Market Trends of Emission Control Catalysts Industry

This section covers the major market trends shaping the Emission Control Catalysts Market according to our research experts:

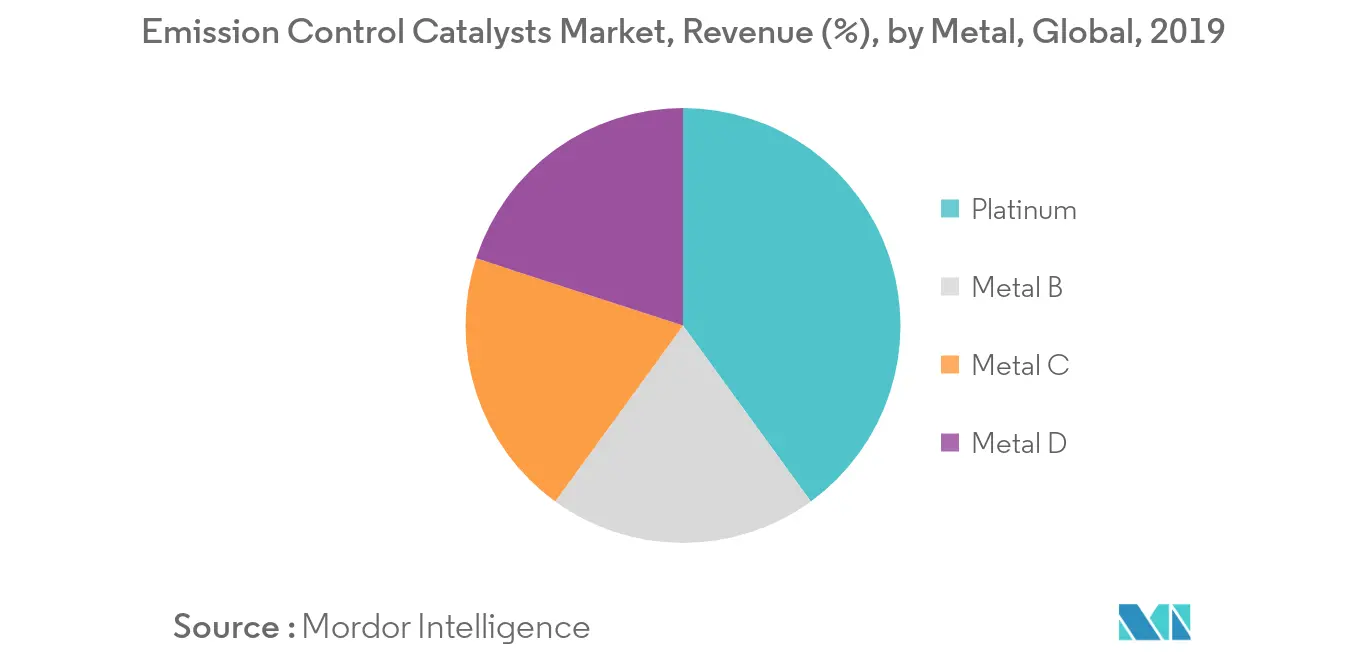

Platinum - The Most used Metal

- Platinum is the most widely used metal for emission control applications, since it improves combustion.

- Improved combustion helps to reduce emissions and enhance the catalyst's performance.

- Since, platinum is effective under oxygen-rich conditions, it is used widely for diesel applications.

- Furthermore, platinum offers several other advantages, such as:

- It has a high melting point, thereby providing thermal durability.

- It possesses excellent oxidation activity at low temperatures.

- It is effective against sulfur compounds and helps in reducing the sulfur content in crude oil, in the refineries.

- It can be efficiently recycled.

- Sources, such as, automobiles, refinery & petrochemical complexes, chemical industries, oil and natural gas processing plants, and pharmaceutical industries, among others, are discovering an increasing number of applications of platinum-based emission control catalysts.

Understand The Key Trends Shaping This Market

Download PDF

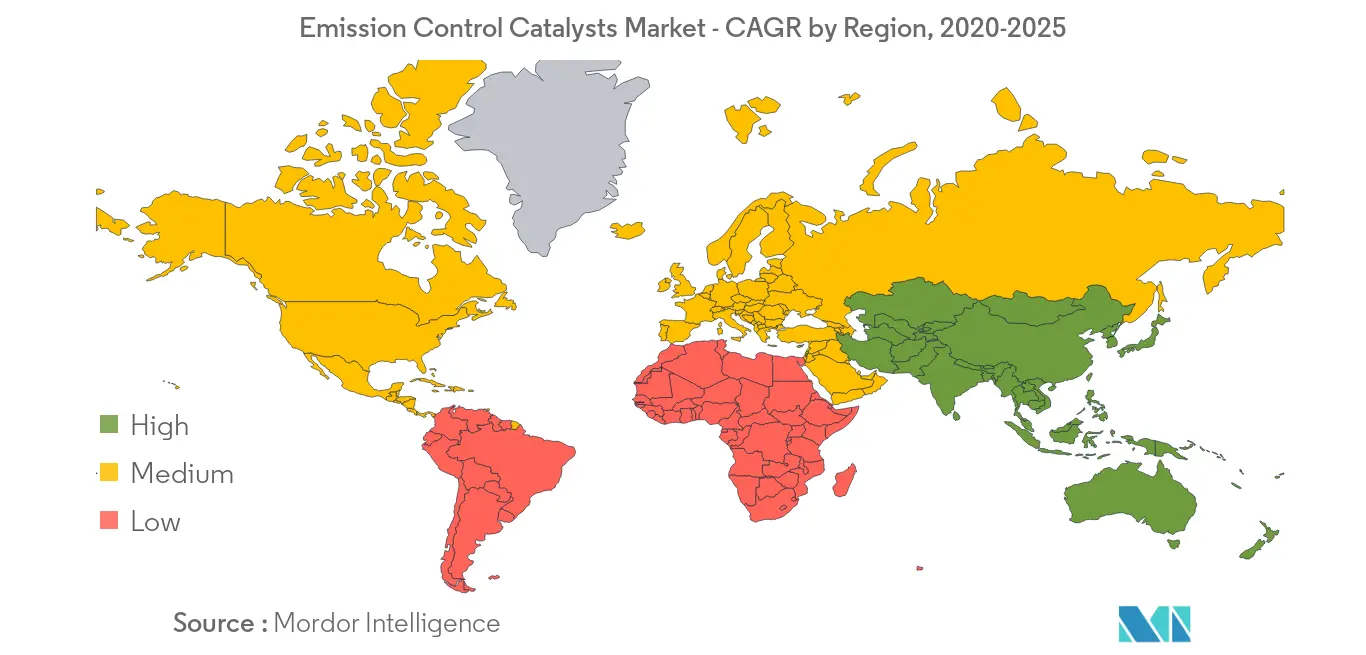

China to Dominate the Asia-Pacific Market

- China is one of the fastest growing economies, globally. Furthermore, almost all the end-user industries have been witnessing growth, owing to the growing population, living standards, and per capita income.

- China is a hub for chemical processing, accounting for a major chunk of the chemicals produced globally. The country contributes more than 35% of the global chemical sales. The chemical industry is another prominent end-user industry in China. Many major companies in the market have their chemical plants in China. With the growing demand for various chemicals, globally, the demand for emission control catalysts from this sector is projected to grow during the forecast period.

- Moreover, the Chinese automotive manufacturing industry is the largest in the world. Though the industry witnessed a slowdown in 2018, wherein the production and sales declined. Similar trend continued, with the production witnessing a 7.5% decline in 2019. According to the China Association of Automobile Manufacturers (CAAM), automotive production is expected to decline by about 2% in the end of 2020.

- The 'Made in China 2025' initiative aims to support in upgrading the existing low-cost mass production to higher value-added advanced manufacturing. The 'Automobile Mid and Long-Term Development Plan' was released in the April 2017, with an objective to make China a strong auto power in the next ten years. This growth in the automotive industry is likely to increase the consumption of emission control catalysts in the industry.

- However, due the onset of COVID-19, the economic growth of China now seems to contract by a considerable extent in 2020. Many manufacturing and associated activities have already taken a hit in early 2020, and the economic situation is expected to remain dire, if the manufacturing activities are not set back on track by mid-2020

Get Analysis on Important Geographic Markets

Download PDF