| Study Period | 2017 - 2028 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2028 |

| Market Size (2024) | USD 6.15 Billion |

| Market Size (2028) | USD 7.74 Billion |

| CAGR (2024 - 2028) | 5.95 % |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Epoxy Adhesive Market Analysis

The Epoxy Adhesive Market size is estimated at 6.15 billion USD in 2024, and is expected to reach 7.74 billion USD by 2028, growing at a CAGR of 5.95% during the forecast period (2024-2028).

The epoxy adhesives industry is experiencing significant transformation driven by broader technological advancements and sustainability initiatives. Manufacturers are increasingly focusing on developing eco-friendly formulations with reduced volatile organic compound (VOC) emissions, responding to stringent environmental regulations and growing consumer awareness. The integration of smart manufacturing processes and automation in production facilities has enhanced operational efficiency and product consistency. Recent innovations include the development of hybrid adhesive solutions that combine the strengths of different adhesive technologies, offering improved performance characteristics for specialized applications.

The industry is witnessing a notable shift towards sustainable development practices, particularly in construction applications where epoxy adhesives play a crucial role. The global construction industry is projected to grow at 3.5% per annum up to 2030, with China, India, the United States, and Indonesia collectively accounting for 58.3% of the overall construction growth globally. This growth is accompanied by increasing emphasis on green building practices and sustainable construction materials, driving innovation in eco-friendly epoxy adhesive formulations. Manufacturers are investing in research and development to create bio-based alternatives and recyclable adhesive solutions that maintain the high-performance characteristics of traditional epoxy adhesives.

The rapid evolution of electronic devices and components has created new opportunities and challenges for epoxy adhesive manufacturers. The global electronics and household appliances industries are expected to grow at CAGRs of 2.51% and 5.77%, respectively, driving demand for specialized electronic adhesives solutions. Advanced formulations are being developed to meet the increasing requirements for thermal conductivity, electrical insulation, and miniaturization in electronic applications. These developments are particularly relevant in the context of emerging technologies such as 5G infrastructure, Internet of Things (IoT) devices, and advanced semiconductor packaging.

The electrification trend in transportation is creating new opportunities for epoxy adhesive innovations. With the electric vehicle segment projected to grow at a CAGR of 17.75% globally, manufacturers are developing specialized adhesive solutions optimized for EV battery assembly, thermal management systems, and lightweight structural components. This has led to the emergence of new epoxy resin formulations designed specifically for battery cell bonding, thermal interface materials, and structural reinforcement in electric vehicles. Recent developments include advanced curing systems that enable faster production cycles and improved bond strength for composite materials commonly used in electric vehicle manufacturing.

Global Epoxy Adhesive Market Trends

Favorable government policies to promote electric vehicles will propel automotive industry

- Since 2021, the global automotive industry has been expected to grow steadily but at a slower pace because of the decline in consumers' preferences for individual ownership of passenger vehicles and their increased preference for shared mobility in transportation. The global automotive industry is expected to experience a growth rate of 2% annually, with an expected value addition of USD 1.5 trillion in total revenue during the forecast period.

- In 2020, due to the impact of the COVID-19 pandemic, vehicle sales declined but recovered rapidly in 2021 because the governments of various countries took measures to support their economies, as automotive markets usually contribute majorly to their GDP. Vehicle sales declined from 90 million units of passenger vehicles in 2019 to 78 million units in 2020.

- The introduction of electric vehicles worldwide has contributed significantly to the overall revenue of the global automotive market because of their cheaper energy costs, environmentally benign nature, and efficient mobility features. Various government policies and standards also work as driving factors to increase EV production. For instance, the EU standards for CO2 emissions increased the demand for electric vehicles in 2021. As per the IEA's Sustainable Scenario, 230 million electric vehicles are required to replace combustion fuel-based vehicles by 2030. In 2021, Tesla, the largest EV manufacturer, recorded a rise of 157% in the number of electric vehicles manufactured. This growing trend of consumers preferring electric vehicles is expected to rise further during the forecast period (2022-2028).

Understand The Key Trends Shaping This Market

Download PDF

Growing residential and infrastructural development to thrive the construction sector

- The building and construction industry witnessed steady growth, with a CAGR of 2.6% from 2017 to 2019. This growth was driven by the upswing in global economic activity and increasing demand for single-family homes. In 2020, the COVID-19 pandemic had a major impact on the global building and construction industry. Constraints in labor supply, disruptions in construction finances and the supply chain, and economic uncertainty negatively impacted the global building and construction industry.

- Though the industry showed positive growth in 2021, the pandemic's effect on supply chains, which resulted in a hike in raw material prices, is still plaguing the industry. However, as the construction industry heavily influences a nation's economy, countries in Europe, North America, and Asia-Pacific have used the construction industry to restart their economic cycles by offering support schemes. Some support schemes include the Homebuilder Programme in Australia and the economic recovery plan of EU countries.

- The Asia-Pacific region experiences the highest volume of construction activities, and it is expected to remain the largest construction market till 2028 due to its huge population, increasing urbanization, and increasing investments in infrastructural development in countries like China, India, Japan, Indonesia, and South Korea.

- Increasing emphasis on green buildings and efforts to reduce emissions from global construction activities are expected to result in more sustainable operational procedures during the forecast period. For example, France has sanctioned EUR 7.5 billion for the construction industry to transform itself into a low-carbon energy economy.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Rapid growth of civil and military aviation will boost the aircraft production

- Fast paced growth of e-commerce industry in developing nations to augment the industry

- Easy availability of resources will support the footwear industry specifically in developing countries

- Rising demand for home & office furniture to aid the growth of the industry

Segment Analysis: End User Industry

Automotive Segment in Epoxy Adhesives Market

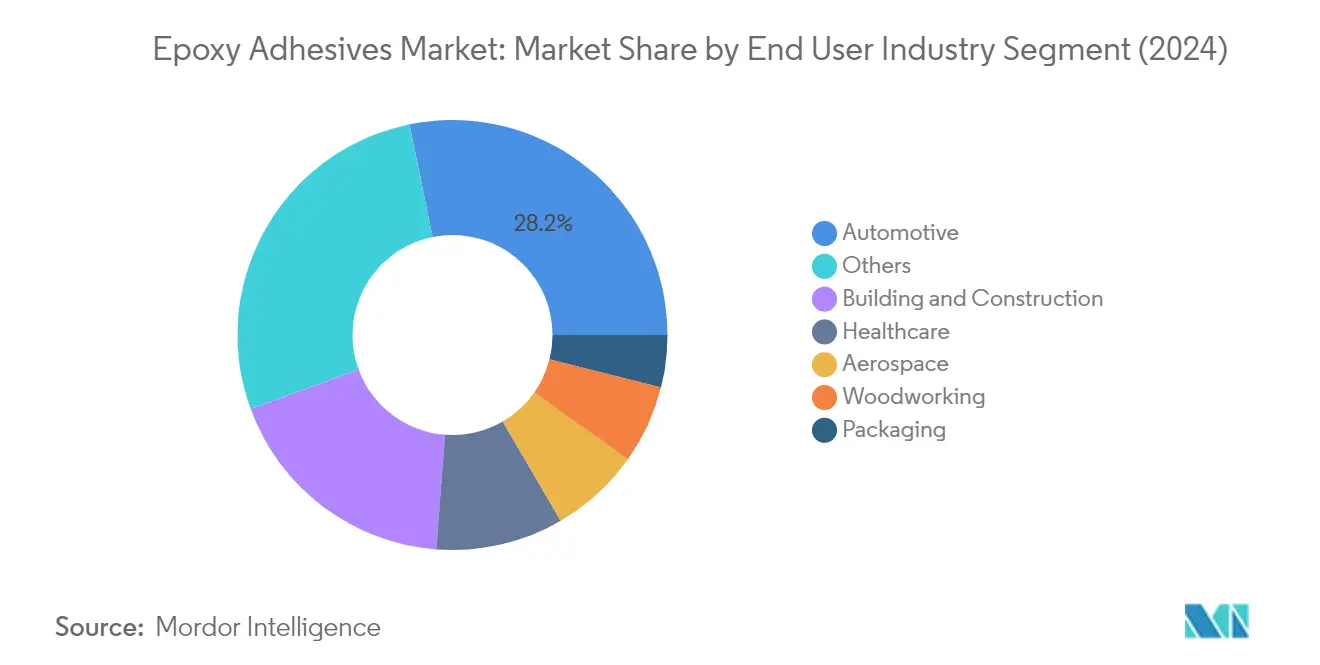

The automotive segment continues to dominate the global epoxy adhesives market, holding approximately 28% market share in 2024. This significant market position is primarily driven by the increasing adoption of epoxy adhesives as replacements for traditional mechanical fasteners in vehicle assembly operations. The automotive industry's shift toward electric vehicles has further boosted the demand for epoxy adhesives, as these materials play a crucial role in battery assembly and lightweight construction. Industrial epoxy adhesives are extensively used in structural bonding applications within the automotive sector, offering high tensile strength properties of approximately 35-41 N/mm2, which is the highest among other adhesive types. These adhesives are crucial in joining seats, tailgate spoilers, side skirts, bumpers, headlights, and dashboards, contributing to both structural integrity and weight reduction in modern vehicles.

Healthcare Segment in Epoxy Adhesives Market

The healthcare segment is emerging as the fastest-growing segment in the epoxy adhesives market, projected to grow at approximately 7% CAGR from 2024 to 2029. This remarkable growth is primarily attributed to the increasing adoption of epoxy adhesives in medical device manufacturing and assembly processes. Medical-grade epoxy adhesives, being 100% solid and containing no solvents, are particularly favored in healthcare applications due to their non-toxic nature and high bond strength. These adhesives are extensively used in manufacturing endoscopes, catheters, atherectomy devices, blood heat exchangers, syringes, and various surgical and orthopedic instruments. The segment's growth is further supported by the rising demand for disposable medical devices and the increasing focus on developing biocompatible adhesive solutions for medical applications.

Remaining Segments in End User Industry

The epoxy adhesives market encompasses several other significant segments including building and construction, aerospace, woodworking and joinery, and packaging industries. The building and construction segment maintains a strong presence due to the extensive use of structural adhesives in flooring, structural bonding, and repair applications. The aerospace segment utilizes composite adhesives for critical structural components and composite bonding applications, while the woodworking and joinery segment relies on these adhesives for furniture manufacturing and structural wood applications. The packaging segment, though smaller, plays a vital role in specialized applications requiring high bond strength and chemical resistance. Each of these segments contributes uniquely to the market's diversity and overall growth, driven by specific industry requirements and technological advancements in adhesive formulations.

Segment Analysis: Technology

Reactive Segment in Epoxy Adhesives Market

The reactive technology segment dominates the global epoxy adhesives market, holding approximately 63% market share in 2024. This significant market position is attributed to reactive epoxy adhesives' superior performance characteristics, including high bond strength and chemical resistance. These adhesives are extensively utilized in automotive manufacturing for structural bonding applications, effectively replacing traditional mechanical fasteners. The segment's dominance is further strengthened by its widespread adoption in aerospace applications, where these adhesives are crucial for bonding structural components. Reactive epoxy adhesives demonstrate exceptional versatility across various substrates including metals, plastics, wood, ceramics, and glass, making them indispensable in industrial applications. The technology's ability to cure at room temperatures and provide long-lasting, permanent resilience and temperature resistance has made it particularly valuable in the production of sensitive electrical parts and components in the automotive industry.

UV Cured Segment in Epoxy Adhesives Market

The UV cured technology segment is emerging as the fastest-growing segment in the epoxy adhesives market for the period 2024-2029. This growth is primarily driven by the increasing adoption of UV cured epoxy adhesives in high-precision applications within the aerospace and electronics industries. The segment's rapid expansion is attributed to several advantageous properties, including faster curing times, high viscosity of up to 17 Pa.s, and superior performance across a broad temperature range. UV cured epoxy adhesives are gaining significant traction in the electronics manufacturing sector, particularly in applications requiring precise bonding and rapid production cycles. The technology's ability to provide instant curing, coupled with its excellent adhesion properties and environmental benefits, has made it increasingly attractive to manufacturers seeking to optimize their production processes and reduce operational costs.

Remaining Segments in Technology

The solvent-borne and water-borne segments complete the technology landscape of the epoxy adhesives market. Solvent-borne epoxy adhesives are particularly valued in electronics and DIY applications, offering enhanced production efficiency and performance characteristics. These adhesives have established a strong presence in aerospace applications due to their structural properties and ability to withstand extreme temperatures. Water-borne epoxy adhesives, while representing a smaller market share, are gaining importance in environmentally conscious applications, particularly in the healthcare sector. Their eco-friendly nature, characterized by very low VOC emissions, makes them increasingly attractive for medical device manufacturing and other sensitive applications where environmental impact is a key consideration.

Epoxy Adhesive Market Geography Segment Analysis

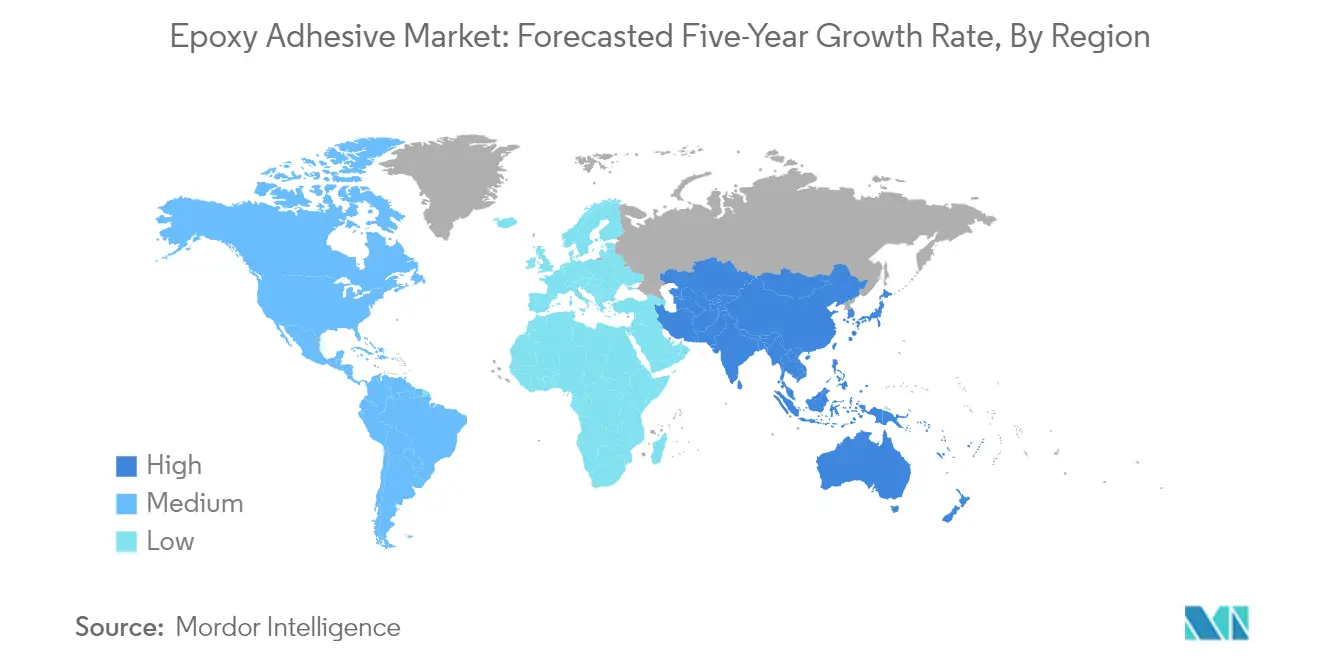

Epoxy Adhesive Market in Asia-Pacific

The Asia-Pacific region represents the largest and most dynamic market for epoxy adhesives globally, driven by robust growth across multiple end-user industries. Countries like China, India, Japan, and South Korea are leading the regional market with their strong manufacturing bases in the automotive, electronics, and construction sectors. The region's market is characterized by increasing adoption of advanced industrial adhesives technologies, particularly in emerging economies where rapid industrialization and infrastructure development are creating substantial demand. The presence of major automotive and electronics manufacturing hubs, particularly in countries like China, Japan, and South Korea, continues to drive market growth, while emerging economies like India and Indonesia are showing increasing demand due to expanding construction and infrastructure projects.

Epoxy Adhesive Market in China

China dominates the Asia-Pacific epoxy adhesives market with approximately 47% market share in 2024, establishing itself as the regional powerhouse. The country's market leadership is supported by its massive manufacturing sector, particularly in the electronics and automotive industries. China's dominance is further strengthened by its position as the world's largest automotive market and electronics manufacturer. The country's robust construction sector and increasing focus on sustainable building practices have also contributed to the growing demand for construction adhesives. The government's emphasis on electric vehicle production and electronics manufacturing has created additional growth opportunities for epoxy adhesive manufacturers.

Epoxy Adhesive Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 7% during 2024-2029. The country's rapid industrial development and increasing investments in infrastructure projects are driving this growth. India's automotive sector expansion, particularly in electric vehicle manufacturing, has created new opportunities for epoxy adhesive applications. The government's push for domestic manufacturing through initiatives aimed at self-reliance has further accelerated market growth. The construction industry's boom and increasing adoption of modern construction techniques have also contributed to the rising demand for epoxy adhesives in the country.

Epoxy Adhesive Market in Europe

The European epoxy adhesives market demonstrates strong growth driven by technological advancements and increasing demand from key end-use industries. The region's market is characterized by strict environmental regulations promoting the use of eco-friendly adhesive solutions. Countries like Germany, France, and the United Kingdom lead the market with their strong industrial bases and innovative approaches to adhesive technologies. The region's focus on sustainable manufacturing practices and increasing adoption of electric vehicles has created new opportunities for epoxy adhesive manufacturers. The presence of major automotive and aerospace manufacturers across various European countries continues to drive market growth.

Epoxy Adhesive Market in Germany

Germany maintains its position as the largest epoxy adhesives market in Europe, holding approximately 22% market share in 2024. The country's market leadership is driven by its robust automotive manufacturing sector and strong presence in industrial manufacturing. Germany's position as a leading European automotive hub, combined with its significant investments in research and development, has established it as a key market for engineering adhesives. The country's focus on high-performance manufacturing and precision engineering continues to drive demand for advanced adhesive solutions.

Epoxy Adhesive Market in United Kingdom

The United Kingdom represents the fastest-growing market in Europe, with an expected growth rate of approximately 7% during 2024-2029. The country's market growth is driven by increasing investments in construction and infrastructure development projects. The UK's focus on renewable energy infrastructure and electric vehicle manufacturing has created new opportunities for epoxy adhesive applications. The aerospace and defense sectors continue to be significant contributors to market growth, with increasing demand for high-performance adhesive solutions.

Epoxy Adhesive Market in Middle East & Africa

The Middle East & Africa region presents a growing market for epoxy adhesives, driven by increasing construction activities and industrial development. The region's market is characterized by significant investments in infrastructure projects and a growing industrial base. Countries like Saudi Arabia and South Africa are leading the regional market with their diverse industrial applications and construction projects. The region's focus on diversifying its economy beyond oil and gas has created new opportunities for specialty adhesives applications across various sectors.

Epoxy Adhesive Market in Saudi Arabia

Saudi Arabia leads the Middle East & Africa epoxy adhesives market, driven by extensive construction activities and infrastructure development projects. The country's market leadership is supported by significant investments in industrial development and manufacturing sectors. Saudi Arabia's Vision 2030 initiative has accelerated construction activities and industrial development, creating sustained demand for epoxy adhesives. The country's growing focus on manufacturing sector development and infrastructure modernization continues to drive market growth.

Epoxy Adhesive Market in South Africa

South Africa emerges as the fastest-growing market in the Middle East & Africa region, driven by increasing industrial activities and infrastructure development projects. The country's market growth is supported by an expanding manufacturing sector and construction activities. South Africa's automotive industry development and increasing focus on industrial manufacturing have created new opportunities for epoxy adhesive applications. The country's growing construction sector and infrastructure development projects continue to drive demand for epoxy adhesives.

Epoxy Adhesive Market in North America

The North American epoxy adhesives market demonstrates strong growth driven by technological advancements and diverse industrial applications. The region benefits from a robust manufacturing sector, particularly in the automotive and aerospace industries. The United States leads the regional market with its extensive industrial base and technological capabilities, while Mexico emerges as the fastest-growing market. The region's focus on sustainable manufacturing practices and increasing adoption of advanced materials in construction and automotive sectors continues to drive market growth. The presence of major manufacturers and ongoing technological innovations in adhesive solutions further strengthens the market position of North America in the global epoxy adhesives industry.

Epoxy Adhesive Market in South America

The South American epoxy adhesives market shows promising growth potential, driven by increasing industrialization and infrastructure development. The region's market is characterized by growing demand from the construction and automotive sectors. Brazil emerges as both the largest and fastest-growing market in the region, leading the market through its diverse industrial applications and expanding manufacturing sector. The region's focus on infrastructure development and increasing industrial activities continues to create new opportunities for epoxy adhesive applications. The automotive manufacturing sector's growth and increasing construction activities across major South American countries contribute significantly to market development.

Get Analysis on Important Geographic Markets

Download PDF

Epoxy Adhesive Industry Overview

Top Companies in Epoxy Adhesives Market

The global epoxy adhesives market is characterized by continuous product innovation and strategic expansion initiatives by leading manufacturers. Companies are heavily investing in research and development to create advanced formulations, particularly focusing on sustainable and environmentally friendly epoxy adhesive solutions with enhanced performance characteristics. Operational agility has become crucial, with manufacturers establishing regional production facilities and strengthening their distribution networks to ensure consistent supply and reduce lead times. Strategic moves in the industry primarily revolve around acquisitions of local companies to gain market access and technological capabilities, while partnerships with raw material suppliers and end-users help secure supply chains and develop application-specific solutions. Geographic expansion, particularly in the emerging markets of the Asia-Pacific and Middle East regions, remains a key focus area through new manufacturing facilities and technical centers.

Consolidated Market Led By Global Players

The epoxy adhesives market exhibits a partly consolidated structure, dominated by large multinational chemical companies with diverse product portfolios. These global conglomerates leverage their extensive research capabilities, established distribution networks, and strong brand recognition to maintain their market positions. Regional players maintain a significant presence in specific geographies through their understanding of local market dynamics and customer relationships, though their influence remains limited on a global scale. The market has witnessed increased consolidation through strategic acquisitions, particularly in emerging markets, as major players seek to expand their geographic footprint and technological capabilities.

The competitive dynamics are shaped by the presence of both specialized adhesive manufacturers and diversified chemical companies that operate across multiple segments. Market leaders have established strong positions through vertical integration, controlling raw material supply chains, and maintaining extensive product portfolios that cater to various end-user industries. The industry has seen a trend of larger companies acquiring smaller, specialized manufacturers to gain access to specific technologies or regional markets, while also investing in joint ventures to strengthen their market presence in high-growth regions.

Innovation and Sustainability Drive Future Success

Success in the epoxy adhesive market increasingly depends on companies' ability to develop innovative products that meet evolving industry requirements while addressing environmental concerns. Manufacturers need to focus on developing bio-based and sustainable adhesive solutions to align with stringent environmental regulations and changing customer preferences. Building strong relationships with key end-user industries, particularly the automotive and construction sectors, through customized solutions and technical support services will be crucial for maintaining market share. Companies must also invest in digital capabilities and technical service centers to provide enhanced customer support and application development assistance.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized products and applications. Developing expertise in specific end-user industries and creating differentiated products that address unique application requirements can help establish market presence. Geographic expansion should be approached through strategic partnerships with local distributors and manufacturers, while investing in research and development capabilities remains essential for long-term success. Companies must also prepare for potential regulatory changes regarding environmental and safety standards, particularly concerning volatile organic compound emissions and chemical safety requirements.

Epoxy Adhesive Market Leaders

-

3M

-

Arkema Group

-

H.B. Fuller Company

-

Henkel AG & Co. KGaA

-

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Epoxy Adhesive Market News

- July 2022: Mapei started the construction of its third manufacturing facility in Kosi, Mathura, to cater to the demand generated from Northern India.

- May 2022: ITW Performance Polymers announced a distribution partnership with PREMA SA in Poland for its Devcon brand.

- February 2022: H.B. Fuller announced the acquisition of Fourny NV to strengthen its Construction Adhesives business in Europe.

Free With This Report

We provide a complimentary and exhaustive set of data points on global and regional metrics that present the fundamental structure of the industry. Presented in the form of 24+ free charts, the section covers rare data on various end-user production trends including automobile production, newly built construction floor area, packaging production, aircraft deliveries, footwear production, and regional data on adhesives and sealants demand, etc.

Epoxy Adhesive Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

-

4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

-

4.2 Regulatory Framework

- 4.2.1 Argentina

- 4.2.2 Australia

- 4.2.3 Brazil

- 4.2.4 Canada

- 4.2.5 China

- 4.2.6 EU

- 4.2.7 India

- 4.2.8 Indonesia

- 4.2.9 Japan

- 4.2.10 Malaysia

- 4.2.11 Mexico

- 4.2.12 Russia

- 4.2.13 Saudi Arabia

- 4.2.14 Singapore

- 4.2.15 South Africa

- 4.2.16 South Korea

- 4.2.17 Thailand

- 4.2.18 United States

- 4.3 Value Chain & Distribution Channel Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

-

5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

-

5.2 Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV Cured Adhesives

- 5.2.4 Water-borne

-

5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 Singapore

- 5.3.1.8 South Korea

- 5.3.1.9 Thailand

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 United Kingdom

- 5.3.2.7 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Saudi Arabia

- 5.3.3.2 South Africa

- 5.3.3.3 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 H.B. Fuller Company

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Hubei Huitian New Materials Co. Ltd

- 6.4.6 Huntsman International LLC

- 6.4.7 Illinois Tool Works Inc.

- 6.4.8 Jowat SE

- 6.4.9 Kangda New Materials (Group) Co., Ltd.

- 6.4.10 KLEBCHEMIE M. G. Becker GmbH & Co. KG

- 6.4.11 MAPEI S.p.A.

- 6.4.12 NANPAO RESINS CHEMICAL GROUP

- 6.4.13 Pidilite Industries Ltd.

- 6.4.14 Sika AG

- 6.4.15 Soudal Holding N.V.

7. KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8. APPENDIX

-

8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- VOLUME OF AIRCRAFTS DELIVERED, UNITS, GLOBAL, 2017-2028

- Figure 2:

- PRODUCTION VOLUME OF AUTOMOBILES, UNITS, GLOBAL, 2017-2028

- Figure 3:

- FLOOR AREA OF NEW CONSTRUCTION, SQUARE FEET, GLOBAL, 2017-2028

- Figure 4:

- PRODUCTION VOLUME OF FOOTWEAR, PAIRS, GLOBAL, 2017-2028

- Figure 5:

- PRODUCTION VOLUME OF PAPER & PAPER BOARD AND PLASTIC PACKAGING, TONS, GLOBAL, 2017-2028

- Figure 6:

- PRODUCTION VOLUME OF FURNITURE, UNITS, GLOBAL, 2017-2028

- Figure 7:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 8:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, GLOBAL, 2017 - 2028

- Figure 9:

- VOLUME OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 10:

- VALUE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, USD, GLOBAL, 2017 - 2028

- Figure 11:

- VOLUME SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, GLOBAL, 2016 VS 2022 VS 2028

- Figure 12:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, GLOBAL, 2016 VS 2022 VS 2028

- Figure 13:

- VOLUME OF EPOXY ADHESIVES CONSUMED IN AEROSPACE INDUSTRY, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 14:

- VALUE OF EPOXY ADHESIVES CONSUMED IN AEROSPACE INDUSTRY, USD, GLOBAL, 2017 - 2028

- Figure 15:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED IN AEROSPACE INDUSTRY BY TECHNOLOGY, %, GLOBAL, 2021 VS 2028

- Figure 16:

- VOLUME OF EPOXY ADHESIVES CONSUMED IN AUTOMOTIVE INDUSTRY, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 17:

- VALUE OF EPOXY ADHESIVES CONSUMED IN AUTOMOTIVE INDUSTRY, USD, GLOBAL, 2017 - 2028

- Figure 18:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED IN AUTOMOTIVE INDUSTRY BY TECHNOLOGY, %, GLOBAL, 2021 VS 2028

- Figure 19:

- VOLUME OF EPOXY ADHESIVES CONSUMED IN BUILDING AND CONSTRUCTION INDUSTRY, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 20:

- VALUE OF EPOXY ADHESIVES CONSUMED IN BUILDING AND CONSTRUCTION INDUSTRY, USD, GLOBAL, 2017 - 2028

- Figure 21:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED IN BUILDING AND CONSTRUCTION INDUSTRY BY TECHNOLOGY, %, GLOBAL, 2021 VS 2028

- Figure 22:

- VOLUME OF EPOXY ADHESIVES CONSUMED IN FOOTWEAR AND LEATHER INDUSTRY, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 23:

- VALUE OF EPOXY ADHESIVES CONSUMED IN FOOTWEAR AND LEATHER INDUSTRY, USD, GLOBAL, 2017 - 2028

- Figure 24:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED IN FOOTWEAR AND LEATHER INDUSTRY BY TECHNOLOGY, %, GLOBAL, 2021 VS 2028

- Figure 25:

- VOLUME OF EPOXY ADHESIVES CONSUMED IN HEALTHCARE INDUSTRY, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 26:

- VALUE OF EPOXY ADHESIVES CONSUMED IN HEALTHCARE INDUSTRY, USD, GLOBAL, 2017 - 2028

- Figure 27:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED IN HEALTHCARE INDUSTRY BY TECHNOLOGY, %, GLOBAL, 2021 VS 2028

- Figure 28:

- VOLUME OF EPOXY ADHESIVES CONSUMED IN PACKAGING INDUSTRY, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 29:

- VALUE OF EPOXY ADHESIVES CONSUMED IN PACKAGING INDUSTRY, USD, GLOBAL, 2017 - 2028

- Figure 30:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED IN PACKAGING INDUSTRY BY TECHNOLOGY, %, GLOBAL, 2021 VS 2028

- Figure 31:

- VOLUME OF EPOXY ADHESIVES CONSUMED IN WOODWORKING AND JOINERY INDUSTRY, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 32:

- VALUE OF EPOXY ADHESIVES CONSUMED IN WOODWORKING AND JOINERY INDUSTRY, USD, GLOBAL, 2017 - 2028

- Figure 33:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED IN WOODWORKING AND JOINERY INDUSTRY BY TECHNOLOGY, %, GLOBAL, 2021 VS 2028

- Figure 34:

- VOLUME OF EPOXY ADHESIVES CONSUMED IN OTHER END-USER INDUSTRIES INDUSTRY, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 35:

- VALUE OF EPOXY ADHESIVES CONSUMED IN OTHER END-USER INDUSTRIES INDUSTRY, USD, GLOBAL, 2017 - 2028

- Figure 36:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED IN OTHER END-USER INDUSTRIES INDUSTRY BY TECHNOLOGY, %, GLOBAL, 2021 VS 2028

- Figure 37:

- VOLUME OF EPOXY ADHESIVES CONSUMED BY TECHNOLOGY, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 38:

- VALUE OF EPOXY ADHESIVES CONSUMED BY TECHNOLOGY, USD, GLOBAL, 2017 - 2028

- Figure 39:

- VOLUME SHARE OF EPOXY ADHESIVES CONSUMED BY TECHNOLOGY, %, GLOBAL, 2016 VS 2022 VS 2028

- Figure 40:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY TECHNOLOGY, %, GLOBAL, 2016 VS 2022 VS 2028

- Figure 41:

- VOLUME OF REACTIVE EPOXY ADHESIVES CONSUMED, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 42:

- VALUE OF REACTIVE EPOXY ADHESIVES CONSUMED, USD, GLOBAL, 2017 - 2028

- Figure 43:

- VALUE SHARE OF REACTIVE EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, GLOBAL, 2021 VS 2028

- Figure 44:

- VOLUME OF SOLVENT-BORNE EPOXY ADHESIVES CONSUMED, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 45:

- VALUE OF SOLVENT-BORNE EPOXY ADHESIVES CONSUMED, USD, GLOBAL, 2017 - 2028

- Figure 46:

- VALUE SHARE OF SOLVENT-BORNE EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, GLOBAL, 2021 VS 2028

- Figure 47:

- VOLUME OF UV CURED ADHESIVES EPOXY ADHESIVES CONSUMED, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 48:

- VALUE OF UV CURED ADHESIVES EPOXY ADHESIVES CONSUMED, USD, GLOBAL, 2017 - 2028

- Figure 49:

- VALUE SHARE OF UV CURED ADHESIVES EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, GLOBAL, 2021 VS 2028

- Figure 50:

- VOLUME OF WATER-BORNE EPOXY ADHESIVES CONSUMED, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 51:

- VALUE OF WATER-BORNE EPOXY ADHESIVES CONSUMED, USD, GLOBAL, 2017 - 2028

- Figure 52:

- VALUE SHARE OF WATER-BORNE EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, GLOBAL, 2021 VS 2028

- Figure 53:

- VOLUME OF EPOXY ADHESIVES CONSUMED BY REGION, KILOGRAM, GLOBAL, 2017 - 2028

- Figure 54:

- VALUE OF EPOXY ADHESIVES CONSUMED BY REGION, USD, GLOBAL, 2017 - 2028

- Figure 55:

- VOLUME SHARE OF EPOXY ADHESIVES CONSUMED BY REGION, %, GLOBAL, 2016 VS 2022 VS 2028

- Figure 56:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY REGION, %, GLOBAL, 2016 VS 2022 VS 2028

- Figure 57:

- VOLUME OF EPOXY ADHESIVES CONSUMED BY COUNTRY, KILOGRAM, ASIA-PACIFIC, 2017 - 2028

- Figure 58:

- VALUE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, USD, ASIA-PACIFIC, 2017 - 2028

- Figure 59:

- VOLUME SHARE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, %, ASIA-PACIFIC, 2016 VS 2022 VS 2028

- Figure 60:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, %, ASIA-PACIFIC, 2016 VS 2022 VS 2028

- Figure 61:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, AUSTRALIA, 2017 - 2028

- Figure 62:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, AUSTRALIA, 2017 - 2028

- Figure 63:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, AUSTRALIA, 2021 VS 2028

- Figure 64:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, CHINA, 2017 - 2028

- Figure 65:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, CHINA, 2017 - 2028

- Figure 66:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, CHINA, 2021 VS 2028

- Figure 67:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, INDIA, 2017 - 2028

- Figure 68:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, INDIA, 2017 - 2028

- Figure 69:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, INDIA, 2021 VS 2028

- Figure 70:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, INDONESIA, 2017 - 2028

- Figure 71:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, INDONESIA, 2017 - 2028

- Figure 72:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, INDONESIA, 2021 VS 2028

- Figure 73:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, JAPAN, 2017 - 2028

- Figure 74:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, JAPAN, 2017 - 2028

- Figure 75:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, JAPAN, 2021 VS 2028

- Figure 76:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, MALAYSIA, 2017 - 2028

- Figure 77:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, MALAYSIA, 2017 - 2028

- Figure 78:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, MALAYSIA, 2021 VS 2028

- Figure 79:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, SINGAPORE, 2017 - 2028

- Figure 80:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, SINGAPORE, 2017 - 2028

- Figure 81:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, SINGAPORE, 2021 VS 2028

- Figure 82:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, SOUTH KOREA, 2017 - 2028

- Figure 83:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, SOUTH KOREA, 2017 - 2028

- Figure 84:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, SOUTH KOREA, 2021 VS 2028

- Figure 85:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, THAILAND, 2017 - 2028

- Figure 86:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, THAILAND, 2017 - 2028

- Figure 87:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, THAILAND, 2021 VS 2028

- Figure 88:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, REST OF ASIA-PACIFIC, 2017 - 2028

- Figure 89:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, REST OF ASIA-PACIFIC, 2017 - 2028

- Figure 90:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, REST OF ASIA-PACIFIC, 2021 VS 2028

- Figure 91:

- VOLUME OF EPOXY ADHESIVES CONSUMED BY COUNTRY, KILOGRAM, EUROPE, 2017 - 2028

- Figure 92:

- VALUE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, USD, EUROPE, 2017 - 2028

- Figure 93:

- VOLUME SHARE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, %, EUROPE, 2016 VS 2022 VS 2028

- Figure 94:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, %, EUROPE, 2016 VS 2022 VS 2028

- Figure 95:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, FRANCE, 2017 - 2028

- Figure 96:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, FRANCE, 2017 - 2028

- Figure 97:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, FRANCE, 2021 VS 2028

- Figure 98:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, GERMANY, 2017 - 2028

- Figure 99:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, GERMANY, 2017 - 2028

- Figure 100:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, GERMANY, 2021 VS 2028

- Figure 101:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, ITALY, 2017 - 2028

- Figure 102:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, ITALY, 2017 - 2028

- Figure 103:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, ITALY, 2021 VS 2028

- Figure 104:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, RUSSIA, 2017 - 2028

- Figure 105:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, RUSSIA, 2017 - 2028

- Figure 106:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, RUSSIA, 2021 VS 2028

- Figure 107:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, SPAIN, 2017 - 2028

- Figure 108:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, SPAIN, 2017 - 2028

- Figure 109:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, SPAIN, 2021 VS 2028

- Figure 110:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, UNITED KINGDOM, 2017 - 2028

- Figure 111:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, UNITED KINGDOM, 2017 - 2028

- Figure 112:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, UNITED KINGDOM, 2021 VS 2028

- Figure 113:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, REST OF EUROPE, 2017 - 2028

- Figure 114:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, REST OF EUROPE, 2017 - 2028

- Figure 115:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, REST OF EUROPE, 2021 VS 2028

- Figure 116:

- VOLUME OF EPOXY ADHESIVES CONSUMED BY COUNTRY, KILOGRAM, MIDDLE EAST & AFRICA, 2017 - 2028

- Figure 117:

- VALUE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, USD, MIDDLE EAST & AFRICA, 2017 - 2028

- Figure 118:

- VOLUME SHARE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, %, MIDDLE EAST & AFRICA, 2016 VS 2022 VS 2028

- Figure 119:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, %, MIDDLE EAST & AFRICA, 2016 VS 2022 VS 2028

- Figure 120:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, SAUDI ARABIA, 2017 - 2028

- Figure 121:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, SAUDI ARABIA, 2017 - 2028

- Figure 122:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, SAUDI ARABIA, 2021 VS 2028

- Figure 123:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, SOUTH AFRICA, 2017 - 2028

- Figure 124:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, SOUTH AFRICA, 2017 - 2028

- Figure 125:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, SOUTH AFRICA, 2021 VS 2028

- Figure 126:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, REST OF MIDDLE EAST & AFRICA, 2017 - 2028

- Figure 127:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, REST OF MIDDLE EAST & AFRICA, 2017 - 2028

- Figure 128:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, REST OF MIDDLE EAST & AFRICA, 2021 VS 2028

- Figure 129:

- VOLUME OF EPOXY ADHESIVES CONSUMED BY COUNTRY, KILOGRAM, NORTH AMERICA, 2017 - 2028

- Figure 130:

- VALUE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, USD, NORTH AMERICA, 2017 - 2028

- Figure 131:

- VOLUME SHARE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, %, NORTH AMERICA, 2016 VS 2022 VS 2028

- Figure 132:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, %, NORTH AMERICA, 2016 VS 2022 VS 2028

- Figure 133:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, CANADA, 2017 - 2028

- Figure 134:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, CANADA, 2017 - 2028

- Figure 135:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, CANADA, 2021 VS 2028

- Figure 136:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, MEXICO, 2017 - 2028

- Figure 137:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, MEXICO, 2017 - 2028

- Figure 138:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, MEXICO, 2021 VS 2028

- Figure 139:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, UNITED STATES, 2017 - 2028

- Figure 140:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, UNITED STATES, 2017 - 2028

- Figure 141:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, UNITED STATES, 2021 VS 2028

- Figure 142:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, REST OF NORTH AMERICA, 2017 - 2028

- Figure 143:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, REST OF NORTH AMERICA, 2017 - 2028

- Figure 144:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, REST OF NORTH AMERICA, 2021 VS 2028

- Figure 145:

- VOLUME OF EPOXY ADHESIVES CONSUMED BY COUNTRY, KILOGRAM, SOUTH AMERICA, 2017 - 2028

- Figure 146:

- VALUE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, USD, SOUTH AMERICA, 2017 - 2028

- Figure 147:

- VOLUME SHARE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, %, SOUTH AMERICA, 2016 VS 2022 VS 2028

- Figure 148:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY COUNTRY, %, SOUTH AMERICA, 2016 VS 2022 VS 2028

- Figure 149:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, ARGENTINA, 2017 - 2028

- Figure 150:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, ARGENTINA, 2017 - 2028

- Figure 151:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, ARGENTINA, 2021 VS 2028

- Figure 152:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, BRAZIL, 2017 - 2028

- Figure 153:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, BRAZIL, 2017 - 2028

- Figure 154:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, BRAZIL, 2021 VS 2028

- Figure 155:

- VOLUME OF EPOXY ADHESIVES CONSUMED, KILOGRAM, REST OF SOUTH AMERICA, 2017 - 2028

- Figure 156:

- VALUE OF EPOXY ADHESIVES CONSUMED, USD, REST OF SOUTH AMERICA, 2017 - 2028

- Figure 157:

- VALUE SHARE OF EPOXY ADHESIVES CONSUMED BY END USER INDUSTRY, %, REST OF SOUTH AMERICA, 2021 VS 2028

- Figure 158:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, GLOBAL, 2019 - 2021

- Figure 159:

- MOST ADOPTED STRATEGIES, COUNT, GLOBAL, 2019 - 2021

- Figure 160:

- REVENUE SHARE OF EPOXY ADHESIVES BY MAJOR PLAYERS, %, GLOBAL, 2021

Epoxy Adhesive Industry Segmentation

Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery are covered as segments by End User Industry. Reactive, Solvent-borne, UV Cured Adhesives, Water-borne are covered as segments by Technology. Asia-Pacific, Europe, Middle East & Africa, North America, South America are covered as segments by Region.| End User Industry | Aerospace | ||

| Automotive | |||

| Building and Construction | |||

| Footwear and Leather | |||

| Healthcare | |||

| Packaging | |||

| Woodworking and Joinery | |||

| Other End-user Industries | |||

| Technology | Reactive | ||

| Solvent-borne | |||

| UV Cured Adhesives | |||

| Water-borne | |||

| Region | Asia-Pacific | Australia | |

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Malaysia | |||

| Singapore | |||

| South Korea | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| Europe | France | ||

| Germany | |||

| Italy | |||

| Russia | |||

| Spain | |||

| United Kingdom | |||

| Rest of Europe | |||

| Middle East & Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| North America | Canada | ||

| Mexico | |||

| United States | |||

| Rest of North America | |||

| South America | Argentina | ||

| Brazil | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the epoxy adhesives market.

- Product - All epoxy adhesive products are considered in the market studied

- Resin - Under the scope of the study, one component and two component based epoxies are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF