narrowbody jets led the European commercial aircraft IFE system market with a 52.56% share in 2024, while widebody platforms posted the fastest growth rate of 4.34% through 2030.

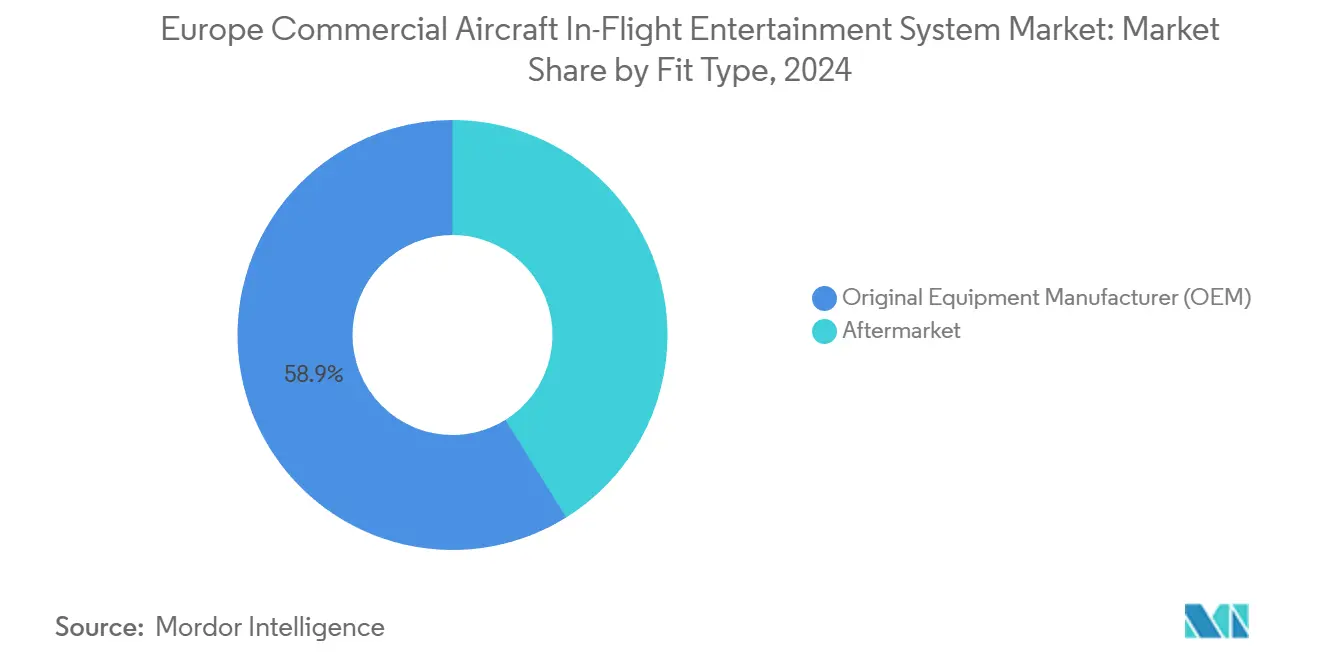

- By fit type, aftermarket retrofits commanded a 4.76% CAGR through 2030, outpacing OEM installs that held 58.87% of the European commercial aircraft IFE system market size in 2024.

- By cabin class, premium economy is projected to advance at a 4.23% CAGR, overtaking the economy cabin’s 43.55% revenue base within the European commercial aircraft IFE system market.

- By geography, Germany accounted for a 30.25% regional share in 2024, and Spain recorded the fastest 4.89% CAGR to 2030 within the European commercial aircraft IFE system market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Commercial Aircraft In-Flight Entertainment System Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for high-bandwidth connectivity aboard European fleets | +1.2% | Germany, UK, France, Netherlands | Medium term (2-4 years) |

| Airlines' focus on ancillary-revenue generation through IFEC portals | +0.8% | Germany, Turkey, Spain | Short term (≤ 2 years) |

| Fleet-modernization cycles boosting retrofit opportunities | +0.9% | Germany, France, UK, Rest of Europe | Long term (≥ 4 years) |

| EU sustainability goals accelerating shift to lighter wireless IFE | +0.6% | EU core markets, spillover to Turkey, UK | Medium term (2-4 years) |

| LEO-satellite roll-outs enabling seamless pan-European coverage | +0.7% | Pan-European | Medium term (2-4 years) |

| NIS2 cybersecurity rules forcing hardware/software refresh | +0.5% | EU member states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand for High-bandwidth Connectivity Aboard European Fleets

Passenger expectations now mirror at-home streaming habits, prompting flagship programs such as Turkish Airlines’ pledge to offer complimentary Wi-Fi fleet-wide by late 2025.[1]Turkish Airlines, “Corporate Communications: Free Wi-Fi Rollout,” turkishairlines.com Lufthansa’s Allegris cabin integrates next-generation satellite pipes that support UHD streaming, real-time gaming, and cloud-based applications.[2]Lufthansa Group, “Allegris Cabin Program,” lufthansa.com Airlines perceive connectivity as a brand differentiator that justifies fare premiums and loyalty gains. The decisive shift from legacy Ku-band to high-throughput multi-orbit constellations unlocks concurrent data streams without buffering bottlenecks. Suppliers able to certify multi-band antennae and deliver cabin-network cybersecurity conforming to ED-202B secure a durable advantage. As bandwidth becomes an amenity rather than an upsell, carriers bundle unlimited data packages into high-yield fare families, driving recurring revenue for service providers even on intra-Europe stage lengths.

Airlines’ Focus on Ancillary-revenue Generation Through IFEC Portals

Seat-back and wireless portals have evolved into digital storefronts that extend duty-free aisles, trip-planning tools, and content subscriptions well beyond the cruise phase. Moment’s 2025 acquisition of Airfree expanded access to 350+ global retailers, enabling home or gate delivery for goods purchased in-flight.[3]Moment, “Acquisition of Airfree,” moment.tech Data from Touch Inflight Solutions shows that passengers engaging with onboard digital services spend USD 90 per flight on extras, substantially lifting non-ticket margins.[4]PAX International, “Touch Inflight Solutions partners with Parrot Analytics,” pax-intl.com Artificial intelligence (AI) modules analyze viewing histories and payment patterns to push hyper-relevant offers, increasing conversion rates while preserving seat-back real estate for high-margin advertising. Airlines embed live credit-card tokenization within hardened networks, which now constitute a core pillar of their long-term commercial strategy.

Fleet-modernization Cycles Boosting Retrofit Opportunities

OEM delivery delays and capital-discipline policies compel carriers to overhaul cabins on mid-life airframes rather than source new hulls. Finnair’s refurbishment of 12 Embraer E190s, with an average age of 16.8 years, highlights lifecycle extension trends that incorporate lighter monuments and streaming-first entertainment backbones. Airbus anticipates roughly 390 A350s will reach the 8-year service threshold by 2028, triggering significant retrofit demand that includes 4K displays and HBCplus connectivity provisions. MRO providers bundle nose-to-tail cabin projects with pre-certified IFE kits, optimizing hangar slots and easing EASA liaison burdens. Retrofit CAGRs now outpace line-fit growth, sustaining the European commercial aircraft IFE system market through cyclical traffic fluctuations.

EU Sustainability Goals Accelerating Shift to Lighter Wireless IFE

The EU’s “Fit for 55” roadmap motivates airlines to shave every unnecessary kilogram. Studies by the Aerospace Technology Institute flag traditional LCD seat-back screens as among the heaviest cabin components, prompting carriers to seek weight savings of up to 70% through bring-your-own-device (BYOD) architectures and thin OLED panels. TactoTek’s injection-molded structural electronics demonstrate 50-70% weight reduction, translating to lifecycle emission cuts of 25 tonnes per kilogram removed. Airlines link these carbon savings directly to corporate ESG disclosures, accelerating procurement toward wireless streaming boxes, projectors, or tablet-rental models that satisfy passenger leisure needs with lower fuel burn.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation and certification costs | -0.7% | Pan-European, smaller carriers | Long term (≥ 4 years) |

| Stringent EASA certification timelines | -0.5% | EU member states, UK | Medium term (2-4 years) |

| Fragmented national spectrum rules delaying IFC deployments | -0.4% | EU core | Short term (≤ 2 years) |

| Trans-Atlantic tariff disputes inflating avionics component prices | -0.3% | Global supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Installation and Certification Costs

EASA airworthiness directives require exhaustive test flights, wiring-integrity checks, and cyber-resilience audits, which prolong the development of Europe's commercial aircraft IFE systems by 12-36 months. Airbus reports A350 retrofit lead times of at least 12 months, stretching to three years for complex modifications. Engineering consultancy fees, labor hours, and hardware staging can lift program budgets beyond USD 2 million per widebody, a financial burden acutely felt by smaller carriers. The composite structures of next-generation aircraft complicate antenna mounting and thermal-dissipation analyses, adding further expense. Suppliers with in-house Design Organization Approval (DOA) status and dedicated liaison officers capture a disproportionate share by shortening the path to Supplemental Type Certificates (STCs).

Stringent EASA Certification Timelines

In October 2024, EUROCAE released ED-202B, introducing mandatory cyber-secure development cycles for all onboard digital systems, including IFE that exchange passenger data or interface with aircraft networks. Existing operators must deploy an Information Security Management System by October 2025, while new applicants will face deadlines in February 2026. These layered obligations force airlines to weigh certification risk over raw feature innovation, influencing vendor selection toward incumbents with proven compliance records. Mod-stack reversions, required when third-party STCs conflict with OEM update packages, extend ground time and create opportunity costs that temper short-term adoption rates.

Segment Analysis

By Aircraft Type: Narrowbody Capacity Leads, Widebody Revenue Upside

Seat-back platforms still held 51.34% value in 2024, but wireless and BYOD IFE solutions are on a 2.45% CAGR uptrend as operators blend embedded screens in premium cabins with BYOD streaming elsewhere. The demand for hybrid kits is forecasted to be driven by airlines that upgrade legacy screens while avoiding costly all-seat replacements. Wireless-only installs flourish among ULCCs that zero-base cabin weight budgeting, though revenue-share models with connectivity providers offset capital outlay.

Paris-based SkyLights promotes cinema-grade VR headsets that bypass seat-back sunk costs, while Moment’s Flymingo box streams over 10,000 hours of content to passenger devices, weighing under 2 kg. Airlines now stipulate open API layers so future AR/VR extensions can piggyback existing cabin networks. This plug-and-play ethos cements hybrid frameworks as the pragmatic path toward long-run digital-service monetization without stranding assets.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By System Type: Hybrid Architectures Become Default Specification

Narrowbodies accounted for 52.56% of the European commercial aircraft IFE system market share in 2024, reflecting dense intra-Europe route maps and standardized installation templates that lower unit costs. Widebody programs are expected to post a 4.34% CAGR, underpinned by IAG’s 2025 order for 71 long-haul jets that will enter service with UHD seat-back screens and multi-band antennas. Regional jets hold a niche position, often adopting streaming-only platforms to minimize payload penalties.

Continental carriers deploy lightweight wireless equipment on A320-family workhorses to balance cost and passenger satisfaction during short stage lengths. In contrast, the emerging premium-heavy A350-900 and B787-10 cabins utilize larger, high-resolution displays, surround-sound Bluetooth, and personalized e-commerce widgets to achieve higher yields. As supply-chain bottlenecks persist, retrofit campaigns on mature single-aisle fleets sustain the European commercial IFE system market. At the same time, new widebody deliveries generate higher revenue per ship-set due to the complexity of cabin zoning.

By Fit Type: Aftermarket Momentum Outpaces OEM Installations

The OEM channel accounted for 58.87% of 2024 revenue, as new A320neo and A350 deliveries left the final assembly line with factory-installed displays, servers, and antennas that arrive flight-ready and certified to Airbus and Boeing standards. Even so, the aftermarket is expected to expand at a 4.76% CAGR through 2030 as carriers extend aircraft service lives and harmonize cabin products across mixed fleets. Deferred airframe orders and lingering supply-chain bottlenecks push operators to refurbish in-service jets rather than wait for new slots, redirecting capital to turnkey retrofit campaigns timed with C-checks. European MRO houses now combine carpet, seat cover, LED lighting, and server upgrades in a single downtime event, lowering the per-tail cost versus separate standalone installs. Electra Airways’ plan to modernize its eight-jet A320 fleet illustrates how even smaller operators can realize more than 1-ton weight savings through integrated cabin packages that include lighter wireless IFE hardware.

Aftermarket demand also benefits from the NIS2 cybersecurity mandate, which requires the removal of legacy media servers lacking encryption or intrusion-detection functions, creating a compliance-driven refresh wave that peaks in 2026. Vendors streamline STC libraries, allowing for the installation of identical wireless servers across A320ceo, B737NG, and Embraer 190 variants with minimal re-engineering, thereby reducing paperwork and turnaround times for operators with diverse fleets. Airlines frequently bundle content-management subscriptions and real-time analytics into service-level agreements, turning capital-intensive hardware swaps into predictable operating expenses. As retrofit labor pipelines tighten, incumbents such as Lufthansa Technik and Air France Industries leverage hangar availability inside their home markets to capture regional contracts, keeping installation revenues within Europe even when the hardware is sourced from the US or Asian suppliers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Cabin Class: Premium economy captures upsell demand

Economy class retained 43.55% revenue in 2024, but premium economy seats are forecast for a 4.23% CAGR as travelers seek affordable comfort and airlines pursue margin-rich upsells. Europe's commercial aircraft IFE system market share for premium economy rose in tandem with Air France's new La Première suite and the rollout of premium economy. Business-class screens transition to 4K resolution with Bluetooth LE audio, further accentuating the experiential gap between economy and business classes.

Passenger surveys reveal willingness to pay USD 86-115 extra on intra-European legs when seats include power outlets, curated OTT catalogs, and high-speed messaging. Airlines tailor content bundles by cabin: early-window Hollywood titles are featured upfront, while ad-supported streaming content is placed at the back. This mass-customization strategy supports ancillary-spend models while maintaining CAPEX discipline, thereby enhancing the European commercial aircraft IFE system's marketability profile.

Geography Analysis

Germany generated 30.25% of 2024 revenue, anchored by the Lufthansa Group’s multibillion-euro Allegris cabin program, which marries custom seat shells with 17-inch OLED displays and gigabit-class satellite pipes. Local OEM clusters in Hamburg and Munich shorten design-approval cycles and support rich aftermarket ecosystems, making Germany the linchpin for high-specification purchases. The European commercial aircraft IFE system market size in Germany is projected to top USD 50 million by 2030 as retrofit waves converge with fresh A350 and B777-9 deliveries.

Spain posts the swiftest 4.89% CAGR, powered by Iberia’s network expansion and resurgent tourism. Iberia introduces new routes for summer 2025, compelling fleet-wide Wi-Fi standardization to attract price-sensitive leisure travelers.

France and the United Kingdom exhibit mature adoption curves, yet each pursues differentiated premium-cabin makeovers to capture leisure-long-haul and corporate contracts. Iberia’s A350 fleet employs Safran RAVE Ultra displays, while British Airways retrofits B777 fleets with Thales AVANT systems that streamline crew maintenance workflows. The Rest of Europe cluster, including the Nordics, Benelux, and Central Europe, tends toward BYOD kits for cost control; however, upticks in charter and ACMI activity introduce new retrofitted volumes. Collectively, these sub-regions sustain the European commercial aircraft IFE system market through balanced growth across diverse economic cycles.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The market is concentrated, with the top five vendors commanding the majority of the revenue, led by Panasonic Holdings Corporation, Thales Group, Collins Aerospace (RTX Corporation), and Safran SA. Panasonic operates 64 maintenance stations across nine repair hubs, providing 24/7 AOG dispatch that few competitors can match. Thales leverages dual-headquartered R&D in Toulouse and Irvine, delivering AVANT Up screens paired with Spotify-integrated UX layers. Collins combines ARINC cabin-router heritage with SES multi-orbit agreements, enabling tailored bandwidth plans per route.

Digital-native disruptors such as Moment, AirFi, and Display Interactive focus on software-defined boxes weighing under 2 kg and deployable overnight. Neo Space Group’s September 2025 deal to buy Display Interactive merges a multi-orbit modem with a proven passenger portal, signaling consolidation amongst challengers. Major airlines hedge risk by dual-sourcing, allocating premium cabins to legacy providers and economy sections or regional subsidiaries to agile newcomers.

Strategic moves in 2025 underscore the importance of service-centric business models. Maxposure’s acquisition of Neutral Digital folds VR, 3D cabin tours, and granular ad-targeting into a single content-services stack, ready for plug-in on Panasonic or Thales hardware. Safran’s joint venture with Intelsat establishes an IFC revenue-share program, reducing airlines’ CAPEX barrier. These collaborations illustrate how suppliers reposition from equipment sellers to lifecycle-service orchestrators within the European commercial aircraft IFE system market.

Europe Commercial Aircraft In-Flight Entertainment System Industry Leaders

-

Thales Group

-

Panasonic Holdings Corporation

-

Safran SA

-

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Safran Passenger Innovations (SPI) innovated to enhance accessibility in the aviation industry by unveiling its final designs for the Accessible IFE system. These designs were initially introduced at the previous year's Aircraft Interiors Expo.

- April 2025: Panasonic Avionics Corporation signed an agreement with Air India, India’s leading global airline, to install its Astrova IFE solution and a suite of digital services on the carrier’s new widebody aircraft.

- April 2025: Airbus signed a Memorandum of Understanding (MoU) with Panasonic Avionics to explore a strategic partnership for the future Connected Aircraft platform. The collaboration aims to develop a new on-board architecture utilizing Panasonic Avionics' next-generation IFE hardware and its Converix software server platform, with a definitive agreement expected later in 2025.

Europe Commercial Aircraft In-Flight Entertainment System Market Report Scope

By System Type

| Seat-back IFE Hardware |

| Wireless/BYOD Streaming Servers |

| In-seat Power and Peripherals |

| Cabin Connectivity (Ku/Ka/LEO) |

By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

By Fit Type

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

By Cabin Class

| First Class |

| Business Class |

| Premium Economy Class |

| Economy Class |

By Geography

| United Kingdom |

| France |

| Germany |

| Spain |

| Rest of Europe |

| By System Type | Seat-back IFE Hardware |

| Wireless/BYOD Streaming Servers | |

| In-seat Power and Peripherals | |

| Cabin Connectivity (Ku/Ka/LEO) | |

| By Aircraft Type | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| By Fit Type | Original Equipment Manufacturer (OEM) |

| Aftermarket | |

| By Cabin Class | First Class |

| Business Class | |

| Premium Economy Class | |

| Economy Class | |

| By Geography | United Kingdom |

| France | |

| Germany | |

| Spain | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Market Definition

- Product Type - Entertainment provided to aircraft passengers during a flight refers to In-flight entertainment. The seatback screens which are used to provide entertainment are included under the IFE system product type.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF