Electric Propulsion Satellites Market Size

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 48.93 Billion |

|

|

Market Size (2029) | USD 83.44 Billion |

|

|

CAGR (2024 - 2029) | 11.27 % |

|

|

Largest Share by Region | North America |

|

|

Market Concentration | Low |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in alphabetical order. |

Electric Propulsion Satellites Market Analysis

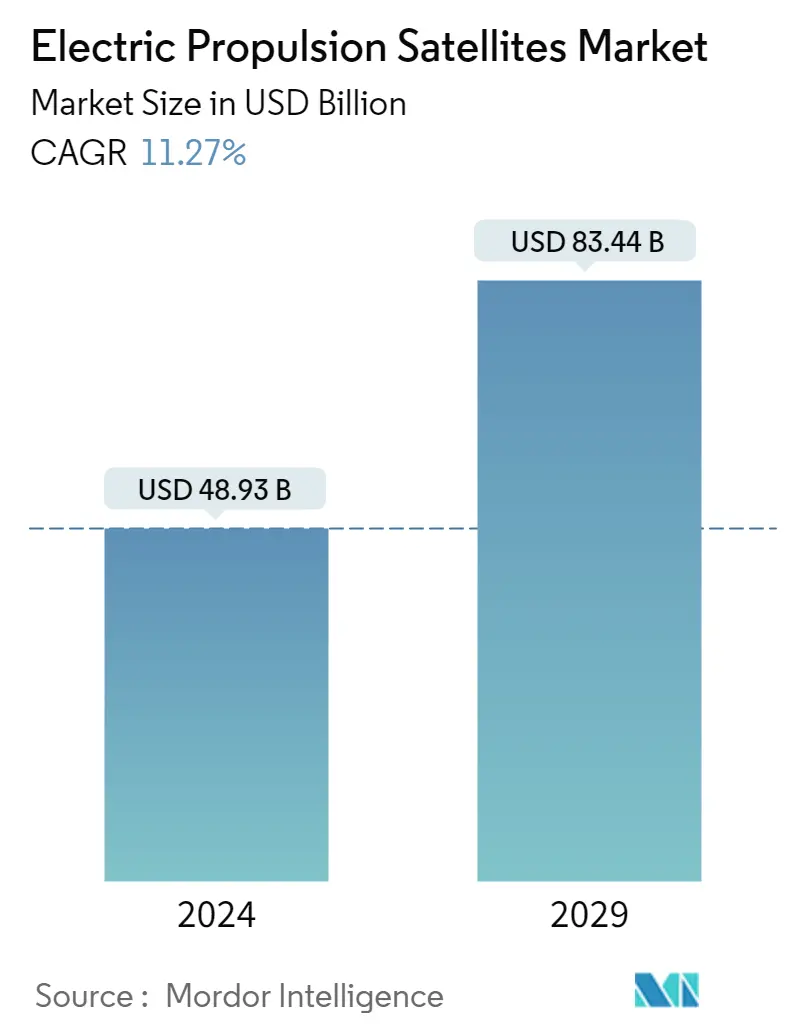

The Electric Propulsion Satellites Market size is estimated at USD 48.93 billion in 2024, and is expected to reach USD 83.44 billion by 2029, growing at a CAGR of 11.27% during the forecast period (2024-2029).

- Space-based activities have flourished during the last decade, as evident from the number of satellites launched for both commercial and defense applications, ranging from telecommunication, earth-observation, to experimental scientific research. The absence of a combustion supporting atmosphere in space has resulted in the increased adoption of electric propulsion technologies for maneuvering satellites in orbit.

- The inherent benefits of integrating an electric-propulsion system to different platforms are also driving the rate of adoption. Besides, the emergence of global green emission initiatives has encouraged the adoption of eco-friendly propulsion technologies, such as electric propulsion.

48.93 Billion

Market Size in 2024 (USD)

83.44 Billion

Market Size in 2029 (USD)

15.04 %

CAGR (2017-2023)

11.27 %

CAGR (2024-2029)

Largest Market by Propulsion type

72.53 %

value share, Full Electric, 2022

Full Electric satellite propulsion sytem are widely utilized for inspace propulsion and manoveuring, therfore enabling it to occupy a major share in the market.

Fastest-Growing Market by Propulsion type

14.55 %

Projected CAGR, Hybrid, 2023-2029

The technology of hybrid propulsion is also gaining traction and it is expected that the adoption rate of this propulsion systems increases over the the forecast period

Largest Market by End User

98.28 %

value share, Commercial, 2022

The commercial segment is expected to occupy a significant share because of the increasing use of satellites for various telecommunication services.

Largest Market by region

69.89 %

value share, North America, 2022

The increasing investment in satellite equipment to enhance the defense and surveillance capabilities, critical infrastructure, and law enforcement agencies using satellite systems are expected to drive the satellite market in the North American region, thereby increasing the scope for electric space propulsion satellites.

Leading Market Player

7 %

market share, Airbus SE, 2022

Airbus is the major player in the market, with strong emphasis in product development and innovation. The company's robust products and wide distribution channel has prompted to occupy majority of the share in the market.

The growing interest of governments and private players in space exploration have fueled the expansion of this market

- The global market for electric satellite propulsion systems witnessed robust growth in recent years, driven by the increasing demand for satellite deployments across various sectors. North America has emerged as a dominant player in the global space propulsion market, mainly due to the presence of established space agencies such as NASA and private companies like SpaceX, Blue Origin, and Boeing. These entities have undertaken ambitious space missions and satellite deployments, driving the demand for advanced propulsion systems. NASA is also working on the Solar Electric Propulsion project, which aims to extend the duration and capabilities of ambitious discoveries and science missions.

- Asia-Pacific has witnessed a rapid expansion of its space capabilities in recent years. Countries like China, India, and Japan have made significant strides in space technology and satellite manufacturing, positioning themselves as formidable players in the global market. In May 2022, Kongtian Dongli, a Chinese satellite electric propulsion company, secured multi-million yuan angel round financing amid a proliferation of Chinese constellation plans.

- Europe has a strong tradition of collaboration in space exploration through organizations like the ESA. ESA's partnerships with multiple member states have resulted in significant advancements in space technology, satellite manufacturing, and launch capabilities. In February 2023, IENAI SPACE, an in-space mobility provider based in Spain, received two ESA contracts within the General Support Technology Program to mature and further develop ATHENA (Adaptable THruster based on Electrospray powered by NAnotechnology) propulsion systems.

Global Electric Propulsion Satellites Market Trends

The increased emphasis on electric propulsion system is expected to aid in the growth of spending on its related space programs

- The grant for research and investment has been a major driver of innovation and growth in the North American satellite launch vehicle market. It has helped to fund the development of new technologies, such as reusable launch vehicles, which have the potential to significantly reduce the cost of satellite launches. In FY2023, according to the President's budget request summary from FY2022 to FY2027, NASA is expected to receive USD 98 million for the development of Solar Electric Propulsion. In March 2021, NASA, along with Maxar Technologies and Busek Co., successfully completed a test of the 6-kilowatt (kW) solar electric propulsion subsystem

- Additionally, in November 2022, ESA announced that it had proposed a 25% boost in space funding over the next three years to maintain Europe's lead in space projects. The ESA is asking its 22 nations to back a budget of EUR 18.5 billion for 2023-2025. In April 2023, Dawn Aerospace was awarded a contract to conduct a feasibility study with DLR (German Aerospace Center) to increase the performance of a nitrous-oxide-based green propellant for satellites and deep-space missions.

- In Asia-Pacific, the demand for space propulsion is driven by increasing space programs. In May 2022, Kongtian Dongli, a Chinese satellite electric propulsion company, announced that it had secured multi-million yuan angel round financing amid a proliferation of Chinese constellation plans. The company’s main products are hall thrusters and microwave electric propulsion systems. Likewise, in February 2023, the Indian government announced that ISRO is expected to receive USD 2 billion for various space-related activities, including the development of the Liquid Propulsion Systems Centre (LPSC) and ISRO Propulsion Complex.

Electric Propulsion Satellites Industry Overview

The Electric Propulsion Satellites Market is fragmented, with the top five companies occupying 23%. The major players in this market are Airbus SE, Northrop Grumman Corporation, Safran SA, Thales and The Boeing Company (sorted alphabetically).

Electric Propulsion Satellites Market Leaders

Airbus SE

Northrop Grumman Corporation

Safran SA

Thales

The Boeing Company

Other important companies include Accion Systems Inc., Ad Astra Rocket Company, Aerojet Rocketdyne Holdings, Inc, Busek Co. Inc., Sitael S.p.A..

*Disclaimer: Major Players sorted in alphabetical order.

Free with this Report

We offer a comprehensive set of global and local metrics that illustrate the fundamentals of the satellites industry. Clients can access in-depth market analysis of various satellites and launch vehicles through granular level segmental information supported by a repository of market data, trends, and expert analysis. Data and analysis on satellite launches, satellite mass, application of satellites, spending on space programs, propulsion systems, end users, etc., are available in the form of comprehensive reports as well as excel based data worksheets.

Electric Propulsion Satellites Market Report - Table of Contents

-

1. EXECUTIVE SUMMARY & KEY FINDINGS

-

2. REPORT OFFERS

-

3. INTRODUCTION

-

3.1 Study Assumptions & Market Definition

-

3.2 Scope of the Study

-

3.3 Research Methodology

-

-

4. KEY INDUSTRY TRENDS

-

4.1 Spending On Space Programs

-

4.2 Regulatory Framework

-

4.2.1 Global

-

4.2.2 Australia

-

4.2.3 Brazil

-

4.2.4 Canada

-

4.2.5 China

-

4.2.6 France

-

4.2.7 Germany

-

4.2.8 India

-

4.2.9 Iran

-

4.2.10 Japan

-

4.2.11 New Zealand

-

4.2.12 Russia

-

4.2.13 Singapore

-

4.2.14 South Korea

-

4.2.15 United Arab Emirates

-

4.2.16 United Kingdom

-

4.2.17 United States

-

-

4.3 Value Chain & Distribution Channel Analysis

-

-

5. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2029 and analysis of growth prospects)

-

5.1 Propulsion Type

-

5.1.1 Full Electric

-

5.1.2 Hybrid

-

-

5.2 End User

-

5.2.1 Commercial

-

5.2.2 Military

-

-

5.3 Region

-

5.3.1 Asia-Pacific

-

5.3.2 Europe

-

5.3.3 North America

-

5.3.4 Rest of World

-

-

-

6. COMPETITIVE LANDSCAPE

-

6.1 Key Strategic Moves

-

6.2 Market Share Analysis

-

6.3 Company Landscape

-

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

-

6.4.1 Accion Systems Inc.

-

6.4.2 Ad Astra Rocket Company

-

6.4.3 Aerojet Rocketdyne Holdings, Inc

-

6.4.4 Airbus SE

-

6.4.5 Busek Co. Inc.

-

6.4.6 Northrop Grumman Corporation

-

6.4.7 Safran SA

-

6.4.8 Sitael S.p.A.

-

6.4.9 Thales

-

6.4.10 The Boeing Company

-

-

-

7. KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

-

8. APPENDIX

-

8.1 Global Overview

-

8.1.1 Overview

-

8.1.2 Porter's Five Forces Framework

-

8.1.3 Global Value Chain Analysis

-

8.1.4 Market Dynamics (DROs)

-

-

8.2 Sources & References

-

8.3 List of Tables & Figures

-

8.4 Primary Insights

-

8.5 Data Pack

-

8.6 Glossary of Terms

-

List of Tables & Figures

- Figure 1:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, ALL, SATELLITE MINIATURIZATION, NUMBER OF MINIATURE SATELLITES LAUNCHED (BELOW 10KG), 2017 - 2022

- Figure 2:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, ALL, SATELLITE MASS, NUMBER OF SATELLITES LAUNCHED (ABOVE 10 KG), 2017 - 2022

- Figure 3:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, ALL, OWNER OF LAUNCH VEHICLE, NUMBER OF LAUNCH VEHICLES USED, 2017 - 2022

- Figure 4:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, ALL, SPENDING ON SPACE PROGRAMS, USD, 2017 - 2022

- Figure 5:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, VALUE, USD, 2017 - 2029

- Figure 6:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY APPLICATION, VALUE, USD, 2017 - 2029

- Figure 7:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY APPLICATION, VALUE, %, 2017 VS 2023 VS 2029

- Figure 8:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY COMMUNICATION, VALUE, USD, 2017 - 2029

- Figure 9:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY EARTH OBSERVATION, VALUE, USD, 2017 - 2029

- Figure 10:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY NAVIGATION, VALUE, USD, 2017 - 2029

- Figure 11:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SPACE OBSERVATION, VALUE, USD, 2017 - 2029

- Figure 12:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY OTHERS, VALUE, USD, 2017 - 2029

- Figure 13:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SATELLITE MASS, VALUE, USD, 2017 - 2029

- Figure 14:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SATELLITE MASS, VALUE, %, 2017 VS 2023 VS 2029

- Figure 15:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY 10-100KG, VALUE, USD, 2017 - 2029

- Figure 16:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY 100-500KG, VALUE, USD, 2017 - 2029

- Figure 17:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY 500-1000KG, VALUE, USD, 2017 - 2029

- Figure 18:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY BELOW 10 KG, VALUE, USD, 2017 - 2029

- Figure 19:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY ABOVE 1000KG, VALUE, USD, 2017 - 2029

- Figure 20:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY ORBIT CLASS, VALUE, USD, 2017 - 2029

- Figure 21:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY ORBIT CLASS, VALUE, %, 2017 VS 2023 VS 2029

- Figure 22:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY ELIPTICAL, VALUE, USD, 2017 - 2029

- Figure 23:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY GEO, VALUE, USD, 2017 - 2029

- Figure 24:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY LEO, VALUE, USD, 2017 - 2029

- Figure 25:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY MEO, VALUE, USD, 2017 - 2029

- Figure 26:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY LAUNCH VEHICLE MTOW, VALUE, USD, 2017 - 2029

- Figure 27:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY LAUNCH VEHICLE MTOW, VALUE, %, 2017 VS 2023 VS 2029

- Figure 28:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY HEAVY, VALUE, USD, 2017 - 2029

- Figure 29:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY INTER PLANETARY, VALUE, USD, 2017 - 2029

- Figure 30:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY LIGHT, VALUE, USD, 2017 - 2029

- Figure 31:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY MEDIUM, VALUE, USD, 2017 - 2029

- Figure 32:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY END USER, VALUE, USD, 2017 - 2029

- Figure 33:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY END USER, VALUE, %, 2017 VS 2023 VS 2029

- Figure 34:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY COMMERCIAL, VALUE, USD, 2017 - 2029

- Figure 35:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY MILITARY & GOVERNMENT, VALUE, USD, 2017 - 2029

- Figure 36:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY OTHER, VALUE, USD, 2017 - 2029

- Figure 37:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SATELLITE SUBSYSTEM, VALUE, USD, 2017 - 2029

- Figure 38:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SATELLITE SUBSYSTEM, VALUE, %, 2017 VS 2023 VS 2029

- Figure 39:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY PROPULSION HARDWARE AND PROPELLANT, VALUE, USD, 2017 - 2029

- Figure 40:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SATELLITE BUS & SUBSYSTEMS, VALUE, USD, 2017 - 2029

- Figure 41:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SOLAR ARRAY & POWER HARDWARE, VALUE, USD, 2017 - 2029

- Figure 42:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY STRUCTURES, HARNESS & MECHANISMS, VALUE, USD, 2017 - 2029

- Figure 43:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY PROPULSION TECH, VALUE, USD, 2017 - 2029

- Figure 44:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY PROPULSION TECH, VALUE, %, 2017 VS 2023 VS 2029

- Figure 45:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY ELECTRIC, VALUE, USD, 2017 - 2029

- Figure 46:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY GAS BASED, VALUE, USD, 2017 - 2029

- Figure 47:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY LIQUID FUEL, VALUE, USD, 2017 - 2029

- Figure 48:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY REGION, VALUE, USD, 2017 - 2029

- Figure 49:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY REGION, VALUE, %, 2017 VS 2023 VS 2029

- Figure 50:

- ASIA-PACIFIC SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY COUNTRY, VALUE, USD, 2017 - 2029

- Figure 51:

- ASIA-PACIFIC SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY COUNTRY, VALUE, %, 2017 VS 2023 VS 2029

- Figure 52:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY AUSTRALIA, VALUE, USD, 2017 - 2029

- Figure 53:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY AUSTRALIA, VALUE, %, 2017 VS 2022

- Figure 54:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY CHINA, VALUE, USD, 2017 - 2029

- Figure 55:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY CHINA, VALUE, %, 2017 VS 2022

- Figure 56:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY INDIA, VALUE, USD, 2017 - 2029

- Figure 57:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY INDIA, VALUE, %, 2017 VS 2022

- Figure 58:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY JAPAN, VALUE, USD, 2017 - 2029

- Figure 59:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY JAPAN, VALUE, %, 2017 VS 2022

- Figure 60:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY NEW ZEALAND, VALUE, USD, 2017 - 2029

- Figure 61:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY NEW ZEALAND, VALUE, %, 2017 VS 2022

- Figure 62:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SINGAPORE, VALUE, USD, 2017 - 2029

- Figure 63:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SINGAPORE, VALUE, %, 2017 VS 2022

- Figure 64:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SOUTH KOREA, VALUE, USD, 2017 - 2029

- Figure 65:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SOUTH KOREA, VALUE, %, 2017 VS 2022

- Figure 66:

- EUROPE SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY COUNTRY, VALUE, USD, 2017 - 2029

- Figure 67:

- EUROPE SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY COUNTRY, VALUE, %, 2017 VS 2023 VS 2029

- Figure 68:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY FRANCE, VALUE, USD, 2017 - 2029

- Figure 69:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY FRANCE, VALUE, %, 2017 VS 2022

- Figure 70:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY GERMANY, VALUE, USD, 2017 - 2029

- Figure 71:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY GERMANY, VALUE, %, 2017 VS 2022

- Figure 72:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY RUSSIA, VALUE, USD, 2017 - 2029

- Figure 73:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY RUSSIA, VALUE, %, 2017 VS 2022

- Figure 74:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY UNITED KINGDOM, VALUE, USD, 2017 - 2029

- Figure 75:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY UNITED KINGDOM, VALUE, %, 2017 VS 2022

- Figure 76:

- NORTH AMERICA SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY COUNTRY, VALUE, USD, 2017 - 2029

- Figure 77:

- NORTH AMERICA SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY COUNTRY, VALUE, %, 2017 VS 2023 VS 2029

- Figure 78:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY CANADA, VALUE, USD, 2017 - 2029

- Figure 79:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY CANADA, VALUE, %, 2017 VS 2022

- Figure 80:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY UNITED STATES, VALUE, USD, 2017 - 2029

- Figure 81:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY UNITED STATES, VALUE, %, 2017 VS 2022

- Figure 82:

- REST OF WORLD SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY COUNTRY, VALUE, USD, 2017 - 2029

- Figure 83:

- REST OF WORLD SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY COUNTRY, VALUE, %, 2017 VS 2023 VS 2029

- Figure 84:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY BRAZIL, VALUE, USD, 2017 - 2029

- Figure 85:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY BRAZIL, VALUE, %, 2017 VS 2022

- Figure 86:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY IRAN, VALUE, USD, 2017 - 2029

- Figure 87:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY IRAN, VALUE, %, 2017 VS 2022

- Figure 88:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SAUDI ARABIA, VALUE, USD, 2017 - 2029

- Figure 89:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY SAUDI ARABIA, VALUE, %, 2017 VS 2022

- Figure 90:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY UNITED ARAB EMIRATES, VALUE, USD, 2017 - 2029

- Figure 91:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY UNITED ARAB EMIRATES, VALUE, %, 2017 VS 2022

- Figure 92:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY REST OF WORLD, VALUE, USD, 2017 - 2029

- Figure 93:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, BY REST OF WORLD, VALUE, %, 2017 VS 2022

- Figure 94:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, MOST ACTIVE COMPANIES, BY NUMBER OF STRATEGIC MOVES, 2017 - 2029

- Figure 95:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET, MOST ADOPTED STRATEGIES, 2017 - 2029

- Figure 96:

- GLOBAL SATELLITE MANUFACTURING AND LAUNCH VEHICLE MARKET SHARE(%), BY MAJOR PLAYERS, 2022

Electric Propulsion Satellites Industry Segmentation

Full Electric, Hybrid are covered as segments by Propulsion Type. Commercial, Military are covered as segments by End User. Asia-Pacific, Europe, North America are covered as segments by Region.

| Propulsion Type | |

| Full Electric | |

| Hybrid |

| End User | |

| Commercial | |

| Military |

| Region | |

| Asia-Pacific | |

| Europe | |

| North America | |

| Rest of World |

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.