Endometriosis Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

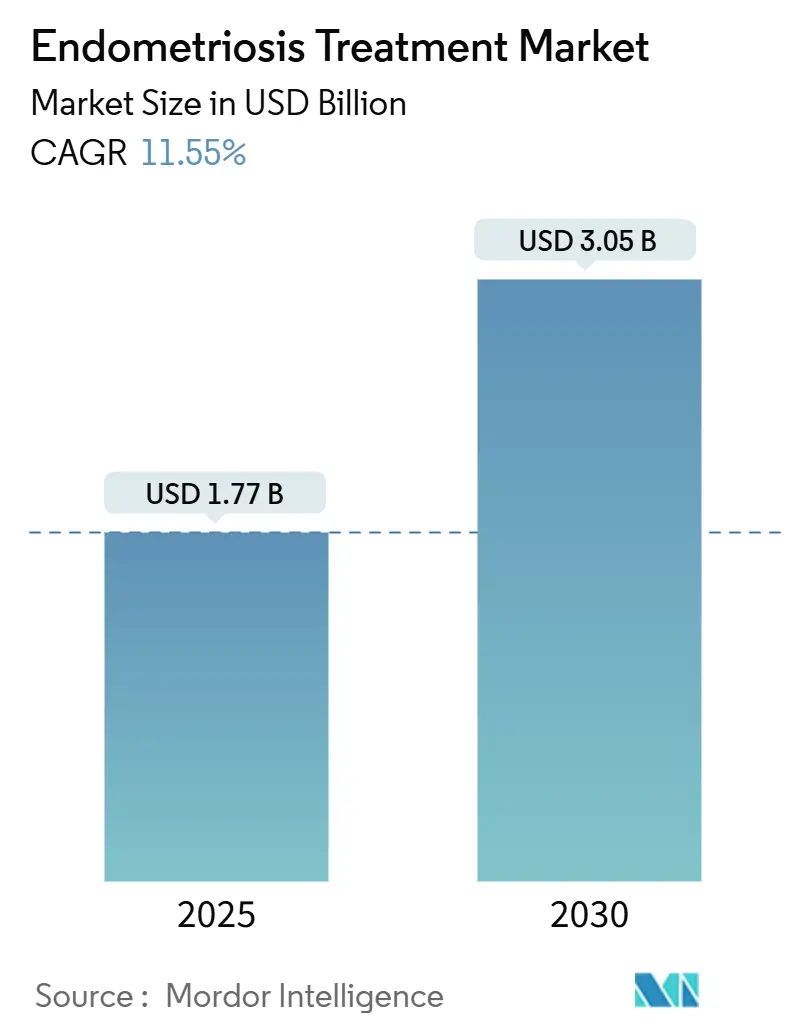

| Market Size (2025) | USD 1.77 Billion |

| Market Size (2030) | USD 3.05 Billion |

| Growth Rate (2025 - 2030) | 11.55% CAGR |

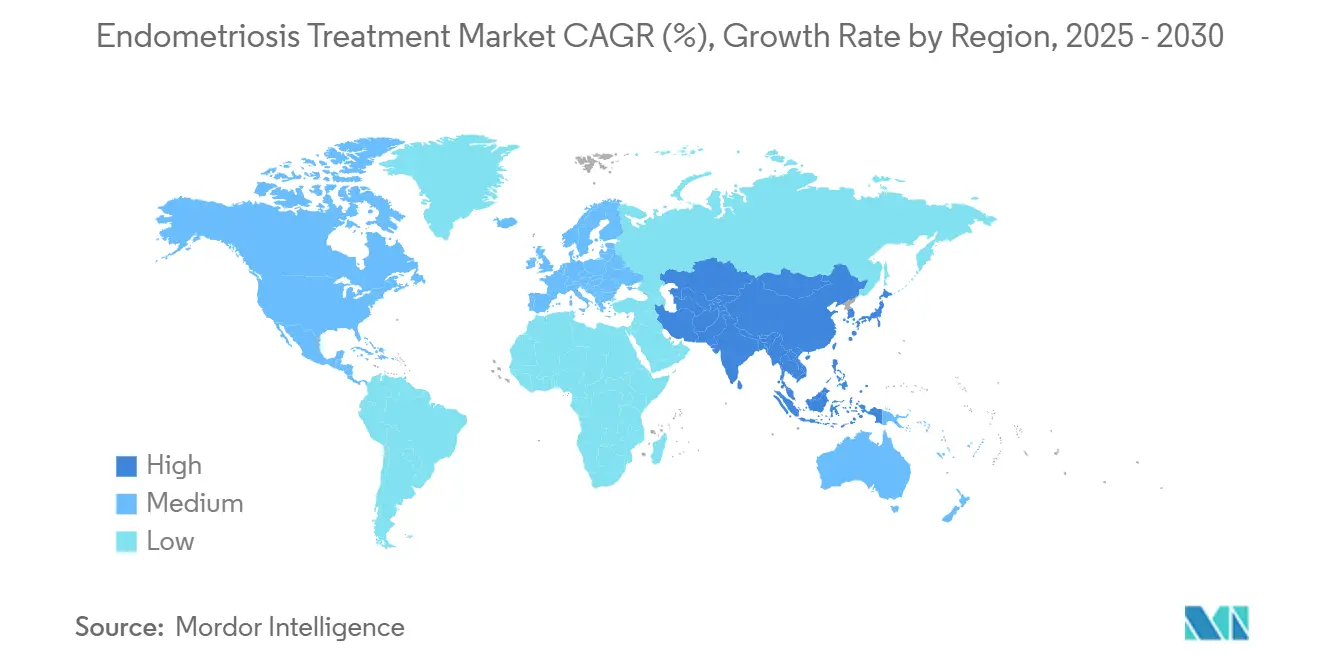

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Endometriosis Treatment Market Analysis by Mordor Intelligence

The Endometriosis Treatment Market size is estimated at USD 1.77 billion in 2025, and is expected to reach USD 3.05 billion by 2030, at a CAGR of 11.55% during the forecast period (2025-2030). Rising disease prevalence, sustained public-health campaigns, and a wave of regulatory approvals for oral gonadotropin-releasing hormone (GnRH) antagonists are setting a new treatment standard. Venture-capital inflows into non-hormonal pipelines, the proliferation of FemTech platforms, and government-funded action plans are expanding patient reach while reshaping competitive strategies. Meanwhile, diagnostic delays, high lifetime costs, and specialist shortages continue to temper uptake, steering innovators toward digital triage tools and minimally invasive care pathways that can bridge access gaps.

Key Report Takeaways

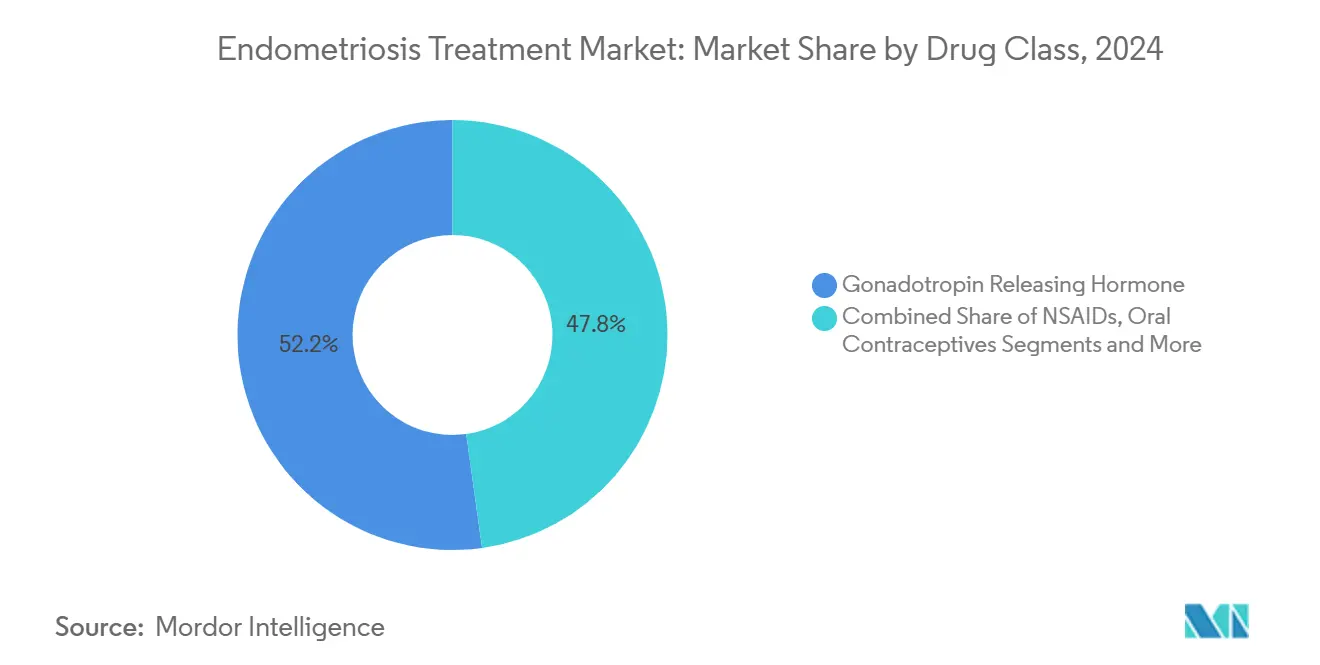

- By drug class, Gonadotropin-releasing hormone therapies led with 52.24% of Endometriosis treatment market share in 2024; oral contraceptives are on track for the fastest 12.43% CAGR to 2030.

- By endometriosis type, superficial peritoneal disease accounted for 42.29% revenue share in 2024, whereas deeply infiltrating disease is projected to advance at an 11.87% CAGR through 2030.

- By treatment type, hormone therapy held 68.62% in 2024; pain-management drugs show the highest 12.34% CAGR to 2030.

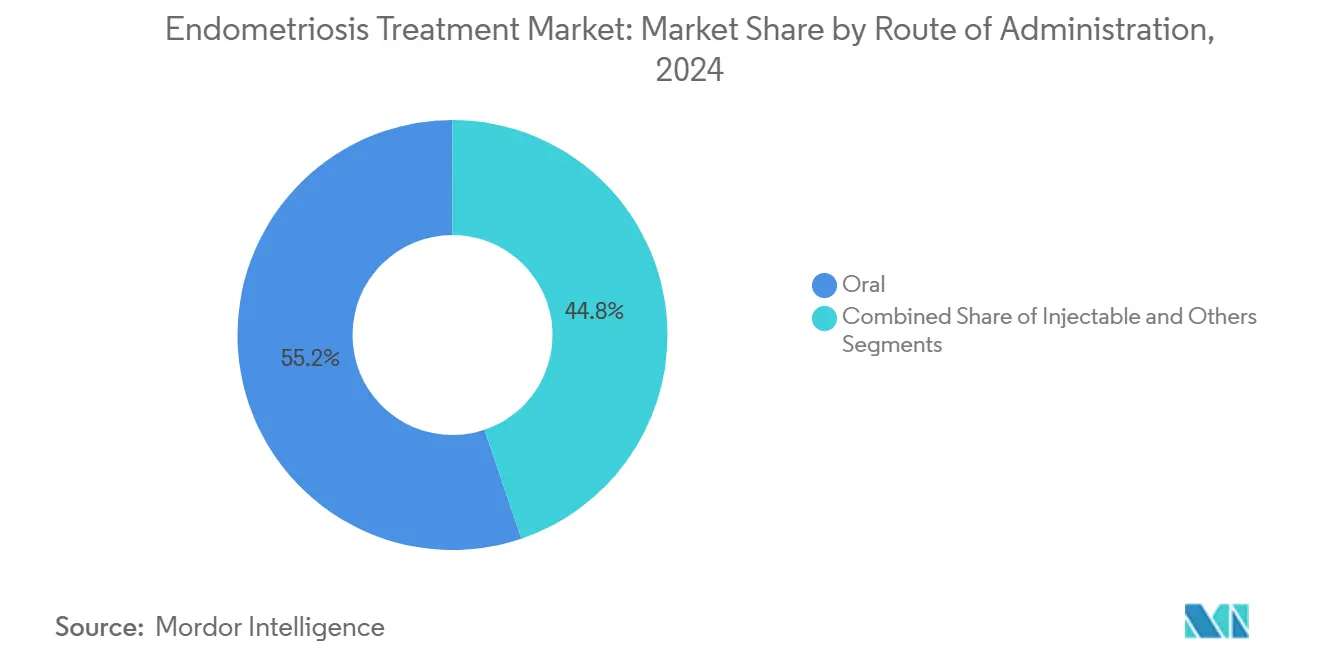

- By route of administration, oral products captured 55.18% in 2024, while injectables are poised for an 11.96% CAGR to 2030.

- By distribution channel, hospital pharmacies claimed 44.95% in 2024; online pharmacies are expanding at 12.74% CAGR through 2030.

- By geography, North America retained 42.13% share in 2024, whereas Asia-Pacific is forecast to grow at a 13.23% CAGR to 2030.

Global Endometriosis Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Among Reproductive-Age Women | +2.1% | Global, with highest impact in Asia-Pacific | Long term (≥ 4 years) |

| Growing Awareness and Earlier Diagnosis Initiatives | +1.8% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Launch of GnRH Antagonist Class | +2.3% | Global, led by developed markets | Short term (≤ 2 years) |

| Surge in FemTech Remote-Monitoring Platforms | +1.4% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Venture Funding for Non-Hormonal R&D Pipelines | +1.6% | Global, concentrated in US and Europe | Long term (≥ 4 years) |

| Government Endometriosis Action Plans | +1.2% | Australia, UK, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Among Reproductive-Age Women

More than 190 million women now live with endometriosis worldwide, and prevalence among Asian populations stands near 15%, markedly higher than the 5–10% range reported in Western cohorts. The demographic trend toward delayed parenthood, coupled with urban lifestyle shifts, is enlarging the at-risk population base in emerging markets. Productivity losses and excess healthcare utilization frame a USD 200 billion global economic burden that has prompted pharmaceutical enterprises to create dedicated women’s-health divisions. Environmental research linking phthalate exposure to symptom aggravation is incentivizing new metabolic and environmental-medicine approaches. Stakeholders are intensifying epidemiological surveillance to quantify sub-regional hotspots, a strategy expected to refine market-entry decisions over the long term.

Growing Awareness and Earlier Diagnosis Initiatives

Public-sector outreach is compressing the historic seven-year diagnostic lag. Australia’s National Action Plan, backed by AUD 87.19 million, is scaling specialist GP clinics and patient-education programs. The World Health Organization’s 2024 declaration elevating endometriosis to priority-condition status has galvanized policy harmonization and insurance-coding revisions across Europe and North America. Digital symptom trackers such as Lyv’s app flag high-risk profiles and direct users toward specialist care, with machine-learning algorithms boosting triage accuracy.[1]Source: Hélène Antier, “Lyv révolutionne la prise en charge de l'endométriose,” Lyv, lyv.app Medical-school curricula are integrating endometriosis modules for the first time, a move likely to diminish misdiagnosis and under-treatment. Collectively, these measures are enlarging the treated population and stimulating prescription volumes.

Launch of GnRH Antagonist Class

Oral antagonists have re-defined the treatment ladder by combining robust efficacy with convenient dosing. In pivotal trials, 75% of women receiving relugolix combination therapy attained clinically meaningful pain relief versus 27–30% in placebo arms. Bone-density safety advantages over earlier agonists enable treatment extensions up to 24 months, aligning therapy duration with the chronic course of disease. Regulatory green lights across the United States, Japan, and Australia have accelerated physician adoption, while pipeline candidates like linzagolix hint at further gains in tolerability. The Endometriosis treatment market is therefore witnessing rapid formulary placement and expanded reimbursement activity, reinforcing top-line growth for GnRH innovators.

Surge in FemTech Remote-Monitoring Platforms

Remote-care solutions are mitigating specialist shortages by bringing evidence-based management into patients’ homes. The CANKADO platform records over 80% acceptance for electronic health assessments, outperforming paper-based alternatives in usability scores.[2]Source: Nina Maindal et al., “Digital mindfulness-based intervention for endometriosis,” BMC Women’s Health, bmcwomenshealth.biomedcentral.com Teleconsultation providers including Visana Health combine pain-tracking, diet coaching, and virtual gynecological visits, broadening access for rural users. Wearable sensors feed real-world evidence into pharmaceutical post-marketing studies, opening ancillary revenue channels. Predictive analytics modules forecast pain flares, helping patients adjust medication timing and improve quality-of-life indices. The resulting patient-level datasets are forging partnerships between software firms and drug makers keen to secure competitive differentiation through integrated care ecosystems.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Lifetime Treatment and Surgery Cost Burden | -1.8% | Global, most severe in developing markets | Long term (≥ 4 years) |

| Adverse Effects / Bone-Density Loss from Long-Term Hormone Use | -1.2% | Developed markets with aging populations | Medium term (2-4 years) |

| Racial and Socio-Economic Disparities in Prescription Access | -0.9% | North America, expanding awareness globally | Long term (≥ 4 years) |

| Limited Specialist Surgeons Driving Wait-Times > 12 Months | -1.4% | Global, most acute in rural and developing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Lifetime Treatment and Surgery Cost Burden

Median patient spending rises from USD 4,318 in the pre-diagnosis phase to USD 17,230 within six months post-diagnosis, a 300% escalation that strains household budgets and payer systems.[3]Source: American College of Obstetricians and Gynecologists, “Endometriosis Analysis: Current Healthcare Utilization and Costs,” greenjournal.org Coverage gaps for therapies priced above USD 1,000 per month intensify inequities, although value-based contracts and manufacturer assistance funds are partly offsetting out-of-pocket exposure. Surgical recurrence rates approaching 40% within five years add repeat procedure costs, while emergency-room visits occur 60% more frequently than in matched controls. These dynamics deter aggressive management and may limit near-term uptake of premium therapies despite demonstrable clinical benefits.

Limited Specialist Surgeons Driving Wait-Times to More Than 12 Months

The shortage of fellowship-trained excision surgeons leads to year-long queues in many regions, compounding disease progression and psychosocial stress. Telehealth consults championed by the Endometriosis Foundation of America show promise yet hinge on reliable broadband infrastructure, which remains patchy in rural communities. Minority groups face even longer waits and complication rates nearly double those of White and Asian patients. Robotic-assisted techniques and expanded residency rotations aim to accelerate skill dissemination, but the complexity of advanced excision continues to cap annual surgeon output. Consequently, many patients default to pain management alone, limiting full therapeutic penetration.

Segment Analysis

By Drug Class: GnRH Dominance Faces Oral-Contraceptive Challenge

Gonadotropin-releasing hormone therapies captured 52.24% of Endometriosis treatment market share in 2024, buoyed by the blockbuster entry of oral antagonists that removed injection barriers and delivered superior symptom control. Robust payer acceptance in North America and Europe sustained premium pricing, reinforcing revenue leadership. However, oral contraceptives are accelerating at a 12.43% CAGR as younger patients prioritize fertility preservation and lower adverse-event profiles. Market expansion is additionally shaped by NSAIDs providing first-line pain relief despite limited disease-modifying effect. The shift toward combination regimens that temper hypoestrogenic side effects is fostering strategic alliances between hormonal and non-hormonal developers, signaling an impending competitive re-balancing.

Looking ahead, innovation pipelines spotlight prolactin-receptor antagonists, metabolic modulators, and cannabinoid formulations, all of which promise disease control without systemic hormone suppression. Clinical momentum around agents such as HMI-115 and dichloroacetate could diversify therapeutic options, ultimately reducing the class risk faced by GnRH incumbents. Should bone-density concerns remain manageable, the Endometriosis treatment market is expected to maintain a heterogeneous portfolio that caters to symptom severity, fertility intent, and co-morbid profile.

Note: Segment shares of all individual segments available upon report purchase

By Endometriosis Type: Deeply Infiltrating Disease Drives Innovation

Superficial peritoneal lesions constituted 42.29% of diagnosed cases in 2024, benefiting from earlier detection through routine laparoscopy. Improved imaging protocols have simultaneously elevated recognition of deeply infiltrating disease, which is advancing at an 11.87% CAGR on the back of refined MRI staging and specialized surgical techniques. Pharmaceutical sponsors are stratifying clinical trials by lesion depth to document differential efficacy across phenotypes.

Endometriomas maintain steady surgical volumes due to high recurrence risk, yet non-invasive modalities such as high-intensity focused ultrasound and targeted nanoparticle ablation are under investigation. Rare extrapelvic manifestations, though numerically small, are receiving newfound attention through precision-diagnostic initiatives, offering a test-bed for biomarker-based treatment assignment. Cross-type data integration is anticipated to refine prognostic algorithms and inform future regulatory submissions.

By Treatment Type: Hormonal Therapy Leads Despite Pain-Management Upsurge

Hormonal approaches dominated 68.62% of 2024 revenue as chronic inflammation necessitated systemic suppression. Extended-duration approvals for Myfembree and other antagonists strengthened adherence levels, translating to recurring sales. Pain-management drugs, however, are expanding at 12.34% CAGR, reflecting payer and provider efforts to minimize opioid reliance through mechanism-specific analgesics and neuromodulation devices.

Multimodal protocols combining low-dose hormones with targeted analgesia are gaining guideline traction. Metabolic and immune-modulating candidates aspire to deliver disease modification sans endocrine impact, a proposition that could erode hormonal share over the forecast horizon. Nonetheless, the proven efficacy and established reimbursement of hormonal regimens will likely preserve near-term dominance in the Endometriosis treatment market.

By Route of Administration: Injectable Growth Challenges Oral Dominance

Oral formulations held 55.18% in 2024 thanks to patient convenience, rapid dose titration, and broad primary-care familiarity. Depot injectables are climbing at an 11.96% CAGR as monthly or quarterly regimens enhance compliance for individuals struggling with daily dosing. Pipeline long-acting depots promise further mileage, especially within populations with work-schedule constraints.

Intrauterine and transdermal systems address niche scenarios requiring topical hormone delivery, while nanoparticle-enabled targeting aspires to localize drug action and mitigate systemic exposure. Digital-health integration enables adherence monitoring across administration routes, giving clinicians real-time insight into dosing fidelity and therapeutic response.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Pharmacies Disrupt Traditional Models

Hospital pharmacies retained 44.95% of prescription value in 2024, reflecting specialist-led initiation protocols and intensive monitoring during therapy start-up. Online pharmacies, propelled by telemedicine uptake, are growing at 12.74% CAGR, delivering discreet fulfilment and broadening access in stigma-laden cultural contexts.

Retail outlets maintain a foothold for over-the-counter NSAIDs but face limitations when dispensing controlled or specialty hormonal products. Emerging specialty pharmacies focused on women’s health bundle nurse counseling, bone-density check scheduling, and adherence reminders, creating high-touch ecosystems that appeal to both payers and patients.

Geography Analysis

North America commanded 42.13% of 2024 revenue, buoyed by advanced reimbursement frameworks, strong advocacy networks, and early adoption of oral GnRH antagonists. The Biden administration’s USD 200 million investment in women’s-health research is fast-tracking precision-medicine conduits. Yet insurance disparities persist, with Black patients receiving fewer prescriptions for endometriosis-related pain and comorbid conditions, highlighting an ongoing equity challenge. Telehealth is narrowing rural gaps, although infrastructure gaps restrain full penetration.

Asia-Pacific is the fastest-growing arena, advancing at a 13.23% CAGR through 2030 on the back of healthcare system expansion, urban migration, and heightened awareness campaigns. Prevalence standing near 15% underscores a large untreated pool that modern fertility trends continue to enlarge. Harmonized regulatory pathways in Japan, South Korea, and Australia are shortening approval cycles, while China’s integration of traditional herbal protocols with pharmaceutical regimens offers culturally attuned care models. Strategic collaborations between multinational firms and local manufacturers are scaling distribution across tier-two cities.

Europe retains a mature demand profile characterized by broad access but constrained national health budgets. The European Medicines Agency streamlines drug access across member states, yet divergent reimbursement policies can lengthen country-level launch timelines. Brexit continues to complicate regulatory alignment between the United Kingdom and continental Europe, prompting companies to maintain dual submission strategies. Middle East and Africa show incremental gains driven by rising private insurance coverage and emerging center-of-excellence programs in the Gulf. South America, led by Brazil, is rolling out centralized procurement models that lower therapy costs and stimulate uptake.

Competitive Landscape

Market concentration remains moderate. AbbVie, Pfizer/Myovant, and Bayer dominate the GnRH landscape through Orilissa and Myfembree, bolstered by expansive trial datasets and direct-to-consumer outreach. Relugolix’s once-daily regimen with estradiol add-back confers compliance and bone-density advantages, sustaining physician preference over agonist predecessors. Patent portfolios covering novel formulations, dosing algorithms, and combination therapies fortify barriers to entry.

Disruptive biotech entrants are redrawing the field. Hope Medicine’s HMI-115 achieved a 42% dysmenorrhea reduction in Phase 2, positioning it as a first-in-class non-hormonal candidate that preserves ovulation. Gynica’s cannabinoid-based intra-vaginal delivery platform and Temple Therapeutics’ phenotype-specific compounds target underserved patient subsets. Digital-diagnostic innovators such as Hera Biotech and Aditxt are forging payer alliances to expedite coverage of fast, non-invasive tests, potentially moving diagnosis from surgical theaters to primary-care settings.

Strategic partnerships marry deep R&D pipelines with commercial muscle. Large pharmaceutical firms seek equity stakes and co-development agreements to hedge against hormonal-therapy obsolescence. Ecosystem models combining drug, diagnostic, and digital monitoring components are emerging as a route to lock in patient lifetime value while differentiating beyond molecule attributes.

Endometriosis Treatment Industry Leaders

-

Bayer AG

-

Pfizer Inc.

-

AbbVie Inc.

-

Teva Pharmaceutical Industries

-

AstraZeneca

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NHS England approved once-daily relugolix–estradiol–norethisterone therapy, branded Ryeqo, for symptomatic treatment of endometriosis.

- May 2024: Gynica began Phase 1 trials for S-301 and S-302 cannabinoid formulations delivered via its IntraVag system at Careggi University Hospital.

- March 2024: Scotland launched the first clinical program evaluating dichloroacetate as a metabolic therapy for endometriosis.

- February 2024: Australia’s TGA cleared Ryeqo, the first oral therapy approved nationally for endometriosis pain.

Global Endometriosis Treatment Market Report Scope

As per the scope of the report, endometriosis is a medical condition in which tissues similar to the endometrium grow in ovaries and fallopian tubes. It can affect women of all ages, including teenagers, and cause pain or infertility. The endometriosis treatment market is segmented by type, treatment type, end user, and geography. By type, the market is segmented into superficial peritoneal endometriosis, endometriomas, deeply infiltrating endometriosis, and other types. By treatment type, the market is segmented into pain medication and hormone therapy. By end user, the market is segmented into hospitals, specialty clinics, and other end users. The report also covers the market sizes and forecasts for the endometriosis treatment market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| NSAIDs |

| Oral Contraceptives |

| Gonadotropin Releasing Hormone |

| Other Drug Classes |

| Superficial Peritoneal Endometriosis |

| Endometriomas |

| Deeply Infiltrating Endometriosis |

| Other Types |

| Pain Management Drugs |

| Hormone Therapy |

| Oral |

| Injectable |

| Others |

| Hospital Pharmacies |

| Retail and Drugstores |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | NSAIDs | |

| Oral Contraceptives | ||

| Gonadotropin Releasing Hormone | ||

| Other Drug Classes | ||

| By Endometriosis Type | Superficial Peritoneal Endometriosis | |

| Endometriomas | ||

| Deeply Infiltrating Endometriosis | ||

| Other Types | ||

| By Treatment Type | Pain Management Drugs | |

| Hormone Therapy | ||

| By Route of Administration | Oral | |

| Injectable | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail and Drugstores | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Endometriosis treatment market and how fast is it growing?

The Endometriosis treatment market stands at USD 1.77 billion in 2025 and is projected to climb to USD 3.049 billion by 2030, translating to an 11.55% CAGR.

Which drug class holds the largest share today?

GnRH-based therapies hold the lead with 52.24% of 2024 revenue, supported by the rapid uptake of oral antagonists such as relugolix combination therapy.

Which region offers the fastest growth opportunity?

Asia-Pacific carries a forecast CAGR of 13.23% through 2030, driven by higher prevalence, improving diagnostic capacity, and expanding healthcare infrastructure.

What are the main cost barriers for patients?

Lifetime expenditures can rise from USD 4,318 pre-diagnosis to USD 17,230 within six months of diagnosis, and monthly therapy costs may exceed USD 1,000 without adequate insurance coverage.

How are digital health solutions influencing the market?

FemTech platforms deliver remote symptom tracking, teleconsultations, and e-pharmacy integration, enhancing access for rural patients and generating real-world data that inform drug development.

Are non-hormonal treatments on the horizon?

Yes, candidates such as HMI-115 (prolactin-receptor antagonist) and dichloroacetate are in clinical phases, aiming to provide disease control without systemic hormone suppression.

Page last updated on: