Enterprise Application Integration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

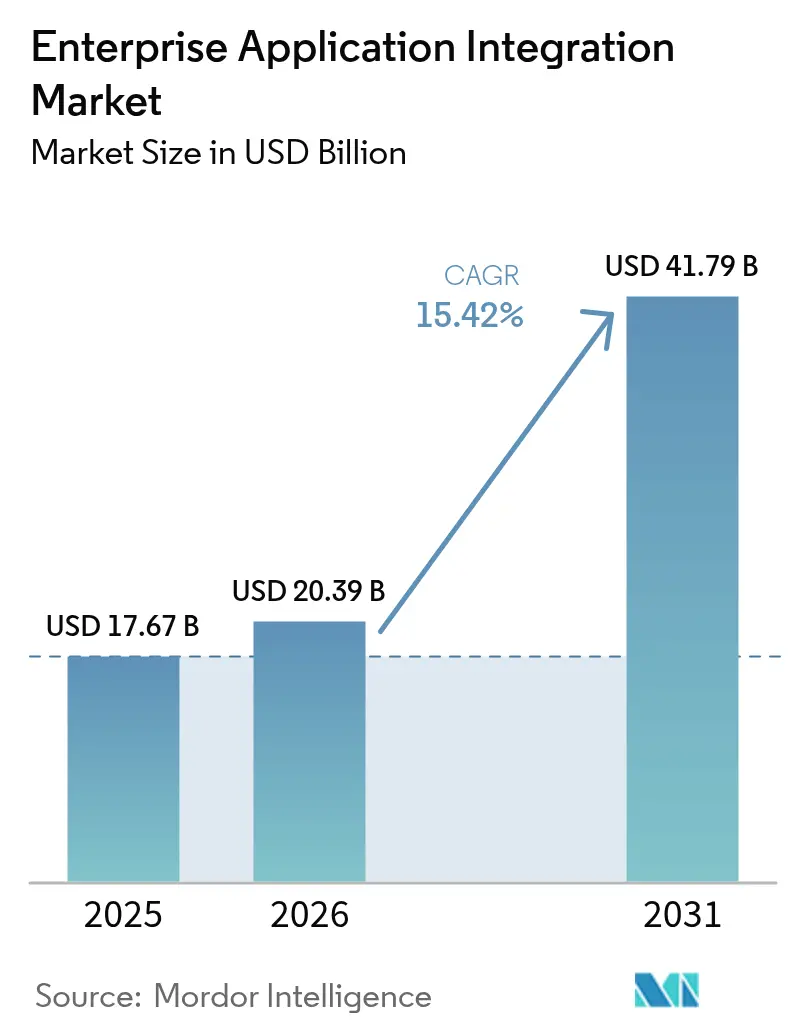

| Market Size (2026) | USD 20.39 Billion |

| Market Size (2031) | USD 41.79 Billion |

| Growth Rate (2026 - 2031) | 15.42% CAGR |

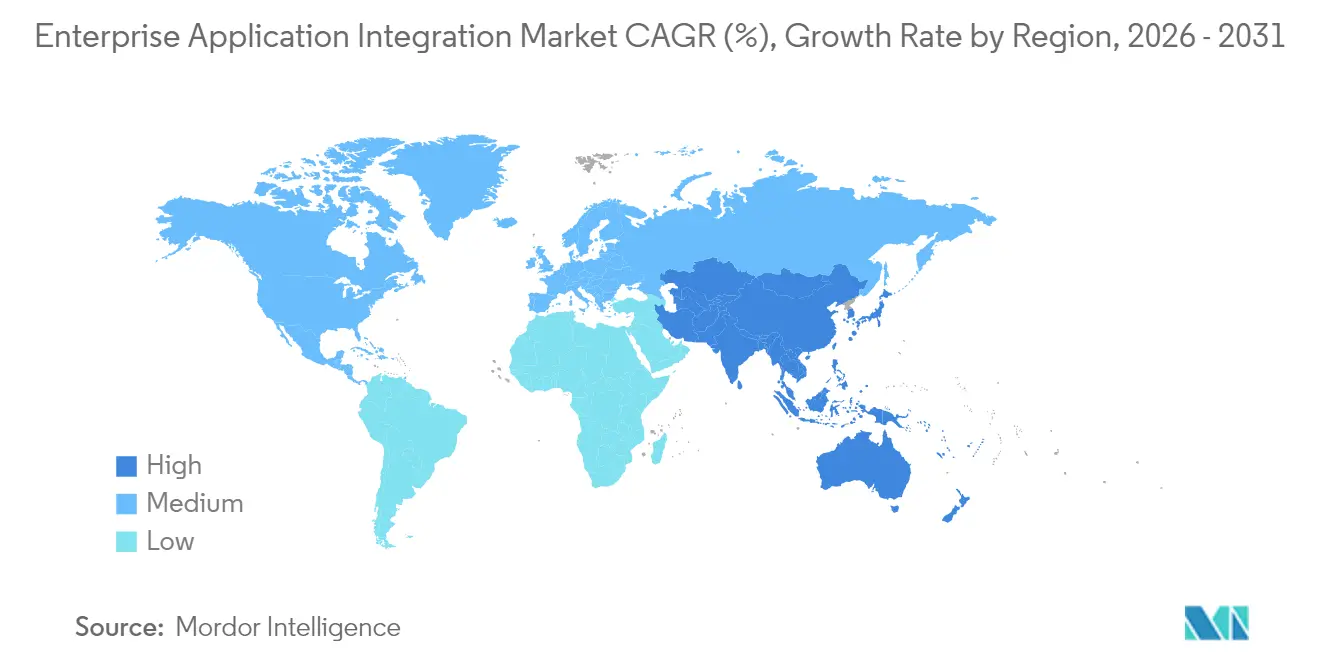

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Application Integration Market Analysis by Mordor Intelligence

The enterprise application integration market size in 2026 is estimated at USD 20.39 billion, growing from 2025 value of USD 17.67 billion with 2031 projections showing USD 41.79 billion, growing at 15.42% CAGR over 2026-2031. The expansion is fueled by enterprises that now treat seamless data flow and application interoperability as critical competitive utilities. North America retains its leadership position because of large cloud budgets and mature API-first cultures, which accelerate adoption. At the same time, the Asia-Pacific region delivers the fastest gains as organizations leapfrog legacy systems and implement multi-cloud programs that demand event-driven and API-led integration patterns. A growing preference for low-code, self-service deployment is widening the user base beyond traditional IT departments, while AI-assisted mapping engines are compressing project timelines and redirecting scarce integration talent toward higher-value tasks. Heightened data-sovereignty regulations in Europe and carbon-aware workload routing mandates are also influencing platform selection, cementing hybrid architectures as the default for global roll-outs.

Key Report Takeaways

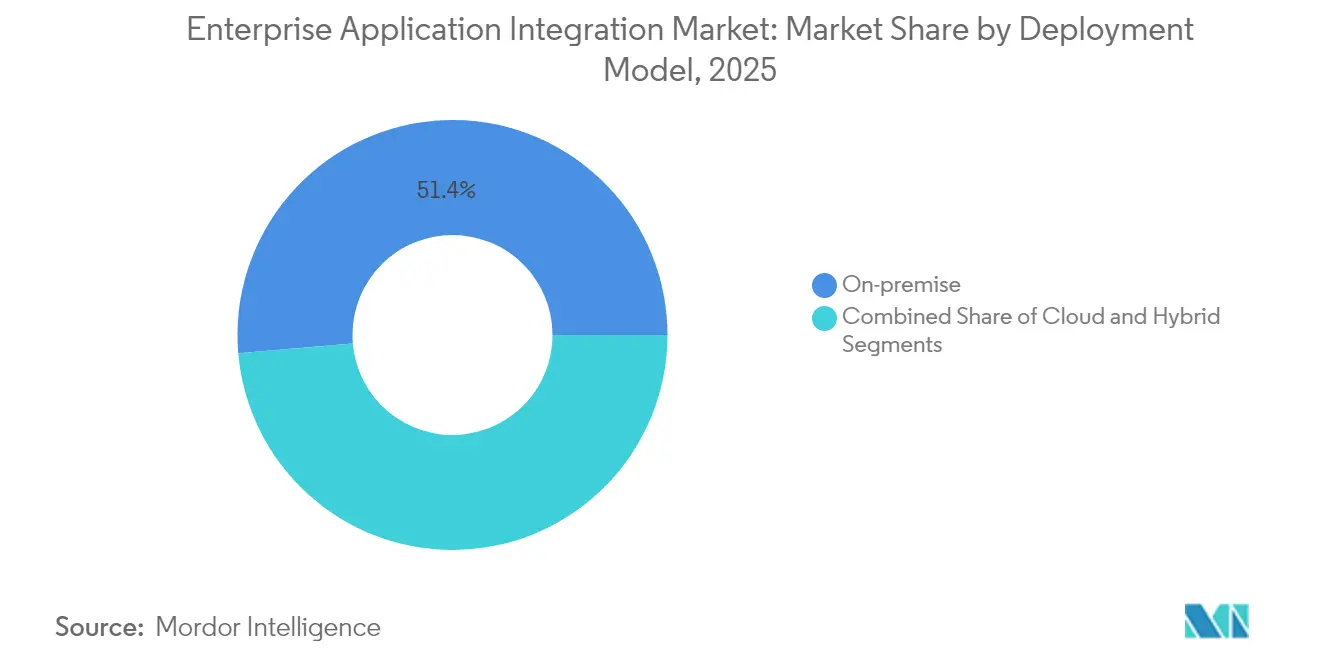

- By deployment model, on-premises held 51.35% share of the enterprise application integration market size in 2025, whereas hybrid deployments are forecast to expand at 17.78% CAGR through 2031.

- By platform type, iPaaS accounted for 33.10% share of the enterprise application integration market size in 2025, while cloud-native iPaaS is projected to register a 24.95% CAGR to 2031.

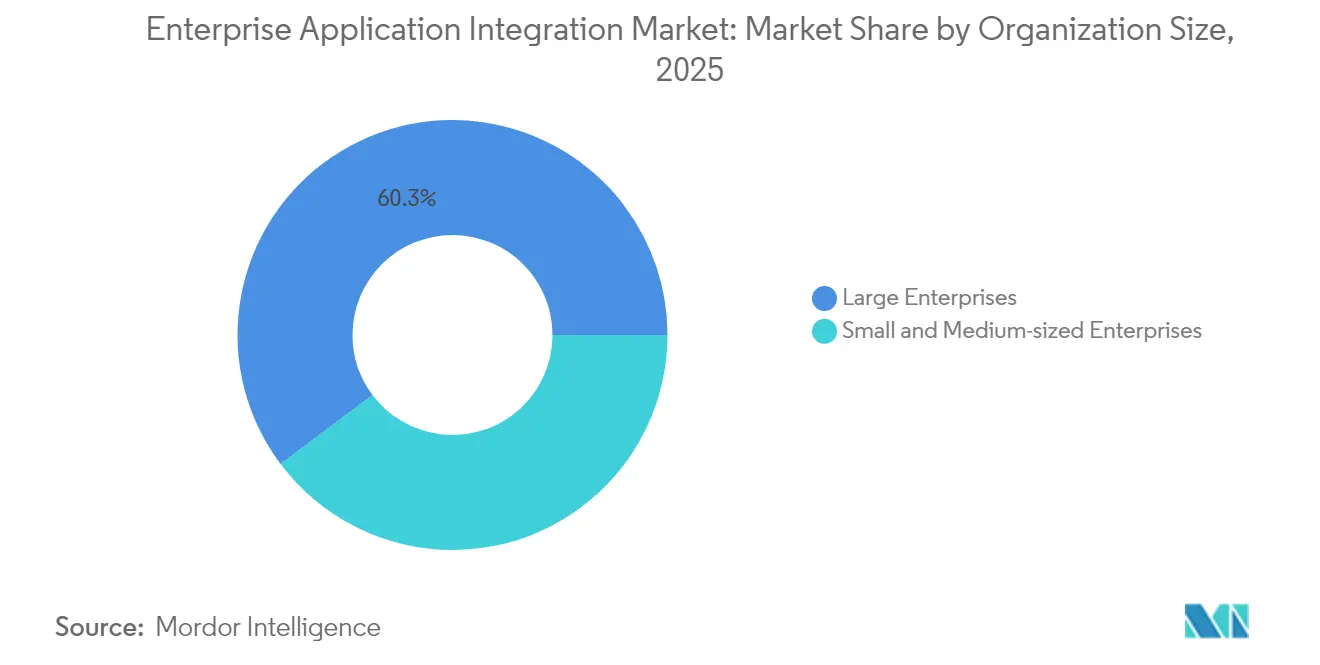

- By organization size, large enterprises generated 60.25% share of the enterprise application integration market size in 2025, however, small and medium enterprises are poised for the fastest growth, with a 21.65% CAGR through 2031.

- By application area, CRM integration led with a 28.30% share of the enterprise application integration market size in 2025, whereas business intelligence and analytics integration is projected to advance at a 23.35% CAGR to 2031.

- By end-user industry, BFSI led with a 53.20% share of the enterprise application integration market size in 2025, whereas the healthcare sector is projected to advance at a 16.88% CAGR from 2025 to 2031.

- By geography, North America accounted for 37.60% share of the enterprise application integration market size in 2025, the Asia-Pacific region is anticipated to post the fastest CAGR of 16.05% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Enterprise Application Integration Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| API-led connectivity accelerating SaaS adoption | +3.20% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Cloud-native iPaaS as de-facto integration backbone | +4.10% | Global, strongest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Event-driven architectures enabling real-time analytics | +2.80% | Global, early adoption in BFSI and IT sectors | Medium term (2-4 years) |

| Generative-AI–assisted mapping and testing tools | +1.90% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Carbon-aware workload routing mandates | +1.40% | Europe leading, North America following | Long term (≥ 4 years) |

| Vendor-agnostic integration marketplaces for micro-SaaS | +1.10% | Global, concentrated in mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

API-led Connectivity Accelerating SaaS Adoption

Reusable API assets now serve as strategic building blocks, shortening release cycles and reducing maintenance overhead. Enterprises adopting the model routinely report integration timeline cuts of 40-60%, which frees budget for incremental digital services. MuleSoft’s growth inside the Salesforce portfolio, combined with Microsoft’s expanding API gateway footprint, illustrates how large vendors are pivoting toward composable integration fabrics.[1]Salesforce, “MuleSoft Announces Latest API-led Innovations,” salesforce.com

Cloud-native iPaaS as De-facto Integration Backbone

Containerized microservices, serverless runtime engines, and automated elasticity enable cloud-native iPaaS platforms to deliver up to 70% total cost of ownership (TCO) savings compared to traditional middleware, as highlighted by Oracle in its recent cloud revenue disclosures.[2]Oracle Investor Relations, “Q1 FY 2025 Results,” oracle.com These economics, coupled with built-in observability and policy enforcement, are steering even risk-averse enterprises toward multi-cloud integration fabrics.

Event-Driven Architectures Enabling Real-time Analytics

Streaming brokers and durable queues let systems respond to business events in milliseconds, supporting real-time fraud detection, supply-chain reprioritization, and instant personalization. Banks deploying Kafka-based architectures confirm measurable drops in fraud losses and gains in customer satisfaction when paired with machine learning pipelines.

Generative-AI-Assisted Mapping and Testing Tools

Integration teams now leverage large language models that read source and target schemas, auto-generate transformation logic, and create test harnesses. IBM’s recent incorporation of HashiCorp assets underscores the strategy of wrapping AI around infrastructure-as-code to shrink build cycles and uplift data quality.[3]IBM Newsroom, “StreamSets Joins IBM Data and AI,” ibm.com Early adopters cite 30-50% reductions in development effort.

Restraints Impact Analysis of Enterprise Application Integration Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Open-source ESB alternatives eroding licence revenue | -2.10% | Global, strongest impact in cost-sensitive markets | Medium term (2-4 years) |

| Shortage of integration-skill talent inflating project costs | -1.80% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Hidden egress-fee economics in hyperscale clouds | -1.30% | Global, particularly affecting multi-cloud strategies | Short term (≤ 2 years) |

| Legacy technical-debt penalties on API security posture | -1.10% | Global, concentrated in established enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Open-source ESB Alternatives Eroding License Revenue

Apache Camel, WSO2, and similar frameworks offer robust integration without licensing costs, appealing to organizations with capable internal engineering teams. Commercial platforms, therefore, emphasize differentiated AI orchestration, managed services, and security certifications in order to justify premium tiers.[4]WSO2 Press Center, “WSO2 Integration Platform Milestones,” wso2.com

Shortage of Integration-Skill Talent Inflating Project Costs

A limited pool of professionals who understand cloud-native architecture, event streaming, and zero-trust security drives consulting rates up and lengthens projects. Vendors counter this by embedding low-code tooling and guided wizards that enable citizen integrators to build flows and enforce policies, as seen in Microsoft’s Power Platform enhancements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Enterprise Application Integration Market Segment Analysis

By Deployment Model:

Hybrid Solutions Bridge Legacy-Cloud DivideHybrid environments accounted for 17.78% CAGR, evidencing the architectural sweet spot between on-premise control and cloud agility. The enterprise application integration market size tied to hybrid roll-outs will likely surpass on-premise outlays after 2027, as migration risk is mitigated while cloud services continue to improve their economics. Banks and regulated healthcare providers integrate mainframes with SaaS by dropping lightweight connectors into private clouds and linking them via secure VPN or SD-WAN tunnels. Deployment toolkits that bundle policy-driven routing, encryption, and real-time observability reduce operational friction, making hybrid integration attractive for continuous regulatory reporting. IBM bundled its recently acquired HashiCorp Terraform modules to automate cluster provisioning across clouds, which simplifies governance for global corporations.

Despite ongoing dominance, on-premise implementations are evolving rather than fading. Organizations migrate their foundational message buses toward container platforms on internal Kubernetes clusters, refreshing hardware only where latency or sovereignty requirements necessitate local processing. This incremental modernization prevents wholesale rip-and-replace projects, lowers capex surprises, and maintains continuity for mission-critical workflows that cannot risk outage windows longer than a few seconds. For global manufacturers, local integration appliances in factories offer deterministic latency while cloud event hubs aggregate data for predictive analytics models.

By Integration Platform Type:

iPaaS Dominance Accelerates Cloud-Native TransitioniPaaS generated 33.10% revenue in 2025 and sits at the center of enterprise blueprints that prioritize subscription economics over perpetual licenses. The segment’s 24.95% CAGR is underpinned by continuous connector library expansion, managed runtime patches, and SLA-bound uptime commitments that free customers from the burdens of middleware patching. Microsoft, Oracle, SAP, and Salesforce deliver bundled iPaaS capability directly in their cloud suites, reducing procurement steps and providing consistent identity models across application layers.

Conversely, ESB platforms retain hold in complex hub-and-spoke topologies within telecom carriers and defense contractors. Vendors supporting these estates now ship containerized runtimes that run inside Kubernetes, thereby easing the lift-and-shift to private clouds when a data center exit is mandated. Data integration tools with pushdown ELT pipelines also claim relevance by feeding lakehouse architectures that demand high-throughput batch ingestion.

By Organization Size:

SME Adoption Democratizes Integration CapabilitiesCRM synchronization produced the greatest contribution to the enterprise application integration market size in 2025, as sales, service, and marketing teams unify customer profiles for omnichannel engagement. However, BI and analytics integration will witness the quickest expansion at a 23.35% CAGR, as leadership teams demand unified data pipelines that feed dashboards, predictive models, and generative AI assistants in near real-time. Data mesh principles proliferate when domain teams publish governed data products through APIs. Integration platforms provide policy engines that enforce lineage, quality, and access, ensuring that analytics conclusions remain trustworthy.

Supply-chain and logistics integration ranks high on the priority list due to geopolitical disruptions that expose visibility gaps. Retailers connect warehouse robots, transportation management, and inventory/ordering modules to rebalance stock in hours rather than weeks. ERP and finance connectors enforce dual entries across legacy general ledger systems and modern SaaS billing, reducing reconciliation cycles from days to minutes. HR integration gains ground as remote work enlarges compliance footprints across multiple countries, compelling automated payroll and benefits data handoffs.

By End-user Industry:

BFSI Leads Digital Transformation InvestmentBFSI dominates spending because real-time risk assessment, open-banking APIs, and anti-money-laundering compliance demand performant integration. The enterprise application integration market share attributed to BFSI is expected to remain prominent through 2031 as payment modernization and ISO 20022 migrations intensify. Financial institutions embed event streaming for instant settlement, feeding downstream fraud models that trigger within seconds. API management layers enable monetization of banking APIs for partners while ensuring throttling and consent management remain compliant.

Healthcare accelerates adoption as telemedicine, electronic health record data exchange, and updated HIPAA guidelines require secure interoperability. Providers are increasingly deploying FHIR-compliant APIs, mapped through iPaaS, to ensure that prescription data flows to pharmacies in real-time. Retail, e-commerce, and manufacturing follow closely, aiming for hyper-personalized shopper journeys and smart factory rollouts that rely on bidirectional integration between operational technology and IT systems. Government digital-service agendas push agencies to expose reusable APIs, often guided by zero-trust security architectures mandated by regulatory frameworks.

Geography Analysis

North America Enterprise Application Integration Market

North America maintained a 37.60% revenue share in 2025, anchored by the United States, where hyperscale cloud regions, venture capital-funded SaaS ecosystems, and robust API economy cultures converge. Federal and state agencies also allocate funds to modernize procurement, taxation, and benefit systems, generating prolonged demand for secure integration gateways. Canada exhibits similar momentum but places a stronger emphasis on data residency, prompting the usage of local-region cloud zones and hybrid edge appliances. Mexico sits at an earlier stage yet climbs swiftly as enterprises modernize ERP and payment rails, often leveraging near-shore service providers that deliver integration services from bilingual talent hubs.

Broader European Markets

Europe represents a sizable opportunity, as the GDPR, the Digital Operational Resilience Act, and emerging carbon footprint disclosures guide platform audits. Germany’s automotive and industrial clusters deploy edge-to-cloud connectors that transport machine telemetry into predictive maintenance models. The United Kingdom finances open-banking roadmaps that enlarge the addressable pool for API management suites. France backs sovereign-cloud initiatives that favor European vendors bundling comprehensive compliance artefacts. Nordic countries, already mature in cloud adoption, pioneer carbon-aware routing where integration engines shift compute to regions with renewable energy availability during peak windows.

APAC Enterprise Application Integration Market

The Asia-Pacific region demonstrates the fastest growth, with a 16.05% CAGR through 2031, as enterprises skip legacy ESB generations and consume iPaaS directly. China invests in large-scale industrial Internet projects and AI acceleration chips that stream vast amounts of telemetry, requiring high-throughput integration fabrics. India’s digital-public-infrastructure stack, including Aadhaar and Unified Payments Interface, normalizes API consumption for millions of citizens and drives local SI firms to specialize in secure, high-volume connectors. Japan and South Korea are investing resources in smart factory initiatives, where edge brokers synchronize robots with ERP systems in real-time. Southeast Asian nations utilize cloud-first regulatory sandboxes to jump-start fintech innovation, creating niches for lightweight integration runtimes.

Competitive Landscape

The landscape shows moderate fragmentation. IBM, Microsoft, Oracle, and SAP integrate their capabilities with adjacent products, such as analytics, security, and developer clouds, offering a bundled value proposition that minimizes vendor sprawl. IBM’s USD 6.4 billion purchase of HashiCorp extends its automation control plane, making multi-cloud provisioning and policy enforcement native functions within its integration suite. Microsoft amplifies the reach of the Power Platform by embedding Copilot-generated connectors, enabling business users to automate tasks without code while benefiting from Azure’s security posture.

Specialists like MuleSoft, Workato, SnapLogic, Celigo, and Jitterbit differentiate through rapid connector release cycles, intuitive UIs, and aggressive marketplace ecosystem expansion. They fill white spaces where customers require best-of-breed depth or industry templates that generalized mega-suites do not yet address. SnapLogic’s SOC 3 certification and ongoing FedRAMP efforts illustrate how challengers close compliance gaps to compete for regulated workloads. Meanwhile, private-equity-backed roll-ups, such as TIBCO and Talend, accelerate cross-selling into existing data-integration bases, forming mid-tier players with significant scale.

Blue Yonder’s acquisition of One Network Enterprises for USD 839 million foreshadows domain-specific integration packages that link supply-chain execution with planning suites. Systems integrators like NTT DATA supplement advisory arms through acquisitions of MuleSoft and analytics specialists, building service capacity to implement complex roadmaps.

Enterprise Application Integration Industry Leaders

IBM Corporation

Fujitsu Limited

Microsoft Corporation

MuleSoft LLC (Salesforce Inc.)

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Enterprise Application Integration Market Companies Covered in this Report

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Salesforce Inc. (MuleSoft LLC)

- Software AG

- TIBCO Software Inc.

- Fujitsu Ltd.

- iTransition Group

- Dell Boomi LLC

- Informatica LLC

- SnapLogic Inc.

- Workato Inc.

- Celigo Inc.

- Jitterbit Inc.

- Talend S.A.

- Red Hat Inc.

- WSO2 Inc.

- Cleo Communications Inc.

- OpenLegacy Inc.

Recent Industry Developments in Enterprise Application Integration Market

- March 2025: IBM completed its USD 6.4 billion acquisition of HashiCorp, integrating infrastructure-as-code into hybrid-cloud automation.

- March 2025: Appian released Platform 24.3 featuring AI Copilot and HITRUST certification for healthcare workloads.

- February 2025: NTT DATA acquired Apisero and Aspirent to bolster MuleSoft, Salesforce, and AI service delivery.

- January 2025: SnapLogic obtained a SOC 3 attestation covering enterprise-grade security controls.

Global Enterprise Application Integration Market Report Scope

Enterprise application integration software refers to server software, hardware, or virtual appliances installed on-premise inside a data center, or offered in a public or private cloud, to integrate applications. It handles the workflow or orchestration of automated multistep requests requiring coordinated interactions across applications, back-end services, and data stores. The study tracks the various types of integration platforms to support on-premise, cloud, and iPaaS (integration Platform-as-a-Service) and end users in the market.

The enterprise application integration market is segmented by deployment type (on-premise, cloud, hybrid), by organization size (large enterprises, small and medium-sized enterprises), by end-user industry (BFSI, IT and telecom, healthcare, retail, government, manufacturing), and by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Segmentation Overview

| On-premise |

| Cloud |

| Hybrid |

| Enterprise Service Bus (ESB) |

| Integration Platform-as-a-Service (iPaaS) |

| API-Gateway / Management Suites |

| Data and ETL/ELT Tools |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| CRM Integration |

| ERP and Finance Integration |

| Supply-Chain / Logistics Integration |

| HR and Workforce Integration |

| Business Intelligence and Analytics Integration |

| BFSI |

| IT and Telecom |

| Healthcare |

| Retail and E-commerce |

| Government |

| Manufacturing |

| Other End-user Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | On-premise | ||

| Cloud | |||

| Hybrid | |||

| By Integration Platform Type | Enterprise Service Bus (ESB) | ||

| Integration Platform-as-a-Service (iPaaS) | |||

| API-Gateway / Management Suites | |||

| Data and ETL/ELT Tools | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-sized Enterprises | |||

| By Application Area | CRM Integration | ||

| ERP and Finance Integration | |||

| Supply-Chain / Logistics Integration | |||

| HR and Workforce Integration | |||

| Business Intelligence and Analytics Integration | |||

| By End-user Industry | BFSI | ||

| IT and Telecom | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Government | |||

| Manufacturing | |||

| Other End-user Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the enterprise integration platform market and its expected growth?

The market is valued at USD 20.39 billion in 2026 and is forecast to reach USD 41.79 billion by 2031, reflecting a 15.42% CAGR.

Which platform type holds the largest revenue share?

Integration Platform-as-a-Service (iPaaS) leads with a 33.10% share in 2025 and maintains a strong growth trajectory.

Why are hybrid deployment models gaining momentum?

Hybrid architectures let enterprises retain on-premises governance while tapping cloud scalability, driving an 17.78% CAGR for hybrid roll-outs through 2031.

Which region is growing the fastest?

Asia-Pacific shows the quickest expansion, projected at 16.05% CAGR as organizations adopt cloud-native integration to bypass legacy constraints.

Page last updated on: