Market Trends of Europe Aviation Industry

Military Segment to Showcase Remarkable Growth During the Forecast Period

Europe has a robust and technologically advanced military helicopter market that is driven by various factors, including geopolitical concerns, modernization efforts, and defense budget allocations. The defense budgets of European countries play a crucial role in shaping the military helicopter market. Despite economic challenges, defense spending has remained a priority for many European nations due to rising security concerns.

In 2022, Europe spent USD 480 billion on its military, an increase of 13% over 2021. By the end of March 2022, numerous European NATO member nations announced plans to increase military expenditures in reaction to the Russian invasion of Ukraine in February 2022, aiming to meet or exceed the NATO spending target of 2% of GDP or higher.

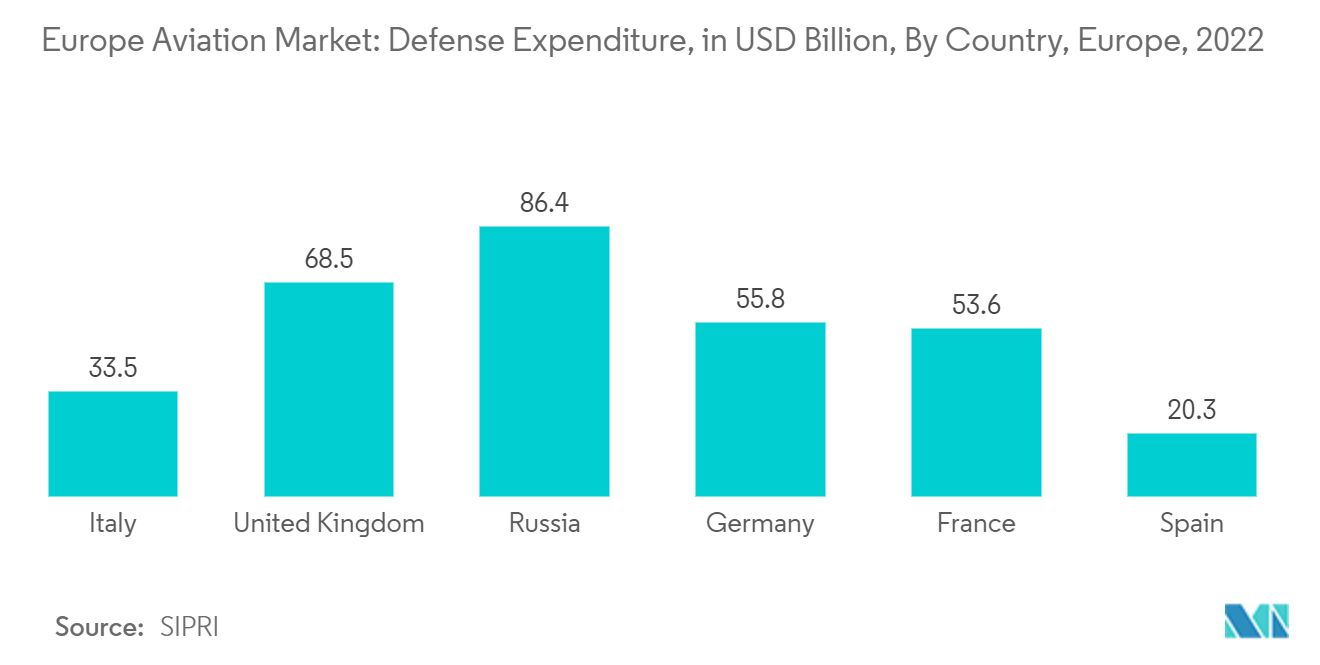

Upgrading aging platforms with state-of-the-art helicopters enables countries to enhance their operational effectiveness, increase mission versatility, and maintain interoperability with NATO and other allied forces. Germany, France, the United Kingdom, Russia, Italy, Spain, the Netherlands, and the Rest of Europe plan to purchase helicopters from 2024 to 2029.

For instance, in March 2022, Germany expressed its plans to procure 15 Eurofighter jets and up to 35 US-made F-35 fighter jets as part of a major boost to upgrade the armed forces in reaction to Russia's invasion of Ukraine. The F-35 jets made by Lockheed Martin would replace Germany's aging 40-year-old Tornado aircraft fleet.

The United Kingdom is Estimated to Dominate the Market During the Forecast Period

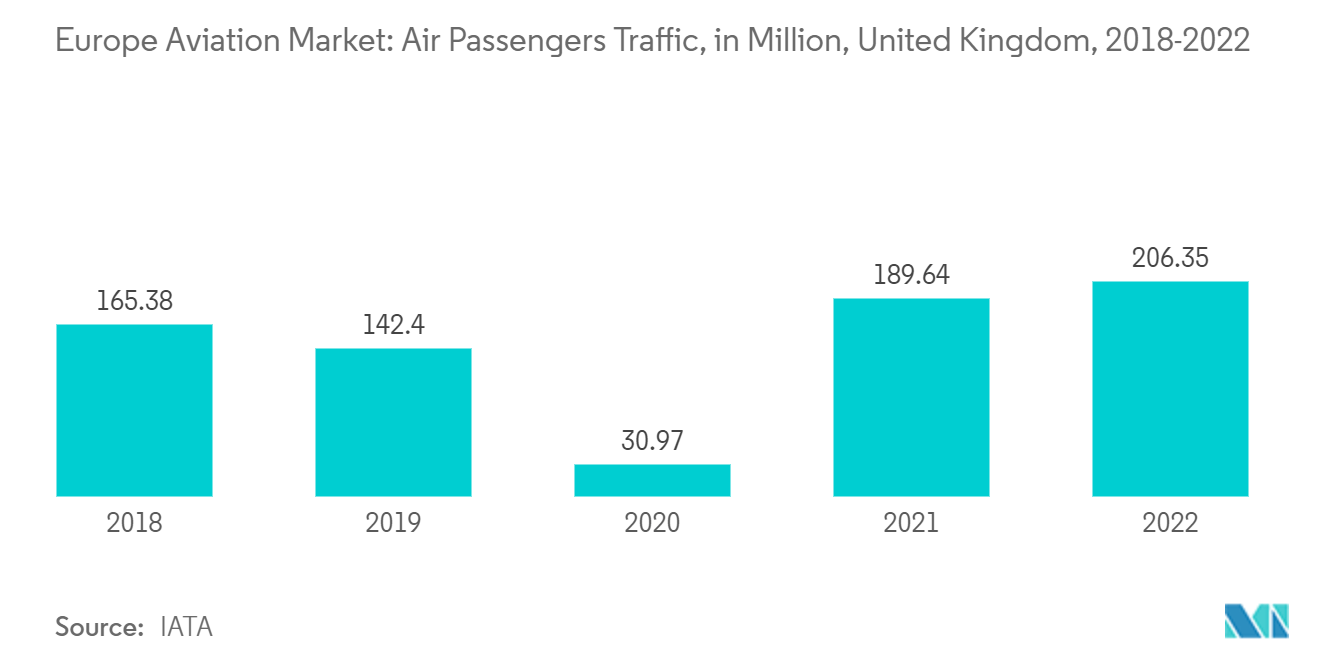

The UK-based airlines were responsible for uplifting a total of 206.35 million air passengers who traveled through the UK in 2022, compared to 189.64 million in 2021. The growth between 2022 and 2021 was 8.8%, and the growth between 2022 and 2020 was 566%. The country’s revenue passenger kilometers recorded a 644% growth in 2022 compared to 2021 and 501% compared to 2020. The inputs to the air transport industry and foreign visitors who arrive by air contribute 4.5% to the country’s GDP.

UK airlines are procuring new aircraft to cater to the demand generated by the rising rates of air travel and to replace aging aircraft with fuel-efficient models. In December 2023, Easyjet ordered 56 A320neo and 101 A321neo models. Similarly, in September 2023, British Airways finalized orders for 6 Boeing B787-10 and 10 A320neos.

General aviation employs around 12,000 people in the United Kingdom. About 96% of the 21,000 civilian aircraft registered in the United Kingdom are used for general aviation, and the GA fleet logs between 1.25 million and 1.35 million hours of flight time yearly. There are 10,000 certified glider pilots and 28,000 people with Private Pilot Licenses (PPL). The use of more accessible aircraft, such as microlights, locally built airplanes, and smaller helicopters, has risen in the past 20 years.

The country's military budget for 2022 was USD 68.5 billion, a rise of 3.7%. Out of the total government spending, the country has allocated 2.2% of its share to the military. Its NATO membership commits the UK to devote 2% of its annual GDP to defense. Currently, the United Kingdom dedicates more than 2% of its GDP to the military. The country is buying new-generation aircraft to improve its aviation capabilities, thus resulting in increased military spending.