Market Size of Europe Cargo And Vehicle Screening Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

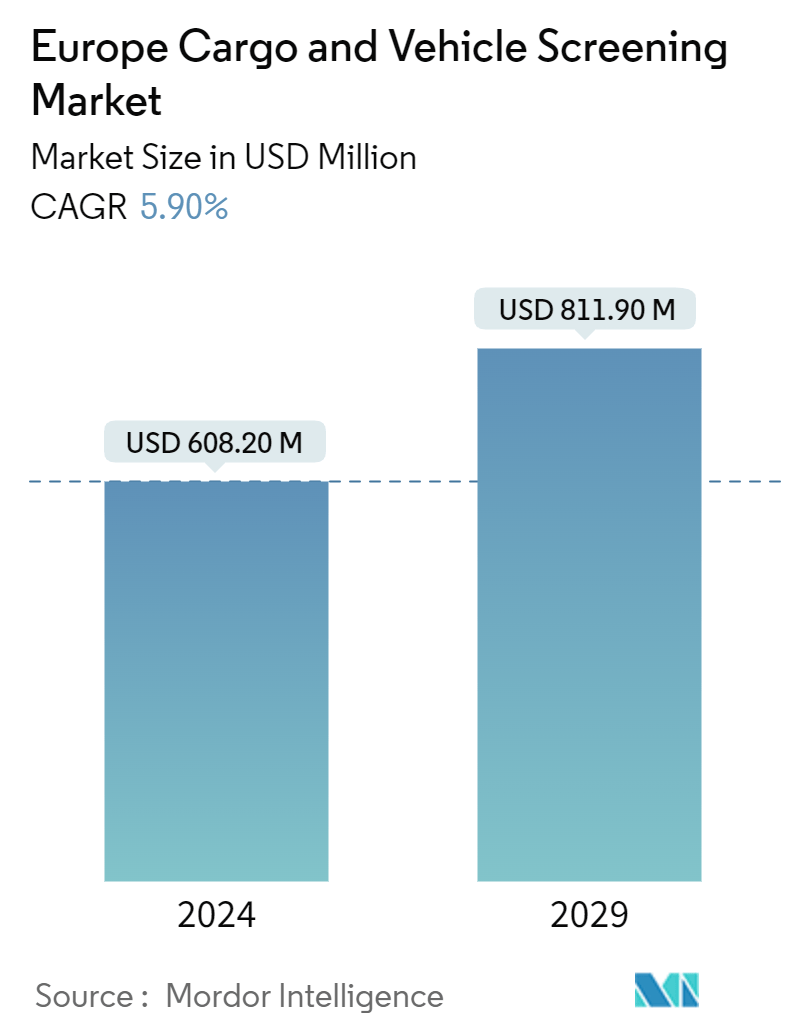

| Market Size (2024) | USD 608.20 Million |

| Market Size (2029) | USD 811.90 Million |

| CAGR (2024 - 2029) | 5.90 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Cargo And Vehicle Screening Market Analysis

The Europe Cargo And Vehicle Screening Market size is estimated at USD 608.20 million in 2024, and is expected to reach USD 811.90 million by 2029, growing at a CAGR of 5.90% during the forecast period (2024-2029).

Cargo screening technologies are being implemented to proactively detect and deter illicit activities within the cargo supply chain. The primary goal is to bolster cargo security while ensuring the unimpeded flow of trade. Notably, there's a heightened focus on bolstering supply chain security and risk assessment, fueling a notable uptick in adopting advanced cargo screening tools and systems in the European region.

• The market is expected to witness a significant surge in Europe owing to the increasing adoption of cargo screening and detection devices throughout the European Union nations in response to the escalating terrorist activities and the changing geo-political dynamics.

• The projected surge in demand for high-efficiency security solutions, in conjunction with the upsurge in terrorist and smuggling activities, is anticipated to increase the implementation of screening devices at major entry points for cargo and vehicles across various European countries. For instance, in April 2024, the Federal Security Service (FSB) reported a significant seizure of explosives in Russia's Pskov region, near the Latvian border. The agency confiscated dozens of kilos of explosives during a routine cargo inspection.

• In early 2023, Romania and Bulgaria led a joint operation, joined by law enforcement agencies from 31 countries, to apprehend suspects involved in procuring firearms from illicit dealers. Facilitated by Europol, this operation led to the seizure of 1,621 weapons, along with 24,735 rounds of ammunition and explosives. Europol's crucial support in combating illegal arms and explosives trafficking underscores its significance. As a result, the rising trend in illicit activities is likely to drive a notable surge in the demand for advanced explosive detection screening technologies, driving opportunities in the market studied.

• Furthermore, to address the rising challenge of drug trafficking, the European Union is proactively crafting regulatory frameworks. These frameworks target the identification of high-risk shipments and goods, particularly those that could jeopardize the security and welfare of the EU and its populace. Such trends also create a favorable ecosystem for the market's growth in the region.

• In addition, the region's market is poised for substantial growth, driven by heightened vendor engagements. Notably, Nuctech has solidified its footing in Europe, with installations in 26 of the 27 EU member states. While facing exclusion from the US market on national security grounds, the company has strategically deployed its cargo scanners. These scanners are operational along Finland's Russian border, at key EU entry points like Belarus and Ukraine, and even at a critical nuclear missile storage facility nestled between Lithuania and Poland.

• Throughout the forecast period, the market could face challenges stemming from budget constraints, regulatory hurdles, and a shortage of skilled labor. Moreover, a lack of screening machines and trained staff might result in cargo piling up on the land side. Furthermore, the market's expansion could be hampered by a demand for enhanced expertise in managing and rectifying machine malfunctions.

• The post-covid period has been challenging for the European countries. Apart from witnessing an economic downturn, the outbreak of war between Russia and Ukraine has significantly influenced the country's economic and geopolitical landscape. While the economic uncertainty of the region may have a negative impact on the market's growth, the changing geo-political dynamics are anticipated to drive countries across the region to invest in advanced cargo and vehicle screening solutions to ensure the safety and security of the people and infrastructure, creating a favorable ecosystem for the market's growth.

Europe Cargo And Vehicle Screening Industry Segmentation

- A cargo and vehicle inspection system inspects cargo and vehicles for unwanted items such as drugs, explosives, or weapons. The inspection process ensures the quality of commodity cargo and its services, which are also used to ensure that all the required standards and regulations are met. The study comprehensively analyzes the trends and dynamics related to cargo and vehicle screening solutions by tracking the market across various segments. Furthermore, it considers the sales of cargo and vehicle screening solutions by major European market players as a baseline for market estimations.

- The European cargo and vehicle screening market is segmented by type of screening system (stationary screening and mobile screening), by end-user vertical (airports, ports and borders, government and defense, critical infrastructure, and commercial), and by country (United Kingdom, Germany, France, and Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type of Screening System | |

| Stationary Screening | |

| Mobile Screening |

| By End User Vertical | |

| Airports | |

| Ports and Borders | |

| Government and Defense | |

| Critical Infrastructure | |

| Commercial |

| By Country*** | |

| United Kingdom | |

| Germany | |

| France | |

| Netherlands | |

| Russia | |

| Spain |

Europe Cargo And Vehicle Screening Market Size Summary

The European cargo and vehicle screening market is poised for significant growth, driven by the increasing need for enhanced security measures across the region. This demand is largely fueled by the rising concerns over terrorist activities and geopolitical tensions, prompting European nations to adopt advanced screening technologies to secure their supply chains. The market is characterized by the implementation of sophisticated cargo screening systems aimed at detecting and preventing illicit activities, thereby ensuring the smooth flow of trade. The focus on supply chain security and risk assessment is further propelling the adoption of these technologies, creating a robust market environment. Key players in the industry are actively engaging in strategic initiatives, such as product innovations and collaborations, to strengthen their market presence and cater to the growing demand for security solutions.

The market landscape is moderately competitive, with major vendors like Nuctech, Westminster Group, and Smiths Detection leading the charge. These companies are leveraging technological advancements, such as mobile screening devices and X-ray technology, to enhance their offerings and address the challenges posed by drug trafficking and smuggling. The United Kingdom stands out as a prominent market within Europe, supported by its extensive freight and logistics industry and the increasing need for advanced screening solutions due to rising illegal activities. Despite potential challenges like budget constraints and regulatory hurdles, the market is expected to thrive, driven by the strategic investments in security infrastructure and the ongoing efforts to combat illicit trade and ensure public safety.

Europe Cargo And Vehicle Screening Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness- Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Consumers

-

1.2.3 Threat of New Entrants

-

1.2.4 Intensity of Competitive Rivalry

-

1.2.5 Threat of Substitutes

-

-

1.3 Impact of Macro Trends on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Type of Screening System

-

2.1.1 Stationary Screening

-

2.1.2 Mobile Screening

-

-

2.2 By End User Vertical

-

2.2.1 Airports

-

2.2.2 Ports and Borders

-

2.2.3 Government and Defense

-

2.2.4 Critical Infrastructure

-

2.2.5 Commercial

-

-

2.3 By Country***

-

2.3.1 United Kingdom

-

2.3.2 Germany

-

2.3.3 France

-

2.3.4 Netherlands

-

2.3.5 Russia

-

2.3.6 Spain

-

-

Europe Cargo And Vehicle Screening Market Size FAQs

How big is the Europe Cargo And Vehicle Screening Market?

The Europe Cargo And Vehicle Screening Market size is expected to reach USD 608.20 million in 2024 and grow at a CAGR of 5.90% to reach USD 811.90 million by 2029.

What is the current Europe Cargo And Vehicle Screening Market size?

In 2024, the Europe Cargo And Vehicle Screening Market size is expected to reach USD 608.20 million.