Market Size of EMEA Satellite Antenna Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

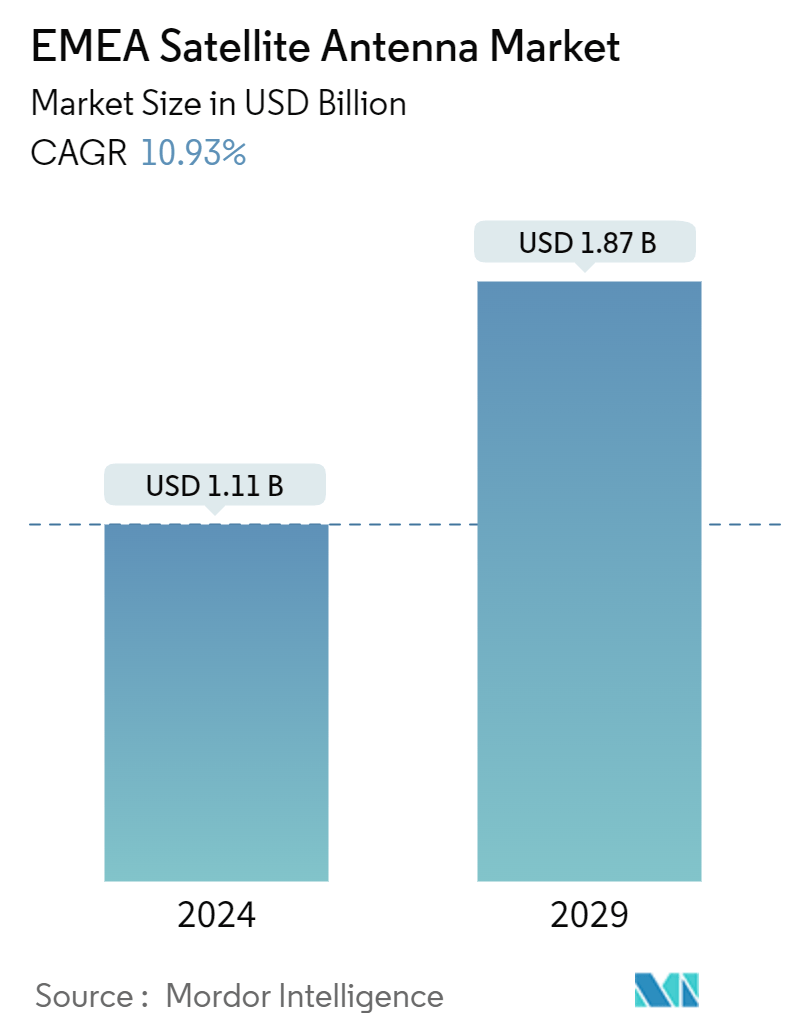

| Market Size (2024) | USD 1.11 Billion |

| Market Size (2029) | USD 1.87 Billion |

| CAGR (2024 - 2029) | 10.93 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

EMEA Satellite Antenna Market Analysis

The EMEA Satellite Antenna Market size is estimated at USD 1.11 billion in 2024, and is expected to reach USD 1.87 billion by 2029, growing at a CAGR of 10.93% during the forecast period (2024-2029).

- The EMEA satellite antenna market is experiencing significant growth, driven by the growing demand for high-speed wireless connectivity. This demand is significantly increasing with the deployment of 5G and the anticipation of 6G networks. 5G satellite communication supports improving mobile broadband services. This technology is used in mission-critical communications that provide low latency and uninterrupted network availability for applications like autonomous vehicles, remote control of critical infrastructure, etc.

- The market is witnessing advancements like flat panels, interoperable, and mobile communication. The rising adoption of electronically steered antennas (ESA) in aerospace and defense presents lucrative growth avenues for industry participants. In March 2024, Hanwha Phasor, a UK-based satellite communications company, announced the upcoming Phasor L3300B land antenna for mobile communications. The Phasor L3300B, an active electronically steered antenna (AESA), is tailored for commercial and military applications. Its main feature is maintaining seamless communication since it facilitates dual simultaneous receive channels. This allows the antenna to establish connections with new satellites without interrupting its current link.

- According to the 5G Infrastructure Public Private Partnership (PPP), a joint initiative by the European Commission and the European ICT Industry, Europe was midway through its 5G journey in 2023. While 5G coverage reached 72% penetration, it is important to note that this figure includes non-standalone deployments. However, the full-scale commercial implementation of 5G, especially in industrial settings, is still on the horizon, promising significant revenue potential.

- As per the GSMA report 2024, many new 5G markets, primarily in developing regions such as Africa (highlighting Ethiopia and Ghana), are set to launch their networks. Moreover, 5G adoption in sub-Saharan Africa was under 1% in 2023; projections indicate a substantial rise, aiming for 17%, catering to 234 million connections by 2030.

- The market faces challenges from the high costs of phased array and electronically steered antennas, alongside regulatory hurdles limiting antenna growth. Meeting regulatory standards and obtaining licenses poses a challenge for manufacturers, particularly for companies operating across diverse regulatory landscapes. Adhering to these standards not only adds complexity but also increases costs for antenna manufacturers.

- The pandemic accelerated the shift toward remote and hybrid work, amplifying the need for reliable internet connectivity for managing work even from remote areas. Additionally, the rise of telehealth services that require robust communication networks is well supported by satellite technologies.

EMEA Satellite Antenna Industry Segmentation

The EMEA satellite antenna market tracks the revenue accrued from the sale of satellite antenna devices/equipment for communication purposes in various application areas offered by market vendors in Europe, the Middle East, and Africa (EMEA) region. Satellite antennas are primarily used to provide communication paths with other satellites, as well as with the earth stations. A typical satellite antenna consists of three main components: antenna structure, beam-forming network, and feed system.

The EMEA satellite antenna report is segmented by frequency band (C band, K/KU/KA band, S and L band, X band, VHF and UHF band, and other frequency bands), antenna type (flat panel antenna, parabolic reflector antenna, horn antenna, fiberglass reinforced plastic antenna, iron antenna with mold stamping, and other antenna types), application (space, land, maritime, and airborne) and country (the United Kingdom, Germany, France, Saudi Arabia, the United Arab Emirates, South Africa, and the Rest of EMEA). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Antenna Type | |

| Flat Panel Antenna | |

| Parabolic Reflector Antenna | |

| Horn Antenna | |

| Fiberglass Reinforced Plastic Antenna | |

| Iron Antenna With Mold Stamping | |

| Other Antenna Types |

| By Application | |

| Space | |

| Land | |

| Maritime | |

| Airborne |

| By Country | |

| United Kingdom | |

| Germany | |

| France | |

| Saudi Arabia | |

| UAE | |

| South Africa |

EMEA Satellite Antenna Market Size Summary

The EMEA satellite antenna market is poised for substantial growth, driven by the increasing demand for high-speed wireless connectivity, particularly with the rollout of 5G and the anticipated 6G networks. This demand is further fueled by advancements in satellite communication technologies, such as flat panels and electronically steered antennas, which are gaining traction in sectors like aerospace and defense. The market is characterized by significant investments in developing solutions to enhance satellite military communication, with countries like Germany and Italy increasing their military expenditures to adopt new technologies. The compact size and advanced capabilities of flat-panel antennas are particularly appealing for applications in marine connectivity and military operations, ensuring reliable communication in remote and challenging environments.

Germany plays a pivotal role in the EMEA satellite antenna market, supported by a robust aerospace and satellite communication industry. The country's demand for broadband communications is on the rise, driven by the need for uninterrupted connectivity across various platforms, including aircraft, ships, and vehicles. This trend is bolstered by investments in modern solutions and infrastructure upgrades, such as the enhancement of ground stations for satellite imagery technology. The market is moderately fragmented, with both local and international players competing fiercely. Recent collaborations and technological advancements, such as Hughes Network Systems' terminal approval for low Earth orbit satellite networks and Eutelsat OneWeb's preparations for commercial services in Saudi Arabia, highlight the dynamic nature of the market and its potential for continued expansion across the EMEA region.

EMEA Satellite Antenna Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 An Assessment of the Impact of Key Macroeconomic Trends

-

-

2. MARKET SEGMENTATION

-

2.1 By Antenna Type

-

2.1.1 Flat Panel Antenna

-

2.1.2 Parabolic Reflector Antenna

-

2.1.3 Horn Antenna

-

2.1.4 Fiberglass Reinforced Plastic Antenna

-

2.1.5 Iron Antenna With Mold Stamping

-

2.1.6 Other Antenna Types

-

-

2.2 By Application

-

2.2.1 Space

-

2.2.2 Land

-

2.2.3 Maritime

-

2.2.4 Airborne

-

-

2.3 By Country

-

2.3.1 United Kingdom

-

2.3.2 Germany

-

2.3.3 France

-

2.3.4 Saudi Arabia

-

2.3.5 UAE

-

2.3.6 South Africa

-

-

EMEA Satellite Antenna Market Size FAQs

How big is the EMEA Satellite Antenna Market?

The EMEA Satellite Antenna Market size is expected to reach USD 1.11 billion in 2024 and grow at a CAGR of 10.93% to reach USD 1.87 billion by 2029.

What is the current EMEA Satellite Antenna Market size?

In 2024, the EMEA Satellite Antenna Market size is expected to reach USD 1.11 billion.