| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 182.91 Billion |

| Market Size (2030) | USD 235.01 Billion |

| CAGR (2025 - 2030) | 5.14 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Europe Aerospace and Defense Market Analysis

The Europe Aerospace And Defense Market size is estimated at USD 182.91 billion in 2025, and is expected to reach USD 235.01 billion by 2030, at a CAGR of 5.14% during the forecast period (2025-2030).

The European aerospace and defense landscape is undergoing a profound transformation driven by rapid technological evolution and changing industry dynamics. Companies across the region are heavily investing in cutting-edge innovations spanning artificial intelligence, advanced materials, 3D printing, and autonomous systems. This technological revolution has catalyzed the development of next-generation military aircraft and defense equipment systems, with major players like BAE Systems, Dassault Aviation, and Leonardo SpA leading substantial research and development initiatives. The integration of these advanced technologies has significantly enhanced the capabilities of both manned and unmanned platforms, reflecting the industry's commitment to maintaining technological superiority in an increasingly competitive global market.

The region's manufacturing and supply chain infrastructure is experiencing significant restructuring to enhance resilience and reduce dependencies. European nations are actively developing domestic production capabilities, particularly in critical areas such as semiconductor manufacturing, to address supply chain vulnerabilities. This strategic shift is accompanied by substantial investments in manufacturing facilities and the development of regional supply networks. The industry's focus on supply chain sovereignty is evident in Germany's initiative to increase its production capacity of large-caliber propellants to 1,200 tons annually by 2025, capable of producing 500,000 modular charges.

Aviation in Europe has demonstrated remarkable recovery and modernization momentum, with air passenger traffic reaching 749 million in the first nine months of 2023 across the EU. This resurgence has catalyzed significant fleet modernization initiatives, with commercial aircraft deliveries increasing by 17% to 324 units in 2023. The industry's robust outlook is further reinforced by projected deliveries of approximately 2,600 commercial aircraft between 2024 and 2029, reflecting airlines' commitment to fleet renewal and capacity expansion to meet growing demand while improving operational efficiency and environmental performance.

Defense collaboration across European nations has intensified, marked by significant joint development programs and capability enhancement initiatives. Europe's defense expenditure reached USD 588 billion in 2023, representing a 16% increase from the previous year, demonstrating the region's commitment to military modernization. This collaborative approach is exemplified by programs such as the UK-Poland defense partnership, which includes the development of over 1,000 Common Anti-Air Modular Missiles - Extended Range (CAMM-ER) and more than 100 iLaunchers, highlighting the growing emphasis on joint capability development and interoperability among European armed forces.

Europe Aerospace and Defense Market Trends

Technological Advancements and Demand for Unmanned Systems

The European aerospace and defense market is experiencing a revolutionary shift driven by rapid technological advancements in artificial intelligence (AI), advanced materials, 3D printing, and autonomous systems. Leading companies like BAE Systems, Dassault Aviation, and Leonardo are investing substantially in research and development to usher in next-generation military aircraft capabilities. The persistent R&D in the military sector for autonomous aircraft has driven significant innovations, exemplified by developments like Bell's 407GXi 3-axis autopilot system, which received the UK's Civil Aviation Authority certification in April 2023, offering enhanced stability augmentation and envelope protection features.

The increasing demand for unmanned aerial vehicles (UAVs) represents a major technological evolution in the sector, with various factors such as the need for efficient surveillance and advancements in artificial intelligence and sensor technologies driving adoption. For instance, in February 2024, the UK announced plans to spend an additional USD 5.7 billion over the next decade on new military drones, focusing on naval mine clearance, one-way attack, heavy lift, and ISR capabilities. Similarly, in October 2023, Germany awarded Rheinmetall a USD 210 million contract to deliver real-time reconnaissance unmanned aerial vehicles to the German Army, demonstrating the growing emphasis on unmanned capabilities across European defense forces.

Understand The Key Trends Shaping This Market

Download PDF

Defense Budget Boosts and Geopolitical Tensions

European defense budgets have witnessed substantial increases, reflecting the region's commitment to strengthening military capabilities and addressing emerging security challenges. For instance, in February 2024, France announced a significant increase in its budget for the armed forces, allocating USD 449 billion from 2024 to 2030, representing a substantial 40% increase compared to the previous period. This surge in defense spending has catalyzed major procurement initiatives, such as France's DPA ordering various weapon systems, including self-propelled howitzers and armored vehicles, for USD 1.2 billion, with notable purchases including 109 new-generation Caesar truck-mounted howitzers from Nexter Systems for approximately USD 380 million.

The evolving geopolitical landscape has prompted increased focus on strategic partnerships and defense modernization programs. In January 2024, NATO's Support and Procurement Agency announced its commitment to assisting a coalition of partner countries, including Germany, the Netherlands, Romania, and Spain, in procuring up to 1,000 Patriot missiles to reinforce their air defense systems capabilities. This initiative, valued at USD 5.5 billion, will facilitate the growth of missile production in Europe while improving availability and guaranteeing the replenishment of allied stockpiles. Additionally, major naval modernization efforts are underway, as evidenced by the British Royal Navy's May 2024 announcement to acquire up to six new multirole support ships and enhance its future frigates with land-attack capabilities, demonstrating the comprehensive nature of defense capability enhancement across the region.

Segment Analysis: Industry

Manufacturing, Design and Engineering Segment in Europe Aerospace and Defense Market

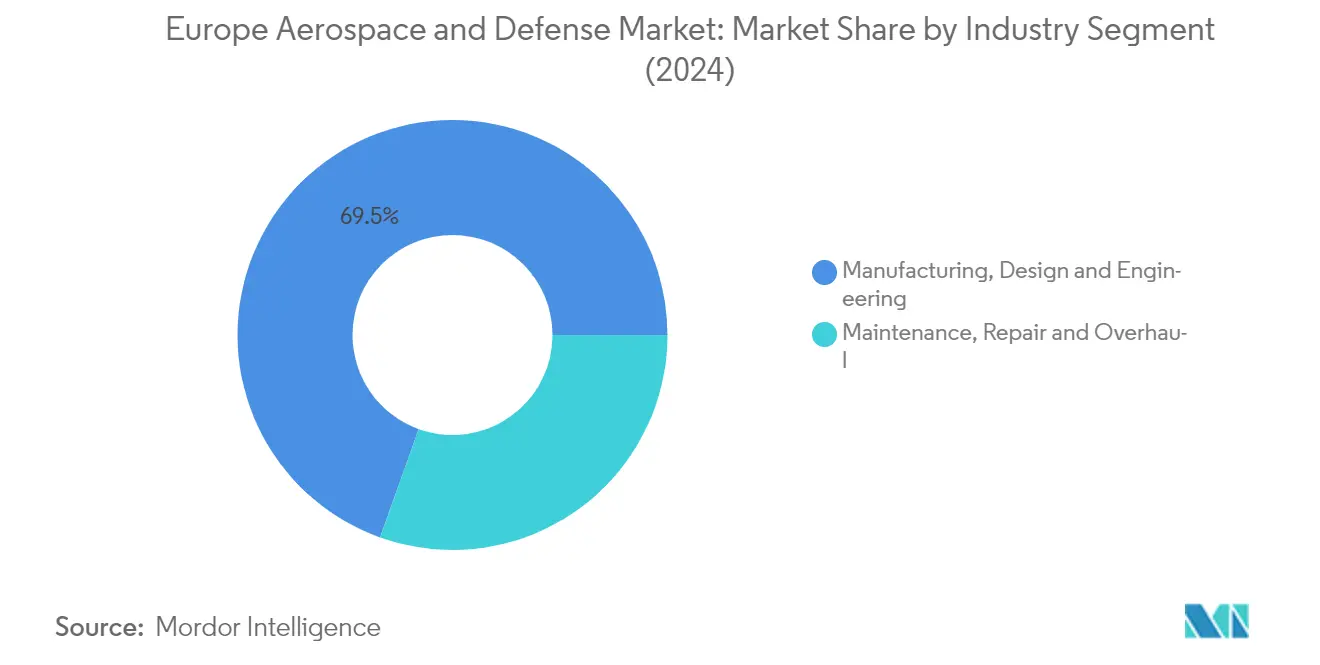

The Manufacturing, Design, and Engineering segment dominates the European aerospace and defense market, commanding approximately 70% of the market share in 2024. This segment's prominence is driven by robust increases in defense budgets, including a substantial boost intended to enhance military capabilities, modernize defense infrastructure, and foster innovation in advanced defense technologies and manufacturing processes. The Act in Support of Ammunition Production (ASAP) has significantly boosted this segment by allocating USD 544.02 million to build up ammunition production capacity to 2 million shells per year by the end of 2025. European defense manufacturers are deeply investing in advanced technologies to stay competitive and deliver state-of-the-art solutions to the armed forces, particularly triggered by the ongoing Russia-Ukraine war. The European Defense Industry, through the Common Procurement (EDIRPA) Work Programme's USD 336.92 million budget, further incentivizes joint procurement, aggregating demand and providing predictability, which encourages manufacturers to scale up production capacities and enhances interoperability.

Maintenance, Repair and Overhaul Segment in Europe Aerospace and Defense Market

The Maintenance, Repair, and Overhaul (MRO) segment plays a crucial role in sustaining and extending the operational life of aerospace and defense equipment across Europe. This segment has been experiencing steady growth driven by aging military equipment in many European nations requiring extensive maintenance, upgrades, and replacement. Strategic partnerships and alliances between airlines, MRO service providers, and OEMs have enhanced the capabilities and reach of the MRO market. For instance, in April 2024, Safran Nacelles and Lufthansa Technik signed a significant license agreement for MRO services for the LEAP-1A nacelles of the Airbus A320neo, bringing together their extensive experience to maintain the highest level of reliability and performance. The segment's growth is further supported by the increasing focus on in-country MRO services implementation strategy, as this approach leads to more operational efficiency and rapid deployment capabilities. The integration of aerospace maintenance strategies has become pivotal in ensuring the longevity and reliability of critical aerospace components.

Segment Analysis: By Sector

Defense Segment in Europe Aerospace and Defense Market

The defense segment maintains its dominant position in the European aerospace and defense market, commanding approximately 49% of the total market share in 2024. This substantial market presence is driven by increased defense spending across European nations, particularly in response to evolving geopolitical tensions. Major European countries have significantly boosted their defense budgets, with many NATO members committing to reach the 2% of GDP spending target. The segment's strength is further reinforced by extensive modernization programs across land, air, and naval domains, including the procurement of next-generation fighter aircraft, advanced naval vessels, and ground combat systems. The defense sector's robust performance is also supported by significant investments in research and development, focusing on emerging technologies like artificial intelligence, cybersecurity, and autonomous systems. The integration of advanced missile systems and military logistics solutions further enhances the segment's capabilities.

Unmanned Vehicles Segment in Europe Aerospace and Defense Market

The unmanned vehicles segment is experiencing remarkable growth, projected to expand at approximately 12% CAGR from 2024 to 2029. This exceptional growth is primarily driven by the increasing adoption of unmanned aerial vehicles (UAVs) for both military and commercial applications. The segment's expansion is fueled by technological advancements in autonomous systems, artificial intelligence, and sensor technologies. Military forces across Europe are increasingly incorporating unmanned systems for surveillance, reconnaissance, and combat missions, while commercial sectors are adopting UAVs for applications ranging from agriculture to infrastructure inspection. The development of sophisticated unmanned ground vehicles (UGVs) and unmanned maritime vehicles (UMVs) is further contributing to the segment's growth, particularly in areas such as battlefield logistics, mine countermeasures, and maritime patrol operations. The integration of avionics and aerospace propulsion technologies is critical in advancing the capabilities of these unmanned systems.

Remaining Segments in Europe Aerospace and Defense Market

The aerospace segment represents another crucial component of the market, encompassing both commercial aviation and space sectors. This segment is experiencing significant developments in commercial aircraft manufacturing, maintenance, repair, and overhaul (MRO) services, and space exploration initiatives. The commercial aviation sector is witnessing a strong recovery in air travel demand, driving new aircraft orders and fleet modernization programs. Meanwhile, the space sector is gaining momentum through increased investments in satellite technology, space exploration missions, and commercial space services. The segment's growth is further supported by innovations in sustainable aviation technologies, including electric propulsion systems and advanced materials, reflecting the industry's commitment to environmental sustainability. The focus on commercial aerospace advancements is pivotal in driving the sector's growth.

Europe Aerospace And Defense Market Geography Segment Analysis

Europe Aerospace and Defense Market

The European aerospace and defense market demonstrates significant diversity across its major economies, with each country contributing unique capabilities and strategic priorities. The market is characterized by strong research and development initiatives, particularly in unmanned systems and advanced military aircraft technologies. Key players in the region include the United Kingdom, Germany, France, Russia, Italy, and Spain, each maintaining distinct specializations within the aerospace and defense sectors. The region's market dynamics are heavily influenced by ongoing geopolitical developments, defense modernization programs, and an increasing focus on indigenous manufacturing capabilities. European nations are actively pursuing collaborative defense projects while simultaneously developing their domestic defense equipment industrial bases.

Europe Aerospace and Defense Market in Russia

Russia maintains its position as the dominant force in the European aerospace and defense market, with its extensive military modernization programs and robust domestic defense industrial base. The country's aerospace sector encompasses a wide range of capabilities, from commercial aviation to military aviation production. Despite international challenges, Russia continues to invest heavily in developing advanced military technologies and maintaining its strategic defense capabilities. The country holds approximately 26% of the European aerospace and defense market share in 2024, reflecting its significant influence in the region. Russia's defense industry particularly excels in areas such as combat aircraft, air defense systems, and naval defense vessels, supported by a network of state-owned and private defense manufacturers.

Europe Aerospace and Defense Market in Germany

Germany emerges as the region's fastest-growing market with a projected growth rate of approximately 7% during 2024-2029, driven by significant increases in defense spending and modernization initiatives. The country's aerospace and defense sector is characterized by its strong focus on technological innovation and international collaboration. Germany's growth is supported by major procurement programs across all military branches, including the acquisition of new fighter aircraft, naval vessels, and land systems. The country's commitment to meeting NATO defense spending targets has resulted in increased investments in military capabilities and defense research. German industries are particularly strong in areas such as land systems, naval technologies, and aerospace components, with a growing focus on unmanned systems and cyber defense capabilities.

Get Analysis on Important Geographic Markets

Download PDF

Europe Aerospace and Defense Industry Overview

Top Companies in Europe Aerospace and Defense Market

The European aerospace and defense market is characterized by continuous innovation and strategic evolution among its key players. Companies are heavily investing in advanced technologies like unmanned systems, cybersecurity for defense solutions, and next-generation aircraft platforms to maintain competitive advantages. Operational agility has become paramount, with manufacturers adopting flexible production systems and digitalized processes to respond quickly to changing market demands. Strategic partnerships and collaborations, particularly in areas like space exploration and defense systems development, have emerged as crucial growth drivers. Market leaders are expanding their geographical footprint through targeted acquisitions and joint ventures, while simultaneously strengthening their core capabilities in areas such as electronic warfare, missile systems, and commercial aviation. The industry's competitive dynamics are further shaped by an increasing focus on sustainable technologies and green aviation solutions, pushing companies to invest in eco-friendly propulsion systems and materials.

Market Structure Reflects Strategic Industry Evolution

The European aerospace and defense market exhibits a complex competitive structure dominated by both large multinational conglomerates and specialized regional players. Major conglomerates leverage their diverse product portfolios and extensive research capabilities to maintain market leadership, while specialized firms carve out niches in specific technological domains or regional markets. The market shows moderate consolidation, with established players maintaining strong positions through their technological expertise and long-standing relationships with government clients. Cross-border collaborations and joint development programs have become increasingly common, particularly in major defense projects and technology for space initiatives, fostering a more integrated European defense industrial base.

The industry landscape is continuously evolving through strategic mergers and acquisitions aimed at acquiring critical technologies and expanding market reach. Companies are increasingly focusing on vertical integration to secure supply chains and enhance operational efficiency. The market structure is further influenced by government policies promoting domestic defense capabilities while encouraging European cooperation. Regional clusters of excellence have emerged, particularly in countries with strong aerospace traditions, creating ecosystems of prime contractors, specialized suppliers, and research institutions working in close collaboration.

Innovation and Adaptability Drive Future Success

Success in the European aerospace and defense market increasingly depends on companies' ability to innovate while maintaining operational efficiency. Incumbent players are strengthening their positions through increased investment in research and development, focusing on emerging technologies like artificial intelligence, autonomous systems, and advanced materials. Market leaders are also expanding their service offerings, moving beyond traditional manufacturing to provide integrated solutions and lifecycle support. Building strong relationships with government clients while diversifying into commercial markets has become crucial for sustainable growth. Companies are also focusing on developing robust supply chain networks and establishing strategic partnerships to enhance their competitive position.

For emerging players and contenders, success lies in identifying and exploiting niche market opportunities while building technological expertise. The ability to offer specialized solutions in areas like cybersecurity, electronics for defense, or unmanned systems provides pathways for market entry and growth. Regulatory compliance and certification capabilities are becoming increasingly important success factors, particularly in light of evolving safety and environmental standards. The industry's high barriers to entry, including substantial capital requirements and complex regulatory frameworks, necessitate careful strategic planning and long-term commitment from new entrants. Companies must also consider the increasing emphasis on environmental sustainability and digital transformation in their strategic planning.

Europe Aerospace and Defense Market Leaders

-

Airbus SE

-

BAE Systems plc

-

Leonardo S.p.A.

-

Safran SA

-

THALES

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Europe Aerospace and Defense Market News

February 2024: France’s Defense Procurement Agency announced the procurement of self-propelled howitzers, armored vehicles, and helicopters valued at more than USD 1.2 billion as part of the nation's military modernization initiative, which will continue until 2030.

December 2023: EasyJet contracted Airbus to deliver 157 more A320neo aircraft and 100 purchase rights. The contract was signed to replace its aging fleet of A319 aircraft and approximately half of its A320ceo aircraft.

Europe Aerospace and Defense Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET SEGMENTATION

-

4.1 Commercial and General Aviation

- 4.1.1 Market Overview

- 4.1.2 Market Dynamics

- 4.1.2.1 Drivers

- 4.1.2.2 Restraints

- 4.1.2.3 Opportunities

- 4.1.3 Market Trends

- 4.1.4 Commercial Aircraft

- 4.1.4.1 Air Traffic

- 4.1.4.2 Training and Flight Simulators

- 4.1.4.3 Airport Services (Ground Support Equipment and Logistics)

- 4.1.4.4 Structures

- 4.1.4.4.1 Airframe

- 4.1.4.4.1.1 Materials (Composite, Metal and Metal Alloys, Other Materials)

- 4.1.4.4.1.2 Adhesives and Coatings

- 4.1.4.4.2 Engine and Engine Systems

- 4.1.4.4.3 Cabin Interiors

- 4.1.4.4.4 Landing Gear

- 4.1.4.4.5 Avionics and Control Systems

- 4.1.4.4.5.1 Communication System

- 4.1.4.4.5.2 Navigation System

- 4.1.4.4.5.3 Flight Control System

- 4.1.4.4.5.4 Health Monitoring System

- 4.1.4.4.6 Electrical Systems

- 4.1.4.4.7 Environmental Control Systems

- 4.1.4.4.8 Fuel and Fuel Systems

- 4.1.4.4.9 MRO

- 4.1.4.4.10 Research and Development

- 4.1.4.4.11 Supply Chain Analysis (Design, Raw Materials, Manufacturing, Assembly, Testing, and Certification)

- 4.1.4.4.12 Competitor Analysis

- 4.1.5 General Aviation (Includes Business Jets, Helicopter, and Personal Aircraft)

- 4.1.5.1 Air Traffic

- 4.1.5.2 Training and Flight Simulators

- 4.1.5.3 Airport Services (Ground Support Equipment and Logistics)

- 4.1.5.4 Structures

- 4.1.5.4.1 Airframe

- 4.1.5.4.1.1 Materials (Composite, Metal and Metal Alloys, Other Materials)

- 4.1.5.4.1.2 Adhesives and Coatings

- 4.1.5.4.2 Engine and Engine Systems

- 4.1.5.4.3 Cabin Interiors

- 4.1.5.4.4 Landing Gear

- 4.1.5.4.5 Avionics and Control Systems

- 4.1.5.4.5.1 Communication System

- 4.1.5.4.5.2 Navigation System

- 4.1.5.4.5.3 Flight Control System

- 4.1.5.4.5.4 Health Monitoring System

- 4.1.5.4.6 Electrical Systems

- 4.1.5.4.7 Environmental Control Systems

- 4.1.5.4.8 Fuel and Fuel Systems

- 4.1.5.4.9 MRO

- 4.1.5.4.10 Research and Development

- 4.1.5.4.11 Supply Chain Analysis

- 4.1.5.4.12 Competitor Analysis

-

4.2 Military Aircraft and Systems

- 4.2.1 Market Overview

- 4.2.2 Defense Spending and Budget Allocation Details

- 4.2.2.1 Army

- 4.2.2.2 Navy and Marine Corps

- 4.2.2.3 Air Force

- 4.2.3 Market Dynamics

- 4.2.3.1 Drivers

- 4.2.3.2 Restraints

- 4.2.3.3 Opportunities

- 4.2.4 Market Trends

- 4.2.5 MRO

- 4.2.6 Research and Development

- 4.2.7 Training and Flight Simulators

- 4.2.8 Competitor Analysis

- 4.2.9 Supply Chain Analysis

- 4.2.10 Customer/Distributor Information

- 4.2.11 Combat Aircraft

- 4.2.11.1 Structures

- 4.2.11.1.1 Airframe

- 4.2.11.1.1.1 Materials (Composite, Metal and Metal Alloys, Other Materials)

- 4.2.11.1.1.2 Adhesives and Coatings

- 4.2.11.1.2 Engine and Engine Systems

- 4.2.11.1.3 Landing Gear

- 4.2.11.2 Avionics and Control Systems

- 4.2.11.2.1 General Avionics

- 4.2.11.2.2 Mission Specific Avionics

- 4.2.11.3 Missiles and Weapons

- 4.2.12 Non-combat Aircraft

- 4.2.12.1 Structures

- 4.2.12.1.1 Airframe

- 4.2.12.1.1.1 Materials (Composite, Metal and Metal Alloys, Other Materials)

- 4.2.12.1.1.2 Adhesives and Coatings

- 4.2.12.1.2 Engine and Engine Systems

- 4.2.12.1.3 Landing Gear

- 4.2.12.2 Avionics and Control Systems

- 4.2.12.2.1 General Avionics

- 4.2.12.2.2 Mission-specific Avionics

- 4.2.12.3 Missiles and Weapons

-

4.3 Unmanned Aerial Systems

- 4.3.1 Market Overview

- 4.3.2 Market Dynamics

- 4.3.2.1 Drivers

- 4.3.2.2 Restraints

- 4.3.2.3 Opportunities

- 4.3.3 Market Trends

- 4.3.4 Research and Development

- 4.3.5 Competitor Analysis

- 4.3.6 Regulatory Landscape and Future Policy Changes

- 4.3.7 Segmentation

- 4.3.7.1 Commercial

- 4.3.7.2 Military

-

4.4 Space Systems and Equipment

- 4.4.1 Market Overview

- 4.4.2 Market Dynamics

- 4.4.2.1 Drivers

- 4.4.2.2 Restraints

- 4.4.2.3 Opportunities

- 4.4.3 Market Trends

- 4.4.4 Research and Development

- 4.4.5 Competitor Analysis

- 4.4.6 Regulatory Landscape and Future Policy Changes

- 4.4.7 Customer Information

- 4.4.8 Segmentation: Space Launch Vehicle, Spacecraft, and Ground Systems

- 4.4.9 Segmentation: Satellites

- 4.4.9.1 By Subsystem

- 4.4.9.1.1 Command and Control System

- 4.4.9.1.2 Telemetry, Tracking, Commanding, and Monitoring (TTCM)

- 4.4.9.1.3 Antenna System

- 4.4.9.1.4 Transponders

- 4.4.9.1.5 Power System

- 4.4.9.2 By Application

- 4.4.9.2.1 Military

- 4.4.9.2.2 Commercial

-

4.5 Geography

- 4.5.1 United Kingdom

- 4.5.2 France

- 4.5.3 Germany

- 4.5.4 Italy

- 4.5.5 Spain

- 4.5.6 Rest of Europe

5. COMPETITIVE LANDSCAPE

- 5.1 Vendor Market Share

-

5.2 Company Profiles*

- 5.2.1 Airbus SE

- 5.2.2 BAE Systems PLC

- 5.2.3 Dassault Aviation SA

- 5.2.4 Fincantieri SpA

- 5.2.5 GKN Aerospace

- 5.2.6 Leonardo SpA

- 5.2.7 Naval Group

- 5.2.8 QinetiQ Group PLC

- 5.2.9 Rheinmetall AG

- 5.2.10 Rolls-Royce PLC

- 5.2.11 Rostec

- 5.2.12 Safran SA

- 5.2.13 THALES

- 5.2.14 Lockheed Martin Corporation

6. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Europe Aerospace and Defense Industry Segmentation

The European aerospace and defense market includes the design and manufacture of aircraft, rockets, missiles, and spacecraft that operate in space. Defense equipment refers to weapons, arms, and equipment used for military purposes. The study conducted in this report provides an in-depth analysis of the European aerospace and defense market.

The European aerospace and defense market is segmented by commercial and general aviation, military aircraft and systems, unmanned aerial systems, and space systems and equipment. The report also offers the market sizes and forecasts for five countries across the region. For each segment, the report offers market sizing and forecasts in value (USD) terms.

| Commercial and General Aviation | Market Overview | ||||

| Market Dynamics | Drivers | ||||

| Restraints | |||||

| Opportunities | |||||

| Market Trends | |||||

| Commercial Aircraft | Air Traffic | ||||

| Training and Flight Simulators | |||||

| Airport Services (Ground Support Equipment and Logistics) | |||||

| Structures | Airframe | Materials (Composite, Metal and Metal Alloys, Other Materials) | |||

| Adhesives and Coatings | |||||

| Engine and Engine Systems | |||||

| Cabin Interiors | |||||

| Landing Gear | |||||

| Avionics and Control Systems | Communication System | ||||

| Navigation System | |||||

| Flight Control System | |||||

| Health Monitoring System | |||||

| Electrical Systems | |||||

| Environmental Control Systems | |||||

| Fuel and Fuel Systems | |||||

| MRO | |||||

| Research and Development | |||||

| Supply Chain Analysis (Design, Raw Materials, Manufacturing, Assembly, Testing, and Certification) | |||||

| Competitor Analysis | |||||

| General Aviation (Includes Business Jets, Helicopter, and Personal Aircraft) | Air Traffic | ||||

| Training and Flight Simulators | |||||

| Airport Services (Ground Support Equipment and Logistics) | |||||

| Materials (Composite, Metal and Metal Alloys, Other Materials) | |||||

| Adhesives and Coatings | |||||

| Engine and Engine Systems | |||||

| Cabin Interiors | |||||

| Landing Gear | |||||

| Communication System | |||||

| Navigation System | |||||

| Flight Control System | |||||

| Health Monitoring System | |||||

| Electrical Systems | |||||

| Environmental Control Systems | |||||

| Fuel and Fuel Systems | |||||

| MRO | |||||

| Research and Development | |||||

| Supply Chain Analysis | |||||

| Competitor Analysis | |||||

| Military Aircraft and Systems | Market Overview | ||||

| Defense Spending and Budget Allocation Details | Army | ||||

| Navy and Marine Corps | |||||

| Air Force | |||||

| Drivers | |||||

| Restraints | |||||

| Opportunities | |||||

| Market Trends | |||||

| MRO | |||||

| Research and Development | |||||

| Training and Flight Simulators | |||||

| Competitor Analysis | |||||

| Supply Chain Analysis | |||||

| Customer/Distributor Information | |||||

| Combat Aircraft | Structures | Airframe | Materials (Composite, Metal and Metal Alloys, Other Materials) | ||

| Adhesives and Coatings | |||||

| Engine and Engine Systems | |||||

| Landing Gear | |||||

| Avionics and Control Systems | General Avionics | ||||

| Mission Specific Avionics | |||||

| Missiles and Weapons | |||||

| Non-combat Aircraft | Structures | Airframe | Materials (Composite, Metal and Metal Alloys, Other Materials) | ||

| Adhesives and Coatings | |||||

| Engine and Engine Systems | |||||

| Landing Gear | |||||

| Avionics and Control Systems | General Avionics | ||||

| Mission-specific Avionics | |||||

| Missiles and Weapons | |||||

| Unmanned Aerial Systems | Market Overview | ||||

| Drivers | |||||

| Restraints | |||||

| Opportunities | |||||

| Market Trends | |||||

| Research and Development | |||||

| Competitor Analysis | |||||

| Regulatory Landscape and Future Policy Changes | |||||

| Segmentation | Commercial | ||||

| Military | |||||

| Space Systems and Equipment | Market Overview | ||||

| Drivers | |||||

| Restraints | |||||

| Opportunities | |||||

| Market Trends | |||||

| Research and Development | |||||

| Competitor Analysis | |||||

| Regulatory Landscape and Future Policy Changes | |||||

| Customer Information | |||||

| Segmentation: Space Launch Vehicle, Spacecraft, and Ground Systems | |||||

| Segmentation: Satellites | By Subsystem | Command and Control System | |||

| Telemetry, Tracking, Commanding, and Monitoring (TTCM) | |||||

| Antenna System | |||||

| Transponders | |||||

| Power System | |||||

| By Application | Military | ||||

| Commercial | |||||

| Geography | United Kingdom | ||||

| France | |||||

| Germany | |||||

| Italy | |||||

| Spain | |||||

| Rest of Europe | |||||

Need A Different Region or Segment?

Customize Now

Europe Aerospace and Defense Market Research FAQs

How big is the Europe Aerospace And Defense Market?

The Europe Aerospace And Defense Market size is expected to reach USD 182.91 billion in 2025 and grow at a CAGR of 5.14% to reach USD 235.01 billion by 2030.

What is the current Europe Aerospace And Defense Market size?

In 2025, the Europe Aerospace And Defense Market size is expected to reach USD 182.91 billion.

Who are the key players in Europe Aerospace And Defense Market?

Airbus SE, BAE Systems plc, Leonardo S.p.A., Safran SA and THALES are the major companies operating in the Europe Aerospace And Defense Market.

What years does this Europe Aerospace And Defense Market cover, and what was the market size in 2024?

In 2024, the Europe Aerospace And Defense Market size was estimated at USD 173.51 billion. The report covers the Europe Aerospace And Defense Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Aerospace And Defense Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Europe Aerospace And Defense Market Research

Mordor Intelligence provides a comprehensive analysis of the aerospace & defense industry. Our expertise spans commercial aerospace, military aviation, and space technology sectors. The research covers the entire spectrum of aerospace and defence systems, including military aircraft, commercial aircraft, and unmanned aerial system technologies. We analyze critical areas such as avionics, aerospace propulsion, aerospace components, and defense electronics. This provides detailed insights into both civil aerospace and military aerospace segments.

Our detailed report, available as an easy-to-download PDF, offers stakeholders valuable insights into developments in air defense system, military radar technologies, and missile systems advancements. The research examines crucial aspects of defense cybersecurity, military logistics, and military communication systems. It also covers innovations in satellite system and practices in aerospace maintenance. The analysis extends to military vehicle technologies, naval defense capabilities, and defense equipment specifications, supported by comprehensive defense simulation data. Stakeholders benefit from our thorough examination of space defense initiatives and aerospace components, enabling informed decision-making in this dynamic sector.