Market Size of Europe Automotive Semiconductor Industry

| Study Period | 2018 - 2029 |

| Base Year For Estimation | 2023 |

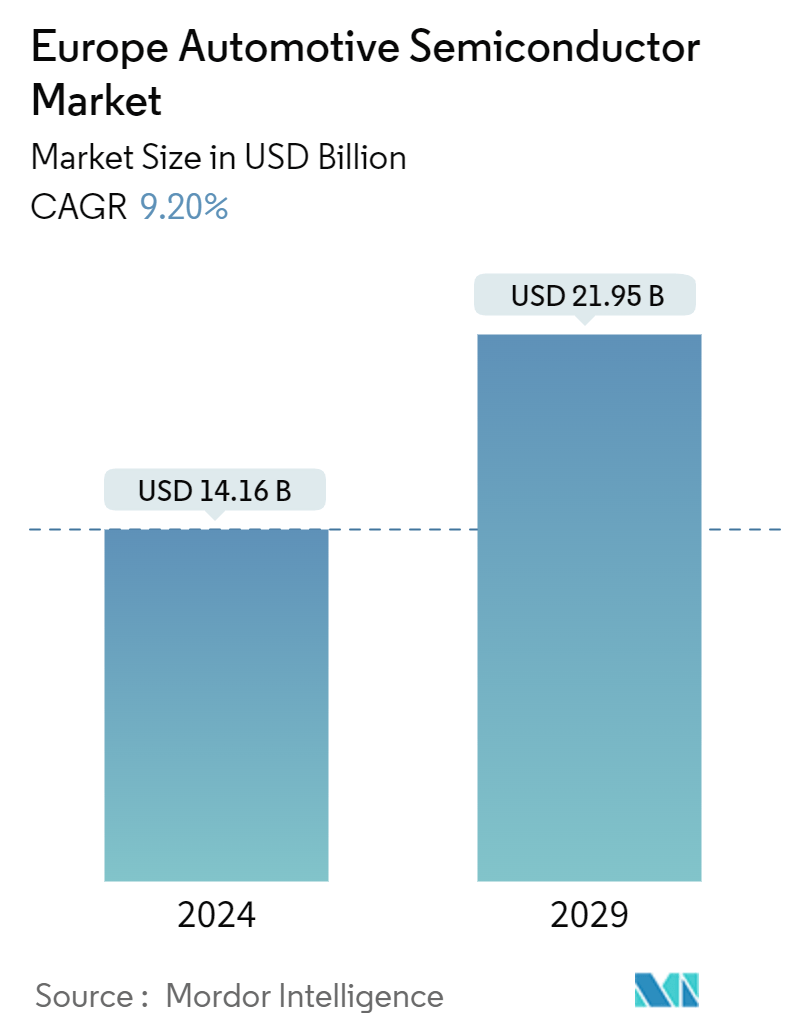

| Market Size (2024) | USD 14.16 Billion |

| Market Size (2029) | USD 21.95 Billion |

| CAGR (2024 - 2029) | 9.20 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Automotive Semiconductor Market Analysis

The Europe Automotive Semiconductor Market size is estimated at USD 14.16 billion in 2024, and is expected to reach USD 21.95 billion by 2029, growing at a CAGR of 9.20% during the forecast period (2024-2029).

- An automotive semiconductor is a type of semiconductor chip specifically designed and used in the automotive industry. These chips play a crucial role in the functioning of various electronic components and systems in vehicles. They are responsible for powering and controlling many features and functions, including safety systems, infotainment systems, engine control units, sensors, etc.

- Automotive semiconductors have become increasingly important as vehicles have become more technologically advanced. They are essential for integrating advanced technologies such as autonomous driving, electric powertrains, and connected car systems. These semiconductors are designed to meet the specific requirements of the automotive industry, including durability, reliability, and the ability to operate in harsh environments.

- One of the primary applications of automotive semiconductors is in Advanced Driver Assistance Systems (ADAS). These systems use sensors, cameras, and processors to enhance vehicle safety and assist drivers in real-time. Semiconductors enable features like adaptive cruise control, lane-keeping assist, automatic emergency braking, blind-spot detection, and pedestrian detection, making driving safer and reducing the risk of accidents.

- Semiconductors play a crucial role in developing advanced infotainment systems in vehicles. These systems provide a seamless integration of entertainment, navigation, and communication features. Automotive semiconductors enable touchscreens, voice recognition, connectivity options, and multimedia playback, transforming the driving experience into a personalized and connected one.

- The increasing investments in the automotive semiconductor industry in Europe are likely to aid the development of the market studied. For instance, in August 2023, Robert Bosch GmbH, TSMC, NXP Semiconductors NV, and Infineon Technologies AG announced a plan to jointly invest in ESMC (European Semiconductor Manufacturing Company GmbH) in Dresden, Germany, to offer advanced semiconductor manufacturing services. ESMC is claimed to mark a substantial step toward constructing a 300 mm fab to support the future capacity requirements of the fast-growing automotive and industrial sectors.

- The project is designed under the framework of the European Chips Act. The planned fab is anticipated to have a monthly production capacity of 40,000 wafers (12-inch) on TSMC’s 28/22 nanometer planar CMOS and 16/12 nanometer FinFET process technology, bolstering Europe’s semiconductor manufacturing ecosystem with advanced FinFET transistor technology and creating approximately 2,000 direct high-tech professional jobs. ESMC seeks to begin construction of the fab in the second half of 2024, with production targeted to commence by the end of 2027.

- Semiconductors enable vehicle connectivity, forming the foundation for connected car technology. They power wireless communication systems, allowing vehicles to connect with other vehicles (V2V), infrastructure (V2I), and the internet (V2X). This connectivity facilitates real-time data exchange, enabling features like traffic updates, remote vehicle diagnostics, over-the-air updates, and even autonomous driving capabilities.

- With the increasing concern for environmental sustainability and the necessity to reduce carbon emissions, electric vehicles (EVs) have gained immense popularity in Europe. EVs rely heavily on semiconductor technology for power management, battery management, and motor control systems. As the demand for EVs continues to rise, so does the demand for automotive semiconductors.

- According to the European Automobile Manufacturers Association (ACEA), the sales volume of battery electric (BEV) and plug-in hybrid electric vehicles (PHEV) in Europe increased from 559.81 thousand in Q2 2022 to 757.83 thousand in Q3 2023. Such an increase in the demand for EVs would offer lucrative opportunities for the growth of the studied market.

- However, the high cost of development and production is a significant barrier to the growth of the market studied. The complex manufacturing processes and testing requirements make these semiconductors expensive, limiting their affordability for both manufacturers and consumers.

- Furthermore, the conflict between Russia and Ukraine is expected to significantly impact the semiconductor industry. The conflict has already exacerbated the electronics & semiconductor supply chain issues and the chip shortage that have affected the industry for some time. The disruption may result in volatile pricing for critical raw materials such as nickel, palladium, copper, titanium, and aluminum, resulting in material shortages. This, in turn, could impact the manufacturing of automotive semiconductors.

Europe Automotive Semiconductor Industry Segmentation

For market estimation, we have tracked the revenue generated from the sale of automotive semiconductors offered by different market players for a diverse range of applications. The market trends are evaluated by analyzing the investments made in product innovation, diversification, and expansion. Furthermore, the advancements in electric vehicles, miniaturization of automotive electronics, advanced driver-assistance systems (ADAS), and connected cars are also crucial in determining the growth of the market.

The European automotive semiconductor market is segmented by vehicle type (passenger vehicle (discrete, optoelectronics. sensors and actuators, logic, memory, analog IC, micro), light commercial vehicle (discrete, optoelectronics. sensors and actuators, logic, memory, analog IC, micro), and heavy commercial vehicle (discrete, optoelectronics. sensors and actuators, logic, memory, analog IC, micro)), application (chassis, power electronics, safety, body electronics, comfort/entertainment, and other applications), and country (Germany, France, Italy, and Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Vehicle Type | |||||||||

| |||||||||

| |||||||||

|

| Application | |

| Chassis | |

| Power Electronics | |

| Safety | |

| Body Electronics | |

| Comfort/Entertainment Unit | |

| Other Applications |

| Country | |

| United Kingdom | |

| Germany | |

| France | |

| Italy |

Europe Automotive Semiconductor Market Size Summary

The European automotive semiconductor market is poised for significant growth, driven by the increasing integration of advanced technologies in vehicles. These semiconductors are essential for powering and controlling various electronic systems, including safety features, infotainment, and engine control units. As vehicles become more technologically advanced, the demand for automotive semiconductors is rising, particularly in applications such as Advanced Driver Assistance Systems (ADAS) and electric vehicles (EVs). The market is supported by substantial investments in semiconductor manufacturing capabilities, such as the joint venture by major companies to establish a new fab in Germany, which aims to enhance Europe's semiconductor production capacity. This growth is further fueled by the rising production of vehicles in Europe and the growing popularity of EVs, which rely heavily on semiconductor technology for efficient power management and connectivity.

Germany stands out as a key player in the European automotive semiconductor market, with a robust ecosystem of manufacturers, suppliers, and technology companies. German firms like Infineon Technologies, Bosch, and Continental AG are at the forefront of developing semiconductors that meet the unique demands of modern vehicles, including those for autonomous driving and energy efficiency. The market is characterized by collaboration between semiconductor companies and automotive manufacturers to drive innovation and meet evolving consumer demands. Despite challenges such as high development costs and geopolitical tensions affecting supply chains, the market is expected to continue its upward trajectory, supported by ongoing advancements in semiconductor technology and strategic partnerships aimed at enhancing vehicle safety, connectivity, and performance.

Europe Automotive Semiconductor Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

1.4 Impact of COVID-19, Aftereffects, and Other Macroeconomic Trends on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 Vehicle Type

-

2.1.1 Passenger Vehicle

-

2.1.1.1 Discrete

-

2.1.1.2 Optoelectronics

-

2.1.1.3 Sensors and Actuators

-

2.1.1.4 Logic

-

2.1.1.5 Memory

-

2.1.1.6 Analog IC

-

2.1.1.7 Micro

-

-

2.1.2 Light Commercial Vehicle

-

2.1.2.1 Discrete

-

2.1.2.2 Optoelectronics

-

2.1.2.3 Sensors and Actuators

-

2.1.2.4 Logic

-

2.1.2.5 Memory

-

2.1.2.6 Analog IC

-

2.1.2.7 Micro

-

-

2.1.3 Heavy Commercial Vehicle

-

2.1.3.1 Discrete

-

2.1.3.2 Optoelectronics

-

2.1.3.3 Sensors and Actuators

-

2.1.3.4 Logic

-

2.1.3.5 Memory

-

2.1.3.6 Analog IC

-

2.1.3.7 Micro

-

-

-

2.2 Application

-

2.2.1 Chassis

-

2.2.2 Power Electronics

-

2.2.3 Safety

-

2.2.4 Body Electronics

-

2.2.5 Comfort/Entertainment Unit

-

2.2.6 Other Applications

-

-

2.3 Country

-

2.3.1 United Kingdom

-

2.3.2 Germany

-

2.3.3 France

-

2.3.4 Italy

-

-

Europe Automotive Semiconductor Market Size FAQs

How big is the Europe Automotive Semiconductor Market?

The Europe Automotive Semiconductor Market size is expected to reach USD 14.16 billion in 2024 and grow at a CAGR of 9.20% to reach USD 21.95 billion by 2029.

What is the current Europe Automotive Semiconductor Market size?

In 2024, the Europe Automotive Semiconductor Market size is expected to reach USD 14.16 billion.