Enterprise Key Management (EKM) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.84 Billion |

| Market Size (2030) | USD 7.77 Billion |

| Growth Rate (2025 - 2030) | 22.32% CAGR |

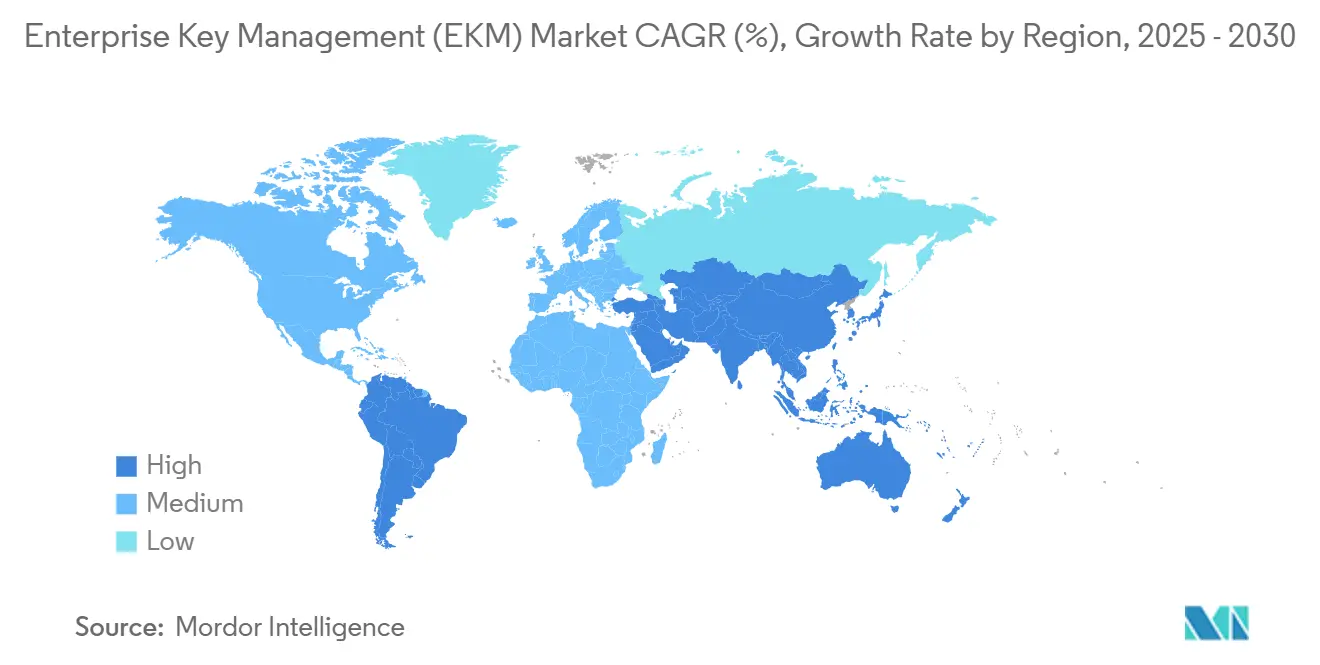

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

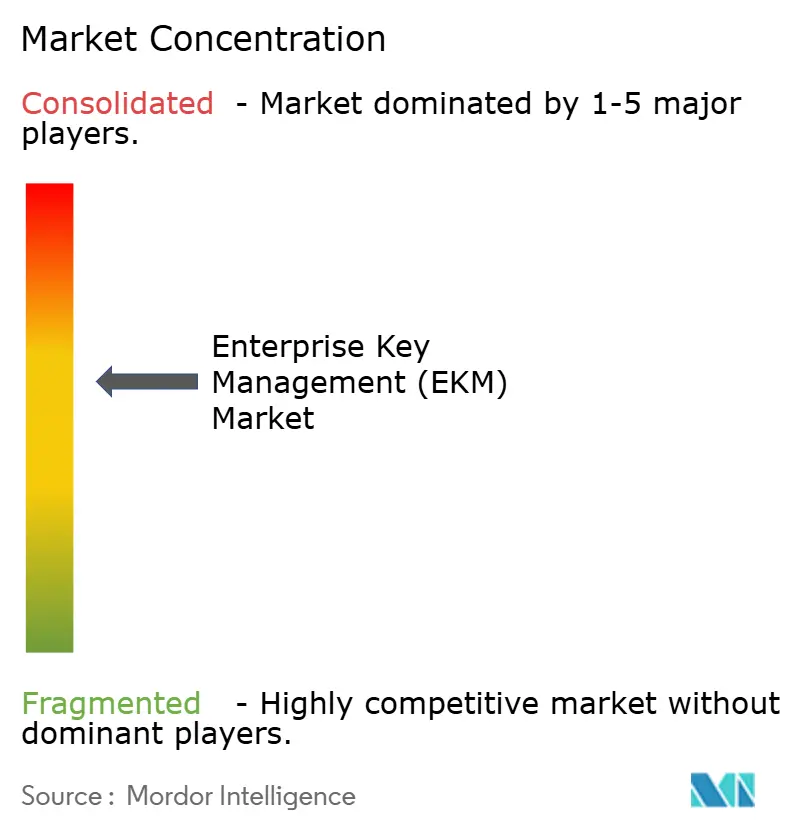

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Enterprise Key Management (EKM) Market Analysis by Mordor Intelligence

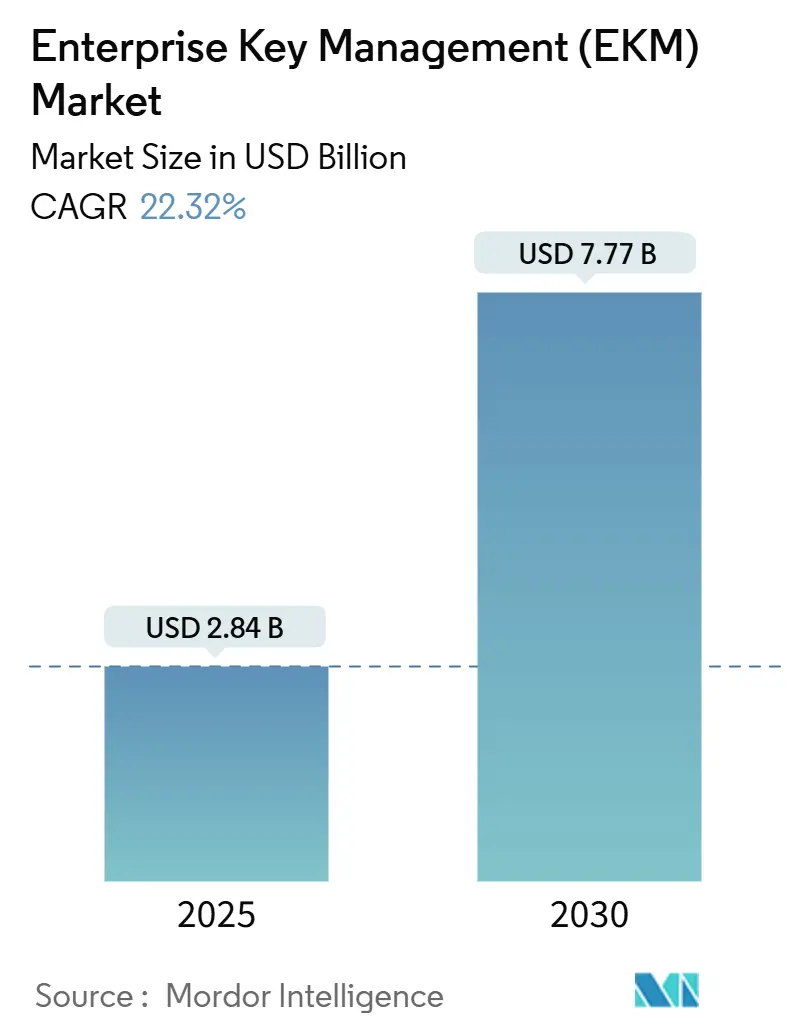

The enterprise key management market size is valued at USD 2.84 billion in 2025 and is forecast to reach USD 7.77 billion by 2030, advancing at a 22.32% CAGR. Surging regulatory mandates, preparations for post-quantum cryptography, and the proliferation of encrypted workloads across hybrid and multi-cloud architectures are the primary forces enlarging the addressable pool of buyers. Organizations view cryptographic keys as the last controllable safeguard in an environment where perimeter controls no longer follow data, and spending priorities are realigning accordingly. Cloud hyperscalers are consolidating share by embedding native key services into their platforms, yet specialist vendors preserve influence by solving multi-cloud interoperability gaps. Meanwhile, shortages of skilled cryptographers and the persistence of legacy systems temper adoption velocity but simultaneously open profitable niches for managed security service providers that supply turnkey governance frameworks.

Key Report Takeaways

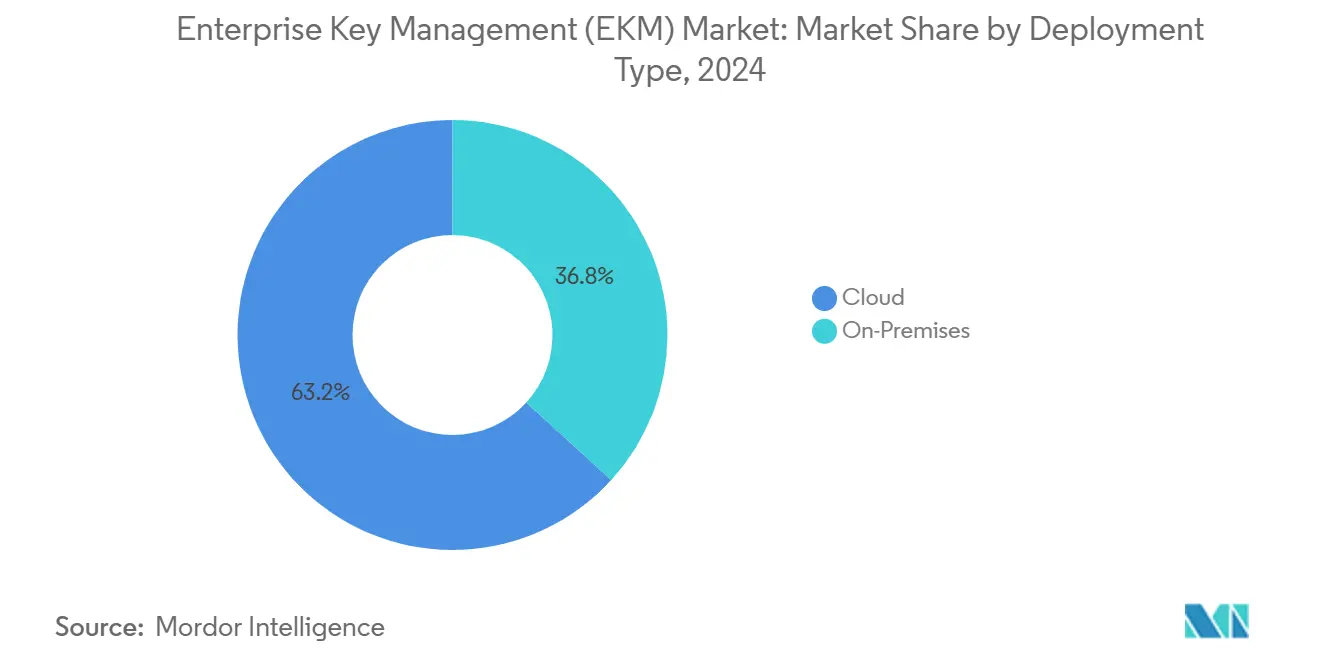

- By deployment type, cloud deployment commanded 63.21% of the enterprise key management market share in 2024 and is projected to expand at a 24.23% CAGR to 2030.

- By size of enterprise, large enterprises held 57.83% revenue share in 2024, while small and medium enterprises are forecast to grow at a 24.11% CAGR through 2030.

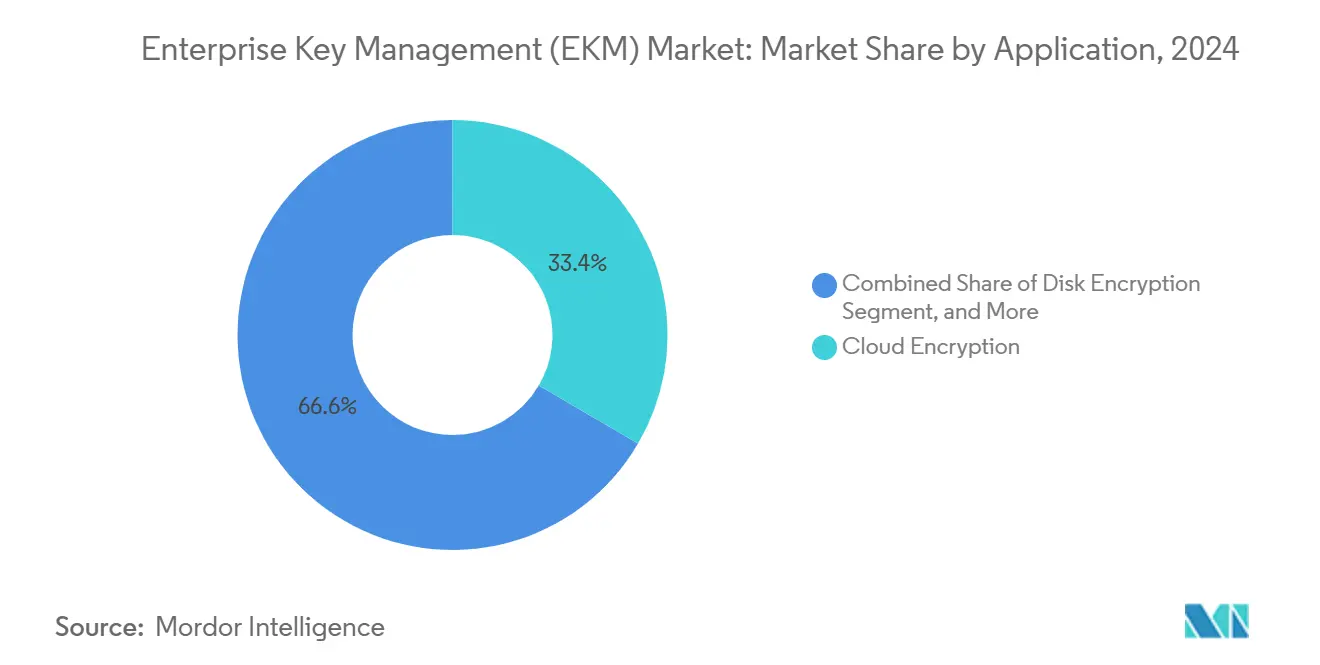

- By application, cloud encryption led with 33.42% revenue share in 2024 and is advancing at a 22.87% CAGR between 2025 and 2030.

- By end-user vertical, banking, financial services and insurance accounted for 31.46% of the enterprise key management market size in 2024 and healthcare is on track for a 22.68% CAGR through 2030.

- By geography, North America held 38.91% revenue share in 2024, whereas Asia Pacific is expected to register 23.14% CAGR up to 2030.

Global Enterprise Key Management (EKM) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing regulatory mandates for data encryption across industries | +4.2% | Global - EU and North America focus | Short term (≤ 2 years) |

| Exponential data growth from cloud and IoT workloads | +3.8% | Global - Asia-Pacific core, MEA spill-over | Medium term (2-4 years) |

| Rising cost of data breaches elevating board-level security budgets | +3.1% | North America and EU expanding to Asia-Pacific | Short term (≤ 2 years) |

| Shift toward hybrid and multi-cloud architectures requiring centralized key management | +4.7% | Global - early North America adoption | Medium term (2-4 years) |

| Emergence of post-quantum cryptography readiness programs | +2.9% | North America and EU, pilot Asia-Pacific | Long term (≥ 4 years) |

| Integration of hardware security modules with DevSecOps pipelines | +3.5% | Global - technology hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Regulatory Mandates for Data Encryption Across Industries

Global regulators now frame encryption as a baseline control, not a discretionary enhancement. In 2024 the European Data Protection Board issued USD 1.6 billion in fines, and 43% cited inadequate encryption controls.[1]European Data Protection Board, “EDPB Annual Report 2024,” edpb.europa.eu Parallel pressure comes from HIPAA cloud guidance updates and overlapping financial directives such as PCI-DSS and SOX that demand demonstrable key segregation. Multinational corporations must therefore orchestrate homogeneous key governance across diverging regional statutes, propelling demand for platforms capable of mapping a single control stack to multiple audit frameworks. Smaller suppliers are swept in as prime contractors embed encryption clauses into procurement contracts, broadening the total purchasing cohort and reinforcing market momentum.

Exponential Data Growth From Cloud and IoT Workloads

Enterprise data volumes climbed 47% year-over-year in 2024, with unstructured sensor output from IoT and edge deployments driving the steepest curve.[2]International Data Corporation, “Worldwide Enterprise Storage Systems Market Forecast 2024-2028,” idc.com Such scale renders appliance-based key stores impractical because millions of devices require low-latency credential rotation even in intermittent-connectivity scenarios. Manufacturing plants that now capture terabytes of telemetry daily and healthcare systems deploying remote patient monitors illustrate the urgency. Cloud-native key services counter this strain through API-driven elasticity, enabling microservices to generate short-lived keys per container instance without manual intervention. As micro-segmentation becomes standard, these services emerge as mandatory underpinnings of modern DevSecOps workflows.

Rising Cost of Data Breaches Elevating Board-Level Security Budgets

The average incident cost rose to USD 4.88 million in 2024, with absent or mismanaged encryption blamed for 67% of financial exposure.[3]IBM Security, “Cost of a Data Breach Report 2024,” ibm.com Boardrooms consequently lifted security budgets 34%, making key management the fastest-growing sub-category within cybersecurity outlays. Cyber insurers now impose strict cryptographic controls as a prerequisite for coverage, transforming key management from a technical afterthought into a financial compliance checkpoint. Banks illustrate the pivot by earmarking up to 20% of technology spending for encryption initiatives, driving procurement cycles that favor platforms demonstrating measurable risk-weighted loss reductions.

Shift Toward Hybrid and Multi-Cloud Architectures Requiring Centralized Key Management

Flexera reports that 89% of enterprises run multi-cloud estates spanning an average 3.4 providers. Each provider offers native key services but seldom supports cross-platform portability, leaving enterprises to risk fragmentation or to adopt neutral governance layers. The issue heightens when on-premises datacenters, edge gateways and sovereign clouds must share credentials while honoring data residency laws. Vendors that expose cloud-agnostic APIs and federated identity bridges address this governance discontinuity, enabling enterprises to standardize policy enforcement and audit logging no matter where the workload runs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited interoperability standards among key management solutions | -2.1% | Global - multi-vendor environments | Medium term (2-4 years) |

| Shortage of cybersecurity professionals skilled in cryptographic key management | -1.8% | Global - acute in North America and EU | Long term (≥ 4 years) |

| High initial integration complexity with legacy systems | -1.4% | Global - established enterprises | Short term (≤ 2 years) |

| Rising cryptographic sprawl leading to governance challenges | -1.6% | Global - cloud-first organizations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Interoperability Standards Among Key Management Solutions

Although PKCS#11 and KMIP exist, they cover baseline functions unsuited for cloud-native patterns and post-quantum algorithms. Proprietary interfaces lock enterprises into single-vendor stacks, complicating exit strategies and multi-cloud rollouts. Migrating keys between provider HSMs often requires data re-encryption, an operational hurdle that curtails agility and inflates cost of ownership. Interoperability gaps consequently decelerate large-scale deployments and inspire procurement teams to insist on open-standard roadmaps before signing multi-year agreements.

Shortage of Cybersecurity Professionals Skilled in Cryptographic Key Management

The global cyber workforce deficit reached 4 million in 2024, and cryptographic expertise represents one of the scarcest subsets. Post-quantum schemes such as lattice-based cryptography further narrow the talent funnel because few practitioners combine algorithm theory with hands-on DevSecOps fluency. Educational curricula have yet to adapt, forcing enterprises to outsource or delay projects. Small and medium enterprises feel the talent pinch most acutely, often relying on managed service providers that raise operating expenditures and introduce third-party risk.

Segment Analysis

By Deployment Type: Cloud Dominance Accelerates Multi-Tenant Adoption

Cloud deployment generated 63.21% of 2024 revenue, cementing its status as the anchor segment within the enterprise key management market. The segment is forecast to record a 24.23% CAGR through 2030 as buyers favor algorithmic agility and elastic scaling over hardware replacement cycles. Cloud-native services integrate seamlessly into DevSecOps toolchains, shortening the interval between code commit and credential issuance for containerized workloads. Financial institutions exemplify adoption momentum by migrating real-time payment platforms to cloud-based vaults that guarantee sub-millisecond key retrieval. The trend intensifies as central banks approve cloud controls for systemically important institutions, removing a longstanding regulatory barrier.

Hardware-centric deployments remain relevant where data sovereignty or latency demands insist on local key custody, yet even these environments increasingly employ hybrid federations that route certain keys to public cloud HSMs for global failover. Vendors that support both patterns within a unified console gain preference because they allow organizations to preserve legacy investments while modernizing selectively. As a result, the enterprise key management market size attributable to hybrid deployments is expanding, although cloud remains both the largest and fastest growing slice.

By Size of Enterprise: SMEs Drive Democratization Through Managed Services

Large enterprises retained 57.83% of enterprise key management market share in 2024, reflecting their mature compliance obligations and deep security staffing benches. Yet small and medium enterprises are advancing at a 24.11% CAGR, propelled by supply-chain mandates that cascade encryption requirements downstream. Subscription pricing removes capex barriers, while managed service providers bundle regulatory reporting to offset skills shortages. Healthcare clinics illustrate the pattern by adopting cloud-vault subscriptions that ensure HIPAA alignment without hiring in-house cryptographers.

Regulators indirectly accelerate SME penetration by penalizing prime contractors for subcontractor lapses, which incentivizes tier-1 firms to sponsor onboarding programs for smaller partners. Consequently, a growing share of enterprise key management market size now originates from mid-market accounts that historically relied on rudimentary password vaults. Vendors that offer pre-packaged compliance templates and automated rotation policies capture disproportionate mindshare among this cohort.

By Application: Cloud Encryption Reshapes Data Protection Strategies

Cloud encryption captured 33.42% of revenue in 2024, outdistancing every on-premises use case and posting a forward CAGR of 22.87%. The rise stems from workloads leaving datacenters en masse and the corresponding need to protect data from hypervisor-level threats. Database encryption trails as the runner-up, sustained by regulatory prescriptions for structured data but constrained by the complexity of retrofitting transparent data encryption across legacy schemas. File-and-folder encryption persists in documentation-heavy verticals while communication encryption leaps forward as zero-trust messaging becomes standard in remote work cultures.

Unified platforms able to orchestrate keys across all encryption classes hold strategic advantage because enterprises wish to avoid separate silos. By aligning encryption coverage at rest, in transit and increasingly in use, these platforms extend enterprise key management market share beyond traditional data-at-rest bastions and into confidential computing arenas. Financial institutions, for instance, now integrate tokenization engines with HSM-backed vaults to anonymize customer data during analytic queries without compromising performance.

Note: Segment shares of all individual segments available upon report purchase

By End-User Vertical: Healthcare Acceleration Outpaces Traditional Leaders

Banking, financial services and insurance accounted for 31.46% of the enterprise key management market size in 2024, consistent with its longstanding encryption culture. Healthcare, however, is expanding at a 22.68% CAGR on the back of telemedicine, connected devices and heightened HIPAA enforcement. Remote patient monitoring sensors generate high-frequency data streams that must be encrypted and signed to preserve integrity in transit, driving demand for vaults that support both symmetric and asymmetric schemes with minimal power draw.

Government and defense maintain steady uptake as classified networks modernize while adhering to FIPS 140-validated hardware. IT and telecommunications operators invest to secure 5G core and edge clouds, creating another growth pocket. Retail brands adopt stronger encryption to meet privacy expectations under California’s CCPA and forthcoming U.S. federal frameworks. These diverse pull factors broaden the vertical profile, reducing historic over-reliance on financial buyers and buttressing long-term market resilience.

Geography Analysis

North America held 38.91% of 2024 revenue, anchored by NIST’s leadership in post-quantum standards and early budget commitments from U.S. federal agencies that require quantum-safe readiness by 2035. Canadian enterprises piggyback on the U.S. innovation stream while tailoring deployments to PIPEDA privacy constraints, and Mexico’s industrial renaissance drives demand for IoT-grade vaults that span factory lines in cross-border supply chains.

Asia Pacific records the briskest trajectory at 23.14% CAGR as sovereign cybersecurity agendas take hold. China’s Cryptography Law compels domestic hosting of keys for critical infrastructure, fueling indigenous vendor growth while obligating Western suppliers to establish joint-venture models. India’s pending Personal Data Protection Bill and Digital India push prompt BFSI and healthcare rollouts, whereas Japan’s Society 5.0 blueprint accelerates factory-floor deployments of edge HSM clusters. South Korea’s advanced telecom infrastructure underpins demand for ultra-low-latency key retrieval at 5G edge nodes.

Europe sustains moderate expansion as GDPR fines demonstrate tangible cost for weak encryption and the forthcoming AI Act extends cryptographic duties to automated decision systems. Germany’s Mittelstand industrial base focuses on machine identity governance, and France’s cloud sovereignty doctrine nurtures local-cloud HSM ecosystems. The United Kingdom, operating under its post-Brexit Data Protection regime, leverages regulatory flexibility to pilot confidential computing constructs in financial services. Collectively, these forces uphold a diversified regional revenue mix and hedge against single-market volatility.

Competitive Landscape

Market concentration is moderate. Amazon Web Services, Microsoft and Google embed vault capabilities directly into core cloud services, monetizing scale advantages and frictionless integration. Specialist players such as Thales, Entrust and HashiCorp defend share by delivering multi-cloud portability, advanced policy engines and niche certifications. Hardware security module incumbents evolve toward software-defined form factors and API-centric models, seeking relevance in containerized infrastructures.

Artificial intelligence and machine learning enrichment emerges as a differentiator; leading platforms instrument behavior analytics that flag anomalous key usage patterns in near real-time. Confidential computing is another battleground; Google’s confidential VM and Azure Confidential Ledger raise expectations that keys will remain shielded even during processing. Product roadmaps are increasingly oriented toward post-quantum agility, reflected in a 67% surge in cryptography patent filings during 2024. Achieving FIPS 140-3 and Common Criteria EAL4+ benchmarks remains vital for defense and government bids, erecting a certification barrier newcomers must cross to penetrate regulated segments.

Enterprise Key Management (EKM) Industry Leaders

-

Amazon Web Services, Inc.

-

Venafi, Inc.

-

Thales Group

-

Google LLC

-

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Microsoft rolled out Azure Key Vault Managed HSM for general use, adding post-quantum cryptography support while retaining FIPS 140-2 Level 3 assurance. The upgrade helps enterprises move to quantum-resistant encryption in advance of the federal transition deadlines.

- September 2025: Thales finished integrating its Luna HSM line with leading cloud confidential-computing services, letting customers run key operations inside trusted execution environments. The move unlocks homomorphic encryption scenarios for finance and healthcare firms that need to compute on protected data.

- August 2025: Amazon Web Services introduced AWS KMS External Key Store, giving organizations the option to keep their encryption keys inside their own HSMs yet still use AWS cloud resources. The hybrid model meets data-sovereignty rules and other strict compliance requirements common in regulated sectors.

- July 2025: IBM Security formed a partnership with Fortanix to build quantum-safe key management for hybrid clouds, marrying IBM’s quantum research with Fortanix’s confidential-computing platform. The effort centers on practical deployments of NIST-approved post-quantum algorithms for enterprise environments.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the enterprise key management market as global revenue from software-centric platforms that generate, store, rotate, and retire cryptographic keys securing data in disks, files, databases, communications, and cloud workloads across heterogeneous infrastructure. Implementation services that ship inseparably with the license are counted within this value.

Scope Exclusion: hardware security modules sold without embedded key-management software and wider encryption gateways are not considered.

Segmentation Overview

- By Deployment Type

- Cloud

- On-Premises

- By Size of Enterprise

- Small- and Medium-sized Enterprises

- Large Enterprises

- By Application

- Disk Encryption

- File and Folder Encryption

- Database Encryption

- Communication Encryption

- Cloud Encryption

- By End-user Vertical

- BFSI

- Healthcare

- Government and Defense

- IT and Telecom

- Retail

- Other End-user Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with product managers at security vendors, CISOs in BFSI and healthcare, cloud architects, and regional system integrators across North America, Europe, and Asia Pacific. These discussions refined deployment splits, price corridors, and five-year penetration assumptions that our desk work could only approximate.

Desk Research

We began with government cybersecurity advisories, customs tariff records, and patent datasets such as NIST NVD, U.S. ITC import codes, and Questel to gauge technology flow. Industry bodies like the Cloud Security Alliance, ISO/IEC SC27, and regional banking regulators supplied adoption triggers and compliance timelines. Company filings, investor presentations, and filtered news inside Dow Jones Factiva enriched average selling prices and roll-out dates. The sources noted illustrate the breadth of material we extract before modeling; many additional outlets supported numerical checks and contextual clarity.

Market-Sizing & Forecasting

We first constructed a top-down demand pool from enterprise security spending and encryption penetration ratios, then validated totals with selective bottom-up supplier roll-ups and channel checks. Key variables like public cloud workload growth, breach incident frequency, data-protection fines, average key-rotation cycles, and hardware security module attach rates steer the model. A multivariate regression supported by scenario analysis projects each input, while interpolation bridges occasional data gaps. This is where Mordor Intelligence differentiates by keeping assumptions transparent and traceable.

Data Validation & Update Cycle

Outputs pass two analyst reviews in which variance against independent metrics is flagged and resolved. We refresh every report annually and issue interim updates when major breaches, regulatory shifts, or landmark acquisitions materially affect the baseline.

Why Our Enterprise Key Management (EKM) Baseline Commands Reliability

Published estimates often diverge because research houses choose different product mixes, price capture points, and refresh tempos.

Mordor's disciplined scoping and yearly rebuild keep our baseline anchored to real purchase behavior.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.84 B (2025) | Mordor Intelligence | |

| USD 2.84 B (2023) | Global Consultancy A | Includes legacy hardware revenue and omits support fee erosion |

| USD 4.93 B (2024) | Regional Consultancy B | Blends key-management software with broader gateway tools |

| USD 2.99 B (2024) | Trade Journal C | Uses uniform global ASPs, ignoring emerging market discounts |

The comparison shows that, by isolating pure software governance layers and refreshing variables every year, we deliver a balanced, transparent baseline that decision-makers can replicate with confidence.

Key Questions Answered in the Report

What is the current value of the enterprise key management market?

The market is valued at USD 2.84 billion in 2025.

How fast is the sector expected to grow?

It is projected to post a 22.32% CAGR from 2025 to 2030.

Which deployment model holds the largest revenue share?

Cloud deployment leads with 63.21% share in 2024.

Which region is expanding the quickest?

Asia Pacific is forecast to grow at a 23.14% CAGR through 2030.

Which application area currently dominates spending?

Cloud encryption generates the highest revenue, holding 33.42% share in 2024.

Why are SMEs ramping up adoption?

Supply-chain encryption mandates and subscription pricing simplify access to enterprise-grade key services for SMEs.

Page last updated on: