Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

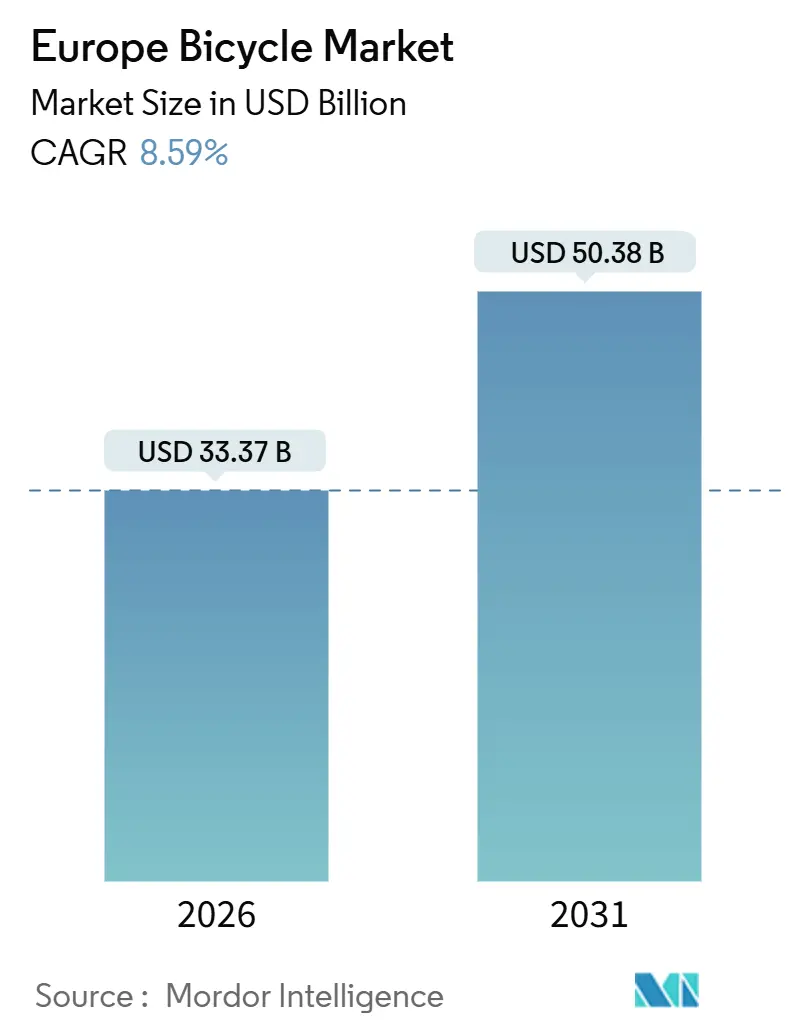

| Market Size (2026) | USD 33.37 Billion |

| Market Size (2031) | USD 50.38 Billion |

| Growth Rate (2026 - 2031) | 8.59% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Bicycle Market Analysis by Mordor Intelligence

The Europe bicycle market size stands at USD 33.37 billion in 2026 and is projected to reach USD 50.38 billion by 2031, registering an 8.59% CAGR over the forecast period. E-bicycles dominate category value, while folding designs appeal to commuters seeking intermodal flexibility. Online platforms improve accessibility, though high-end bikes continue to rely on showroom sales. Demand remains strong, driven by public-sector capital investments, corporate wellness programs, and stricter climate mandates, even as subsidies fluctuate. Declining battery pack costs enable mid-drive motors with higher torque and reduced weight. Additionally, workplace charging requirements under the Alternative Fuels Infrastructure Regulation are eliminating barriers to daily e-bike commuting. However, manufacturers face challenges from counterfeit products and competition from e-scooters, necessitating a focus on strengthening brand equity and highlighting utilitarian performance.

Key Report Takeaways

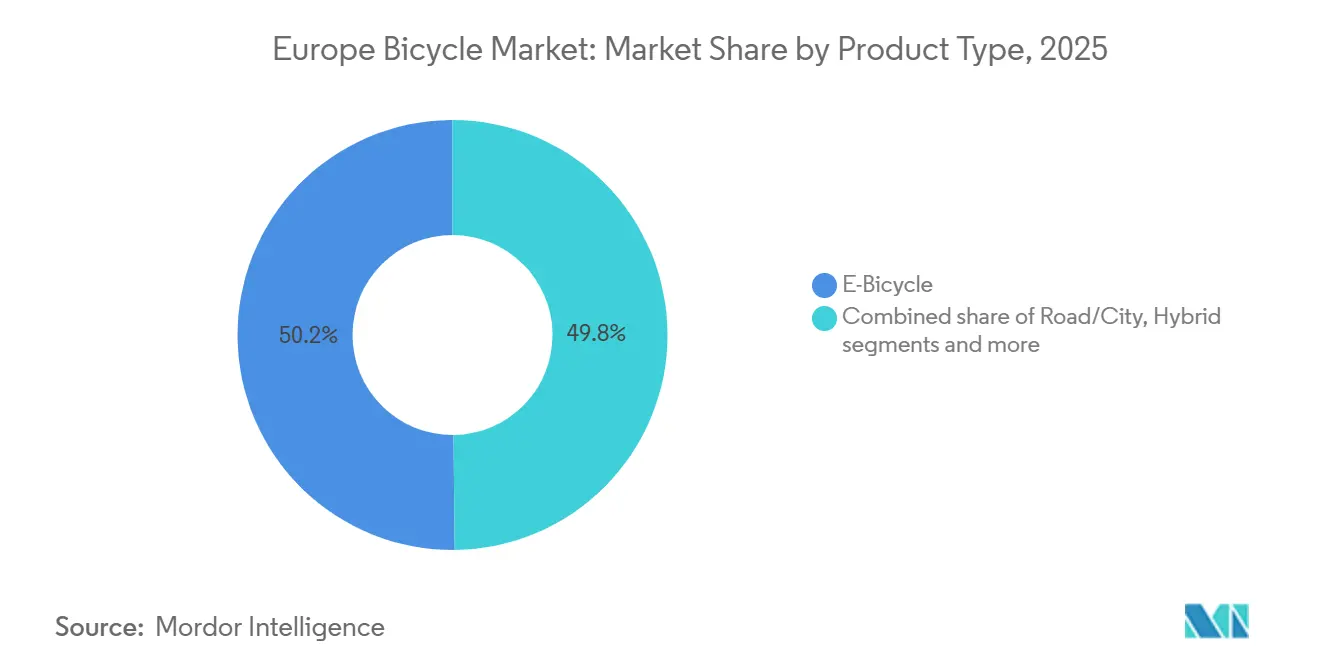

- By product type, e-bicycles led with 50.17% revenue share in 2025, and the segment is forecast to expand at a 9.56% CAGR through 2031.

- By design, regular frames accounted for 83.35% of 2025 sales, while folding bicycles recorded the highest projected CAGR at 10.21% over 2026-2031.

- By end user, men contributed 46.36% of the 2025 demand, whereas the children’s segment is advancing at a 9.85% CAGR to 2031.

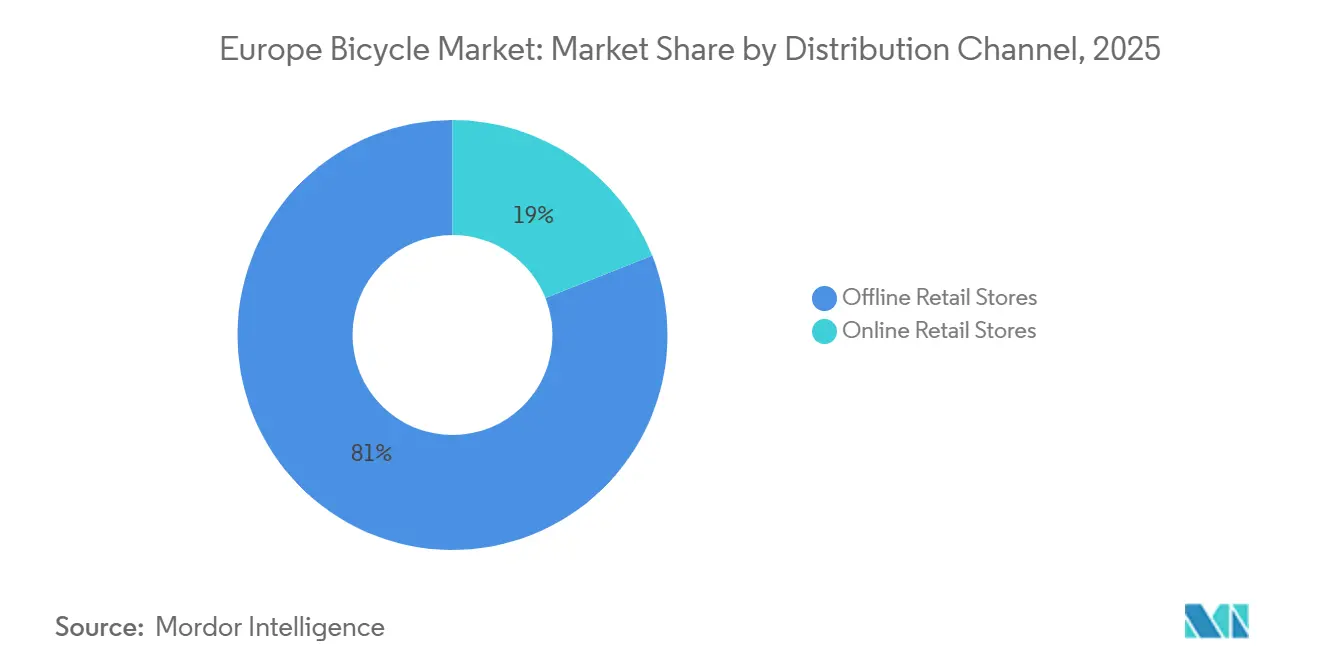

- By distribution channel, offline retail stores captured 81.02% of the 2025 value; online platforms are expanding at a 10.27% CAGR through 2031.

- By geography, Germany held a 28.22% share in 2025, and Spain is projected to grow at a 10.33% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Bicycle Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing traffic congestion in urban areas leading to higher adoption of bicycles for daily commuting | +1.8% | Germany, France, Italy, Spain (major metropolitan areas) | Medium term (2-4 years) |

| Growing awareness of health and fitness driving a rise in cycling activities | +1.2% | Netherlands, Germany, UK | Long term (≥ 4 years) |

| Government efforts to promote sustainable transportation encouraging bicycle usage | +2.1% | Spain, France, Germany, Belgium, Netherlands | Short term (≤ 2 years) |

| Rising environmental consciousness and sustainability goals boosting bicycle adoption | +1.5% | Northern Europe (Sweden, Netherlands, Germany), spreading to Southern Europe | Medium term (2-4 years) |

| Corporate wellness initiatives fostering greater use of bicycles among employees | +0.9% | Germany, Netherlands, UK, France (urban corporate hubs) | Medium term (2-4 years) |

| Escalating fuel prices positioning bicycles as an economical mode of transportation | +1.0% | Spain, Italy, Poland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban congestion drives commuter bicycle adoption

European cities are addressing traffic saturation by redefining first-mile and last-mile mobility economics. Paris allocated EUR 250 million (USD 272 million) between 2021 and 2026 to develop 1,400 kilometers of bike lanes. This shift reflects municipalities' focus on induced demand, favoring cargo e-bikes and speed pedelecs over leisure models. Increasing urban density and rising fuel costs position bicycles as a cost-efficient alternative. E-bikes, in particular, extend commuting distances and attract professionals seeking flexible, low-emission travel options. Policies such as the EU's Sustainable Urban Mobility Plans and national subsidies are integrating cycling into public transit systems, enhancing first and last-mile connectivity while reducing car dependency. In 2024, 75% of the EU's population resides in cities, according to the World Bank [1]Source: World Bank, "Urban population (% of total population) - European Union", worldbank.org, intensifying urban congestion. This demographic trend increases daily mobility needs, driving the adoption of bikes and e-bikes as efficient solutions for navigating crowded urban areas and minimizing travel times.

Health and fitness awareness fuels recreational cycling

In 2024, Sport England reported that 7,169,700 individuals in England engaged in cycling, highlighting a significant shift where cycling has evolved from being merely a mode of transportation to becoming a core component of wellness and fitness routines [2]Source: Sport England, "Active Lives Adult Survey", sportengland.org. This transformation has been largely driven by the growing emphasis on health and well-being in the post-pandemic era. As a result, fitness-focused consumers are increasingly seeking high-end features, such as lightweight carbon frames for enhanced performance, electronic shifting systems for smoother gear transitions, and integrated power meters for accurate performance monitoring, over prioritizing affordability. This growing demand for premium products allows manufacturers to maintain strong profit margins, even as overall sales volumes begin to stabilize. Moreover, this consumer segment exhibits lower price sensitivity, offering manufacturers a degree of insulation against policy changes, such as France's decision to terminate its bike bonus subsidy in February 2025.

Government sustainable transportation policies accelerate market growth

European nations are increasingly incorporating quantitative targets and multi-year funding commitments into their national cycling strategies, reflecting a growing emphasis on sustainable transportation. France's Plan Vélo for 2023-2027 exemplifies this trend, with a substantial allocation of EUR 2 billion (USD 2.18 billion) over the five-year period, equating to an annual investment of EUR 250 million (USD 272 million). This funding commitment persists despite the planned termination of direct purchase subsidies by February 2025. Similarly, the Netherlands is demonstrating its commitment to cycling infrastructure by allocating EUR 1 billion in 2025. A critical observation is that in mature markets like France, the phase-out of subsidies is redirecting financial resources toward infrastructure development and fleet programs. This strategic shift is fostering the growth of B2B sales channels and leasing models, which are gaining prominence over traditional retail approaches. While this transition may result in compressed margins for conventional dealers, it simultaneously creates significant opportunities for corporate fleet managers to expand their operations and capitalize on the evolving market dynamics.

Environmental consciousness and sustainability goals drive adoption

In 2024, the European Union's TEN-T regulation mandated that member states integrate cycling into their trans-European transport networks. This regulation requires Sustainable Urban Mobility Plans to include dedicated cycling infrastructure by 2025, ensuring a structured approach to promoting sustainable transportation. The regulatory framework establishes a baseline demand for cycling infrastructure that is driven by compliance rather than relying solely on consumer preferences. Importantly, the sustainability mandates place a stronger focus on cargo e-bikes and shared mobility fleets, as these options achieve significantly higher CO₂ displacement per unit compared to leisure bicycles. In Germany, the frequency of bicycle usage has been steadily increasing. According to the National Academy of Science and Engineering, 21% of the population in Germany reported cycling daily in 2024, highlighting a growing shift towards sustainable mobility practices [3]Source: National Academy of Science and Engineering, "Mobilitätsmonitor 2024", acatech.de.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alternative transportation options such as motorcycles and rapid transit systems reduce bicycle adoption rates | -1.2% | Southern Europe (Italy, Spain), Eastern Europe (Poland, Russia) | Medium term (2-4 years) |

| Elevated prices of electric bicycles limit widespread consumer acceptance across regions | -1.5% | Eastern Europe, Southern Europe, price-sensitive segments across all regions | Short term (≤ 2 years) |

| Proliferation of fake bicycle products negatively impacts market expansion | -0.8% | Europe | Long term (≥ 4 years) |

| Inadequate road infrastructure in rural regions affects bicycle riding experience | -0.7% | Eastern Europe (Poland, Russia), rural Spain, Italy, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Alternative transportation options constrain bicycle market share

Urban mobility budgets are becoming increasingly fragmented due to the growing popularity of e-scooters and the expansion of rapid transit networks. Shared e-scooters are replacing not only cycling trips and walking but also public transport journeys. This highlights that micro-mobility options are competing more directly with bicycles than with cars. In the Netherlands, the prohibition of e-scooters on public roads protects its cycling market. Conversely, Spain and France allow e-scooters, which intensifies direct competition. In Italy, the strong motorcycle culture adds another layer of complexity: in cities like Rome and Milan, motorcycles remain popular for their weather protection and speed, even with congestion charges, limiting bicycle adoption. For bicycle manufacturers, the strategic focus should be on enhancing utility, such as cargo capacity and weather resistance, rather than prioritizing speed or convenience, as e-scooters and transit options already dominate those areas.

Elevated e-bicycle prices limit mass-market penetration

In Europe, e-bike retail prices range from EUR 1,500 to EUR 5,000 (USD 1,633 to USD 5,443), with premium models exceeding EUR 7,000 (USD 7,620). This price range creates affordability challenges, even as battery costs decline. Although lithium-ion battery pack prices have dropped, retail prices have not decreased proportionally. Manufacturers are absorbing tariffs, logistics costs, and warranty reserves. In Eastern Europe, where median household incomes are lower than in Western Europe, e-bike adoption remains slower despite strong interest, primarily due to limited financing options. This situation suggests a potential shift: leasing and subscription models, which are already common in corporate wellness programs, could expand into consumer markets. This shift would transform revenue recognition from one-time sales to recurring streams, affecting manufacturers' working-capital dynamics.

Segment Analysis

By Product Type: E-Bicycles Reshape Category Economics

In 2025, e-bicycles accounted for 50.17% of the European market share and are expected to grow at a 9.56% CAGR through 2031. Mid-tier models are increasingly using lithium-iron-phosphate batteries instead of nickel-manganese-cobalt chemistries, offering a longer cycle life and lower costs, though with a slight reduction in energy density. The second-largest category, road and city bicycles, serves commuters who value speed and efficiency on paved roads. On the other hand, mountain and all-terrain models cater to recreational users in the Alpine and Nordic regions. Hybrid bicycles, which combine road and off-road features, were once popular among versatile riders. However, their market share is declining as e-bike motors remove the need for compromise. Riders can now choose specialized frames and rely on pedal assistance to handle diverse terrains. While cargo and recumbent models remain niche, they are growing rapidly, particularly in urban logistics.

As e-bicycles continue to dominate, traditional bicycle manufacturers without motor and battery integration capabilities are experiencing compressed margins. Companies like Bosch and Shimano demonstrate vertical integration, allowing component suppliers to capture value that previously belonged to frame builders. This trend is pressuring brands such as Canyon and Specialized to either develop proprietary electronics or face commoditization. The EU's Alternative Fuels Infrastructure Regulation, which requires workplace charging points, is removing a major barrier to e-bike adoption. This policy not only highlights a forward-thinking approach but also reverses traditional market dynamics, with policy now outpacing consumer demand.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Design: Folding Bicycles Gain Urban Commuter Traction

In 2025, regular-design bicycles accounted for 83.35% of the market. However, folding variants are experiencing rapid growth, with a 10.21% CAGR projected for 2026-2031, making them the fastest-growing segment. Brompton's G Line, launched in 2024, highlights the evolving perception of folding models. Featuring 20-inch wheels, 8-speed gearing, and hydraulic disc brakes, these bicycles are now competing on performance rather than being seen solely as utilitarian. Similarly, the Electric P Line, equipped with a lightweight titanium frame weighing 15.6 kilograms, underwent 8 years of in-house research and development to achieve UL2849 certification. This achievement reflects stricter safety standards, which are raising entry barriers for low-cost competitors. Folding bicycles are particularly effective for intermodal commuting, such as transitioning from train to office or car to trail. This advantage explains their significant growth in densely populated cities like London, Paris, and Berlin, where extensive public transit systems often leave last-mile gaps.

Regular designs maintain their dominance due to superior ride quality, component compatibility, and higher resale value. Enthusiasts and long-distance commuters prioritize frame stiffness and wheel size over portability, ensuring continued demand for traditional geometries. The key insight is that folding bicycles are not replacing regular models but are instead establishing a parallel category. They cater to urban professionals who integrate cycling with public transit rather than competing directly. Manufacturers should avoid positioning folding bikes as universal solutions and instead focus on targeting specific commuter profiles with tailored marketing and distribution strategies.

By End User: Children's Segment Accelerates on Safety and Health Trends

In 2025, men represented 46.36% of the cycling market, highlighting their historical dominance in cycling participation. However, the children's segment is growing at the fastest pace, with a projected CAGR of 9.85% from 2026 to 2031. This growth is driven by parents emphasizing outdoor activities and schools, particularly in cycling-focused countries like the Netherlands and Denmark, integrating cycling into physical education programs. While women form a significant segment, their growth is hindered by safety concerns and inadequate infrastructure. Women place greater importance on protected bike lanes compared to men, making their participation more dependent on infrastructure quality than product features. Furthermore, the children's segment benefits from frequent bike replacements as children outgrow their frames, creating recurring revenue opportunities that are absent in adult segments.

On a deeper level, children's bicycles act as entry points for brands, shaping long-term customer preferences. Although the women's segment is growing at a slower rate, it remains strategically important. Female cyclists demonstrate stronger brand loyalty and are more likely to purchase accessories, apparel, and service packages, increasing their lifetime customer value. Brands that go beyond the "shrink it and pink it" strategy by designing frame geometry, saddles, and marketing specifically for women are capturing a larger share of this growing segment.

By Distribution Channel: Online Retail Gains Despite Physical Showroom Advantages

In 2025, offline retail stores accounted for 81.02% of the market share. However, online channels are expected to grow at a 10.27% CAGR from 2026 to 2031, driven by advancements in e-commerce infrastructure and the adoption of direct-to-consumer strategies. According to Eurostat data, 77% of EU internet users made online purchases in 2024, highlighting the widespread acceptance of e-commerce, a trend now being leveraged by the bicycle market. Consumers increasingly exhibit omnichannel behavior, researching products online, testing them in-store, and purchasing from the channel offering the best terms, thereby blurring the distinction between online and offline channels.

Offline retail continues to dominate the market for high-value e-bikes and custom builds, as consumers prioritize test rides, fit adjustments, and in-person consultations. Conversely, online platforms excel in selling accessories, components, and entry-level models, where product knowledge is readily available, and price transparency supports digital comparisons. The strategic takeaway for manufacturers is to adopt hybrid distribution strategies: leveraging physical stores for brand experiences and complex sales while utilizing online platforms for efficiency and volume. This approach avoids treating distribution as a binary choice. Canyon Bicycles illustrates this strategy with its direct-to-consumer model, which bypasses traditional dealers entirely. This model demonstrates how vertical integration can eliminate intermediary margins but also emphasizes the need for significant investments in logistics, customer service, and brand marketing to build the trust typically associated with physical retailers.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, Germany held a significant 28.22% share of the European bicycle market, establishing itself as a leader in the region. This dominance is largely attributed to the National Cycling Plan 3.0, which allocates an impressive EUR 1.46 billion (approximately USD 1.59 billion) in federal funding for the decade spanning 2021 to 2030. The plan sets an ambitious goal of achieving a 25% cycling modal share by 2030. Germany's market leadership is further reinforced by its extensive network of advanced bike lanes, which span thousands of kilometers, government subsidies that encourage e-bike adoption, and a growing number of commuters opting for bicycles in heavily congested urban centers such as Berlin.

Spain is emerging as the fastest-growing geographic market, with a robust CAGR of 10.33% projected for the period from 2026 to 2031. This rapid growth is driven by increasing urban mobility requirements, government-backed incentives to promote cycling, and the rising popularity of leisure and tourism cycling in key cities like Barcelona and Madrid. The e-bike and cargo bike segments are playing a pivotal role in this expansion, supported by European Union funding aimed at enhancing cycling infrastructure. These factors collectively enable Spain to outpace more mature and established markets in the region.

The Netherlands, on the other hand, is approaching market saturation. A significant proportion of daily trips in the country are already made by bicycle, and e-bikes dominate new sales. Infrastructure investments are now primarily focused on widening existing bike lanes rather than constructing new ones. Market growth in the Netherlands is largely driven by the replacement of standard bicycles with premium models and the increasing adoption of upgraded cargo bikes. Italy, meanwhile, maintains a stable position in the market. Growth in Italy is fueled by a rising demand for high-end, premium models. Additionally, the United Kingdom, Nordic countries, and Eastern Europe are contributing to the overall growth of the European bicycle market, driven by government incentives and the ongoing trend of urbanization.

Competitive Landscape

The European bicycle market is moderately fragmented, fostering a competitive environment where established players such as Accell Group NV, Giant Manufacturing Co. Ltd, Pon Holdings BV, Trek Bicycle Corporation, and Scott Sports SA face challenges from financial pressures and new market entrants. This competition has driven manufacturers to prioritize product differentiation and strategic market positioning. Regional players are also gaining traction by targeting specific market segments and efficiently utilizing local distribution networks.

The industry's competitive landscape is shifting, with a growing emphasis on direct-to-consumer sales models and corporate leasing programs. Companies with strong digital capabilities and service infrastructures are benefiting the most from this transition, which represents a move away from traditional retail-focused strategies. In response, conventional retailers are adapting their business models and strengthening their online presence. Additionally, manufacturers are expanding their after-sales service networks to build direct customer relationships and enhance long-term brand loyalty.

Opportunities are emerging in areas such as cargo e-bikes for last-mile delivery, subscription and leasing models that transition revenue from one-time sales to recurring streams, and blockchain-based authentication systems. For instance, the European Union Intellectual Property Office's EBSI-ELSA blockchain pilot highlights the use of digital product passports to authenticate supply chains. This approach positions anti-counterfeiting measures as a tool for justifying premium pricing. Disruptors like Urban Arrow and Riese and Müller are gaining attention by focusing on cargo and utility e-bikes designed for commercial logistics rather than leisure. Their products are attracting interest from companies like DHL, UPS, and municipal fleets that prioritize total cost of ownership over upfront costs. The market is also witnessing a technological divide: premium brands are incorporating IoT connectivity, theft prevention, and predictive maintenance, while value-oriented brands compete on price and availability. This has created a barbell market structure, putting pressure on mid-tier players that lack clear differentiation.

Europe Bicycle Industry Leaders

-

Trek Bicycle Corporation

-

Accell Group NV

-

Pon Holdings BV

-

Scott Sports SA

-

Giant Manufacturing Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: ENYRING GmbH partnered with Swobbee to deploy a swappable battery platform for e-bikes across Berlin and Amsterdam, boosting urban micromobility infrastructure.

- April 2025: Ampler unveiled the Nova and Nova Pro electric bicycles featuring USB-C charging compatibility. These models incorporate advanced battery technology and offer riders the convenience of charging their devices through integrated USB-C ports.

- April 2025: Gabriel India Limited entered the European bicycle market by introducing suspension solutions for city, cargo, SUV, and mountain bikes. The company focuses on providing suspension forks for specific bicycle categories.

- September 2024: Brompton expanded its product line by introducing folding gravel bikes with 20-inch wheels. The new models combine the company's folding mechanism with larger wheels to provide better stability and versatility for off-road cycling.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Europe bicycle market comprises every newly manufactured pedal-propelled or electrically assisted two-wheeler that is sold for mobility, sport, leisure, cargo, or rental purposes across 10 tracked countries. Vehicles such as mopeds, e-scooters, kick-scooters, and children's ride-ons fall outside this scope.

Scope Exclusion: Motorcycles, micro-mobility devices without functional pedals, and second-hand bicycle transactions are not considered.

Segmentation Overview

-

By Product Type

- Road/City

- Mountain/All-Terrain

- Hybrid

- E-Bicycle

- Other Types

-

By Design

- Regular

- Folding

-

By End-User

- Men

- Women

- Children

-

By Distribution Channel

- Offline Retail Stores

- Online Retail Stores

-

By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

Detailed Research Methodology and Data Validation

Desk Research

Our analysts first assembled baseline data from public sources such as Eurostat trade codes, Germany's ZIV, France's Union Sport & Cycle, the European Cyclists' Federation, and patent filings retrieved via Questel. Annual reports of listed bicycle groups, customs import-export records, and press archives on Dow Jones Factiva enriched supply, price, and policy signals. These illustrate unit flows, retail price ranges, fiscal incentives, and modal-share shifts. The sources cited here illustrate, not exhaust, the body of secondary material referenced.

Primary Research

Subsequently, we interviewed component makers, leading bike assemblers, urban-planning officials, and fleet-sharing operators across Western and Central Europe. Their insights clarified subsidy uptake timelines, factory utilization swings, and average selling prices, allowing us to challenge earlier desk assumptions and adjust discounting on dealer inventory.

Market-Sizing & Forecasting

A top-down model converts country-level production, import, and export tonnage into unit volumes, which are then multiplied by weighted ASPs derived from retail scanner data and distributor feedback. Select bottom-up checks, sampled OEM revenue roll-ups, and online channel audits anchor the totals. Key variables tracked include bike ownership per 1,000 residents, e-bike subsidy value per unit, average urban commute distance, GDP per capita, and lithium-ion battery pack cost. A multivariate regression (GDP, urbanization, subsidy intensity, battery price) generates the 2025-2030 forecast path. Scenario analysis stress-tests fuel-price or incentive shocks. Data gaps in low-reporting countries are bridged through three-year moving-average interpolation, later confirmed with local trade bodies.

Data Validation & Update Cycle

Outputs undergo variance checks against historical import codes, survey demand indicators, and listed-company guidance. An analyst peer reviews anomalies before sign-off. The study refreshes annually, and interim updates are triggered by material policy or demand shocks.

Why Mordor's Europe Bicycle Baseline Commands Reliability

Published estimates often diverge because firms differ in scope definitions, geography depth, and refresh cadence.

Key gap drivers include whether electric cargo bikes are counted, how aggressive the ASP curve is, and if Eastern European demand is modeled or inferred. Mordor's study reports the full pedal and electric bicycle universe and applies 2024 exchange averages, whereas other publishers may freeze rates earlier or omit e-mobility segments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 29.97 B (2025) | Mordor Intelligence | - |

| USD 22.02 B (2024) | Global Consultancy A | Excludes e-bikes; relies on 2022 production ratios |

| USD 20.80 B (2024) | Industry Research House B | Limited to five Western nations; conservative subsidy uptake |

| USD 29.35 B (2024) | Trade Journal C | Retail sales only; single-date FX conversion |

In brief, our balanced top-down build, country-level granularity, and annual update rhythm give decision-makers a transparent, repeatable baseline that aligns closely with on-ground dynamics and validated stakeholder expectations.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Europe bicycle market in 2026?

The Europe bicycle market size is valued at USD 33.37 billion in 2026, with an 8.59% CAGR projected through 2031.

Which product category grows fastest in Europe?

E-bicycles expand at 9.56% CAGR to 2031, outperforming every other product type.

What share do online channels hold for bicycle sales?

Online platforms represented 18.98% of 2025 value and are growing at 10.27% CAGR, steadily gaining ground on physical stores.

Which country leads European bicycle demand?

Germany accounted for 28.22% of 2025 revenue, supported by EUR 1.46 billion in federal cycling funding.