Enteral Feeding Formulas Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

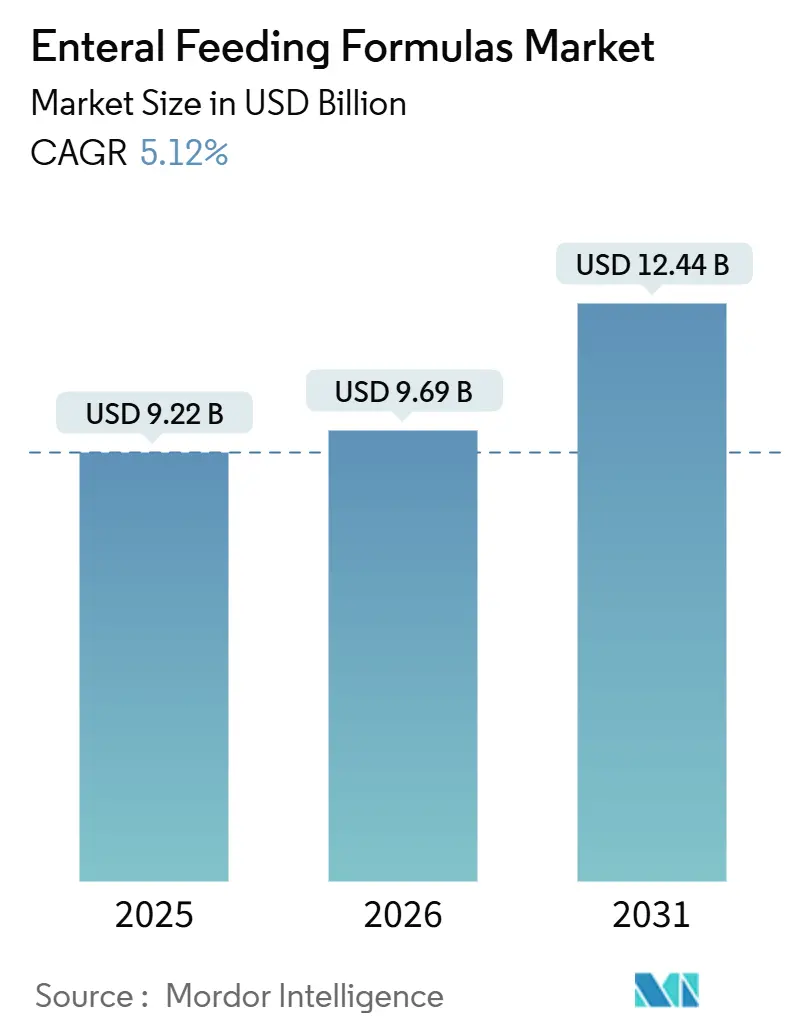

| Market Size (2026) | USD 9.69 Billion |

| Market Size (2031) | USD 12.44 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enteral Feeding Formulas Market Analysis by Mordor Intelligence

The Enteral Feeding Formulas Market size is expected to increase from USD 9.22 billion in 2025 to USD 9.69 billion in 2026 and reach USD 12.44 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

Demand is being propelled by demographic aging, wider use of enteral nutrition for chronic disease management, and the steady shift of complex feeding regimens from hospitals to homes. The growing preference for whole-food ingredients, advances in closed-loop delivery systems, and reimbursement models that reward lower-cost care settings are reinforcing adoption. At the same time, portable pumps with wireless connectivity are lowering technical barriers for caregivers, and outcome-linked payment programs are steering providers toward formulas with proven clinical benefits. Competitive differentiation is now centered on disease-specific compositions, plant-based proteins, and smart infusion technologies that reduce infection and misconnection risks.

Key Report Takeaways

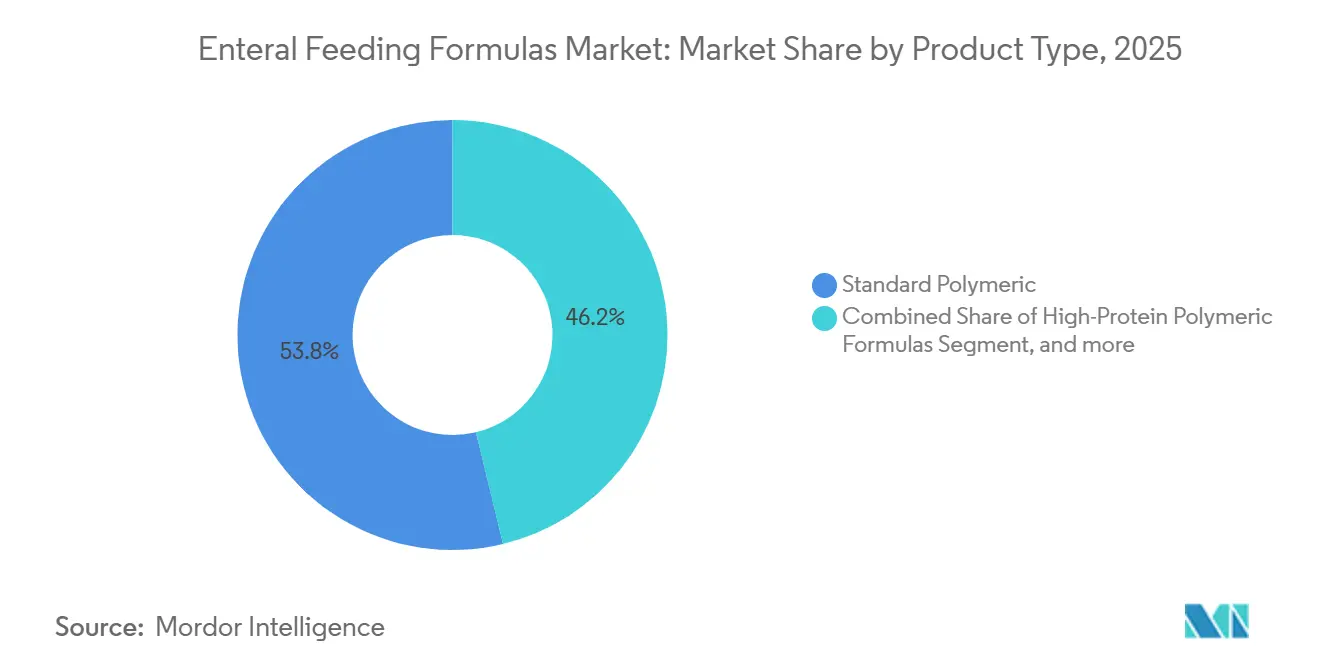

- By product type, standard polymeric formulas led with 53.78% of the enteral feeding formulas market share in 2025; blenderized real-food products are forecast to expand at a 7.54% CAGR through 2031.

- By caloric density, isocaloric blends captured 45.42% share of the enteral feeding formulas market size in 2025, while hypercaloric variants are advancing at a 7.88% CAGR over 2026-2031.

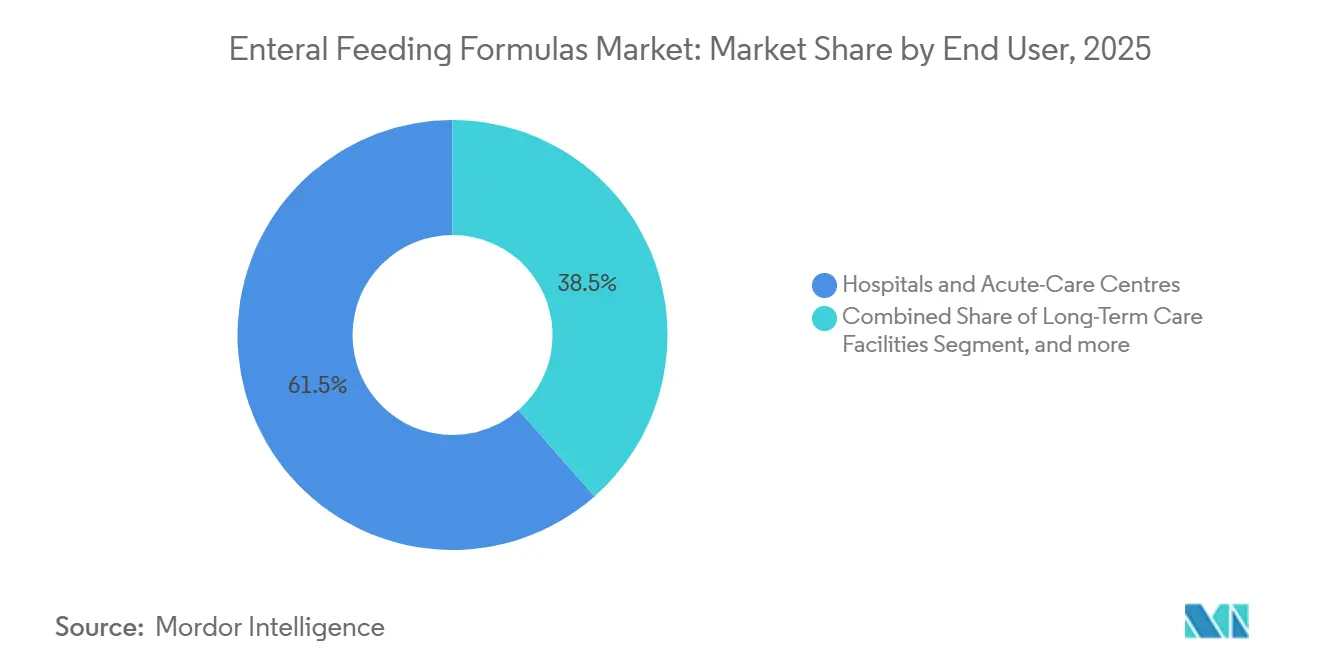

- By end user, hospitals and acute-care centers held 61.48% of the enteral feeding formulas market share in 2025, whereas home enteral nutrition is projected to grow at an 8.54% CAGR through 2031.

- By age group, adults accounted for 53.25% of consumption in 2025 and pediatric formulas are rising at an 8.32% CAGR through 2031.

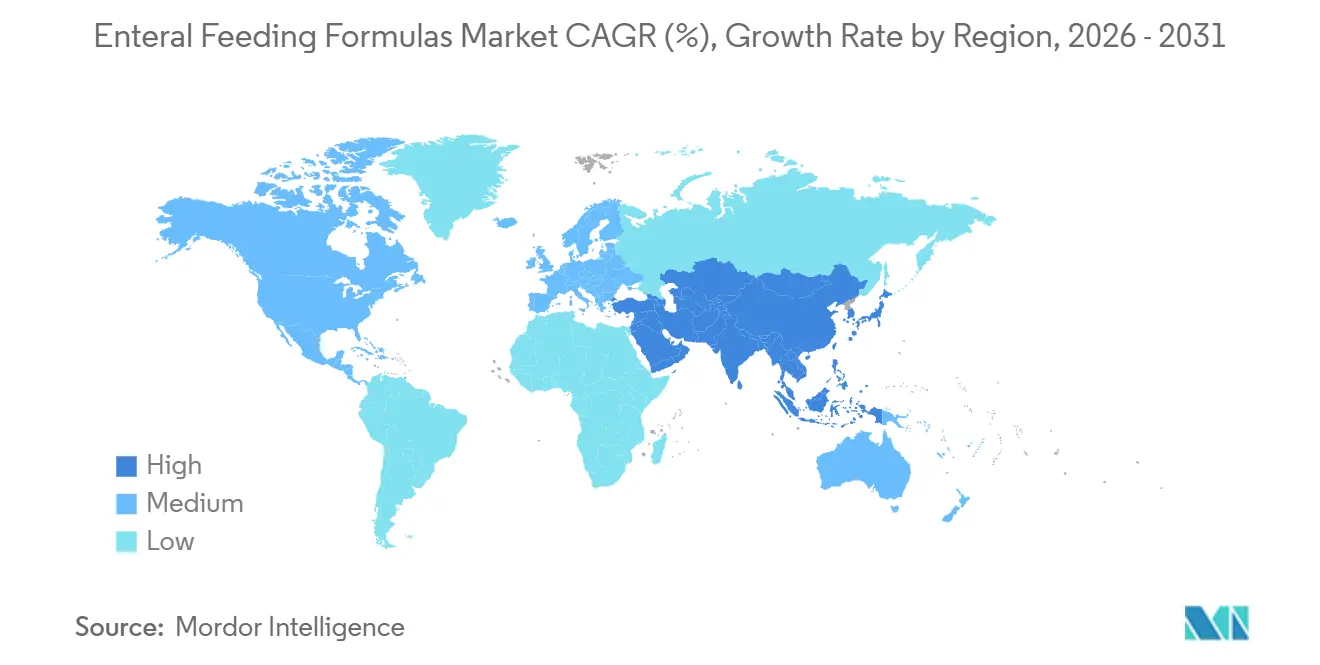

- By geography, North America dominated with 41.86% revenue share in 2025; Asia-Pacific is poised to record a 6.43% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enteral Feeding Formulas Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Chronic and Age-Related Diseases | +1.2% | Global, with acute impact in Japan, Europe, and North America | Long term (≥ 4 years) |

| Cost Advantage of Enteral Versus Parenteral Nutrition | +0.9% | Global, particularly North America, Europe, and emerging APAC markets | Medium term (2-4 years) |

| Expansion of Home Healthcare Infrastructure | +1.0% | North America and Europe core, expanding to urban APAC and Latin America | Medium term (2-4 years) |

| Technological Advancements in Enteral Pumps and Closed Systems | +0.7% | Global, with early adoption in North America and Western Europe | Short term (≤ 2 years) |

| Product Innovation in Disease-Specific and High-Protein Formulas | +0.8% | Global, with premium uptake in developed markets | Medium term (2-4 years) |

| Adoption of Value-Based Care and Outcome-Linked Reimbursement Models | +0.6% | North America and select European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic and Age-Related Diseases

The global population of people aged 70+ in 2024 was 494.4 million and is expanding steadily as life expectancy rises and fertility falls[1]United Nations, “World Population Prospects 2024,” un.org. Chronic ailments such as stroke, dementia, and cancer frequently impair swallowing or elevate metabolic demands, making long-term enteral feeding essential. Japan illustrates this trend, where citizens aged 65 + represent 29.1% of the population and dysphagia prevalence exceeds 50%. China has more than 280 million people aged 60+, and it is investing in geriatric care centers that routinely prescribe texture-modified formulas. Globally, non-communicable diseases now cause 74% of deaths, reinforcing demand for nutritionally complete formulas that lower complication risks.

Cost Advantage of Enteral Versus Parenteral Nutrition

Enteral regimens deliver nutrients at 30-50% lower cost than parenteral therapy because they avoid sterile compounding and the need for central venous access. Meta-analyses show that early tube feeding reduces bloodstream infections by 40% and shortens intensive-care stays by 2.3 days, saving USD 8,000-12,000 per patient. In 2025, the U.S. Centers for Medicare & Medicaid Services expanded bundled payments that reward hospitals for deploying cost-effective enteral protocols[2]Centers for Medicare & Medicaid Services, “Bundled Payments for Care Improvement,” cms.gov. Emerging health systems in Latin America and the Asia-Pacific are likewise adopting tube feeding to reduce overall treatment expenditure.

Expansion of Home Healthcare Infrastructure

Home enteral nutrition is growing at 8.54% as lightweight pumps and telehealth oversight let caregivers administer feeds safely outside hospitals. U.S. Medicare Part B covers formulas and supplies for permanent feeding-tube users, encouraging earlier discharge. European payers in Germany, France, and the United Kingdom have expanded reimbursement for home care, while Japan’s long-term care insurance subsidizes supplies for elders. Clinical trials confirm that home programs lower infection rates and reduce total care costs by about 40% compared with long-term facilities.

Technological Advancements in Enteral Pumps and Closed Systems

Mandatory ENFit connectors under ISO 80369-3 are minimizing misconnections that previously caused severe harm. The FDA issued 2024 guidance that accelerated adoption, triggering replacement demand for legacy sets. Closed systems have cut bacterial contamination by 60% in multicenter studies, while smart pumps notify users of occlusions in real time, easing nursing workload.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variable Reimbursement And Insurance Coverage Globally | -0.8% | Emerging APAC, MEA, Latin America; state-level variability in North America | Medium term (2-4 years) |

| Clinical Complications Such As Aspiration Pneumonia And GI Intolerance | -0.5% | Global, higher incidence in acute-care and long-term care settings | Short term (≤ 2 years) |

| Supply Chain Volatility For Medical-Grade Macronutrient Inputs | -0.4% | Global, more acute where dairy protein imports dominate | Medium term (2-4 years) |

| Limited Clinical Evidence For Emerging Plant-Based And Blenderized Formulas | -0.3% | North America and Europe initially, expanding into APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Variable Reimbursement and Insurance Coverage Globally

Coverage differs widely by country and insurer, limiting access in price-sensitive regions. U.S. Medicaid policies vary by state, sometimes requiring prior authorization that delays therapy. In India, the Ayushman Bharat scheme excludes enteral nutrition, forcing many families to self-fund[3]Government of India, “Ayushman Bharat scheme benefits,” india.gov.in. Out-of-pocket costs can exceed 50% of annual household income in several Latin American markets, thereby restricting the uptake of premium, disease-specific blends.

Clinical Complications Such as Aspiration Pneumonia and GI Intolerance

Aspiration pneumonias occur in 5-15% of tube-fed patients and carry mortality up to 65%, prompting cautious initiation, especially in ventilated or neurologically impaired cases. Gastrointestinal intolerance—diarrhea, constipation, bloating—affects up to 30% of recipients and often leads to feed interruptions. Although blenderized and fiber-enriched formulas improve tolerance, higher prices and patchy reimbursement hinder widespread substitution.

Segment Analysis

By Product Type: Whole-Food Formulas Reshape Synthetic Dominance

Standard polymeric blends controlled 53.78% of 2025 revenue, reflecting broad clinical familiarity and favorable payment status. Yet the enteral feeding formulas market is shifting as blenderized real-food options post a 7.54% CAGR, propelled by evidence of better bowel regularity and caregiver preference for recognizable ingredients. High-protein lines aimed at oncology and critical-care patients are rising, while peptide-based semi-elemental and elemental amino-acid variants are used for malabsorption or severe allergy cases. Disease-specific innovations, notably diabetes and renal formulas, command premium pricing through validated metabolic benefits. Plant-based entrants such as Kate Farms are winning share by replacing dairy proteins with pea isolates, reinforcing the perception that allergen-light compositions reduce intolerance.

A growing subset of immune-modulating products enriched with arginine and omega-3s is demonstrating 30% fewer postoperative infections, making them attractive despite higher unit costs. These shifts underscore a broader re-orientation of the enteral feeding formulas market toward differentiated formulations that address tolerance, metabolic control, and patient preferences simultaneously.

Note: Segment shares of all individual segments available upon report purchase

By Caloric Density: Hypercaloric Blends Meet Volume Constraints

Isocaloric offerings at 1.0 kcal/ml held 45.42% of segment revenue in 2025, but hypercaloric formats at 1.2-1.5 kcal/ml are tracking a 7.88% CAGR as clinicians seek to meet energy goals in fluid-restricted patients. Very-high-calorie products above 2.0 kcal/ml remain niche due to viscosity challenges that can occlude pumps. Manufacturers are lowering osmolality to curb diarrhea, broadening acceptance. This focus on concentrated nutrition aligns with shorter hospital stays and sicker inpatients who require rapid repletion, reinforcing growth prospects for dense blends in the enteral feeding formulas market.

By End-User: Home Settings Grow Fastest

Hospitals accounted for 61.48% of 2025 demand, yet home enteral programs are expanding at 8.54% as payers emphasize cost-effective after-care. Closed systems, combined with lightweight, Bluetooth-enabled pumps, are empowering lay caregivers, and telehealth reimbursement enables dietitians to adjust regimens remotely. Long-term care facilities remain steady buyers of geriatric dysphagia products, but the highest incremental volume through 2031 will stem from home settings, underscoring how the enteral feeding formulas industry is migrating closer to patients.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Pediatric Segment Leads Growth

Adults dominated consumption at 53.25% in 2025, reflecting cancer and trauma prevalence, yet pediatric formulas are registering the fastest rise at 8.32% CAGR. Exclusive enteral nutrition induces remission in up to 80% of pediatric Crohn’s disease cases, while neonatal feeds for preterm infants reduce the risk of necrotizing enterocolitis. Brands such as Nestlé Compleat Pediatric, which blend whole-food ingredients, have improved tolerance, further accelerating momentum in the enteral feeding formulas market.

Geography Analysis

North America generated 41.86% of global revenue in 2025 thanks to Medicare Part B coverage, advanced home-care networks, and value-based payment models that penalize readmissions. Canada shows province-level variation, whereas Mexico’s growth depends on public hospital investment and private insurance uptake.

Asia-Pacific is the fastest-growing region, with a 6.43% CAGR. Japan’s super-aged society and national long-term care insurance drive sustained demand for nutrient-dense formulas. China’s Healthy China 2030 roadmap is expanding medical-nutrition offerings across tertiary and community facilities. India’s urban private hospitals are early adopters, but high out-of-pocket costs still curb rural penetration.

Europe benefits from comprehensive national health systems that reimburse hospital and home feeds. Germany negotiates rates via sickness funds, France covers 100% for chronic disease, and the United Kingdom uses formularies that increasingly favor cost-effective blends. Southern European countries are broadening home support programs to relieve inpatient pressure.

Competitive Landscape

Abbott, Fresenius Kabi, and Nestlé Health Science anchor a moderately consolidated field, leveraging broad portfolios, global manufacturing facilities, and clinical datasets to meet reimbursement criteria. Abbott’s nutrition revenue reached USD 8.3 billion in 2023, buoyed by Ensure and Glucerna. Fresenius Kabi combines hospital channel strength with new FDA-cleared closed-system launches, while Nestlé has added plant-based and clean-label subsidiaries to address evolving consumer tastes.

Disruptors such as Kate Farms and Real Food Blends are carving out niches through plant-based proteins and blenderized recipes. Investor funding of USD 200 million positions Kate Farms for international expansion. Danone and Baxter are focusing on immune-modulating and hypercaloric innovations, respectively, aiming for differentiated efficacy claims that resonate in outcome-linked reimbursement climates. Technological edge—closed bags, ENFit compliance, antimicrobial tubing, and smart pump integration—is an escalating battleground across the enteral feeding formulas market.

Enteral Feeding Formulas Industry Leaders

Abbott Laboratories

Nestle SA

Reckitt Benckiser Group plc. (Mead Johnson)

Danone S.A.

Fresenius SE & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Alcresta Therapeutics, Inc., one of the leading commercial-stage company focused on developing and commercializing novel enzyme-based products announced that the U.S. Food and Drug Administration (FDA) has cleared expanded use of RELiZORB to now include patients of all ages including neonates and infants.

- January 2025: Otsuka Pharmaceutical Factory, In,c. launched "ENOSOLID Semi-Solid for Enteral Use". This product is a semi-solid enteric nutrition formula that appropriately contains major nutrients, vitamins, and trace elements based on the typical Japanese nutrition intake pattern.

Global Enteral Feeding Formulas Market Report Scope

As per the scope of the report, enteral feeding refers to the delivery of a nutritionally complete feed containing protein, carbohydrates, fat, water, minerals, and vitamins directly into the stomach, duodenum, or jejunum.

The Enteral Feeding Formulas Market Report is Segmented by Product Type (Standard Polymeric, High-Protein Polymeric, Peptide-Based, Elemental, Disease-Specific, Immune-Modulating, and Blenderized), Caloric Density (Low Energy, Isocaloric, Hypercaloric, and Very-High Calorie), End-User (Hospitals, Long-Term Care, Home Enteral Nutrition, and Outpatient Clinics), Age Group (Neonates, Pediatrics, Adults, and Geriatrics), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Standard Polymeric Formulas |

| High-Protein Polymeric Formulas |

| Peptide-Based / Semi-Elemental Formulas |

| Elemental (Amino-Acid) Formulas |

| Disease-Specific Formulas |

| Immune-Modulating / Synbiotic Formulas |

| Blenderized Real-Food Formulas |

| Low Energy (<1.0 kcal/ml) |

| Isocaloric (≈1.0 kcal/ml) |

| Hypercaloric (1.2–1.5 kcal/ml) |

| Very-High Calorie (≥2.0 kcal/ml) |

| Hospitals & Acute-Care Centres |

| Long-Term Care Facilities |

| Home Enteral Nutrition (HEN) |

| Out-Patient / Ambulatory Clinics |

| Neonates (0-28 Days) |

| Pediatrics (1 Month–17 Yrs) |

| Adults (18-64 Yrs) |

| Geriatrics (≥65 Yrs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Standard Polymeric Formulas | |

| High-Protein Polymeric Formulas | ||

| Peptide-Based / Semi-Elemental Formulas | ||

| Elemental (Amino-Acid) Formulas | ||

| Disease-Specific Formulas | ||

| Immune-Modulating / Synbiotic Formulas | ||

| Blenderized Real-Food Formulas | ||

| By Caloric Density | Low Energy (<1.0 kcal/ml) | |

| Isocaloric (≈1.0 kcal/ml) | ||

| Hypercaloric (1.2–1.5 kcal/ml) | ||

| Very-High Calorie (≥2.0 kcal/ml) | ||

| By End-User | Hospitals & Acute-Care Centres | |

| Long-Term Care Facilities | ||

| Home Enteral Nutrition (HEN) | ||

| Out-Patient / Ambulatory Clinics | ||

| By Age Group | Neonates (0-28 Days) | |

| Pediatrics (1 Month–17 Yrs) | ||

| Adults (18-64 Yrs) | ||

| Geriatrics (≥65 Yrs) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the enteral feeding formulas market be by 2031?

It is forecast to reach USD 12.44 billion, reflecting a 5.12% CAGR from 2026 to 2031.

Which segment is growing fastest by end-user?

Home enteral nutrition is advancing at 8.54% annually as payers shift care to lower-cost settings and portable pumps ease administration.

Why are hypercaloric blends gaining popularity?

Clinicians use 1.2-1.5 kcal/ml formulas to meet energy targets in fluid-restricted or critically ill patients, driving a 7.88% CAGR through 2031.

Which companies lead the field?

Abbott, Fresenius Kabi, and Nestlé Health Science collectively account for the largest global share, supported by broad portfolios and clinical data.

What is driving growth in Asia-Pacific?

Rapid demographic aging in Japan and China, plus expanding healthcare coverage, underpins the region's 6.43% CAGR outlook.