| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 4.41 Billion |

| Market Size (2030) | USD 5.41 Billion |

| CAGR (2025 - 2030) | 4.20 % |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

EMEA Secondary Macronutrients Market Analysis

The EMEA Secondary Macronutrients Market size is estimated at USD 4.41 billion in 2025, and is expected to reach USD 5.41 billion by 2030, at a CAGR of 4.2% during the forecast period (2025-2030).

The EMEA secondary macronutrients market is experiencing significant transformation driven by the increasing emphasis on sustainable and organic farming practices. Agricultural operations across the region are witnessing a paradigm shift toward environmentally conscious farming methods, with a notable rise in organic certification requirements for fertilizer nutrients products. This trend is exemplified by the recent approval of products like polysulfate for organic farming by both the EU and USDA certification bodies, demonstrating the industry's adaptation to changing consumer preferences. The growing awareness of soil nutrient health and environmental impact has led to increased adoption of balanced plant nutrition management practices, particularly in European countries where regulatory frameworks actively promote sustainable agriculture.

Technological advancement and innovation in fertilizer formulations are reshaping the industry landscape. Manufacturers are developing sophisticated blending techniques to create customized solutions that combine secondary macronutrients with other essential nutrients. A significant development in this direction is demonstrated by the 2022 strategic partnership between K+S and Cinis Fertilizer, which aims to produce up to 600,000 tons of synthetic potassium sulfate annually, showcasing the industry's move toward more efficient and sustainable production methods. The integration of digital farming tools, such as the Farm Sustainability Tool for Nutrients (FaST), is revolutionizing agricultural nutrients management practices across the region.

The market is witnessing a notable shift in distribution and supply chain dynamics, with companies focusing on establishing robust regional networks to ensure consistent product availability. Major industry players are expanding their production capabilities and forming strategic alliances to strengthen their market presence. The industry has seen significant investments in infrastructure development, particularly in production facilities across Europe and the Middle East, aimed at meeting the growing demand for secondary macronutrients. This expansion is complemented by the development of specialized logistics networks designed to handle the unique requirements of different fertilizer formulations.

The evolution of farming practices and changing crop patterns are significantly influencing market dynamics. Based on recent agricultural surveys in Britain, approximately 35% of crops and grass received sulfur dressing, indicating the growing recognition of secondary macronutrients' importance in modern agriculture. Farmers are increasingly adopting precision agriculture techniques, leading to more targeted and efficient use of secondary macronutrients. This trend is particularly evident in the cultivation of high-value crops and in regions with intensive farming practices, where the optimization of soil nutrient usage has become crucial for maintaining soil fertility and ensuring sustainable crop yields.

EMEA Secondary Macronutrients Market Trends

Rising Production of High-Quality Crops and the Need for Sustainable Agricultural Development Drive the Market

The increasing demand for crop nutrition is leading to a growing dependency on secondary macronutrients for food grain production due to high population gains in the EMEA region. The nutrient load per unit area is rising steadily due to limited arable land used for food production, thereby decreasing nutrient efficiency in the soil profile and creating a higher demand for secondary macronutrient fertilizers. This situation is particularly evident in countries like Egypt and Spain, which are major producers of vegetable crops in the EMEA region, with Egypt producing over 15,420 thousand metric tons and Spain producing approximately 13,259 thousand metric tons of vegetables annually.

The excessive and continuous usage of agricultural land has decreased soil nutrient content, reducing crop production capabilities across EMEA countries. In the agriculture industry, magnesium fertilizer is increasingly being included as a fertilizer in the soil to correct magnesium deficiency, particularly for cash crops and vegetables. Plant nurseries are showing high demand for magnesium-rich soil to create appropriate conditions for the efficient development of potted plants. Furthermore, secondary nutrient fertilizers provide flexible options for applications, including pre-plant, starter, side-dress, and fertigation, making them compatible with pesticides and thus driving their adoption among farmers seeking better crop yields.

Understand The Key Trends Shaping This Market

Download PDF

Secondary Macronutrients Ensure Healthy Plant Growth

Agricultural practices have significantly evolved in EMEA countries, with consumer preferences for high-quality food products gaining prominence. Though required in small quantities, plant macronutrients are proving highly effective in ensuring the healthy growth of plants. The presence of calcium fertilizer in plants helps provide the necessary structural support for the plant cell, while magnesium fertilizer is essential for photosynthesis as it stimulates the enzymes required for plant growth. Sulfur, also necessary in moderate quantities, helps plants develop chlorophyll and protein synthesis, making it crucial for overall plant health and development.

Studies conducted by the Michigan State University Extension have found that plants endure nutrient deficiencies when secondary macronutrients are not available in adequate quantities in the soil. This can be attributed to the usage of high levels of primary fertilizers in the soil. Changes in soil pH, as well as differences in soil temperature, also reduce the plant's uptake of nutrients, leading to calcium and magnesium deficiency in soils. According to the UAE Ministry of Environment and Water (MOEW) and Environmental Agency - Abu Dhabi, the soil conditions in many EMEA regions are among the most challenging in the world, with increasing salinization, sand violation, waterlogging, and loss of productive topsoil driving the need for secondary macronutrient supplementation.

Rising Key Players' Initiatives

Major players in the EMEA secondary macronutrients market are enhancing their existing product lines by blending elemental sulfur fertilizer, calcium, and magnesium with other fertilizers to improve the yield of the resulting blended fertilizers. In a significant development, K+S signed a letter of intent with the Swedish company Cinis Fertilizer to cooperate in the synthetic production of potassium sulfate (SOP). Under this agreement, K+S will supply Cinis Fertilizer with its entire potassium chloride (MOP) requirements and, in return, purchase up to 600,000 tons of potassium sulfate (SOP) per year.

The industry is witnessing increased innovation in product development and strategic partnerships. For instance, ICL company's product polysulfate received approval for use in organic farming, with both its standard and granular grades getting accredited by the EU and USDA as organic fertilizers. Additionally, Saudi Basic Industries Corporation (SABIC) has developed an innovative product called urea calcium sulfate (UCS), which is the first of its kind fertilizer product that uses by-product calcium sulfate. These initiatives by key players are not only expanding the market but also promoting sustainable agricultural practices through the development of more efficient and environmentally friendly secondary macronutrient products.

Segment Analysis: Nutrient Type

Sulfur Segment in EMEA Secondary Macronutrients Market

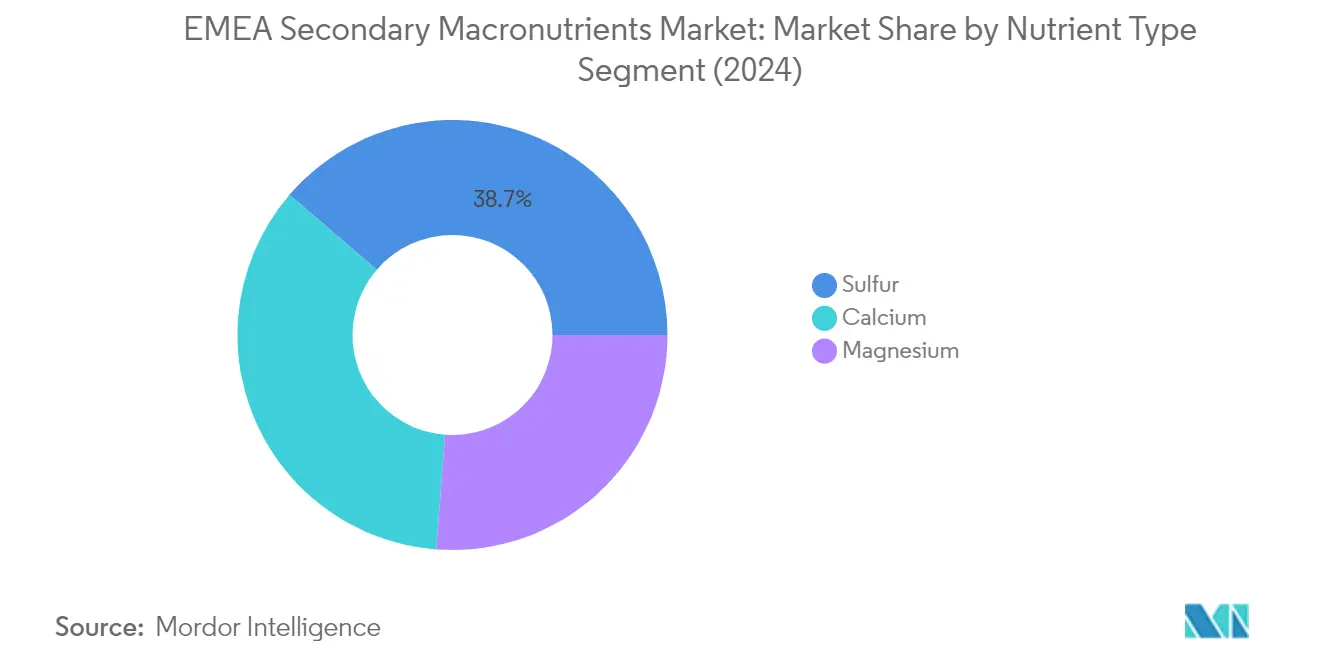

The sulfur fertilizer segment continues to dominate the EMEA secondary macronutrients market, holding approximately 39% market share in 2024. This significant market position is attributed to sulfur's critical role as the fourth major nutrient essential for plant growth and development. Sulfur is particularly vital for the formation of proteins, amino acids, and oils, serving as a structural component of protoplasm. The segment's dominance is further strengthened by the increasing adoption of sulfur fertilizer in major agricultural regions across Europe and the Middle East, where it is extensively used for crops like oilseed rape, cereals, and various high-value crops. The growing recognition of sulfur's role in improving crop quality and yield, particularly in regions with sulfur-deficient soils, has maintained its position as the leading secondary macronutrient in the market.

Calcium Segment in EMEA Secondary Macronutrients Market

The calcium fertilizer segment is emerging as the fastest-growing category in the EMEA secondary macronutrients market, projected to grow at approximately 5% from 2024 to 2029. This accelerated growth is driven by the increasing awareness among farmers about calcium's crucial role in plant cell wall development and overall crop health. The segment's growth is particularly notable in intensive farming regions where calcium deficiency has become a significant concern for crop productivity. The expansion of protected cultivation practices, especially in greenhouse farming across European countries, has further boosted the demand for calcium fertilizer. Additionally, the rising adoption of precision farming techniques and the growing focus on fruit and vegetable production, where calcium plays a vital role in fruit quality and shelf life, are contributing to the segment's rapid growth trajectory.

Remaining Segments in Nutrient Type

The magnesium fertilizer segment completes the nutrient type segmentation, playing a crucial role in the EMEA secondary macronutrients market. Magnesium's significance stems from its essential function in photosynthesis and chlorophyll formation, making it indispensable for overall plant health and development. The segment has maintained steady growth due to its critical role in enzyme activation and protein synthesis in plants. Magnesium deficiency has become increasingly recognized as a limiting factor in crop production across various EMEA regions, particularly in intensive farming systems. The segment's growth is supported by the agricultural sector's increasing focus on balanced crop nutrition and the rising adoption of magnesium-enriched fertilizer products in both traditional and modern farming practices.

Segment Analysis: Application Method

Liquid Segment in EMEA Secondary Macronutrients Market

The liquid application segment dominates the EMEA secondary macronutrients market, holding approximately 61% market share in 2024. This significant market position is primarily driven by the high adoption of fertigation and foliar applications across the EMEA region. Liquid application methods are particularly preferred by farmers due to their superior efficacy and reduced labor costs compared to other application methods. The segment's popularity is further enhanced by its versatility in application methods, including fertigation, which is the most extensively adopted method, followed by foliar application. The liquid segment's dominance is also attributed to its ability to provide uniform nutrient distribution, better nutrient absorption by plants, and increased flexibility in application timing. Additionally, the segment is experiencing robust growth and is projected to expand at nearly 5% CAGR from 2024 to 2029, driven by increasing adoption of precision farming techniques and modern irrigation systems across the region.

Solid Segment in EMEA Secondary Macronutrients Market

The solid application segment continues to maintain a significant presence in the EMEA secondary macronutrients market, serving as a traditional and reliable method of nutrient application. This segment is particularly important in regions with limited access to advanced irrigation systems or where conventional farming practices remain prevalent. Solid fertilizers offer advantages such as longer nutrient release periods and easier storage and transportation capabilities. The segment's stability is supported by its widespread use in commercial hydroponic systems, where solid macronutrient fertilizers are preferred due to their customizability according to plant needs. Furthermore, solid fertilizers play a crucial role in indoor cultivation practices and are particularly valued in areas where controlled-release fertilization is required for optimal crop management.

Segment Analysis: Crop Type

Grains and Cereals Segment in EMEA Secondary Macronutrients Market

The grains and cereals segment continues to dominate the EMEA secondary macronutrients market, commanding approximately 43% of the total market share in 2024. This significant market position is driven by the extensive cultivation of cereal crops across Europe, particularly in countries like France, Germany, and the United Kingdom. The segment's dominance is attributed to the critical role of secondary plant nutrients in preventing diseases and disorders in crops like rice and wheat. Calcium-rich fertilizers are particularly essential for developing good root systems in paddy crops, while magnesium compounds are crucial for cereal crops, especially during the early growing season when their shallow root systems cannot access nutrients from deeper soil layers. The increasing focus on maximizing yields in limited arable areas has led farmers to better understand the importance of secondary plant nutrients alongside primary nutrients, contributing to the segment's sustained market leadership.

Fruits and Vegetables Segment in EMEA Secondary Macronutrients Market

The fruits and vegetables segment is emerging as the fastest-growing category in the EMEA secondary macronutrients market, projected to grow at approximately 5% during the forecast period 2024-2029. This robust growth is primarily driven by the increasing demand for high-quality fruits and vegetables in the Middle East region, where soil conditions necessitate extensive use of plant macronutrients. Calcium has become particularly crucial for major fruits and vegetables including apples, citrus, carrots, potatoes, lettuce, and tomatoes. The segment's growth is further supported by research findings showing improved quality and yield in orange trees through calcium nitrate fertilizer application. Additionally, the application of sulfur in potato cultivation has shown significant benefits in nitrogen stabilization and protein formation, while magnesium applications are becoming increasingly common in similar quantities as sulfur for optimal crop development.

Remaining Segments in Crop Type

The other significant segments in the EMEA secondary macronutrients market include pulses and oilseeds, turf and ornamentals, and other crop types. The pulses and oilseeds segment plays a vital role in the market, particularly due to the high sulfur requirements in oilseed crops for protein synthesis and vitamin production. The turf and ornamental segment has carved out its niche in the market, driven by the increasing demand for aesthetic landscaping and the growing recognition of calcium's importance in promoting vigorous plant growth and healthy foliage. Other crop types, including commercial crops like cotton and date palms, contribute to the market's diversity by requiring specific combinations of secondary macronutrients for optimal growth and yield enhancement.

EMEA Secondary Macronutrients Market Geography Segment Analysis

EMEA Secondary Macronutrients Market in Europe

Europe dominates the EMEA secondary macronutrients market due to expanding agricultural practices and increasing requirements for high-quality agricultural produce. The region has witnessed significant developments in farming technologies and sustainable agricultural practices. Countries like France, Germany, and the United Kingdom have been at the forefront of adopting advanced fertilization techniques. The market in Europe is primarily driven by the large use of secondary macronutrient fertilizers in cereal crop production, coupled with growing health awareness and increasing consumption of plant-sourced foods.

EMEA Secondary Macronutrients Market in France

France leads the European secondary macronutrients market with its extensive agricultural sector and advanced farming practices. The country has witnessed a recent trend of customized fertilizers that provide site-specific nutrient management by achieving maximum fertilizer use efficiency. The implementation of the Farm Sustainability Tool for nutrients (FaST) has revolutionized how farmers manage nutrient applications. France holds approximately 32% market share in the European region, making it the largest market. The country's focus on sustainable agriculture and precision farming techniques has contributed significantly to its market dominance.

EMEA Secondary Macronutrients Market in Spain

Spain demonstrates the highest growth potential in the European region, with an expected growth rate of approximately 5% during 2024-2029. The country's agricultural sector, particularly in crops like wheat, barley, vegetables, tomatoes, olives, and citrus fruits, has shown increasing adoption of secondary macronutrients. Spanish farmers are increasingly demanding high-quality cultivars and agricultural chelates to overcome soil deficiency problems. The implementation of new regulations for sustainable nutrition of agricultural soils has further accelerated market growth. The country's Mediterranean climate and diverse agricultural landscape provide optimal conditions for the application of secondary macronutrients.

EMEA Secondary Macronutrients Market in the Middle East

The Middle East region has emerged as a significant market for secondary macronutrients, driven by the need to enhance agricultural productivity in challenging climatic conditions. The region's focus on food security and self-sufficiency has led to increased investments in agricultural technologies and nutrients. Countries across the Middle East are actively working to overcome their natural limitations in agriculture through advanced fertilization techniques.

EMEA Secondary Macronutrients Market in Saudi Arabia

Saudi Arabia dominates the Middle East secondary macronutrients market with approximately 29% market share. The country's position is strengthened by its significant sulfur production capabilities and the presence of major fertilizer companies. Saudi Arabia's ambitious agricultural development programs and focus on achieving self-sufficiency in food security have driven the market growth. The country has also made significant strides in developing innovative fertilizer products, particularly in combining secondary macronutrients with other essential nutrients.

EMEA Secondary Macronutrients Market in the United Arab Emirates

The United Arab Emirates shows the highest growth trajectory in the Middle East region, with a projected growth rate of approximately 5% during 2024-2029. The country's focus on advanced agricultural technologies and sustainable farming practices has created a strong demand for secondary macronutrients. The UAE's efforts to overcome its challenging soil conditions and climate limitations through innovative agricultural solutions have contributed to this growth. The country's investment in research and development of agricultural technologies has further strengthened its position in the regional market.

EMEA Secondary Macronutrients Market in Africa

The African market for secondary macronutrients is characterized by growing agricultural modernization and increasing awareness about soil nutrient management. The region faces unique challenges in terms of soil quality and agricultural productivity, driving the demand for secondary macronutrients. Various countries in the region are focusing on improving their agricultural output through better nutrient management practices.

EMEA Secondary Macronutrients Market in South Africa

South Africa leads the African secondary macronutrients market, benefiting from its well-established agricultural sector and advanced farming practices. The country's commercial farming sector demonstrates frequent use of fertilizer nutrients, supported by regular soil analysis and corrective measures. South Africa's diverse agricultural landscape, including major crops like maize, wheat, and sugarcane, has created sustained demand for secondary macronutrients.

EMEA Secondary Macronutrients Market in Nigeria

Nigeria exhibits the strongest growth potential in the African region, driven by its expanding agricultural sector and increasing focus on crop yield optimization. The country's efforts to improve agricultural productivity, particularly in regions like the Northern Nigerian Savanna, have spurred the demand for secondary macronutrients. Nigeria's adoption of modern farming techniques and increasing awareness about balanced plant nutrition requirements has positioned it as a key growth market in the region.

Get Analysis on Important Geographic Markets

Download PDF

EMEA Secondary Macronutrients Industry Overview

Top Companies in EMEA Secondary Macronutrients Market

The EMEA secondary macronutrients market is characterized by the strong presence of established players like K+S Company, Yara International ASA, EuroChem Group AG, and Israel Chemical Company, who have demonstrated consistent market leadership. These companies have been actively pursuing product innovations, particularly in developing enhanced fertilizer blends incorporating elemental sulfur, calcium, and magnesium to improve yield effectiveness. Operational agility has been evident through strategic partnerships, such as collaborations for synthetic production and distribution agreements to expand market reach. Companies have shown commitment to expansion through new production facilities, particularly in Russia and France, while also focusing on research and development to create sustainable and environmentally friendly solutions. The market has witnessed significant strategic moves, including long-term supply agreements, technology partnerships, and investments in organic farming certifications to meet evolving customer demands.

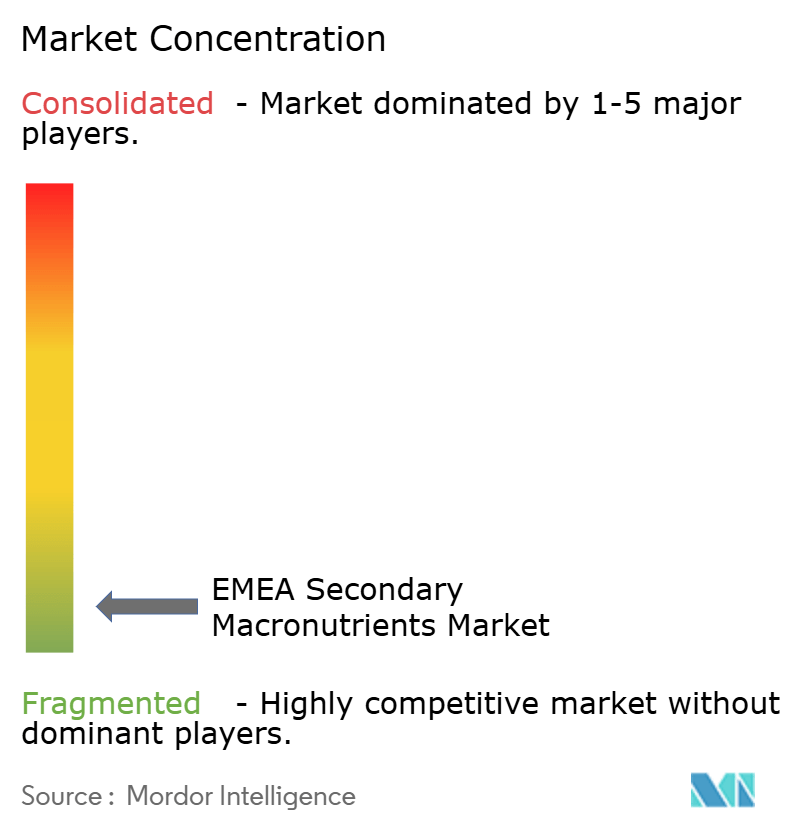

Fragmented Market with Strong Regional Players

The competitive landscape exhibits a fragmented structure with major players holding approximately one-quarter of the market share, while numerous regional and local players constitute the remaining portion. Global conglomerates like Yara International and EuroChem maintain significant influence through their extensive distribution networks and technological capabilities, while regional specialists such as Saudi United Fertilizer Company and SAF Sulphur Company leverage their local market knowledge and specialized product portfolios. The market demonstrates moderate consolidation tendencies, with established players maintaining their positions through strong brand recognition, technical expertise, and well-established customer relationships.

The merger and acquisition landscape has been relatively active, with companies pursuing strategic acquisitions to strengthen their market presence and expand their geographical footprint. Notable transactions include the acquisition of Al Takamul National Agriculture Company, which demonstrates the industry's focus on vertical integration and operational synergies. Companies are increasingly pursuing partnerships and joint ventures rather than outright acquisitions, particularly in emerging markets, to minimize risks while gaining market access and sharing technological expertise.

Innovation and Sustainability Drive Future Success

For incumbent players to maintain and expand their market share, focus needs to be placed on developing innovative product formulations that address specific regional crop requirements while meeting sustainability criteria. Companies must invest in research and development to create differentiated products, strengthen their distribution networks, and build strong relationships with farming communities. The increasing emphasis on organic farming and environmental protection necessitates the development of eco-friendly solutions, while digital technologies and precision agriculture present opportunities for value-added services and customer engagement.

Contenders looking to gain ground in the market must focus on niche segments and underserved regions while building strong local partnerships and distribution networks. The high concentration of end-users in the agricultural sector presents both opportunities and risks, making it crucial for companies to diversify their product applications and end-user base. The threat of substitution from organic alternatives and potential regulatory changes regarding fertilizer usage and environmental protection requires companies to maintain flexible business models and invest in sustainable solutions. Success in this market increasingly depends on the ability to provide comprehensive crop nutrition solutions while adapting to changing agricultural practices and environmental regulations. The integration of agricultural nutrients and fertilizer nutrients is essential for companies aiming to enhance their offerings in the secondary macronutrients sector. Additionally, incorporating agricultural minerals and plant supplements can further diversify product portfolios and meet the evolving demands of the agricultural industry.

EMEA Secondary Macronutrients Market Leaders

-

Yara International ASA

-

EuroChem Group AG

-

K+S Company

-

Al-tayseer Chemical Industry

-

Haifa Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

EMEA Secondary Macronutrients Market News

- March 2023: Syngenta and ICL signed an agreement to strengthen their existing partnership, which has contributed to innovation, investment, and service improvements in the turf industry.

- June 2022: K+S signed a letter of intent with the Swedish company CinisFertilizer to cooperate with the synthetic production of potassium sulfate (SOP). This implies that K+S is to supply CinisFertilizer with its entire potassium chloride (MOP) requirements and in return purchase up to 600,000 metric tons of potassium sulfate (SOP) per year from Cinis.

EMEA Secondary Macronutrients Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Secondary Macronutrients Ensure Healthy Plant Growth

- 4.2.2 Rising Key Players Initiatives

- 4.2.3 Crop Diversification in the Region

-

4.3 Market Restraints

- 4.3.1 Increasing Usage of Primary Nutrients Fertilizers

- 4.3.2 Increased Demand for Organic Agriculture In EMEA Countries

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Nutrient Type

- 5.1.1 Sulfur

- 5.1.2 Calcium

- 5.1.3 Magnesium

-

5.2 Application Method

- 5.2.1 Solid

- 5.2.2 Liquid

-

5.3 Crop Type

- 5.3.1 Grains And Cereals

- 5.3.2 Pulses And Oilseeds

- 5.3.3 Fruits And Vegetables

- 5.3.4 Turfs And Ornamentals

- 5.3.5 Other Crop Types

-

5.4 Geography

- 5.4.1 Europe

- 5.4.1.1 Germany

- 5.4.1.2 United Kingdom

- 5.4.1.3 France

- 5.4.1.4 Italy

- 5.4.1.5 Spain

- 5.4.1.6 Russia

- 5.4.1.7 Rest of Europe

- 5.4.2 Middle East

- 5.4.2.1 United Arab Emirates

- 5.4.2.2 Saudi Arabia

- 5.4.2.3 Kuwait

- 5.4.2.4 Egypt

- 5.4.2.5 Rest of Middle East

- 5.4.3 Africa

- 5.4.3.1 South Africa

- 5.4.3.2 Morocco

- 5.4.3.3 Nigeria

- 5.4.3.4 Rest of Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

-

6.3 Company Profiles

- 6.3.1 Al-tayseer Chemical Industry

- 6.3.2 Yara International ASA

- 6.3.3 Eurochem Group AG

- 6.3.4 K+S Company

- 6.3.5 Saudi United Fertilizer Company (al-asmida)

- 6.3.6 ICL

- 6.3.7 SAF Sulphur Company

- 6.3.8 Haifa Group

- 6.3.9 Trade Corporation International SA

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

EMEA Secondary Macronutrients Industry Segmentation

Magnesium (Mg), sulfur (S), and calcium (Ca) are considered secondary macronutrients as they are less commonly yield limiting than the primary macronutrients (P, N, and K), yet are required by crops in relatively larger amounts. The EMEA secondary macronutrients market is segmented by Nutrient Type (Sulphur, Calcium, and Magnesium), Application Method (Solid, and Liquid), Crop Type (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, Turfs and Ornamentals, and Other Crop Types), and Geography (Europe, Middle East, and Africa). The report offers the market size and forecasts in terms of value (USD) for all the above segments.

| Nutrient Type | Sulfur | ||

| Calcium | |||

| Magnesium | |||

| Application Method | Solid | ||

| Liquid | |||

| Crop Type | Grains And Cereals | ||

| Pulses And Oilseeds | |||

| Fruits And Vegetables | |||

| Turfs And Ornamentals | |||

| Other Crop Types | |||

| Geography | Europe | Germany | |

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Middle East | United Arab Emirates | ||

| Saudi Arabia | |||

| Kuwait | |||

| Egypt | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Morocco | |||

| Nigeria | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

EMEA Secondary Macronutrients Market Research Faqs

How big is the EMEA Secondary Macronutrients Market?

The EMEA Secondary Macronutrients Market size is expected to reach USD 4.41 billion in 2025 and grow at a CAGR of 4.20% to reach USD 5.41 billion by 2030.

What is the current EMEA Secondary Macronutrients Market size?

In 2025, the EMEA Secondary Macronutrients Market size is expected to reach USD 4.41 billion.

Who are the key players in EMEA Secondary Macronutrients Market?

Yara International ASA, EuroChem Group AG, K+S Company, Al-tayseer Chemical Industry and Haifa Group are the major companies operating in the EMEA Secondary Macronutrients Market.

Which is the fastest growing region in EMEA Secondary Macronutrients Market?

Middle East and Africa is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in EMEA Secondary Macronutrients Market?

In 2025, the Europe accounts for the largest market share in EMEA Secondary Macronutrients Market.

What years does this EMEA Secondary Macronutrients Market cover, and what was the market size in 2024?

In 2024, the EMEA Secondary Macronutrients Market size was estimated at USD 4.22 billion. The report covers the EMEA Secondary Macronutrients Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the EMEA Secondary Macronutrients Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

EMEA Secondary Macronutrients Market Research

Mordor Intelligence provides a comprehensive analysis of the secondary macronutrients market. We leverage deep expertise in agricultural nutrients and plant nutrition research. Our extensive report examines the complete spectrum of essential nutrients. It focuses on secondary plant nutrients, including applications of sulfur fertilizer, calcium fertilizer, and magnesium fertilizer. This analysis covers crucial soil amendment practices and evolving plant macronutrients requirements across the EMEA region. The report is available as an easy-to-download report PDF.

Stakeholders across the value chain benefit from detailed insights into crop nutrition trends, soil nutrient dynamics, and agricultural minerals development. The report provides actionable intelligence on specialty fertilizer innovations and crop micronutrients applications. It also examines the effectiveness of plant supplements and strategies for optimizing fertilizer nutrients. Our analysis supports strategic decision-making in crop fertilizer development and implementation. It offers valuable perspectives on sustainable agricultural practices and market evolution, all in an accessible format.