| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Volume (2025) | 17.00 Billion liters |

| Market Volume (2030) | 19.94 Billion liters |

| CAGR | 3.24 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Biodiesel Market Analysis

The Europe Biodiesel Market size is estimated at 17.00 billion liters in 2025, and is expected to reach 19.94 billion liters by 2030, at a CAGR of 3.24% during the forecast period (2025-2030).

The European biodiesel industry is undergoing a significant transformation driven by sustainability initiatives and technological advancements. The sector has witnessed a notable shift towards waste-based feedstocks, with used cooking oil (UCO) emerging as a predominant raw material. This transition is exemplified by the United Kingdom's biodiesel sector, where used cooking oil comprised approximately 75% of biodiesel production in recent years. Major industry players are actively expanding their waste-based feedstock capabilities, as demonstrated by Argent Energy's May 2022 announcement to increase its biodiesel production capacity in the Port of Amsterdam to 540,000 tons per year, focusing primarily on waste-based feedstocks.

The infrastructure development across Europe continues to evolve with significant investments in advanced biofuel facilities. In March 2022, Repsol initiated the construction of an advanced biofuels plant at its Cartagena Refinery in Spain, with an investment of approximately EUR 200 million to supply about 250,000 tons of advanced biofuels annually. Similarly, in February 2022, BDI-BioEnergy International GmbH secured a contract with Renewable Energy Group to upgrade two biodiesel plants in Germany by installing state-of-the-art feedstock pretreatment technology, highlighting the industry's commitment to technological advancement and operational efficiency.

The European biodiesel supply chain is experiencing a fundamental restructuring as the industry moves away from traditional feedstocks. In May 2022, the German Ministry of Agriculture announced plans to phase out biofuels produced from food and feed crops by 2030, signaling a significant shift in feedstock sourcing strategies. This transition has led to increased focus on alternative fuel feedstocks such as waste oils, animal fats, and second-generation biofuel like algae, creating new opportunities for sustainable fuel production while addressing food security concerns.

The market dynamics are increasingly influenced by stringent regulatory requirements and sustainability targets. The implementation of the Renewable Energy Directive II (RED II) has set ambitious targets for renewable energy in transport, with a 14% target by 2030. The industry has responded with innovative solutions, as evidenced by Bio-Bean's initiative in the UK to produce biodiesel from coffee waste, demonstrating the sector's ability to adapt to regulatory changes while exploring novel feedstock options. The regulatory framework has also prompted major players to invest in research and development of renewable diesel and advanced biofuels, contributing to the market's technological evolution and sustainability profile.

Europe Biodiesel Market Trends

Supportive Government Policies and Renewable Energy Targets

The European biodiesel market is primarily driven by strong governmental support through policies and renewable energy targets aimed at reducing greenhouse gas emissions in the transportation sector. The European Union's Renewable Energy Directive II (RED II) has set an ambitious overall renewable energy target of 32% by 2030, with a specific 14% target for the transport sector. This directive has led to the implementation of various country-specific blending mandates, with nations like France setting a target of 8% biodiesel blending by 2028, Belgium following a 9.5% blending mandate as of January 2021, and Ireland committing to incrementally raising blend proportions to at least B20 in diesel by 2030.

The policy framework has been further strengthened by individual country initiatives to promote sustainable biodiesel production. For instance, Finland has approved legislation mandating a biodiesel blending of 20% from 2020 onwards, while the Netherlands has implemented RED II directives into Dutch law in June 2021, setting a 32% target for renewable energy by 2030. These policies are complemented by penalties for non-compliance, such as in Spain, where producers face a penalty of EUR 736 per missed certificate if they fail to meet blending mandates, ensuring strict adherence to renewable fuel requirements and driving market growth.

Understand The Key Trends Shaping This Market

Download PDF

High Dependence on Oil Imports and Energy Security Concerns

Europe's significant reliance on oil imports has emerged as a crucial driver for the biodiesel market, as countries seek to reduce their dependence on foreign oil supplies. According to Eurostat data, Russia alone accounted for a substantial portion of the EU's oil and petroleum product imports, followed by Norway, Kazakhstan, and the United States, highlighting the region's vulnerability to supply chain disruptions and geopolitical tensions. This dependence has led to increased focus on developing domestic biodiesel production capabilities as a strategy to enhance energy security and reduce exposure to international oil market volatility.

The ongoing geopolitical tensions, particularly the Russia-Ukraine conflict, have further emphasized the urgency of developing alternative fuel sources. This situation has accelerated investments in biodiesel infrastructure and production facilities across Europe. For example, major investments have been made in biodiesel facilities, such as Repsol's EUR 200 million investment in an advanced biofuels plant at Cartagena Refinery in Spain, which will supply about 250,000 tons of advanced biofuels annually. Similarly, Argent Energy's expansion plans to increase its biodiesel production capacity to 540,000 tons per year in the Port of Amsterdam demonstrate the industry's response to energy security concerns.

Growing Focus on Sustainable Feedstock Solutions

The biodiesel market is increasingly driven by the shift towards sustainable feedstock solutions, particularly in response to environmental concerns and regulatory requirements. The European Union's decision to phase out palm oil-based biodiesel by 2030 has catalyzed innovation in feedstock sourcing, with a notable transition towards waste-based materials such as used cooking oil (UCO) and animal fats. This shift is evidenced by the implementation of double counting mechanisms under RED II for UCO and animal fat-based biodiesel, providing additional incentives for producers to adopt these sustainable alternatives.

The industry's commitment to sustainable feedstock is demonstrated through significant investments in processing capabilities and infrastructure. For instance, in February 2022, BDI-BioEnergy International GmbH announced a contract with Renewable Energy Group to upgrade two biodiesel plants in Germany by installing feedstock pre-treatment technology to process fats and oils. Additionally, innovative approaches are emerging, such as Bio-Bean's initiative in the UK to produce biodiesel using coffee waste as feedstock, collecting from businesses across the country and demonstrating the potential for novel sustainable feedstock solutions. These developments are supported by the increasing adoption of waste-based feedstocks, with UCO comprising about 75% of biodiesel production in some regions.

Segment Analysis: Feedstock

Rapeseed Oil Segment in Europe Biodiesel Market

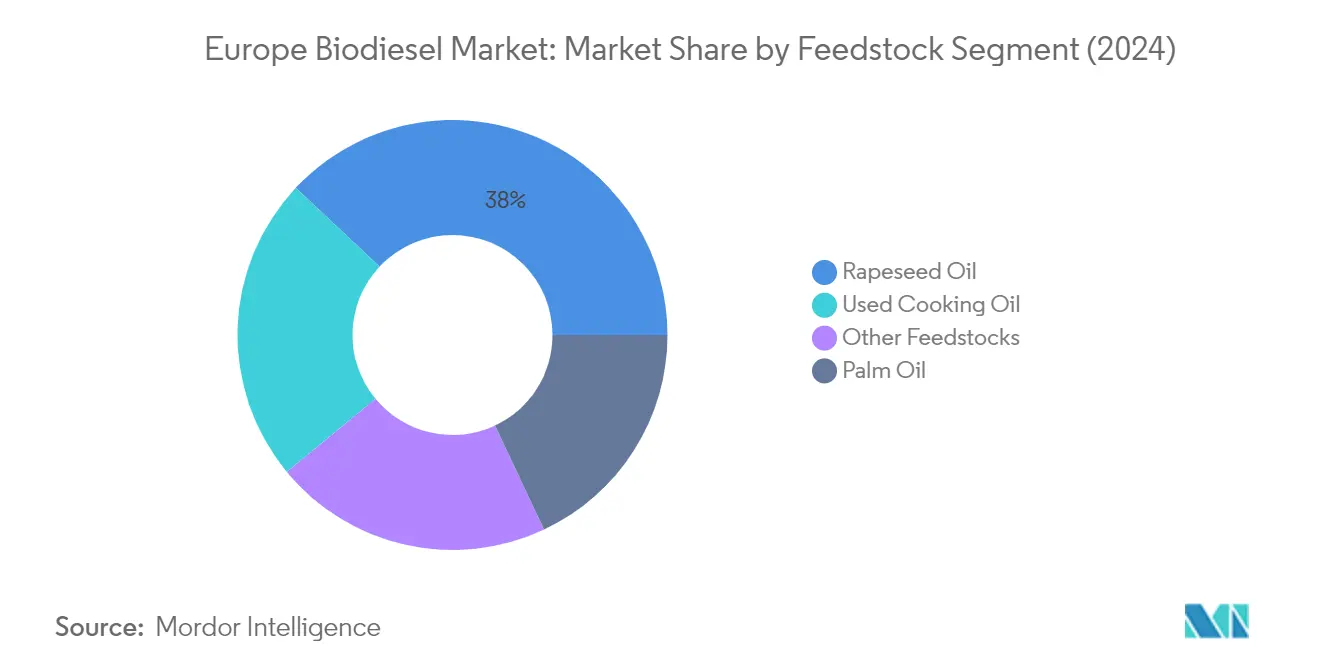

Rapeseed oil continues to maintain its dominant position in the European biodiesel feedstock market, accounting for approximately 38% of the total feedstock mix in 2024. This feedstock is particularly prevalent in Western Europe, where mild winters dominate, with France, Germany, and the United Kingdom accounting for about 90% of the rapeseed production in the European Union. The high oil content of rapeseed (approximately 40%) makes it more profitable compared to alternatives like soybeans, which contain only about 18% oil. Rapeseed oil's popularity as a biodiesel feedstock is further supported by its superior technical properties and well-established supply chains across Europe. The segment's strength is reinforced by extensive local cultivation infrastructure and the ability to meet stringent European quality standards for biodiesel production.

Used Cooking Oil Segment in Europe Biodiesel Market

Waste cooking oil (UCO) has emerged as the fastest-growing feedstock segment in the European biodiesel market for the period 2024-2029. This growth is primarily driven by the implementation of double counting under RED II, which provides enhanced incentives for waste-based feedstocks. UCO's rising prominence is also attributed to its favorable fatty acid composition, which is better suited for biodiesel production compared to rapeseed oil. The segment's expansion is further supported by increasing collection networks across Europe and growing imports from major suppliers like Malaysia, China, and the United States. The European Union's focus on reducing greenhouse gas emissions and promoting circular economy principles has created a strong regulatory framework favoring waste cooking oil-based biodiesel production.

Remaining Segments in Feedstock Market

The other significant feedstock segments in the European biodiesel market include palm oil and various alternative feedstocks such as animal fats, soybean oil, and sunflower oil. Palm oil's role is diminishing due to the European Union's decision to phase it out by 2030 under RED II regulations. Animal fats have gained traction as an alternative feedstock, particularly in countries like Italy, the Netherlands, and France, benefiting from double-counting incentives similar to waste cooking oil. Soybean oil faces limitations in northern Europe due to cold weather performance issues, while sunflower oil maintains a smaller but stable presence in the feedstock mix, primarily in countries like Greece, France, and Bulgaria.

Segment Analysis: Biodiesel Blends

B5 Segment in European Biodiesel Blends Market

The B5 biodiesel blend continues to dominate the European biodiesel market in 2024, accounting for approximately 50% of the total market share. This widespread adoption is primarily attributed to its universal approval by diesel automobile and truck manufacturers, eliminating operational and warranty concerns. The B5 blend, consisting of less than 5% pure biodiesel and more than 95% petroleum diesel fuel, is particularly favored due to its compatibility with existing engine systems and infrastructure. In Europe, the blend is covered under EN 590 standards and is extensively used in mobile machinery and transportation sectors. The segment's dominance is further supported by its proven track record in reducing greenhouse gas emissions while maintaining optimal engine performance without requiring modifications to existing vehicles.

B20 Segment in European Biodiesel Blends Market

The B20 biodiesel blend is emerging as the fastest-growing segment in the European biodiesel market for the period 2024-2029. This robust growth is driven by several factors, including its optimal balance of cost, emissions reduction capabilities, and cold-weather performance. The segment's expansion is significantly bolstered by progressive government policies, such as Ireland's commitment to incrementally raise blend proportions to B20 fuel by 2030. The growth is further supported by major industry developments, including Progress Rail's approval for B20 fuel use across its engine series, demonstrating increasing industrial acceptance. B20's ability to provide substantial environmental benefits while avoiding many cold-weather performance and material compatibility concerns associated with higher blends makes it particularly attractive for widespread adoption across various applications.

Remaining Segments in Biodiesel Blends Market

The B100 fuel segment, while representing a smaller portion of the European biodiesel market, plays a crucial role in specific applications where maximum environmental benefits are prioritized. This pure biodiesel blend offers the highest potential for emissions reduction but faces challenges including higher costs, cold weather sensitivity, and the need for specialized engine modifications. The segment has found particular success in Sweden's market, where infrastructure and policies support its use. However, its adoption remains limited in other European regions due to practical considerations such as storage requirements, engine compatibility issues, and the need for special anti-freezing precautions, particularly in Nordic countries.

Europe Biodiesel Market Geography Segment Analysis

Biodiesel Market in Germany

Germany stands as the powerhouse of Europe's biodiesel industry, commanding approximately 45% of the market share in 2024. The country's dominant position is supported by its robust infrastructure and comprehensive policy framework promoting renewable diesel in transportation. Germany's biodiesel sector is characterized by its advanced biodiesel production facilities and significant investments in research and development. The country's commitment to reducing greenhouse gas emissions has led to the implementation of stringent blending mandates and sustainability criteria for biodiesel production. The industry benefits from a well-established network of biodiesel feedstock suppliers, particularly in the used cooking oil and waste fats sectors, following the country's strategic shift away from crop-based feedstocks. German biodiesel producers have demonstrated remarkable adaptability in responding to evolving regulatory requirements and market demands, particularly in developing innovative technologies for processing diverse feedstock materials. The sector continues to attract substantial investments in capacity expansion and technological upgrades, reinforcing its position as Europe's biodiesel manufacturing hub.

Biodiesel Market in France

France maintains its position as a crucial player in the European biodiesel landscape, with its market characterized by sophisticated biodiesel production capabilities and strong governmental support. The French biodiesel industry has demonstrated remarkable resilience through its diversified biodiesel feedstock approach, particularly focusing on waste-based materials and agricultural residues. The country's strategic location and well-developed logistics infrastructure facilitate efficient distribution across European markets. French producers have been particularly successful in implementing double-counting mechanisms for waste-based biodiesel, creating additional market incentives. The industry benefits from strong collaboration between agricultural cooperatives, research institutions, and industrial players, fostering innovation in production processes. The country's commitment to sustainable transportation has resulted in the development of advanced biodiesel production facilities, particularly in major industrial zones. French biodiesel producers have also been at the forefront of developing new technologies for processing alternative feedstocks, strengthening the industry's sustainability credentials.

Biodiesel Market in Spain

Spain has established itself as a significant force in the European biodiesel sector, leveraging its strategic Mediterranean location and robust agricultural base. The Spanish biodiesel industry has undergone substantial modernization, with producers investing in advanced processing capabilities and expanding their feedstock portfolio. The country's biodiesel sector benefits from strong integration with its agricultural industry, particularly in regions with significant oilseed cultivation. Spanish producers have demonstrated considerable expertise in processing various feedstock types, including used cooking oil and agricultural waste. The industry has developed strong export capabilities, serving both domestic and international markets efficiently. Spain's biodiesel sector is characterized by its focus on sustainability and circular economy principles, with many facilities incorporating advanced waste management and energy efficiency systems. The country's warm climate provides favorable conditions for biodiesel storage and handling, contributing to operational efficiency throughout the year.

Biodiesel Market in Other Countries

The broader European biodiesel market encompasses several other significant players, each contributing uniquely to the region's biofuel landscape. Countries like the Netherlands, Italy, and Poland have developed specialized niches within the biodiesel sector, often focusing on specific feedstock types or production technologies. The Nordic countries, including Sweden and Finland, have made significant strides in developing cold-weather-suitable biodiesel formulations. Eastern European nations have emerged as important players in the feedstock supply chain, particularly in rapeseed cultivation and waste oil collection. Countries like Belgium and Austria have focused on developing high-quality biodiesel products for specific market segments. The diversity of these markets contributes to the overall resilience of the European biodiesel sector, with each country leveraging its unique advantages and resources. This varied landscape has fostered innovation and competition, driving improvements in production efficiency and product quality across the continent.

Get Analysis on Important Geographic Markets

Download PDF

Europe Biodiesel Industry Overview

Top Companies in Europe Biodiesel Market

The European biodiesel market is characterized by established players like Shell PLC, BP PLC, Bunge Limited, Air Liquide SA, and Greenergy International Limited driving innovation and market development. Companies are increasingly focusing on developing advanced biodiesel technologies and expanding their production capabilities through strategic investments in new facilities. The industry has witnessed a strong trend toward vertical integration, with companies establishing control over feedstock supply chains while simultaneously developing innovative processing technologies. Market leaders are actively pursuing sustainability initiatives, particularly in waste-based feedstock utilization and the development of next-generation biofuels. These companies are also strengthening their positions through strategic partnerships and collaborations across the value chain, from feedstock suppliers to end-users in various sectors, including transportation, marine, and industrial applications.

Dynamic Market with Strong Growth Potential

The European biodiesel market exhibits a moderately consolidated structure, dominated by both global energy conglomerates and specialized biofuel producers. Major oil and gas companies leverage their extensive distribution networks and technical expertise to maintain significant market shares, while specialized players differentiate themselves through innovative feedstock sourcing and processing technologies. The market has witnessed significant merger and acquisition activity, particularly focused on expanding geographical presence and securing feedstock supply chains, with companies like BP acquiring stakes in specialized biofuel producers and technology providers.

The competitive landscape is further shaped by regional players who have established a strong local presence through strategic partnerships with agricultural suppliers and industrial customers. Market participants are increasingly pursuing vertical integration strategies, either through direct acquisitions or strategic alliances, to secure feedstock supplies and optimize production costs. The industry has seen a notable trend of cross-border collaborations, particularly in technology sharing and joint development of advanced biodiesel production facilities, indicating a shift toward more integrated and efficient operations across the European market.

Innovation and Sustainability Drive Future Success

Success in the European biodiesel market increasingly depends on companies' ability to innovate in feedstock utilization and processing technologies while maintaining cost competitiveness. Incumbent players are focusing on expanding their renewable fuel portfolios through investments in advanced processing technologies and sustainable feedstock sources, particularly in waste-based and second-generation biodiesel production. Market leaders are also strengthening their positions by developing integrated supply chains and establishing strategic partnerships with key stakeholders across the value chain, from agricultural suppliers to end-users in various sectors.

For new entrants and smaller players, success lies in developing specialized capabilities in niche segments, particularly in advanced biofuel technologies and sustainable feedstock sourcing. The market presents significant opportunities for companies that can effectively address the growing demand for sustainable fuel and renewable transportation fuel while navigating regulatory requirements and managing feedstock supply challenges. Companies must also consider the increasing competition from alternative renewable fuels and electric mobility solutions, making it essential to develop robust product differentiation strategies and maintain operational flexibility to adapt to changing market conditions and regulatory frameworks.

Europe Biodiesel Market Leaders

-

Shell PLC

-

BP PLC

-

Bunge Limited

-

Air Liquide SA

-

Harvest Energy

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Europe Biodiesel Market News

- January 2023, Germany's Ministry of Environment announced plans to send proposals to the cabinet soon for the country to withdraw from the usage of crop-based biofuels to accomplish decreases in greenhouse gases.

- March 2022: Rossi Biofuel Zrt, a subsidiary of the ENVIEN Group, inaugurated a new biodiesel plant in Hungary. This plant was built by BDI-BioEnergy International GmbH. The facility is a multi-feedstock plant in Komárom, Hungary. The new plant has 60,000 tons per annum capacity, and thus, the total biodiesel production capacity of the company increased from 150,000 to 210,000 tons per annum.

Europe Biodiesel Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, until 2028

- 4.3 Government Policies and Regulations

- 4.4 Recent Trends and Developments

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Supportive Policies and Regulations

- 4.5.1.2 Energy Security

- 4.5.2 Restraints

- 4.5.2.1 Feedstock Availability and Price Volatility

- 4.6 Supply-Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Feedstock

- 5.1.1 Rapeseed Oil

- 5.1.2 Palm Oil

- 5.1.3 Used Cooking Oil

- 5.1.4 Other Feedstocks

-

5.2 Biodiesel Blends

- 5.2.1 B5

- 5.2.2 B20

- 5.2.3 B100

-

5.3 Geography

- 5.3.1 Germany

- 5.3.2 Spain

- 5.3.3 United Kingdom

- 5.3.4 France

- 5.3.5 Rest of Europe

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Shell PLC

- 6.3.2 BP PLC

- 6.3.3 Bunge Limited

- 6.3.4 Air Liquide SA

- 6.3.5 Harvest Energy

- 6.3.6 Abengoa Bioenergia SA

- 6.3.7 Envien Group

- 6.3.8 Greenergy International Ltd.

- 6.3.9 GBF German Biofuels GMBH

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Advanced Feedstocks

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Europe Biodiesel Industry Segmentation

Biodiesel is a renewable fuel derived from biomass sources, such as vegetable oils, animal fats, or recycled cooking oils. It is produced through transesterification, which involves chemically reacting the biomass feedstock with an alcohol (usually methanol or ethanol) in the presence of a catalyst, such as sodium hydroxide or potassium hydroxide.

Europe's biodiesel market is segmented by feedstock, biodiesel blends, and geography. By feedstock, the market is segmented into Coarse Grain, Sugar Crop, Vegetable Oil, and Others; by biodiesel blends, the market is segmented into B5, B20, and B100. The report also covers the market size and forecasts for the European biodiesel market across major regions. The report offers the market size and forecasts for the European biodiesel market in volume for all the above segments.

| Feedstock | Rapeseed Oil |

| Palm Oil | |

| Used Cooking Oil | |

| Other Feedstocks | |

| Biodiesel Blends | B5 |

| B20 | |

| B100 | |

| Geography | Germany |

| Spain | |

| United Kingdom | |

| France | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Europe Biodiesel Market Research FAQs

How big is the Europe Biodiesel Market?

The Europe Biodiesel Market size is expected to reach 17.00 billion liters in 2025 and grow at a CAGR of 3.24% to reach 19.94 billion liters by 2030.

What is the current Europe Biodiesel Market size?

In 2025, the Europe Biodiesel Market size is expected to reach 17.00 billion liters.

Who are the key players in Europe Biodiesel Market?

Shell PLC, BP PLC, Bunge Limited, Air Liquide SA and Harvest Energy are the major companies operating in the Europe Biodiesel Market.

What years does this Europe Biodiesel Market cover, and what was the market size in 2024?

In 2024, the Europe Biodiesel Market size was estimated at 16.45 billion liters. The report covers the Europe Biodiesel Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Biodiesel Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Europe Biodiesel Market Research

Mordor Intelligence provides a comprehensive analysis of the European biodiesel industry. We leverage our extensive expertise in alternative fuel research and consulting. Our latest report examines the complete value chain, from biodiesel feedstock to production. It covers fatty acid methyl ester (FAME) technologies, renewable diesel developments, and green diesel innovations. The analysis includes various feedstock sources, such as vegetable oil fuel and waste cooking oil. It also provides detailed insights into biodiesel production methodologies and market dynamics.

Stakeholders across the industry can access our downloadable report PDF, which offers valuable insights into sustainable fuel trends and advanced biofuel technologies. The report examines various biodiesel blend options, including B100 fuel and B20 fuel specifications. It also analyzes the potential of second generation biofuel developments. Our research supports decision-making for manufacturers, suppliers, and investors in the renewable transportation fuel sector. We provide detailed analysis of clean diesel alternatives and their role as a diesel substitute. The comprehensive coverage ensures stakeholders understand the evolving landscape of biofuel technologies and market opportunities.