Embedded Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

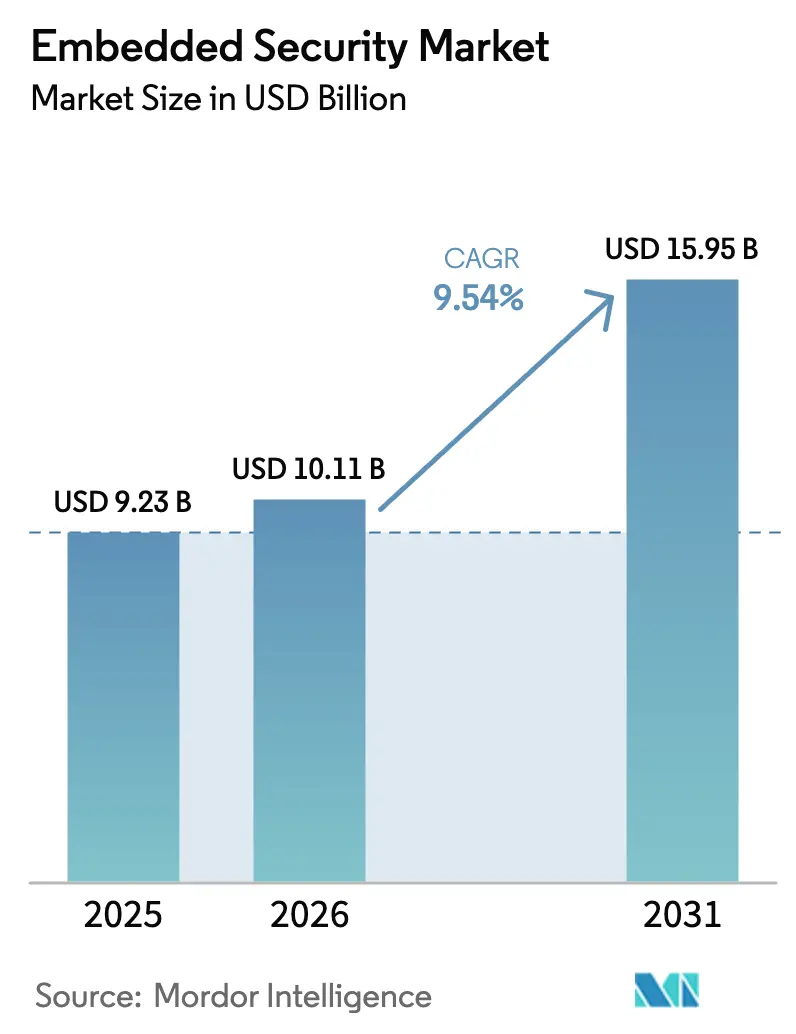

| Market Size (2026) | USD 10.11 Billion |

| Market Size (2031) | USD 15.95 Billion |

| Growth Rate (2026 - 2031) | 9.54% CAGR |

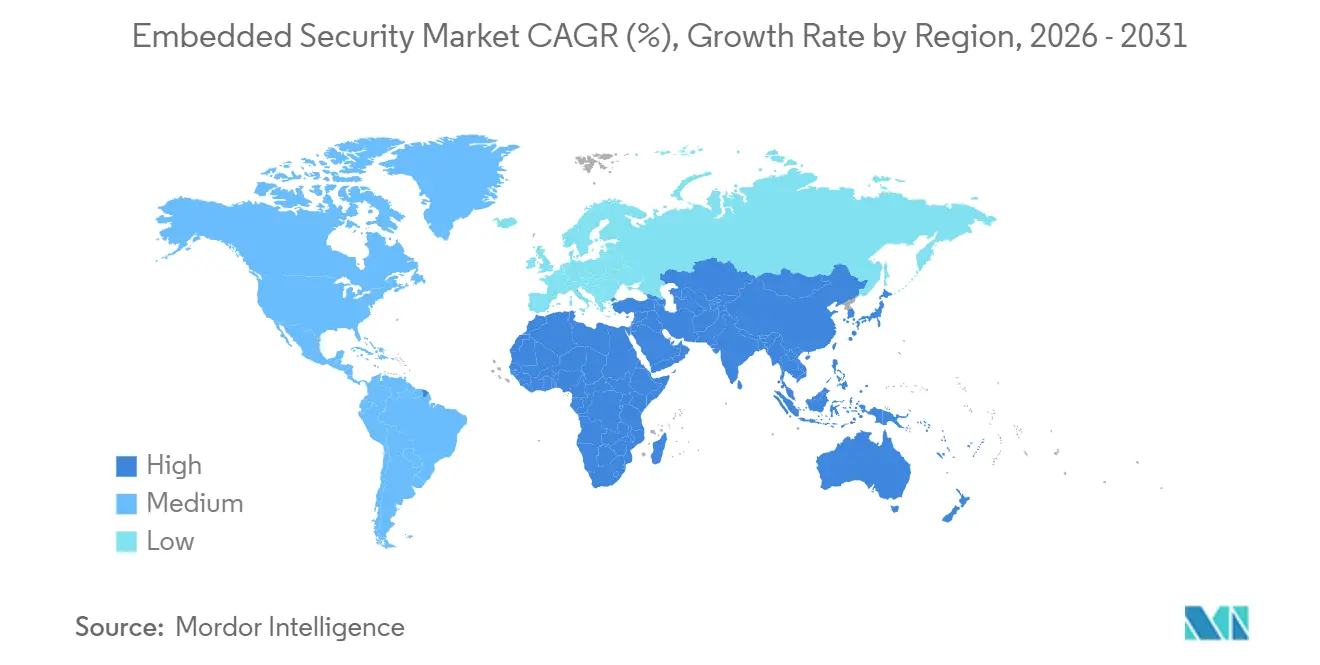

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

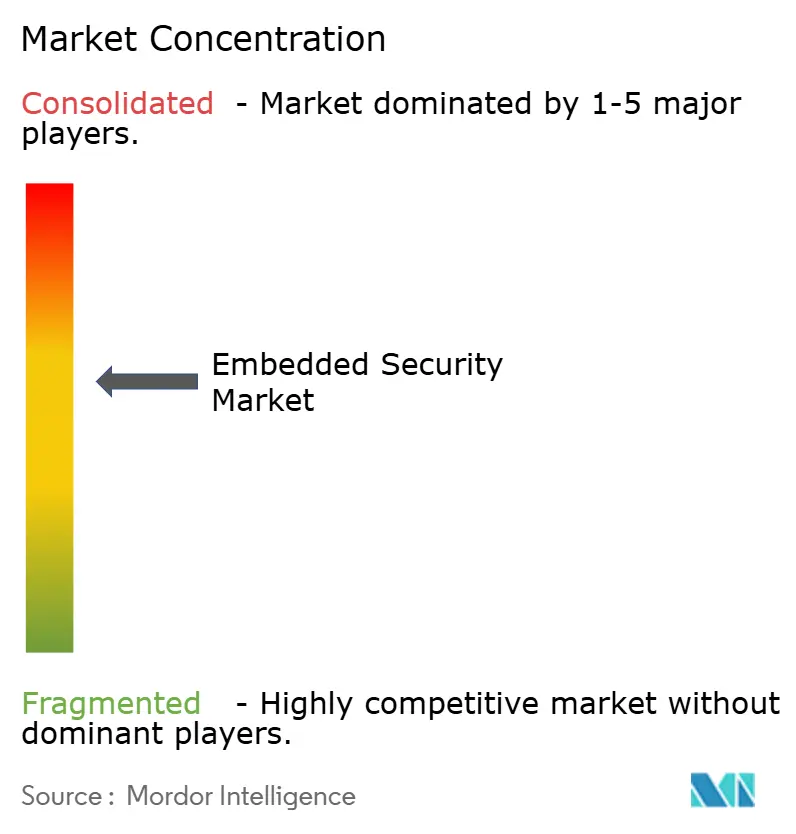

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embedded Security Market Analysis by Mordor Intelligence

The Embedded Security Market size is projected to expand from USD 9.23 billion in 2025 and USD 10.11 billion in 2026 to USD 15.95 billion by 2031, registering a CAGR of 9.54% between 2026 to 2031. Heightened data-sovereignty rules, the European Union’s Cyber Resilience Act, and UN Regulation 155 have transformed hardware-root-of-trust adoption from an optional safeguard into a design mandate, especially for edge devices inside connected vehicles and industrial controllers. Automotive electrification triples the number of electronic control units per vehicle, expanding silicon content while widening the attack surface. Cloud HSM instances keep growing because enterprises favor elastic capacity, yet the same customers embed secure elements locally to meet data-localization statutes. Demand also reflects the spread of FIDO passkeys, eSIM provisioning, and post-quantum cryptography pilots, each of which elevates hardware-based credential storage. Asia Pacific anchors fabrication capacity, while the Middle East’s smart-city build-outs make it the fastest-expanding geography.

Key Report Takeaways

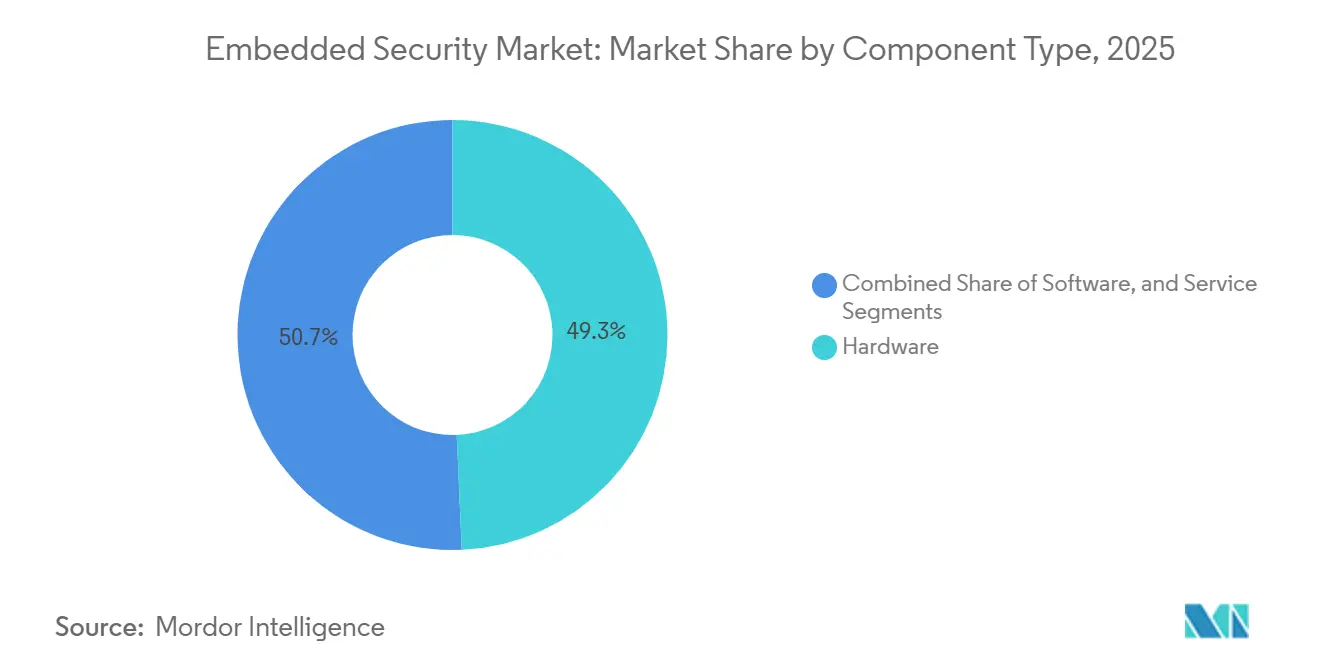

- By component type, hardware maintained a 49.32% embedded security market share in 2025, whereas services recorded the highest 11.42% CAGR to 2031.

- By deployment, cloud led with 57.52% revenue share in 2025, and it is advancing at a 12.62% CAGR through 2031.

- By application, payment captured 36.64% of the embedded security market size in 2025, while authentication is poised for a 10.64% CAGR to 2031.

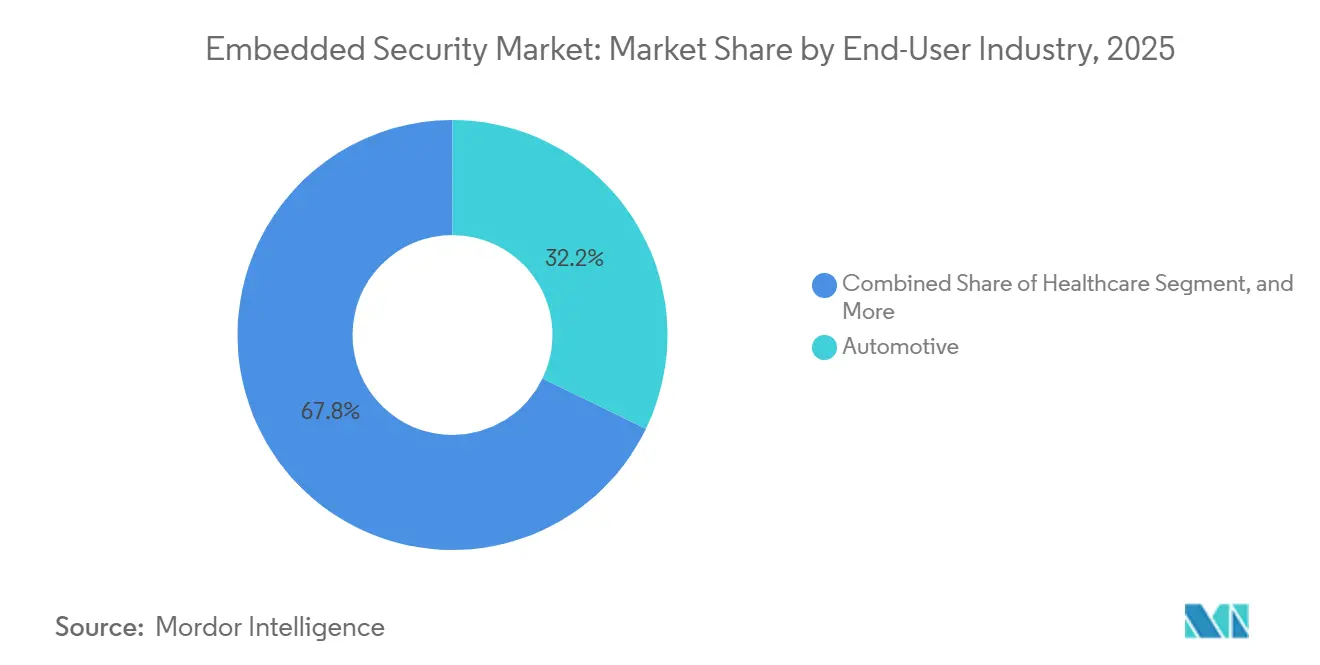

- By end-user industry, automotive held 32.18% of 2025 demand, whereas healthcare is forecast to expand at a 10.22% CAGR between 2026 and 2031.

- By geography, Asia Pacific commanded a 40.42% revenue share in 2025; the Middle East is on track for the fastest 11.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Embedded Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification and ADAS Adoption in Automotive ECUs | +2.1% | Europe, China, North America | Medium term (2-4 years) |

| EMVCo Contactless Payment Mandates for Cards and POS Terminals | +1.8% | Europe and Asia Pacific | Short term (≤ 2 years) |

| Expanding IoT Edge Nodes in Smart-Home and Industrial Settings | +1.6% | Asia Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Post-Quantum-Crypto Migration Roadmaps for Long-Life Controllers | +1.3% | North America and EU, pilots in Asia Pacific | Long term (≥ 4 years) |

| EU Cyber-Resilience Act Requiring Hardware Roots of Trust | +1.5% | Europe, ripple to Middle East and Asia Pacific | Short term (≤ 2 years) |

| Digital Battery Passports Creating Secure-Element Demand | +1.2% | Europe, uptake in China and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification And ADAS Adoption In Automotive ECUs

Battery-electric platforms integrate up to 100 electronic control units, each obligated to support secure boot, encrypted firmware updates, and authenticated over-the-air patches. Infineon confirmed 18% annual growth in automotive security-controller revenue as Tier-1 suppliers embed AURIX TC4x devices in battery-management and zonal architectures.[1]Infineon Technologies, “Annual Report 2024,” infineon.com Centralized compute designs such as Tesla’s Hardware 4 concentrate cryptographic workloads, lifting per-vehicle silicon value. Advanced driver-assistance sensors exchange safety-critical data over Ethernet backbones, so OEMs insert secure gateways with intrusion-detection firmware. Stellantis and STMicroelectronics are co-developing vehicle-to-grid modules that embed dedicated secure elements, signaling how bidirectional charging extends security beyond the cabin.

EMVCo Contactless Payment Mandates For Cards And POS Terminals

EMVCo’s Contactless Kernel 3.0 forces new payment terminals shipped after January 2025 to implement relay-attack mitigation and biometric verification, compelling dual-interface secure elements with NFC controllers. Mastercard reported 78% contactless penetration in Europe and 65% in Asia Pacific, leaving North America at 42% and primed for hardware refresh.[2]Mastercard, “Form 10-K Annual Report 2024,” mastercard.com PCI PTS 7.0 simultaneously tightens physical-tamper rules, pushing terminal vendors from generic processors toward certified secure chips. NXP saw a 12% sequential lift in secure-payment IC revenue on India’s RuPay card roll-out and Brazil’s Pix expansion. Embedded secure elements also power tokenized wallets in eSIM-enabled smartphones, a segment that shipped 1.2 billion units in 2024.

Expanding IoT Edge Nodes In Smart-Home And Industrial Settings

Matter-certified devices exceeded 500 models by September 2024, each storing onboarding keys inside secure elements to guarantee encrypted Thread and Wi-Fi sessions.[3]Mastercard, “Form 10-K Annual Report 2024,” mastercard.com Industrial vendors mirror the trend to comply with IEC 62443; Siemens integrated TPM 2.0 modules into new SIMATIC S7-1500 PLCs, enabling encrypted links to cloud analytics. Hardware-rooted identity boosts cyber-insurance eligibility and reduces compliance audits, offsetting a USD 2-5 component premium. AWS IoT Device Defender offers discounted tiers for hardware-verified endpoints, creating a virtuous cycle.

Post-Quantum-Crypto Migration Roadmaps For Long-Life Controllers

NIST finalized FIPS 203, 204, and 205 algorithms in August 2024, triggering redesigns for controllers that must remain secure through the 2040s. Infineon’s OPTIGA Trust M MTR and Qualcomm’s QCC730 audio SoC already integrate hybrid classical-quantum key exchange. The trade-off is heavier code and higher clock cycles, nudging OEMs toward Cortex-M33 cores with larger SRAM. U.S. federal agencies must inventory cryptographic systems by 2025, cascading quantum-safe requirements to contractors and utilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ASP Gap Versus Commodity Microcontrollers in Cost-Sensitive IoT | -1.4% | Global, acute in Asia Pacific consumer IoT | Short term (≤ 2 years) |

| Fragmented Standards Across Verticals (GlobalPlatform vs. TCG) | -0.9% | Global, regulatory divergence in major regions | Medium term (2-4 years) |

| Supply-Chain "Ghost-Foundry" Risk Limiting Qualified Sources | -0.7% | North America and Europe defense markets | Medium term (2-4 years) |

| Shortage of Secure-Element Firmware Verification Skill Sets | -0.6% | Global, pronounced in healthcare and industrial | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High ASP Gap Versus Commodity Microcontrollers In Cost-Sensitive IoT

Secure MCUs cost USD 1.50-3.00 compared with USD 0.30-0.50 generic parts, a premium that squeezes consumer-IoT gross margins. Attach rates stay below 25% in smart-home accessories despite available STM32L5 and STM32U5 devices that integrate Arm TrustZone. Higher quiescent current also shortens battery life by up to 30%. Microchip’s PIC32CM LS00, priced at USD 0.85, narrows the gap but still forces product re-certification.

Fragmented Standards Across Verticals

Payment and telecom ecosystems adopt GlobalPlatform, whereas automotive and PC suppliers lean on Trusted Computing Group TPM 2.0, fragmenting silicon roadmaps. Vendors like NXP must sustain both A71CH secure elements and discrete TPMs, duplicating inventory and qualification expense. China’s mandate for SM2/3/4 algorithms adds region-specific variants, further splitting volumes. FIDO Alliance’s Device Onboard aims to bridge gaps but had fewer than 50 certified products by late 2024.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Services Outpace Hardware On Migration Complexity

The embedded security market size for hardware reached nearly half of total revenue in 2025, yet services are rising faster as organizations confront 12- to 18-month Common Criteria evaluations. Hardware margins compress in mature payment and SIM segments, while post-quantum-ready secure elements and TPMs keep absolute revenue solid. Software tools, such as static analyzers and key-management middleware, close gaps that once favored turnkey firmware and empower OEMs to retain intellectual property.

Services growth reflects a scarcity of side-channel experts and certified evaluators, driving consulting day rates above USD 2,000. Thales, Rambus, and Synopsys now wrap lifecycle management, certification artifacts, and security audits into recurring packages, blurring the line between silicon sale and subscription. As platform-as-a-service offerings mature, the embedded security market welcomes more hybrid revenue models that bundle chips, firmware, and cloud dashboards in a single contract.

By Application: Authentication Gains Momentum As Passwordless Logins Spread

Payment still leads the embedded security market with a 36.64% slice of revenue in 2025, but authentication posts a double-digit growth trajectory supported by phishing-resistant passkey mandates. Governments and cyber-insurers increasingly penalize single-factor logins, prompting enterprises to adopt FIDO2 hardware tokens and device-bound keys. Content-protection hardware stabilizes as studios pivot to software-based multi-DRM inside trusted execution environments, trimming demand for legacy set-top boxes.

Authentication’s ascent is amplified by cloud providers that require passkeys for administrative consoles and by healthcare reforms that call for multi-factor access to electronic health records. The shift aligns with hardware that can store both classical and lattice-based keys, future-proofing investment. As a result, the embedded security market size tied to authentication is set to narrow the gap with payment by the end of the decade, particularly in regions that lag in contactless penetration.

By End-User Industry: Healthcare Accelerates On FDA Guidance

Automotive captured 32.18% of 2025 revenue, reflecting deep ECU penetration, but growth is flattening as premium models reach saturation. Healthcare, by contrast, carries the fastest 10.22% CAGR as regulators push cryptographic device identity for networked pumps, ventilators, and imaging systems. Embedded secure elements reduce recall risk and support encrypted over-the-air therapy adjustments, lifting per-device silicon value.

Flagship phones integrate secure enclaves at near-100% attach rates, whereas budget handsets and smart-home accessories remain cost-pressured. Telecommunications infrastructure adopts hardware roots of trust for 5G base stations, yet long capital-replacement cycles curb growth. Defense and space payloads pay the highest ASPs, but export controls limit volumes, keeping their share small within the embedded security industry.

By Deployment: Cloud Dominates Yet Coexists With On-Premise Gateways

Cloud options owned 57.52% share in 2025 and clock a 12.62% CAGR, propelled by instant provisioning and elastic capacity. Amazon, Microsoft, and Google each rolled out FIPS 140-3 Level 3 HSM instances, luring regulated sectors that once favored data-center appliances. Even so, automotive plants and payment-network switches still host on-premise HSMs for root-key ceremonies and ultra-low-latency operations.

Firmware signing occurs on-premise, while distribution and certificate rotation move to the cloud. This dual model explains why the embedded security market continues to sell hardware modules for physical vaults even as cloud revenue accelerates. Vendors now differentiate by bundling tokens that operate seamlessly across both realms, cementing customer lock-in.

Geography Analysis

Asia Pacific controlled 40.42% of embedded security market revenue in 2025. Taiwan and South Korea supply leading-edge secure-element wafers, while China’s Multi-Level Protection Scheme forces domestic cryptographic IP, lifting local demand. Despite its size, the region’s growth moderates as mature smartphone and payment-card penetration reduces incremental volume.

The Middle East is the fastest-growing geography at 11.52% CAGR, fueled by Saudi Arabia’s NEOM smart-city contracts exceeding USD 500 million and the UAE Cybersecurity Decree that mandates hardware encryption for critical infrastructure. Projects span smart grids, autonomous transit, and national identity layers, creating a pipeline for secure elements across industrial, consumer, and civic devices.

North America and Europe jointly contribute roughly 45% of revenue. Both regions face slower growth due to mature automotive and payment ecosystems, but they lead post-quantum pilots and industrial-IoT retrofits. Europe’s Cyber Resilience Act forces secure-element integration yet depends on Asian fabs for supply, exposing geopolitical risk. In the United States, defense restrictions confine sourcing to DMEA-trusted foundries, tightening supply but ensuring provenance. South America and Africa remain early-stage markets; Brazil’s Pix payment and Nigeria’s eNaira CBDC offer pockets of opportunity yet lack scale to shift global rankings.

Regulatory Landscape

Embedded security demand is being pulled into compliance-by-design by horizontal and sector rules that elevate hardware roots of trust, vulnerability handling, and lifecycle support from best practice to procurement and conformity requirements. A key anchor is Regulation (EU) 2024/2847 (Cyber Resilience Act), which sets cybersecurity obligations for products with digital elements, including secure-by-default configurations and documented cybersecurity risk assessments, with conformity commonly linked to harmonized standards such as ETSI EN 304 623 for a presumption of conformity once cited.

Outside the EU, government guidance is tightening expectations on IoT manufacturers around maintenance, support, and end-of-life. In March 2026, Australia brought into force the Cyber Security (Security Standards for Smart Device) Rules 2025 after a 12-month transition, while NIST updated IR 8259r1 in April 2026 and issued an initial public draft of SP 800-213r1 in June 2026 to formalize IoT cybersecurity practices for federal contexts. Together, these updates reinforce SBOM-aligned documentation, coordinated vulnerability disclosure, and lifecycle controls that cascade into supplier requirements.

Value Chain Analysis

The embedded security value chain starts with cryptographic architecture and security IP selection (roots of trust, secure elements, TPM blocks, secure boot and update stacks). It then moves to silicon implementation through IDMs and fabless players that depend on concentrated foundry capacity, followed by packaging, test, and certification. Upstream contributors include IP and enablement ecosystems such as Arm Platform Security Architecture (PSA) and Trusted Firmware-M (TF-M), alongside silicon security providers such as Infineon, NXP, STMicroelectronics, Microchip, and Rambus that ship secure MCUs, secure elements, TPMs, and root-of-trust blocks. Midstream friction is shaped by formal evaluations, including Common Criteria and FIPS 140-3 in regulated deployments, and by vertical standard divergence (GlobalPlatform in payment and telecom versus TCG TPM 2.0 in PC and parts of industrial and automotive). This can force dual roadmaps, duplicated inventory, and longer qualification cycles.

Downstream, OEMs and Tier-1s integrate security silicon and firmware into devices, then rely on provisioning, key injection, certificate lifecycle management, and update infrastructure. Over time, this integration increasingly blends on-device secure storage with cloud services. The main bottlenecks remain trusted manufacturing and the integrity of test and provisioning steps, where counterfeit parts, unauthorized hardware modifications, and untrusted fabrication and testing facilities raise provenance requirements, especially for defense and critical infrastructure supply chains. As regulatory obligations such as the EU Cyber Resilience Act move vulnerability handling and lifecycle support into mandatory processes, more of the value chain shifts toward design-time security (left-of-fab) and repeatable compliance artifacts that connect silicon choices, firmware stacks, and service layers used to operate devices through end-of-life.

Competitive Landscape

The top five vendors, Infineon, NXP, STMicroelectronics, Qualcomm, and Samsung, command about 55-60% of revenue, indicating moderate concentration. These incumbents rely on broad certification libraries to cut customer time-to-market. Cloud hyperscalers, however, design custom security processors that offload cryptographic workloads from traditional secure elements, diluting share. Startups such as PQShield and Secure-IC focus on lattice-based accelerators, positioning themselves for post-quantum transitions.

Differentiation is moving from transistor counts to lifecycle services. NXP’s EdgeLock 2GO and Infineon’s subscription bundles tie silicon to cloud provisioning, generating recurring revenue and raising switching costs. FPGA vendors like Lattice add roots-of-trust to programmable logic, displacing discrete TPMs in telecom racks. Infineon logged 47 post-quantum-related patents in 2024, while Qualcomm submitted 32 covering mobile secure-enclave architectures.

Standards-body participation provides avenue for influence; Infineon and NXP chair work groups in both TCG and GlobalPlatform, enabling them to steer specifications toward their roadmaps. Meanwhile, Arm’s acquisition of Certus signals upstream integration of secure-boot IP directly into Cortex-M cores, a move that could marginalize low-end discrete secure elements in cost-sensitive IoT gear.

Embedded Security Industry Leaders

Infineon Technologies AG

NXP Semiconductors NV

STMicroelectronics NV

Microchip Technology Inc.

Samsung Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven manufacturer obligations are creating whitespace for embedded security platforms that bundle silicon, provisioning, and compliance workflows into repeatable programs for IoT and industrial devices. These programs need secure-by-default configurations, vulnerability handling, and lifecycle support with demonstrable evidence. In March 2026, Microchip expanded its Trust Platform with a TrustFLEX secure authentication IC (TA101) and TrustMANAGER with keySTREAM service positioned to help manufacturers address EU Cyber Resilience Act and IEC 62443-aligned requirements. This points to buyer preference for turnkey device identity, key management, and secure onboarding, rather than stand-alone chips. NIST IR 8259r1 (April 2026) also broadened guidance to cover maintenance and end-of-life, which increases demand for embedded secure update, certificate rotation, and device decommissioning features that connect firmware and cloud tooling to hardware-rooted credentials.

Post-quantum readiness is moving from pilot activity to productized building blocks, creating room for suppliers that can deliver PQC-capable roots of trust without overtaxing power and memory budgets. GlobalPlatform launched Pavona in May 2026 as an open silicon distribution with production-grade PQC stacks and taped-out reference designs at TSMC 3 nm (N3), which reduces adoption friction for OEMs that want standardized, implementation-ready security foundations. Procurement pressure from payment modernization, industrial IEC 62443 adoption, and automotive cybersecurity requirements also increases the addressable scope for certified TPMs and secure elements. At the same time, services revenue continues to expand around certification evidence, secure provisioning, and lifecycle operations that reduce time-to-compliance for device makers with limited in-house side-channel and verification expertise.

Recent Industry Developments

- July 2026: Infineon launched the SECORA ID Key S USB, a Java Card-based security solution aimed at FIDO2 and PKI authentication use cases. By packaging hardware-backed credentials in a deployable form factor, it supports passwordless enterprise rollouts and device-bound credential strategies that depend on tamper-resistant storage.

- October 2025: Cadence completed its acquisition of Secure-IC, adding embedded security IP and expertise into its design and verification portfolio. The move pushes security considerations earlier in the chip design flow, supporting OEMs that need stronger design-time assurance to meet rising compliance and certification demands.

- September 2024: STMicroelectronics announced FIPS 140-3 certification for its STSAFE-TPM family, including ST33KTPM2X and ST33KTPM2A. Certified TPM availability reduces procurement barriers for regulated industrial and critical infrastructure deployments that require validated cryptographic modules.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue earned from security functions that are built into connected devices at the chip, module, or firmware level, so the device can store keys, authenticate, encrypt data, and boot securely during its usable life.

Scope exclusions: Stand-alone network security appliances, general PC endpoint suites, and purely cloud-only security services are excluded from this market sizing.

Segmentation Overview

- By Component Type

- Hardware

- Software

- Services

- By Application

- Payment

- Authentication

- Content Protection

- Other Applications

- By End-User Industry

- Automotive

- Healthcare

- Consumer Electronics

- Telecommunications

- Aerospace and Defense

- Other End-User Industries

- By Deployment

- On-Premise

- Cloud

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on device shipments, security standards, and adoption signals that can be checked in public data. We typically refer to sources such as NIST publications, ENISA guidance, IEEE standards notes, the FCC equipment authorization database for connected devices, and ITU materials on IoT and security topics.

To keep the model practical, we also review company filings and investor presentations to understand product mix and pricing direction for embedded security items. Where available, patent databases are used to map technology focus (secure elements, roots of trust, secure boot) and to sanity-check how quickly certain features are being designed in. The desk sources listed here are illustrative only, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test adoption rates, pricing logic, and how embedded security is bundled inside chips, modules, or software stacks. We spoke with participants across the value chain, including component suppliers, device makers, system integrators, and large end users, and we covered key demand regions across APAC, EMEA, and the Americas to avoid single-region bias.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 45% |

| Mid tier: 52% | Functional/Unit leaders: 37% | EMEA: 36% |

| Smaller Players: 17% | Managers: 50% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where device demand pools are reconstructed by application and then filtered by the share of devices that require hardware-rooted security features. We translate those demand pools into value using a practical mix of attach rates and average selling price ranges for secure elements, TPM-type blocks, and related embedded security software and services.

To keep totals realistic, results are corroborated with selective bottom-up approximations, such as sampled supplier revenue disclosures, channel feedback on typical content per device, and a few ASP times volume checks for high-usage device categories. When a sub-area has limited public visibility, gaps are handled by using proxy indicators like connected-device shipment trends, automotive electronics content growth, IoT module penetration, and the pace of security regulation and certification activity, and then adjusted through interview feedback.

For forecasting, we rely on scenario analysis supported by a light multivariate regression view on key drivers, including connected device shipments, growth in automotive and industrial IoT deployments, security-by-design compliance activity, and the expected shift toward hardware roots of trust. The final forecast is paced so that rapid adoption areas are reflected, while price erosion in mature silicon categories is not ignored.

Data Validation & Update Cycle

Outputs are checked across multiple steps before sign-off, so unusual jumps by region, application, or component are flagged and revisited. We compare the model with independent signals, such as device shipment direction, security feature adoption statements in filings, and public standards and certification activity, and then we re-check assumptions when variance looks too large.

A second analyst review is used to confirm that definitions were applied consistently and that currency and timing choices are aligned across inputs. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulation changes or sharp demand shifts in key device categories. Before delivery, a fresh pass is completed so clients receive an up-to-date view.

Mordor Intelligence's Embedded Security Market Size Compared Against Other Published Estimates

Published market numbers for embedded security can look far apart even when the topic sounds the same, because each publisher sets its own line on what gets counted and how pricing is treated. The spread usually comes from differences in component coverage, whether services are bundled, how device volumes are mapped to security content, and how quickly assumptions are refreshed.

The main gap comes from whether device-resident security only is counted, or if broader cyber programs and stand-alone security products get pulled in, and this choice shifts the total quickly in IoT-heavy applications. Some estimates also apply a single blended ASP that does not separate secure silicon content from software and services, and currency timing can add noise when the base year is volatile, which is why the market sizes below do not match exactly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.11 B (2026) | |

| Industry Research House A | USD 8.10 B (2024) | Uses an earlier base year and a slower growth profile, and its scope leans more on select embedded security offerings while not always aligning device-level security content with newer connected-device categories. |

| Global Consultancy B | USD 12.45 B (2026) | Likely applies broader inclusion for services and related security items across applications, which can lift the total when hardware, software, and service value are blended with fewer constraints on what counts as embedded. |

The table shows that scope and pricing treatment explain most of the difference, more than any single growth assumption. The main gap comes from excluding stand-alone network security and cloud-only services, and by counting embedded security only when it is permanently integrated into device hardware or firmware, a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is driving the current growth of the embedded security market?

Rapid IoT expansion, automotive cybersecurity mandates, and new regulations such as the EU Cyber Resilience Act are collectively pushing demand for hardware-rooted trust and lifecycle security services.

How fast is revenue growing for embedded security solutions?

Market revenue is set to climb from USD 10.11 billion in 2026 to USD 15.95 billion by 2031, reflecting a 9.54% CAGR.

Which component category is expanding the quickest?

Services, driven by certification consulting and lifecycle-management subscriptions, record an 11.42% CAGR through 2031.

What role do cloud deployments play?

Cloud held 57.52% share in 2025 and grows 12.62% annually because managed HSM instances offer elastic capacity and compliance certifications.

Why is healthcare demand accelerating?

FDA draft guidance from 2024 encourages cryptographic device identity and secure updates, pushing healthcare equipment toward embedded secure elements at a 10.22% CAGR.

Which region delivers the fastest growth?

The Middle East leads with an 11.52% CAGR, fueled by mega-projects like NEOM and new cybersecurity mandates in the Gulf states.

How concentrated is vendor competition?

The top five players control just over half of revenue, yielding a moderate 6/10 concentration score amid rising hyperscaler and startup activity.

Page last updated on: