Electronic Design Automation Tools (EDA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

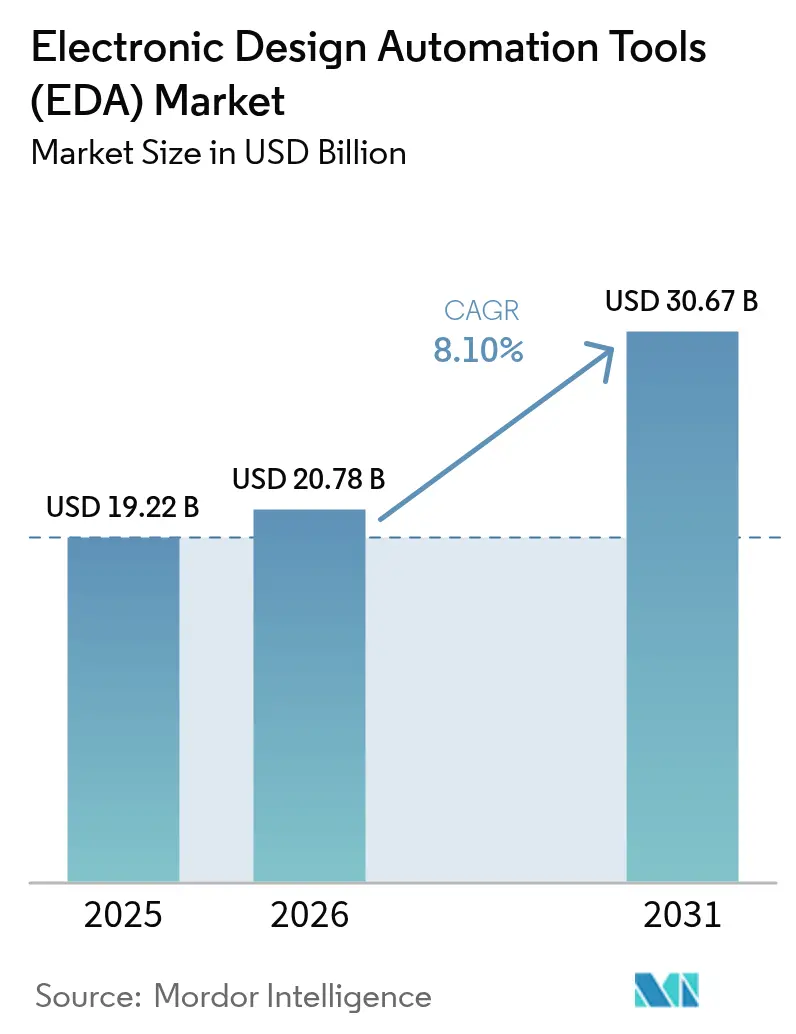

| Market Size (2026) | USD 20.78 Billion |

| Market Size (2031) | USD 30.67 Billion |

| Growth Rate (2026 - 2031) | 8.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Design Automation Tools (EDA) Market Analysis by Mordor Intelligence

Electronic Design Automation Tools market size in 2026 is estimated at USD 20.78 billion, growing from 2025 value of USD 19.22 billion with 2031 projections showing USD 30.67 billion, growing at 8.1% CAGR over 2026-2031. The outlook builds on faster transistor scaling, AI-enabled design flows, and closer foundry–tool collaboration. Chip architects are shifting from manual rule tuning to data-driven optimization that shortens tape-out cycles and lowers re-spin risk. Cloud-based capacity bursting is widening access to advanced verification, while automotive functional-safety mandates push formal methods into mainstream design. The 2025 completion of Synopsys’ USD 35 billion acquisition of Ansys signals a systemic move toward unified device-to-system platforms able to co-optimize silicon, package, and full-system performance simultaneously. Meanwhile, geopolitical export controls spur parallel EDA ecosystems, compelling vendors to certify flows for multiple regional foundries to avoid revenue erosion.

Key Report Takeaways

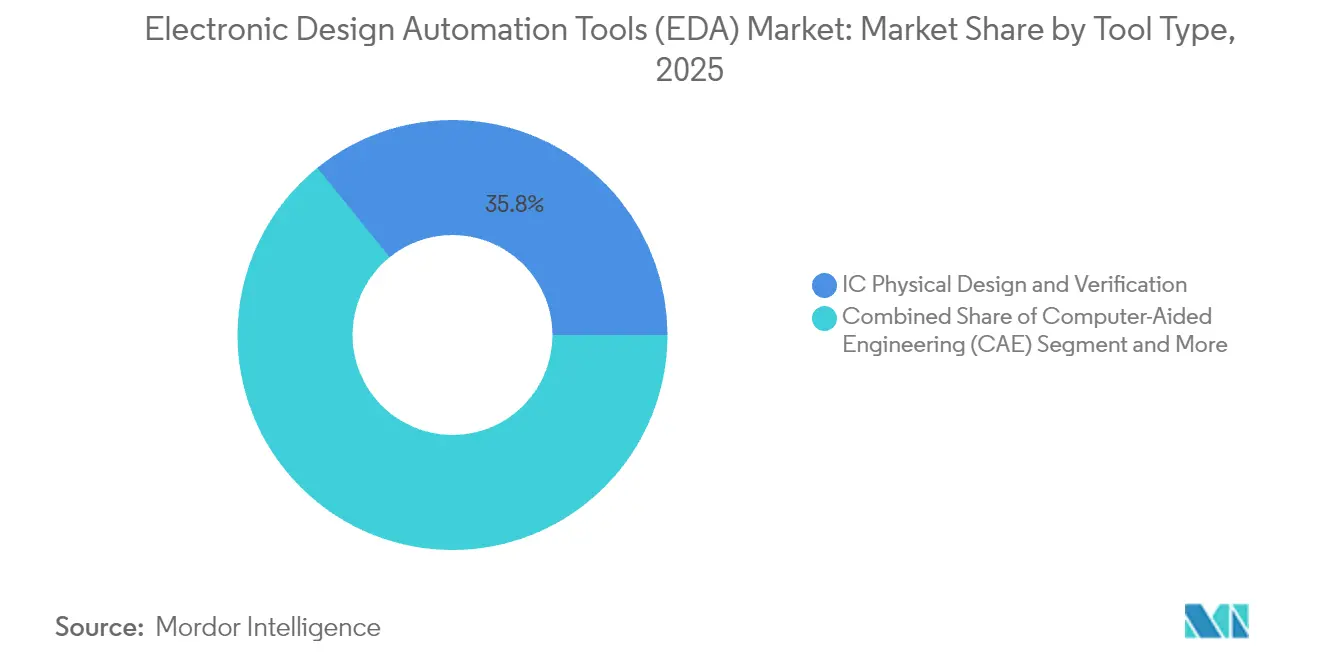

- By tool category, IC Physical Design and Verification led with 35.82% revenue share in 2025; Semiconductor Intellectual Property is projected to expand at a 9.7% CAGR through 2031.

- By design-flow stage, Layout, Routing and Timing Closure commanded 32.10% share of the Electronic Design Automation Tools market size in 2025, while Front-End RTL tools post the fastest CAGR at 9.35% through 2031.

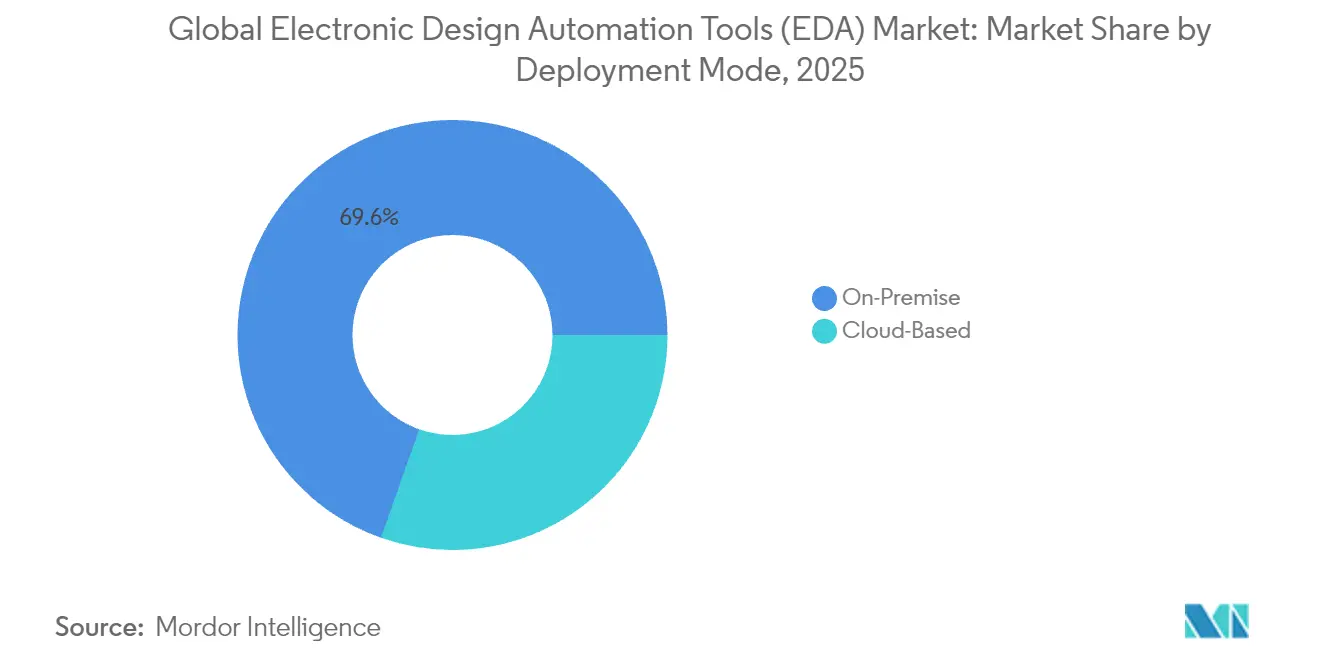

- By deployment mode, On-Premise solutions retained 69.60% share of the Electronic Design Automation Tools market size in 2025 even as Cloud-Based offerings advance at a 9.25% CAGR to 2031.

- By end-user, Communication Infrastructure held 26.55% of the Electronic Design Automation Tools market share in 2025; Automotive and Mobility is accelerating at a 9.85% CAGR to 2031.

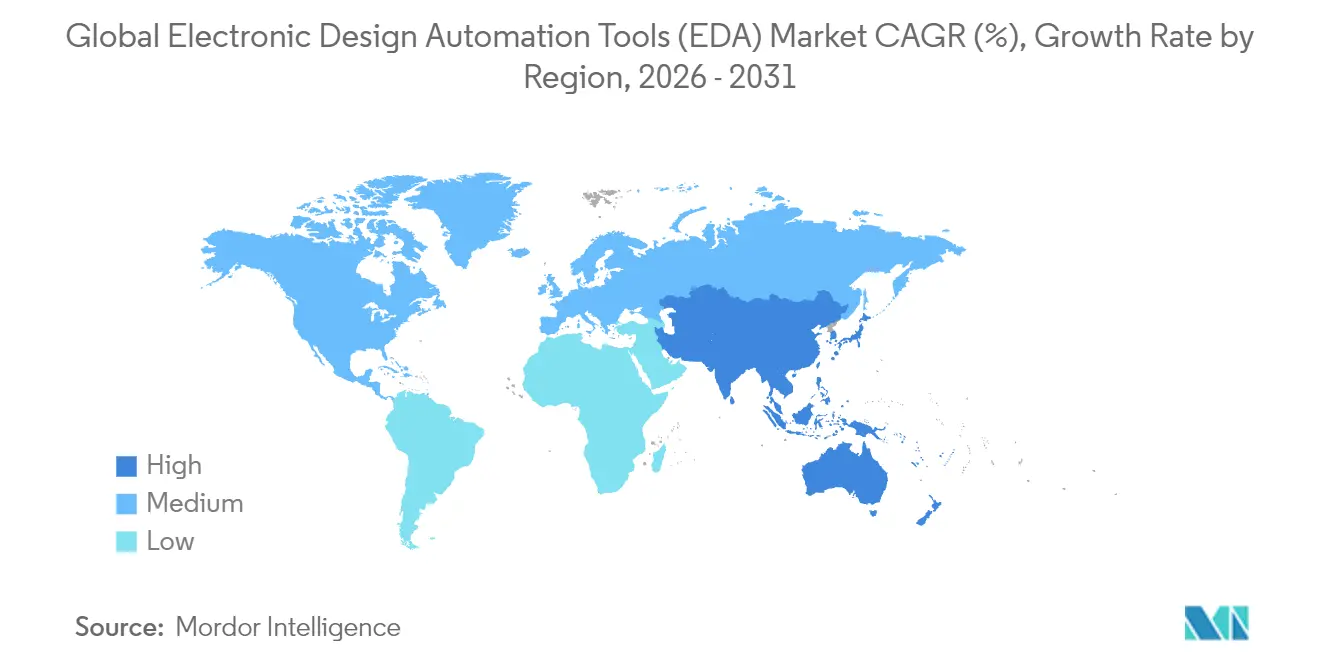

- By geography, Asia-Pacific held 42.05% of the Electronic Design Automation Tools market share in 2025, and it is expected to grow at a 9.55% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electronic Design Automation Tools (EDA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring chip-density in advanced nodes | +2.1% | Global, concentrated in APAC foundries | Medium term (2-4 years) |

| Proliferation of AI/ML accelerators & custom SoCs | +1.8% | Global, led by North America and APAC | Short term (≤ 2 years) |

| Rise of cloud-native EDA workflows (EDA-as-a-Service) | +1.2% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Automotive ISO 26262 functional-safety compliance needs | +0.9% | Global, strongest in EU and North America | Long term (≥ 4 years) |

| Growing open-source hardware movement driving verification demand | +0.7% | Global, with concentration in Asia-Pacific | Medium term (2-4 years) |

| U.S.–China export-control bifurcation accelerating on-shore design flows | +0.6% | China, India, with spillover to Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Chip-Density in Advanced Nodes

Gate-All-Around transistors, backside power delivery, and multi-die packaging produce a ten-fold rise in design-rule checks compared with 7 nm processes. Foundries now co-develop flows with EDA leaders; Synopsys and TSMC certified full digital and analog toolchains for A16 and N2P nodes in April 2025.[1]Synopsys, “AI-Driven Design Solutions Reduce Turnaround Time,” synopsys.com Unified exploration-to-signoff environments reduce costly re-spins—each exceeding USD 50 million at 3 nm. Intel’s 18A program likewise relies on integrated flows for 2.5D/3D architectures that merge compute, memory, and I/O on a single substrate.

Proliferation of AI/ML Accelerators and Custom SoCs

Hyperscale and edge providers increasingly commission purpose-built inference silicon. Cadence posted 40% YoY growth in semiconductor IP revenue in Q1 2025, attributing momentum to AI and chiplet projects.[2]Cadence Design Systems, “Cadence Reports First Quarter 2025 Financial Results,” cadence.com NVIDIA, ASML, TSMC, and Synopsys reported 40× lithography simulation speed-ups through the CuLitho software stack, enabling reticle layouts that meet AI power-per-watt targets.[3]NVIDIA, “NVIDIA, ASML, TSMC and Synopsys Set Foundation for Next-Generation Chip Manufacturing,” resources.nvidia.com As accelerator heterogeneity rises, SIP reuse and on-package interconnect standards intensify demand for IP verification.

Rise of Cloud-Native EDA Workflows (EDA-as-a-Service)

Synopsys Cloud illustrates a hybrid model in which license-entitled tools burst onto AWS or Microsoft Azure to finish simulation regressions overnight while golden IP remains on-premises for security. Elastic scaling eliminates idle hardware and cuts verification schedule by days for smaller design teams. Despite benefits, 70.5% of users kept mission-critical flows in private data centers in 2024, citing export-controlled designs and air-gap mandates in defense contracts. A growing cadre of fabless startups nevertheless treat pay-per-use compute as the only affordable path to 5 nm design.

Automotive ISO 26262 Functional-Safety Compliance Needs

ISO 26262 dictates formal proof that random hardware faults remain within failure-in-time limits across a vehicle’s lifetime. EDA vendors now bundle fault-campaign automation, safety case generation, and tool-qualification kits; Synopsys’ Z01X and Siemens’ Tessent integrate with formal analysis to demonstrate diagnostic coverage above 90% for critical blocks.[4]Siemens Digital Industries Software, “Tessent Safety for ISO 26262 Compliance,” plm.automation.siemens.com Software-defined vehicles amplify verification complexity, as single domain-controllers supervise multiple drive-by-wire subsystems. Regulators expect traceable verification artifacts from RTL through gate-level netlists, elevating demand for certified flows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating licensing costs for leading EDA suites | -1.4% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Talent shortage in sub-5 nm physical-design engineers | -1.1% | Global, concentrated in APAC and North America | Long term (≥ 4 years) |

| IP-theft & cyber-intrusion risks in cloud deployments | -0.8% | Global, with heightened concern in defense sectors | Medium term (2-4 years) |

| Slower than expected Moore's-Law cadence extensions | -0.5% | Global, affecting foundry roadmaps | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Licensing Costs for Leading EDA Suites

Annual enterprise bundles for comprehensive 3 nm sign-off now exceed USD 1 million per seat, forcing mid-tier fabs to prioritize tool modules and extend refresh cycles. Oligopolistic supply means price leverage remains with vendors, particularly for timing closure and lithography simulation packages that have no open-source substitute.

Talent Shortage in Sub-5 nm Physical-Design Engineers

The U.S. Semiconductor Workforce Development Act projects a gap of 67,000 highly specialized engineers by 2028, a shortfall echoed by TSMC’s Arizona fab, which has struggled to localize advanced node staff. Sub-5 nm layouts require expertise in voltage-droop mitigation, backside PDNs, and advanced packaging—skills seldom covered in undergraduate curricula. Vendors now embed AI-driven design advisors to compress ramp-up time, but still face multi-year proficiency curves.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tool Type: AI Catalyzes SIP Expansion

Semiconductor Intellectual Property (SIP) posted a 9.7% CAGR forecast, the fastest among tool categories, owing to rising chiplet architectures that favor verified interface blocks and mixed-signal cores. In 2025, SIP accounted for 18.74% of the Electronic Design Automation Tools market revenue, yet its attach rate per project has doubled since 2023 as foundries promote known-good-die strategies. The Electronic Design Automation Tools market size for SIP applications is projected to grow at a significant rate by 2031, underscoring the shift from monolithic SoCs to heterogeneous assembly.

IC Physical Design and Verification retained a 35.82% share thanks to the mandatory nature of placement, routing, static-timing, and DRC in every tape-out. However, AI-enhanced floorplanning automates multi-objective optimization, shrinking turnaround time by 30% on recent 3 nm designs.

Note: Segment shares of all individual segments available upon report purchase

By Design-Flow Stage: Front-End RTL Surges

Front-End Design tools record a 9.35% CAGR as high-level synthesis (HLS) and natural-language-to-RTL generators improve productivity. The Electronic Design Automation Tools market size for RTL automation is projected to grow significantly by 2031 on the back of AI-assisted code generation that captures functional intent in fewer iterations. Layout, Routing, and Timing Closure still governs 32.10% of the Electronic Design Automation Tools market share, reflecting the irreplaceable nature of sign-off-caliber timing convergence and advanced 3D parasitic extraction.

Generative design platforms now produce placement guidance that reduces wire length by 11% and leakage by 9% versus human scripts. Yet final SOC hand-off still relies on certified timing and electrical-rule reports accepted by foundries, cementing the relevance of established back-end toolchains.

By Deployment Mode: Hybrid Models Prevail

On-Premise installations controlled 69.60% revenue in 2025, a figure slowly eroding as cloud acceptance grows. Security-conscious sectors keep golden RTL, netlists, and sign-off decks in local data centers, but burst verification workloads to cloud for regression sweeps-particularly useful when sign-off windows coincide with multiple design groups. Cloud-based flows improve tool accessibility for emerging Fab-Lite regions, with some startups reporting cost reductions of 40% versus leasing identical hardware.

The Electronic Design Automation Tools market size attributed to cloud deployments is forecast grow significantly by 2031, supported by subscription licensing that aligns expense with project milestones. Vendors increasingly bundle scalable compute credits within enterprise agreements to encourage migration.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Automotive Leads

Automotive and Mobility exhibits a 9.85% CAGR, outpacing all other verticals as zonal architectures and autonomous-drive stacks oblige new functional-safety verification. ISO 26262 ASIL-D controllers require exhaustive fault coverage documented across RTL, gate, and transistor views-tripling simulation vector counts versus infotainment processors. Communication Infrastructure maintained the largest 2025 slice at 26.55%, but growth tempers as 5G macro rollouts mature.

Electric-vehicle powertrains and ADAS chips also spur demand for mixed-signal verification, bridging digital control loops with analog sensor interfaces.

Geography Analysis

Asia-Pacific held a 42.05% share in 2025 and advances at a 9.55% CAGR to 2031. Foundry clustering in Taiwan and South Korea anchors regional tool demand, while China accelerates sovereign EDA stacks in response to U.S. export controls. State-backed initiatives channel subsidies toward AI-assisted place-and-route engines and SPICE simulators, aiming to localize flows before 3 nm production ramps. India leverages a large engineering base; design-service firms there grew 17% in 2024 as Western customers sought cost-effective RTL and DFT support.

North America retains influence through leadership in AI algorithms, IP catalogs, and cloud infrastructure. The region’s share contracted slightly to 29.15% in 2025, yet remains the primary source of reference tool flows for leading-edge nodes. Export-control regimes require vendors to implement license-key geofencing, adding compliance cost but also locking in North American IP chains. Collaboration between Intel Foundry and Synopsys on 18A certified flows reinforces the U.S. bid to regain advanced manufacturing share. Europe focuses on automotive and industrial applications, with ISO 26262 driving premium verification tool adoption. TSMC’s 2025 design center launch in Munich aims to embed foundry engineers within the regional supply chain, providing first-hand support for 3D-IC packaging and power-efficient AI accelerators. The EU Chips Act grants emphasize RandD tax credits for electronic-design clusters, further stimulating regional EDA uptake. Middle East and Africa and South America remain nascent, but showing double-digit growth where government fab projects or IoT rollouts emerge.

Competitive Landscape

The market exhibits oligopolistic concentration: Synopsys, Cadence, and Siemens collectively control the majority of revenue through end-to-end suites and deep foundry certification pipelines. Synopsys’ July 2025 completion of the USD 35 billion Ansys acquisition creates the first vertically integrated device-to-system design stack, fusing semiconductor sign-off, CFD, thermal, and mechanical simulation into a single environment. Cadence tailors its offerings with system-persona-optimized IP and harnesses generative AI for strategic placements. Siemens, tapping into the digital-twin advantages of its industrial software division, broadens its verification processes to encompass factory simulations, catering to the needs of smart-manufacturing clients.

Regional challengers focus on sovereignty mandates. China’s state-sponsored tool vendors have secured pilot tape-outs for 14 nm automotive controllers and plan 7 nm certification by 2026. While performance gaps persist, bundled subsidies and mandatory domestic-tool quotas ensure a rising share in local projects. Cloud-native disruptors, mainly U.S. startups, deliver browser-based schematic capture and PCB co-simulation, targeting makers and mid-volume OEMs ignored by tier-1 EDA suites. However, absence of certified 3 nm flows limits penetration into bleeding-edge markets.

Foundry alliances remain pivotal. Membership in TSMC’s 3DFabric Alliance or Samsung SAFE program grants partners early design-rule visibility and joint marketing. Tool suppliers unable to guarantee day-zero process-design-kit availability risk exclusion from lucrative first-wave tape-outs. The competitive narrative is therefore driven less by tool features and more by ecosystem breadth, IP catalog size, and scalability across cloud plus on-premise environments.

Electronic Design Automation Tools (EDA) Industry Leaders

ANSYS Inc.

Cadence Design Systems Inc.

Keysight Technologies Inc

Synopsys Inc.

Xilinx Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Synopsys finalized its USD 35 billion purchase of Ansys, forming a chip-to-system design powerhouse spanning EDA, multiphysics, and mechanical simulation.

- May 2025: TSMC opened a Munich design center to co-develop AI and automotive chips with European clients.

- April 2025: Synopsys and Intel Foundry released production-ready digital and analog flows for 18A technologies, including multi-die packaging support.

- April 2025: Cadence posted Q1 2025 revenue of USD 1.242 billion and raised full-year guidance on IP demand for AI and chiplets.

Global Electronic Design Automation Tools (EDA) Market Report Scope

Electronic design automation (EDA) is a software product that helps in designing electronic systems with the aid of computers; these tools are often used to design circuit boards, processors, and different types of complex electronics. The software tool is also known as electronic computer-aided design, and it has largely replaced manual methods for designing circuit boards and semiconductors.

The Global Electronic Design Automation Tools (EDA) Market is segmented by Type (Computer-aided Engineering (CAE), IC Physical Design and Verification, Printed Circuit Board and Multi-chip Module (PCB and MCM), Semiconductor Intellectual Property (SIP), Services), by Application (Communication, Consumer Electronics, Automotive, Industrial), and by Geography.

| Computer-Aided Engineering (CAE) |

| IC Physical Design and Verification |

| PCB and Multi-Chip Module (MCM) |

| Semiconductor Intellectual Property (SIP) |

| Services |

| Front-End Design (RTL) |

| Logic Synthesis and Functional Verification |

| Layout, Routing and Timing Closure |

| Sign-off (DFM, Power, SI, Thermal) |

| On-Premise |

| Cloud-Based |

| Communication Infrastructure |

| Consumer Electronics |

| Automotive and Mobility |

| Industrial and Energy |

| Aerospace and Defense |

| Medical Devices |

| Other Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Tool Type | Computer-Aided Engineering (CAE) | |

| IC Physical Design and Verification | ||

| PCB and Multi-Chip Module (MCM) | ||

| Semiconductor Intellectual Property (SIP) | ||

| Services | ||

| By Design-Flow Stage | Front-End Design (RTL) | |

| Logic Synthesis and Functional Verification | ||

| Layout, Routing and Timing Closure | ||

| Sign-off (DFM, Power, SI, Thermal) | ||

| By Deployment Mode | On-Premise | |

| Cloud-Based | ||

| By End-User Industry | Communication Infrastructure | |

| Consumer Electronics | ||

| Automotive and Mobility | ||

| Industrial and Energy | ||

| Aerospace and Defense | ||

| Medical Devices | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How large will EDA tool revenues be by 2031?

The Electronic Design Automation Tools market is projected to reach USD 30.67 billion by 2031, expanding at an 8.1% CAGR from 2026.

Which region grows fastest in EDA adoption?

Asia-Pacific leads with a 9.55% CAGR through 2031, buoyed by foundry clustering and sovereign tool programs.

What segment expands quickest inside EDA?

Semiconductor Intellectual Property registers the highest 9.7% CAGR as chiplet and heterogeneous-integration projects multiply.

Why is automotive design driving tool demand?

ISO 26262 safety mandates require exhaustive formal verification, pushing Automotive and Mobility tool spending to a 9.85% CAGR.

How does cloud usage affect EDA economics?

Cloud-native workflows cut verification turnaround time and lower capital outlay, yet IP sensitivity keeps 69.60% of flows on-premise.

Which companies dominate the tool landscape?

Synopsys, Cadence, and Siemens together control about 70% of global revenue, reinforced by foundry-certified flows and extensive IP catalogs.

Page last updated on: