Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 0.52 Billion |

| Market Size (2030) | USD 0.84 Billion |

| Growth Rate (2025 - 2030) | 10.10% CAGR |

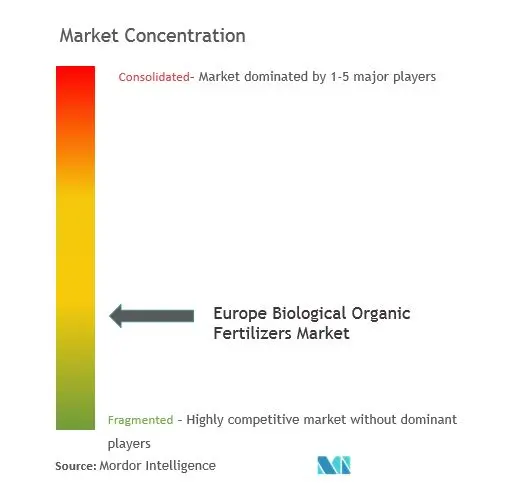

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Biological Organic Fertilizers Market Analysis by Mordor Intelligence

The Europe biological organic fertilizers market size reached USD 0.52 billion in 2025 and is projected to rise to USD 0.84 billion by 2030, reflecting a 10.10% CAGR during the forecast period. Policy mandates that convert cropland to certified organic systems, tight nitrate-loss caps, and rapid biogas-digestate scale-up are lifting demand, while precision fertigation and insect-frass innovation are reshaping product mixes. Competitive dynamics favor suppliers that combine proprietary strains, cold-chain logistics, and agronomic advisory, yet transport cost inflation and nutrient-content variability continue to pressure margins. Governments expand eco-scheme subsidies to de-risk adoption for cereal and oilseed growers, and digital platforms embed biological recommendations into crop plans. Collectively, these forces position the Europe biological organic fertilizers market for sustained double-digit expansion even as conventional nutrient prices fluctuate.

Key Report Takeaways

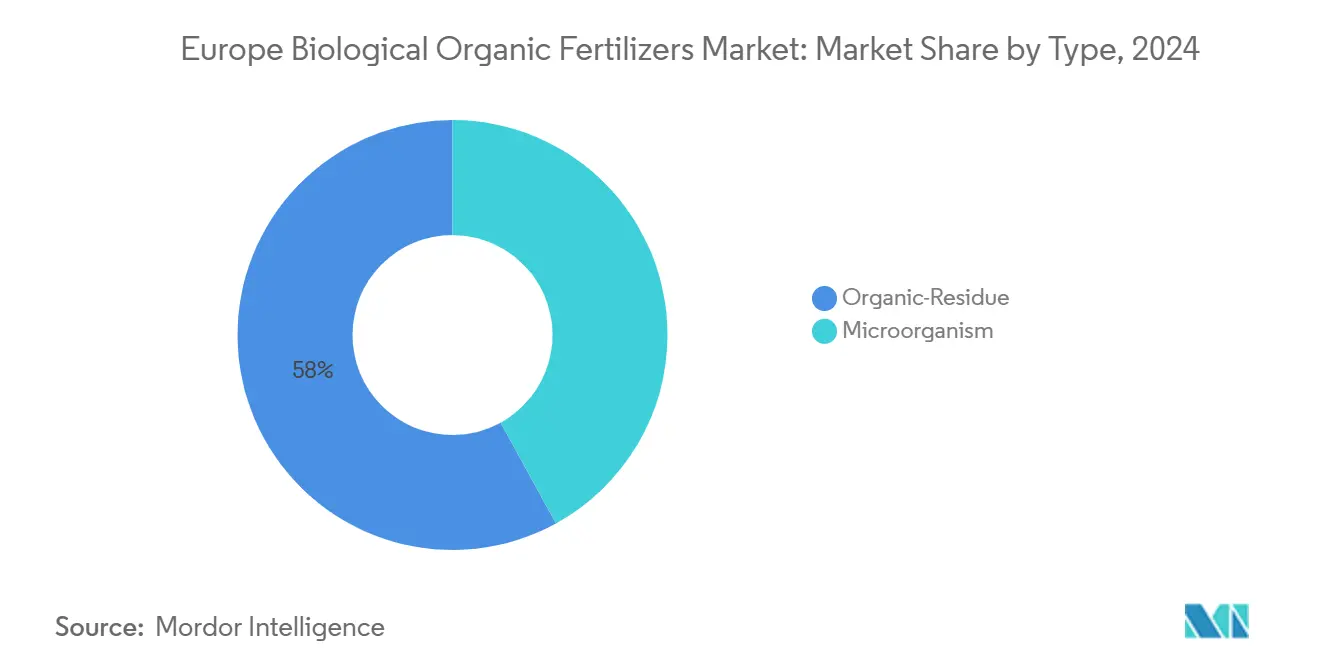

- By type, organic-residue-based products captured 58% of the Europe biological organic fertilizers market share in 2024, while microorganism-based inputs are advancing at a 12.8% CAGR to 2030.

- By form, dry formulations held 64% of the Europe biological organic fertilizers market size in 2024, whereas liquids are expanding at 14.9% CAGR through 2030.

- By crop, cereals and grains accounted for 42% of the Europe biological organic fertilizers market share in 2024, and commercial crops are growing fastest at 12.1% CAGR.

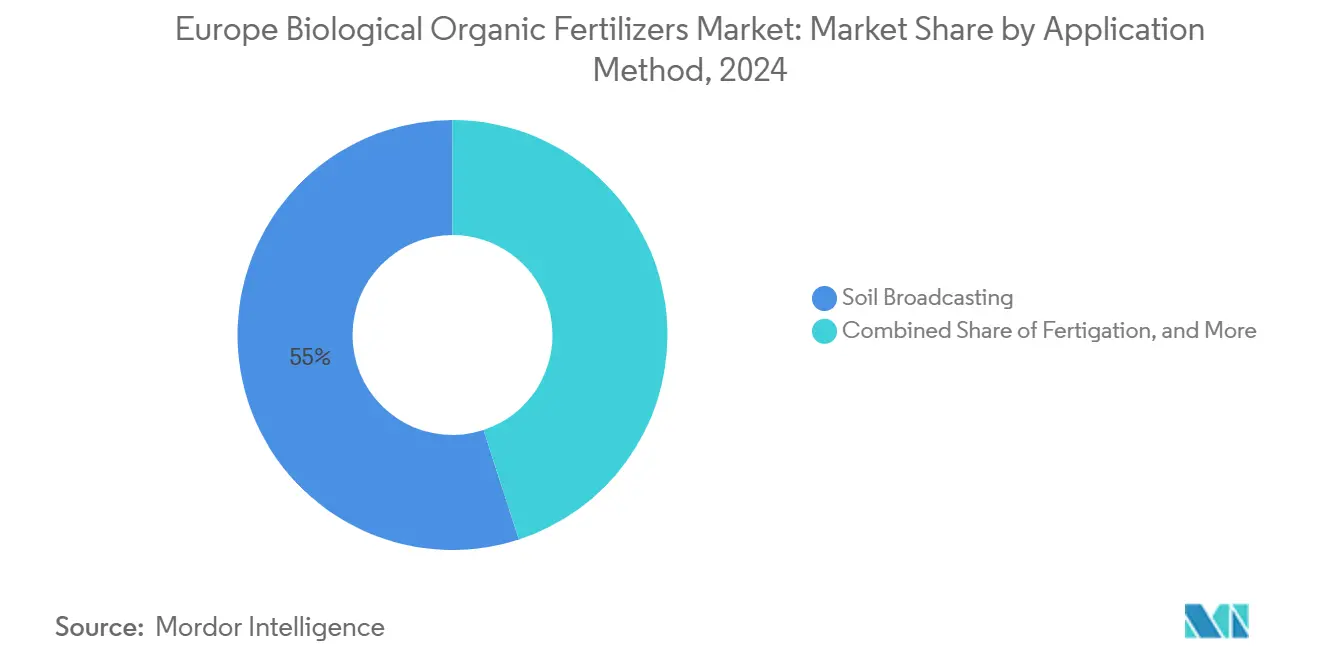

- By application method, soil broadcasting dominated with 55% revenue of Europe biological organic fertilizers market in 2024, fertigation is forecast to post a 16.2% CAGR to 2030.

- By geography, Germany led regional revenue with 21% of the Europe biological organic fertilizers market share in 2024, and Spain is projected to deliver the highest national CAGR at 13.5% through 2030.

Europe Biological Organic Fertilizers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European Union Farm-to-Fork Initiative and Organic Land Use Promotion | +2.30% | Pan-Europe, strongest in Germany, France, Italy, and Spain | Medium term (2-4 years) |

| Stricter European Union Nutrient-Loss Caps on Synthetic Fertilizers | +1.80% | Germany, Netherlands, and Denmark | Short term (≤ 2 years) |

| Rapid Expansion of Anaerobic-Digestate Supply Chains | +1.50% | Germany, France, and Italy | Medium term (2-4 years) |

| Commercial Scale-Up of Insect-Frass Fertilizer Plants | +1.90% | Spain, Italy, and Netherlands | Short term (≤ 2 years) |

| Common Agricultural Policy (CAP) Eco-scheme Carbon-Farming Payments | +1.40% | France, Spain, and Poland | Medium term (2-4 years) |

| Precision Fertigation Driving Liquid Biofertilizer Demand | +1.20% | Netherlands, France, and Belgium | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

European Union Farm-to-Fork Initiative and Organic Land Use Promotion

The Green Deal stipulates that one-quarter of European Union farmland must be organic by 2030, tripling 2024 certified acreage and structurally lifting biological fertilizer demand [1]Source: European Commission, “Common Agricultural Policy at a Glance,” ec.europa.eu. National budgets back the ramp-up, Germany earmarked EUR 30 million (USD 32 million) for on-farm composting subsidies, and France logged a 14% jump in certified hectares in 2024. Organic-residue inputs benefit most because they valorize farm waste, yet faster product approvals under Regulation 2019/848 also accelerate microbial-strain launches. Traceability frameworks tighten compliance, though uneven enforcement in Eastern Europe could delay uniform uptake.

Stricter European Union Nutrient-Loss Caps on Synthetic Fertilizers

Revised nitrate rules trim allowable nitrogen to 170 kg per hectare in vulnerable zones, forcing growers to replace urea with slow-release digestate and microbial phosphorus-solubilizers [2]Source: European Environment Agency, “Agriculture and Environment,” eea.europa.eu. Germany’s ordinance adds balance-sheet penalties, pushing liquid digestate sales up 22% in 2024. Netherlands phosphorus cutbacks are steering horticulture toward Bacillus and Trichoderma blends. Compliance risk is rising for livestock-dense areas, giving supply-chain leverage to biogas cooperatives and inoculant specialists.

Rapid Expansion of Anaerobic-Digestate Supply Chains

Europe’s 18 billion m³ biomethane output co-produced more than 120 million metric tons of digestate in 2024, turning a disposal issue into a fertilizer feedstock pool. Germany’s 9,500 plants lock in offtake deals, France committed EUR 200 million (USD 214 million) to upgrade pellet lines, and Italy tracks quality via blockchain for a 15% price premium. Digestate lowers the cost of goods for residue-based manufacturers, though logistics outside biogas clusters still weigh on margins.

Precision Fertigation Driving Liquid Biofertilizer Demand

Drip systems on 6.2 million hectares let growers inject microbials in real time, cutting labor by 30% and improving nutrient-use efficiency by up to 25%. Spain retrofitted 40% of Almería greenhouses in 2024, and Italy’s orchard fertigation reduced phosphorus use by 18%. Wageningen trials found strawberry Brix up 8% under liquid Bacillus delivery. Suppliers with cold-chain and stabilized blends gain a first-mover edge.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Transport Costs for Bulky Organic Inputs | -1.10% | Pan-Europe, acute in Iberia, Eastern Europe | Short term (≤ 2 years) |

| Nutrient Variability and Lack of European Union-wide Quality Standard | -0.90% | All member states | Medium term (2-4 years) |

| Limited Shelf-Life of Microbial Inoculants | -0.70% | Southern and Eastern Europe | Short term (≤ 2 years) |

| Peat Extraction Limits Constrain Certified Feedstocks | -0.60% | Ireland, Baltics, and Finland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Transport Costs for Bulky Organic Inputs

Low nutrient density means moving compost or digestate 200 km can cost EUR 25 (USD 27) per metric ton, dwarfing urea freight bills and deterring adoption in remote grain belts. Diesel was up 18% year-on-year in 2024, compounding freight inflation. Pelletization shrinks volume, but lines cost EUR 0.5-2 million (USD 0.54-2.1 million), affordable mainly to large co-ops, widening the gap between core and fringe regions.

Nutrient Variability and Lack of European Union-wide Quality Standard

Batch-to-batch nitrogen swings exceed 15% in 22% of tested composts, hampering precision-fertility planning. Regulation 2019/1009 controls contaminants but sets no nutrient tolerances, so formulations range from 3-2-2 to 6-4-3. Italy’s voluntary seal covers 40% of output yet lacks cross-border recognition. Until the European Committee for Standardization (CEN) norms arrive post-2027, risk-averse arable growers will under-apply or stick with synthetics.

Segment Analysis

By Type: Microorganism Products Narrow the Gap

Organic-residue fertilizers accounted for 58% of the market share in 2024 revenue, driven by established compost, manure, and digestate channels that help maintain low costs per hectare in cereal and grain rotations. Microorganism products are set to outpace at a 12.8% CAGR as retailers penalize synthetic residues and Regulation 2019/1009 halves approval times. Field data from Denmark showed cold-tolerant Bacillus strains lifting wheat yields 8%.

Residue inputs encounter challenges related to haulage and nutrient uniformity, while microbial products face issues with shelf life and farmer trust. Bundling initiatives, such as the 2024 agreement between Symborg and Fertiberia, aim to integrate inoculants into mainstream use by leveraging conventional distribution channels. Insect frass blurs the line, bringing microbial richness and organic matter in one Stock Keeping Unit (SKU) and carving niches in greenhouse vegetables and ornamentals, indicating that the Europe biological organic fertilizers market will evolve toward hybrid solutions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Liquid Surge Driven by Fertigation

Dry products kept a 64% share in 2024, reflecting decades of broadcast machinery across 180 million hectares of arable land. Liquids, however, are rising fastest with a CAGR of 14.9%. Fertigation retrofits in Spain and Italy reduced nitrogen leaching by 23% in University of Almería trials. The Europe biological organic fertilizers market size for liquids is set to reach a significant market value by 2030. Koppert recorded a 35% sales jump in 2024 on liquid Trichoderma for greenhouse tomatoes.

Dry formats remain crucial where storage and spreading scale matter. Pelletized manure now covers 18% of the dry segment after recent capacity additions in Germany and France. Growers increasingly pair a dry base with liquid top-dressings, particularly in high-value horticulture. Suppliers that master both lines will capture differentiated demand curves across the Europe biological organic fertilizers market.

By Crop Type: Commercial Crops Accelerate

Cereals and grains absorbed 42% of the 2024 volume, underwritten by France and Germany’s wheat and barley belts that draw premiums of EUR 40-60 (USD 43-64) per metric ton for organic grain [3]Source: Eurostat, “Organic Farming Statistics,” ec.europa.eu. Commercial crops, including cotton, flax, and hemp, are slated for a 12.1% CAGR as textile buyers audit nitrogen footprints. Andalusia’s cotton already applies organic fertilizers on 22% of its area. Fruits and vegetables command 33% share, as retailer traceability audits drive intensive spend.

Oilseeds and pulses stand at 9% as rapeseed and sunflower growers test phosphorus-solubilizers. Turf and ornamentals account for the remaining share. Dutch municipalities mandated peat-free substrates on 70% of public contracts in 2024, boosting compost demand. Common Agricultural Policy (CAP) eco-scheme payments narrow cost gaps in cereals, signaling incremental conversion yet leaving high-value produce as the growth spearhead of the Europe biological organic fertilizers market.

By Application Method: Fertigation Wins Momentum

Soil broadcasting retains 55% revenue, leveraging tractor-mounted spreaders that cover up to 80 hectares daily. Fertigation posted the highest growth and is projected to grow with a 16.2% CAGR by 2030, supported by Spain’s 1.2 million irrigated hectares and Italy’s micro-sprinkler orchards. IRTA trials showed lettuce nitrogen-use efficiency up 19% with liquid Azospirillum via drip lines. Foliar spraying captures 5-8% of spend, vital for vineyards under drought stress but limited by weather windows.

Greenhouse operations in the Netherlands recycle fertigation solutions, integrating biofertilizers to stabilize microbial consortia. Broadcast remains economical for extensive grains, hybrids that mix broadcast residue baselines with in-season fertigation reflect best practice across the Europe biological organic fertilizers market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany led 2024 revenue at 21% of the Europe biological organic fertilizers market share in 2024, due to 9,500 biogas plants supplying digestate that covered 40% of national demand. Bavaria and North Rhine-Westphalia remain hotspots. Common Agricultural Policy (CAP) eco-scheme subsidies and an 11.2% organic-acreage baseline underpin expansion. France follows, deploying EUR 200 million (USD 214 million) of biogas upgrades and logging 14% organic-acreage growth, especially in viticulture. Italy’s 2.2 million certified hectares generate consistent compost and insect-frass pull in Emilia-Romagna fruit and Sicily vegetables.

Spain is projected to deliver the highest national CAGR at 13.5% through 2030. Spain’s Almería greenhouse belt retrofitted 40% of fertigation lines for liquid biofertilizers, driving a 19% sales lift in 2024. The United Kingdom mirrors the European Union Green Deal goals through its Environmental Land Management Scheme. East Anglia cereals draw on food-waste digestate imports, sustaining 8% organic-acreage gains. Russia remains nascent, limited by certification gaps and a mineral-fertilizer bias, though pilot farms in Krasnodar and Voronezh are experimenting with compost.

Poland, the Netherlands, Belgium, the Baltics, and others collectively hold a significant share. Dutch greenhouses and Belgian insect farms fuel technology leadership, while Poland’s Common Agricultural Policy (CAP) payments cover 70% of conversion costs. Eastern Europe’s uptake hinges on cold-chain expansion and subsidy disbursement speed, but overall, Southern Europe’s fertigation retrofits and Northern Europe’s digestate abundance will keep the Europe biological organic fertilizers market on a robust growth trajectory.

Competitive Landscape

The top five companies, including Hello Nature International Srl, Novonesis Group, Fertikal N.V., RovensaNext, and Koppert Biological Systems BV, held a significant collective share in 2024, signaling moderate fragmentation. Vertical integration is visible as biogas operators like Verbio monetize digestate via pellet plants, and horizontal moves include Rovensa’s 2024 compost acquisition in Spain. Emerging disruptors Ynsect and Protix scale insect-frass capacity, challenging compost economics, while BASF’s Xarvio platform embeds biofertilizer guidance into digital crop plans.

Technology serves as a key differentiator in the market, with advancements such as encapsulation and lyophilization enhancing inoculant shelf-life. This is exemplified by Novonesis Group’s stabilized Bacillus product launch targeting Southern markets. Bundling strategies, like the collaboration between Symborg, Inc. and Fertiberia, S.A. (Sociedad Anónima), integrate biological and conventional nutrients into a single Stock Keeping Unit (SKU), simplifying processes for farmers. Patent filings increased to 47 in 2024, driven by entities such as Novonesis Group, BASF SE, and Wageningen University, with a focus on strain optimization and formulation stability.

Regulation 2019/1009 standardizes entry requirements but does not address nutrient-content claims, allowing brands to differentiate through quality assurance. Mergers and acquisitions are projected to gain momentum as agrochemical companies diversify their portfolios, while regional cooperatives capitalize on their proximity to protect cereal segments within the Europe biological organic fertilizers market.

Europe Biological Organic Fertilizers Industry Leaders

-

Fertikal N.V.

-

RovensaNext

-

Koppert Biological Systems BV

-

Hello Nature International Srl

-

Novonesis Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: Ynsect has launched a 15,000 metric tons insect frass production line in Amiens to support greenhouse vegetable cultivation. This initiative is projected to contribute to the growth of the biological organic fertilizers market in Europe by providing a sustainable and nutrient-rich fertilizer option.

- July 2024: Rovensa Next has announced the launch of Wiibio, a soil-regenerating biofertilizer with biostimulant properties. Wiibio is designed to enhance plant development by stimulating the natural plant growth cycle while contributing to soil health and vitality, providing support to growers. This innovation is projected to positively impact the European biological organic fertilizers market by addressing the growing demand for sustainable and effective soil health solutions.

- June 2024: BASF’s Xarvio integrated biofertilizer modules have been adopted by 18% of large farms in Germany and France, contributing to the growth of the Europe biological organic fertilizers market by promoting sustainable farming practices and enhancing crop productivity.

Europe Biological Organic Fertilizers Market Report Scope

Biological organic fertilizers are derived from many animal and plant-based residues and mineral ores and developed from beneficial microorganisms, like bacteria and fungi. These are low-cost, renewable sources of plant nutrients, which supplement chemical fertilizers. The European biological organic fertilizer market is segmented by Type (Microorganisms and Organic Residues), by Form (Dry and Liquid), by Crop Type (Cereals & Grains, Fruits & Vegetables, Oilseeds & Pulses, and More), by Application Method ( Soil Broadcasting, Fertigation, and Foliar Spray), and by Geography (Germany, United Kingdom, and More).

By Type

| Microorganism |

| Organic-Residues |

By Form

| Dry |

| Liquid |

By Crop Type

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Commercial Crops |

| Turf and Ornamentals |

By Application Method

| Soil Broadcasting |

| Fertigation |

| Foliar Spray |

By Geography

| Germany |

| France |

| Italy |

| Spain |

| United Kingdom |

| Russia |

| Rest of Europe |

| By Type | Microorganism |

| Organic-Residues | |

| By Form | Dry |

| Liquid | |

| By Crop Type | Cereals and Grains |

| Fruits and Vegetables | |

| Oilseeds and Pulses | |

| Commercial Crops | |

| Turf and Ornamentals | |

| By Application Method | Soil Broadcasting |

| Fertigation | |

| Foliar Spray | |

| By Geography | Germany |

| France | |

| Italy | |

| Spain | |

| United Kingdom | |

| Russia | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Europe biological organic fertilizers market in 2025?

It stands at USD 0.52 billion and is forecast to reach USD 0.84 billion by 2030.

What CAGR is projected for biological organic fertilizers in Europe through 2030?

The market is projected to expand at a 10.10% CAGR over 2025-2030.

Which product type is growing fastest in Europe?

Microorganism-based biofertilizers are advancing at a 12.8% CAGR, narrowing the gap with residue-based inputs.

Why are liquid formulations gaining traction?

The spread of drip-irrigation fertigation cuts labor and nutrient losses, propelling liquids at a 14.9% CAGR.

Which country leads in regional revenue?

Germany holds the top position with 21% market share, driven by digestate from its biogas network.

Page last updated on: