Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 7.02 Billion |

| Market Size (2030) | USD 9.15 Billion |

| Growth Rate (2025 - 2030) | 5.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Automotive Glass Market Analysis by Mordor Intelligence

The European automotive glass market size is valued at USD 7.02 billion in 2025 and is projected to reach USD 9.15 billion by 2030, registering a CAGR of 5.45% (2025 to 2030). The acceleration reflects a structural swing from commodity tempered products toward laminated, acoustic, and electrochromic glazing that meets stringent EU safety rules and battery-electric-vehicle (BEV) efficiency targets. Windshields integrate rain sensors, cameras, and heads-up display (HUD) interlayers, elevating unit value and cementing OEM design-in dominance. Panoramic sunroofs, often spanning 1.5-2.0 square meters, raise thermal-management complexity and spur demand for infrared-blocking interlayers. Smart glass adoption is widening as material costs fall, while production is steadily localizing in Central Europe to shorten lead times and cut logistics emissions.

Key Report Takeaways

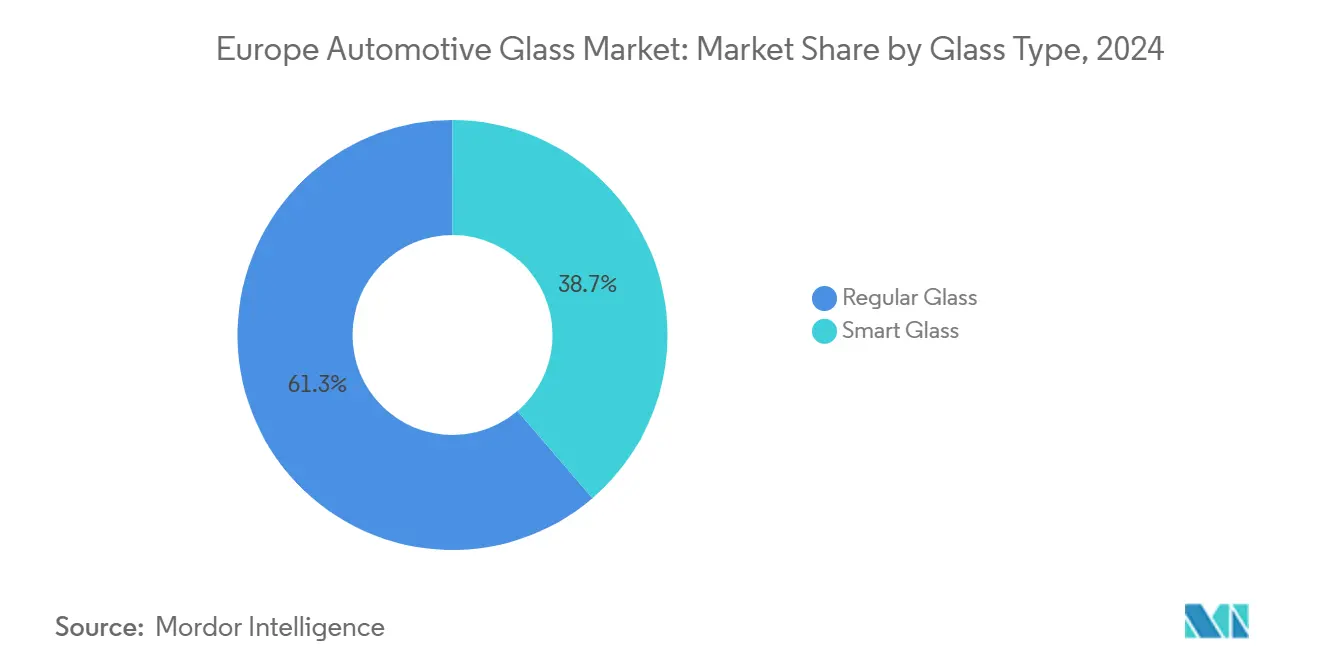

- By glass type, regular variants led with 61.28% of the European automotive glass market share in 2024, whereas smart glass is forecasted to expand at a 6.42% CAGR through 2030.

- By application, windshields accounted for 46.98% of the European automotive glass market size in 2024, while sunroofs are projected to advance at a 5.99% CAGR to 2030.

- By vehicle type, passenger cars controlled 72.51% revenue in 2024 and are the fastest growing at 5.79% CAGR through 2030.

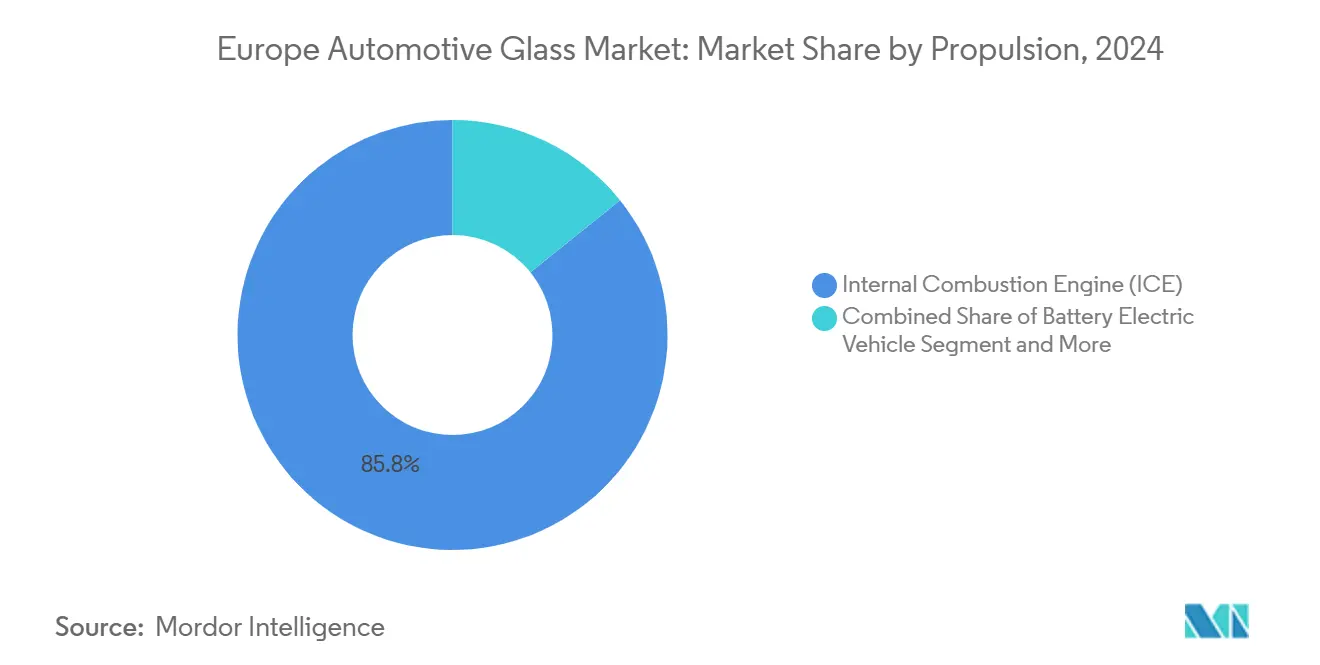

- By propulsion, internal-combustion platforms held 85.79% of demand in 2024, yet battery electric vehicles are set to rise at a 9.42% CAGR to 2030.

- By sales channel, OEM procurement captured 92.94% revenue in 2024, whereas the aftermarket is expected to grow at a 6.53% CAGR to 2030.

- By country, Germany led with 25.53% revenue in 2024; Poland is projected to post the highest 6.76% CAGR to 2030.

Europe Automotive Glass Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Panoramic Sunroofs and Larger Glazing Areas | +1.2% | Germany, France, United Kingdom, Italy, Spain | Medium term (2-4 years) |

| EU Vehicle Safety Regulations | +0.9% | Europe-wide (Germany, France, Italy, Spain, Poland, Czech Republic) | Short term (≤ 2 years) |

| Integration of Smart/Electrochromic Glass | +0.8% | Germany, France, United Kingdom, Sweden | Medium term (2-4 years) |

| Lightweight Acoustic Glazing Demand | +0.7% | Germany, France, Netherlands, Norway, Sweden | Medium term (2-4 years) |

| Supply-Chain Localization Incentives | +0.6% | Poland, Czech Republic, Hungary, Slovakia, Romania | Long term (≥ 4 years) |

| Automotive Circular-Economy Mandates | +0.4% | Europe-wide (Germany, France, Netherlands, Belgium) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Panoramic Sunroofs and Larger Glazing Areas in European Sport Utility Vehicle and Crossover Launches

Sport utility vehicle (SUV) and crossover launches increasingly specify roof glass that enlarges perceived cabin space and commands premium option pricing. OEMs in Germany, France, and the United Kingdom saw compact and mid-size SUVs lead the new-registration mix. Larger apertures lift interior heat gain, pushing suppliers toward multi-layer laminates with infrared-absorbing PVB to manage solar load. The additional area also necessitates stiffer roof frames, creating design collaboration between glassmakers and body engineers. Switchable polymer-dispersed-liquid-crystal (PDLC) panels are migrating from luxury nameplates into upper-mid trims as material prices fall. Over the medium term, panoramic glass roofs are expected to feature solar cells that trickle-charge accessory batteries, further increasing surface value per vehicle.

EU Vehicle Safety Regulations Mandating Advanced Laminated and HUD-Ready Windshields

UN Regulation No. 43 requires laminated windshields across all categories to reduce occupant ejection risk, while Euro NCAP’s 2025 roadmap offers additional safety points for embedded HUD capability[1]United Nations Economic Commission for Europe, “UN Vehicle Regulations,” UNECE, unece.org. These rules compress development cycles and favor suppliers that can co-engineer interlayers supporting camera mounts and reflective coatings. OEM engineering teams are incorporating windshield curvature tolerances tighter than 0.2 mm to maintain optical clarity for forward-looking sensors. The mandates also increase replacement complexity in the aftermarket, reinforcing design-in advantages for tier-one producers equipped with in-house validation labs. As sensor suites proliferate, HUD-ready glass is poised to become the baseline on most C-segment vehicles by 2030.

Accelerating OEM Integration of Smart/Electrochromic Glass for Energy Efficiency and Occupant Comfort

Electrochromic, suspended-particle-device, and PDLC technologies allow drivers to modulate light transmission electronically, limiting reliance on mechanical shades. Demonstration vehicles show opacity shifts in under three seconds at power draws below 5 W per m². Germany, France, and Sweden account for the bulk of early adoption as premium buyers accept the added cost for thermal comfort and privacy. On BEV platforms, smart glass cuts HVAC load, freeing capacity for drivetrain efficiency. Upcoming Stellantis ride-hailing shuttles intend to deploy instant-tint side panes that double as information screens, widening the use-case set.

Lightweight Acoustic Glazing Demand Driven by EV Range Optimization Targets

Elimination of engine noise in BEVs exposes wind and tire sound that previously masked cabin disturbances, increasing the value proposition for acoustic laminates. Saint-Gobain testing shows double-glazed low-emissivity units trim HVAC consumption. Eastman’s 0.76 mm acoustic interlayer improves noise attenuation by up to 10 dB without mass penalty, meeting aggressive weight targets[2]"Saflex Acoustic (Q Series) PVB Interlayer" Eastman, saflex-vanceva.eastman.com. Germany and the Netherlands, where BEV penetration is significant, have become lead markets for this glass. Future iterations are expected to embed heating wires and antenna arrays on ultra-thin substrates, supporting the industry shift toward software-defined cockpits.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production and Integration Cost | -0.5% | Europe-wide (Germany, France, Italy, Spain, Poland) | Medium term (2-4 years) |

| ADAS Windshield Calibration Skill Shortage | -0.4% | United Kingdom, Germany, France, Italy, Spain | Short term (≤ 2 years) |

| Volatility in Soda Ash and Energy Prices | -0.3% | Germany, France, Poland, Czech Republic, Spain | Short term (≤ 2 years) |

| Stringent EU End-of-Life Recycling Targets | -0.2% | Europe-wide (Germany, France, Netherlands, Belgium) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production and Integration Cost of Smart/Advanced Glazing Limiting Penetration in Mass-Market Segments

Electrochromic and SPD systems add approximately EUR 300-800 (USD 353 to 941.5) per vehicle, a delta that mass-market OEMs struggle to offset when competing on price. Organic electrochromic films promise simpler stacks yet face hermetic-sealing challenges that depress yield. Volume brands in Poland, Spain, and Italy prioritize cost-down programs, limiting deployment to flagship trims. The restraint moderates diffusion speed even as consumer awareness grows, keeping penetration below outside premium segments through 2027. Long-term, scale and material breakthroughs must cut costs to unlock high-volume platforms.

Skills Shortage for ADAS Windshield Calibration in Aftermarket Service Networks

Only a small fraction of European technicians hold certifications for camera and radar calibration, creating replacement bottlenecks and higher insurance costs. The gap is acute in the United Kingdom, where independent repairers dominate, and turnover is high. Compliance with UN Regulation No. 10, which governs electromagnetic compatibility, further complicates the process by requiring post-install validation. Slow training pipeline expansion risks elevating claim cycle times just as ADAS windshield share grows significantly by 2030. Investment in calibration rigs and standardized curricula remains essential to avoid safety and liability exposure.

Segment Analysis

By Glass Type: Smart Glass Gains Traction Despite Cost Barriers

Regular laminated and tempered variants commanded 61.28% revenue in 2024, driven by their use in windshields, backlites, and sidelites where proven durability and cost efficiency prevail. UN Regulation No. 43 mandates laminated windshields, keeping baseline demand high and supporting the Europe automotive glass market size predictability. Tempered glass continues as standard for sidelites and backlites; its rapid disintegration upon impact aids passenger egress and simplifies recycling streams. Smart glass, however, is accelerating at a 6.42% CAGR as electrochromic, SPD, and PDLC technologies migrate from luxury concepts into series production.

Electrochromic solutions lead the smart subset by volume and are widely favored for precise tint control and low power draw. These stacks employ tungsten-oxide or lithium-ion layers that darken under applied voltage, offering step-less modulation within one percent increments. SPD films align suspended particles to enable transparency when energized, delivering faster switching but requiring continuous power. PDLC is gaining traction for privacy windows in luxury MPVs and ride-sharing shuttles. The European automotive glass market continues to reward suppliers who can integrate smart layers without sacrificing optical clarity or acoustic damping.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Windshields Dominate, Sunroofs Accelerate

Windshields held 46.98% revenue in 2024 because of their size and the embedded technology stack that now includes cameras, infrared heating meshes, and HUD projection foils. Euro NCAP’s 2025 protocol awards points for HUD functions, reinforcing OEM preference for laminated surfaces able to maintain optical transmittance at defined refractive indices. Aftermarket replacement can cost significantly for ADAS-equipped panes, expanding revenue potential beyond first fit. Sunroofs are projected to grow at a 5.99% CAGR as automakers differentiate trims with expansive glass that improves perceived cabin space. Modules integrating switchable PDLC and solar cells can harvest up to 150 W under peak irradiance, contributing to accessory loads and boosting the European automotive glass market share for roof applications.

Backlites and sidelites, accounting for roughly one-third of volume, are transitioning from tempered to laminated construction to meet rising acoustic and security expectations. Electrified drivetrains reveal new noise sources, making acoustic sidelites a potent refinement tool. Mirrors, although small in area, now incorporate electrochromic dimming and camera feeds, capitalizing on UN Regulation No. 46’s allowance for virtual mirrors UNECE. Quarter and vent panels remain commodity items yet benefit from adoption of laminated quiet-zone glass in premium SUVs. Across all applications, the Europe automotive glass market rewards multi-function designs that couple coatings, sensors, and electronics into a single pane.

By Vehicle Type: Passenger Cars Lead, SUVs Drive Growth

Passenger cars held 72.51% of 2024 demand, reflecting the region’s entrenched hatchback, sedan, and compact models. Cost-focused B- and C-segment vehicles specify tempered backlites and sidelites, but acoustic laminated windshields are becoming standard on mid-range trims. Passenger cars, SUVs, and crossovers in particular, are projected to grow at a 5.79% to 2030 and represent the largest incremental glazing surface per unit. Germany and France witnessed significant registrations in 2024, and the body style’s popularity is expected to maintain significant growth in Poland and the Czech Republic in the coming years.

Luxury and sports cars, though lower in volume, drive outsized value by demanding lightweight acoustic laminates and smart sunroofs costing two-to-three times standard glass. Light commercial vehicles (LCVs) rely on durable tempered glass for cargo areas, but are adopting laminated windshields with camera brackets as ADAS becomes mandatory. Medium and heavy commercial vehicles (MHCVs) prioritize direct-vision compliance under UN Regulation No. 167, calling for taller windshields and larger side glazing. Vehicle-type mix shifts toward SUVs and luxury BEVs, boosting the European automotive glass market size for premium panes that bundle coatings, sensors, and smart functions.

By Propulsion: Internal Combustion Engine Dominates, Battery Electric Vehicles Surge

Internal-combustion engines generated 85.79% of demand in 2024, mirroring the installed base across non-premium segments and commercial fleets. These vehicles primarily adopt cost-efficient tempered sidelites and laminated windshields. BEVs are expected to grow at a 9.42% CAGR, aided by EU CO₂ penalties and purchase incentives, and require lightweight acoustic glass to offset battery mass. Saint-Gobain’s double-glazed low-e units reduce HVAC loads significantly, extending range and reinforcing the value proposition. Hybrid electric vehicles strike a balance, integrating selective laminated sidelites to mitigate cabin quietness gaps without breaching cost ceilings.

Fuel-cell vehicles remain marginal but mirror BEV glazing requirements. Norway leads BEV penetration with substantial new registrations in 2024, while Germany, France, and the Netherlands combine infrastructure rollouts with subsidies that accelerate adoption. BEV architectures also favor larger roof openings and HUD-ready windshields to differentiate digital cockpits, driving incremental surface area. As propulsion shifts, the European automotive glass market emphasizes ultra-thin laminated structures with conductive heating and low-emissivity coatings that preserve optical performance.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sales Channel: OEM Dominates, Aftermarket Gains Momentum

OEM channels captured 92.94% revenue in 2024 because glazing decisions are locked during vehicle design and tied to multi-year supply agreements. Tier-one producers operate just-in-time lines adjacent to German, Spanish, and Polish assembly plants, ensuring specification continuity and rapid iteration. The European automotive glass market, therefore, revolves around long-term OEM relationships that bundle R&D support with logistics integration. The aftermarket, though only 7.06% by value, is growing faster at 6.53% due to the rising parc of ADAS-equipped windshields that demand calibrated replacements.

Skilled-labor shortages and specialized equipment needs keep barriers high, enabling certified distributors to command premium pricing. Expansion of OEM-approved networks and mobile calibration vans is improving service coverage, especially in rural France and Italy. Despite OEM dominance, sustained insurance-funded replacement volumes provide an attractive niche for suppliers capable of reproducing factory specifications and offering calibration guarantees.

Geography Analysis

Germany holds 25.53% of 2024 revenue, anchored by Volkswagen Group, BMW, Mercedes-Benz, and Audi. Local production by Saint-Gobain Sekurit, AGC, and NSG ensures short supply chains, while Stuttgart’s emerging smart-glass cluster hosts Gauzy’s second European factory, announced in 2025. German OEMs lead adoption of panoramic sunroofs and HUD-ready windshields, reinforcing high-value mix. Stellantis leverages French plants for laminated acoustic windshields, while Italian SUV programs specify switchable roof glass to bolster premium trims. Spanish assembly lines for SEAT and Ford focus on cost-optimized tempered sidelites, whereas UK premium brands integrate HUD and acoustic laminates to maintain refinement.

Poland is Europe’s fastest riser with a 6.76% CAGR, benefiting from supply-chain localization strategies that place float and laminating capacity closer to Central European assembly hubs. Fuyao expanded regional capacity in 2024, and NSG is commissioning a sputtering line in Sandomierz by 2027. Neighboring Czech Republic and Hungary gain spillover investment due to favorable labor costs and EU funding. This cluster shortens lead times and absorbs logistics shocks for German and French OEMs assembling vehicles in Eastern Europe.

Rest-of-Europe markets display heterogeneous dynamics. Norway’s substantial BEV share drives demand for lightweight acoustic and low-e glazing, while Sweden and the Netherlands prioritize energy-efficient smart glass in line with sustainability mandates. Belgium and the Netherlands progress as logistics hubs supporting aftermarket distribution into Western Europe. As OEMs push smart-glass features into mid-level trims, advanced production is expected to expand toward Benelux and the Nordic states. The regional mosaic ultimately favors suppliers with multi-site footprints that can tailor products to varying propulsion mixes and regulatory nuances.

Competitive Landscape

The Europe automotive glass market centers on five incumbents, Saint-Gobain Sekurit, AGC Inc., NSG Group, Fuyao Glass, and Guardian Industries, that command the majority share through vertically integrated float capacity and proprietary coatings. These players handle rising energy and soda-ash costs while meeting OEM cost-reduction targets. Chinese entrant Fuyao is scaling local production in Hungary and the Czech Republic to hedge tariffs and meet just-in-time delivery needs.

White-space opportunities hinge on reducing smart-glass costs to make electrochromic and SPD technologies accessible to mass-market brands. Gauzy’s dual SPD-PDLC stack, which toggles opacity in under three seconds at low power, exemplifies the innovation premium. Polycarbonate glazing suppliers such as Covestro and Teijin are positioning lightweight alternatives for roof and backlite applications. Regulatory barriers linked to UN R43 laminated requirements and Euro NCAP HUD incentives impede smaller suppliers lacking in-house testing.

Strategic moves highlight technology collaboration. Webasto pairs solar harvesting with switchable roofs to offer energy-positive modules, while AGC’s 2025 IAA Munich showcase featured integrated antenna arrays within windshield coatings. Guardian is investing in low-iron float lines to supply ultra-clear substrates for HUD projection, whereas NSG focuses on sputter-coated low-e laminates for BEVs. Competitive differentiation now revolves around combining coatings, sensors, and electronics into single panes that cut cabin heat load and support autonomous driving.

Europe Automotive Glass Industry Leaders

-

AGC Inc.

-

Saint Gobain

-

Fuyao Group

-

Nippon Sheet Glass Co., Ltd.

-

Xinyi Glass Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: AGC Glass Europe entered a strategic partnership to integrate high-purity recycled cullet from end-of-life solar panels into float-glass production.

- November 2025: Carlex Glass America unveiled plans for a USD 55 million expansion of its advanced manufacturing operations in Davidson County, set to introduce next-generation production lines at its Nashville facility.

- May 2025: AGC Automotive Czech began building a laminated windshield line at its Chudeřice plant to expand capacity and automation.

- January 2025: AGC Glass Europe announced a new insulating vacuum-glass line at its Lodelinsart site, scheduled for 2026 start-up.

Europe Automotive Glass Market Report Scope

The Europe Automotive Glass Market covers the latest trends and technological development and provides analysis on the market demand by Glass Type (Regular Glass (Laminated Glass and Tempered Glass) and Smart Glass (Electrochromic, Suspended Particle Device (SPD), Polymer Dispersed Liquid Crystal (PDLC), and Thermochromic)), Application (Windshield (Front Glass), Backlite (Rear Window), Sidelite (Side Windows), Sunroof (Roof Glass), Rear-view and Side-view Mirrors (Reflective Glass), and Other Glazing (Quarter and Vent Windows)), Vehicle Type (Passenger Cars (Hatchback, Sedan, SUV & Crossover, Luxury & Sports), Light Commercial Vehicles (LCVs), and Medium and Heavy Commercial Vehicles (MHCVs)), Propulsion (Internal Combustion Engine (ICE), Battery Electric Vehicle (BEV), Hybrid Electric Vehicle (HEV/PHEV), and Fuel Cell Electric Vehicle (FCEV)), Sales Channel (OEM and Aftermarket), Country (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), and market share of major automotive glass manufacturing companies in Europe.

By Glass Type

| Regular Glass | Laminated Glass |

| Tempered Glass | |

| Smart Glass | Electrochromic |

| Suspended Particle Device (SPD) | |

| Polymer Dispersed Liquid Crystal (PDLC) | |

| Thermochromic |

By Application

| Windshield |

| Backlite (Rear Window) |

| Sidelite (Side Windows) |

| Sunroof |

| Rear-view and Side-view Mirrors |

| Other Glazing (Quarter and Vent) |

By Vehicle Type

| Passenger Cars | Hatchback |

| Sedan | |

| Sport Utility Vehicle and Crossover | |

| Luxury and Sports | |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles |

By Propulsion

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV/PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

By Sales Channel

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Glass Type | Regular Glass | Laminated Glass |

| Tempered Glass | ||

| Smart Glass | Electrochromic | |

| Suspended Particle Device (SPD) | ||

| Polymer Dispersed Liquid Crystal (PDLC) | ||

| Thermochromic | ||

| By Application | Windshield | |

| Backlite (Rear Window) | ||

| Sidelite (Side Windows) | ||

| Sunroof | ||

| Rear-view and Side-view Mirrors | ||

| Other Glazing (Quarter and Vent) | ||

| By Vehicle Type | Passenger Cars | Hatchback |

| Sedan | ||

| Sport Utility Vehicle and Crossover | ||

| Luxury and Sports | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV/PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Sales Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will the Europe automotive glass market be by 2030?

It is forecasted to reach USD 9.15 billion by 2030, expanding at a 5.45% CAGR.

Which glass type is growing fastest in Europe?

Smart glass, led by electrochromic and SPD variants, is projected to grow at 6.42% a year through 2030.

Why are panoramic sunroofs important for suppliers?

They add up to 2.0 m² of glazing per vehicle, raise unit value, and require advanced interlayers that block infrared heat.

Which country offers the greatest growth opportunity?

Poland shows the highest forecast CAGR at 6.76% as OEMs and suppliers localize production in Central Europe.