Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

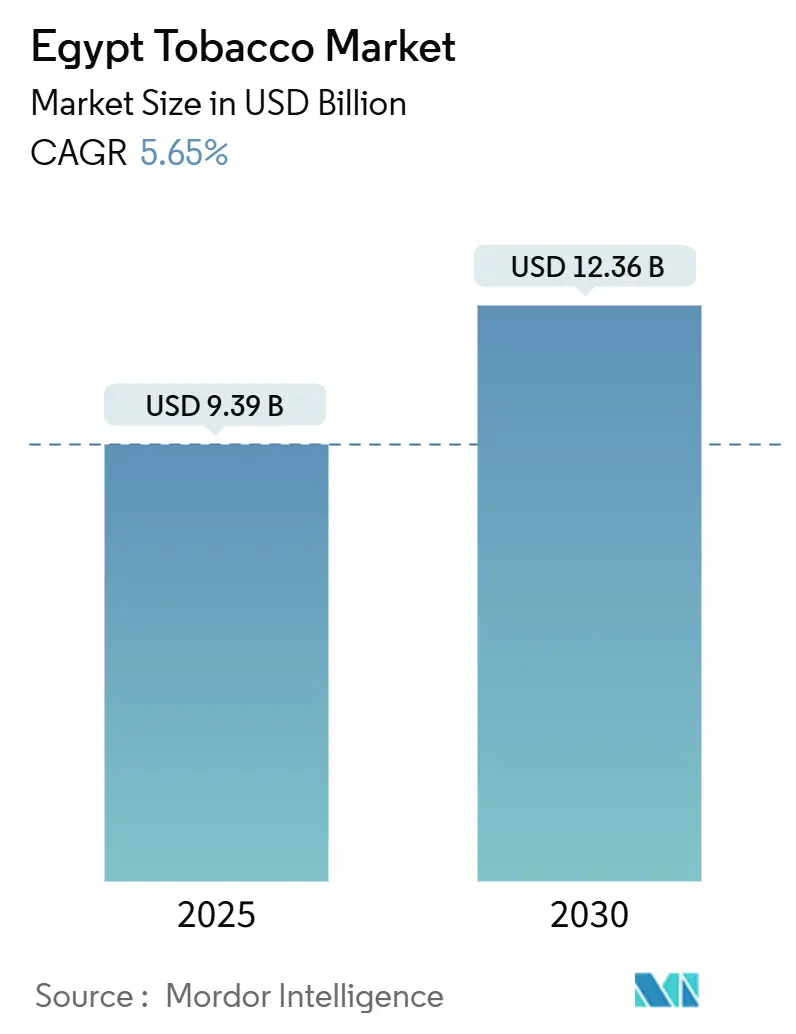

| Market Size (2025) | USD 9.39 Billion |

| Market Size (2030) | USD 12.36 Billion |

| Growth Rate (2025 - 2030) | 5.65% CAGR |

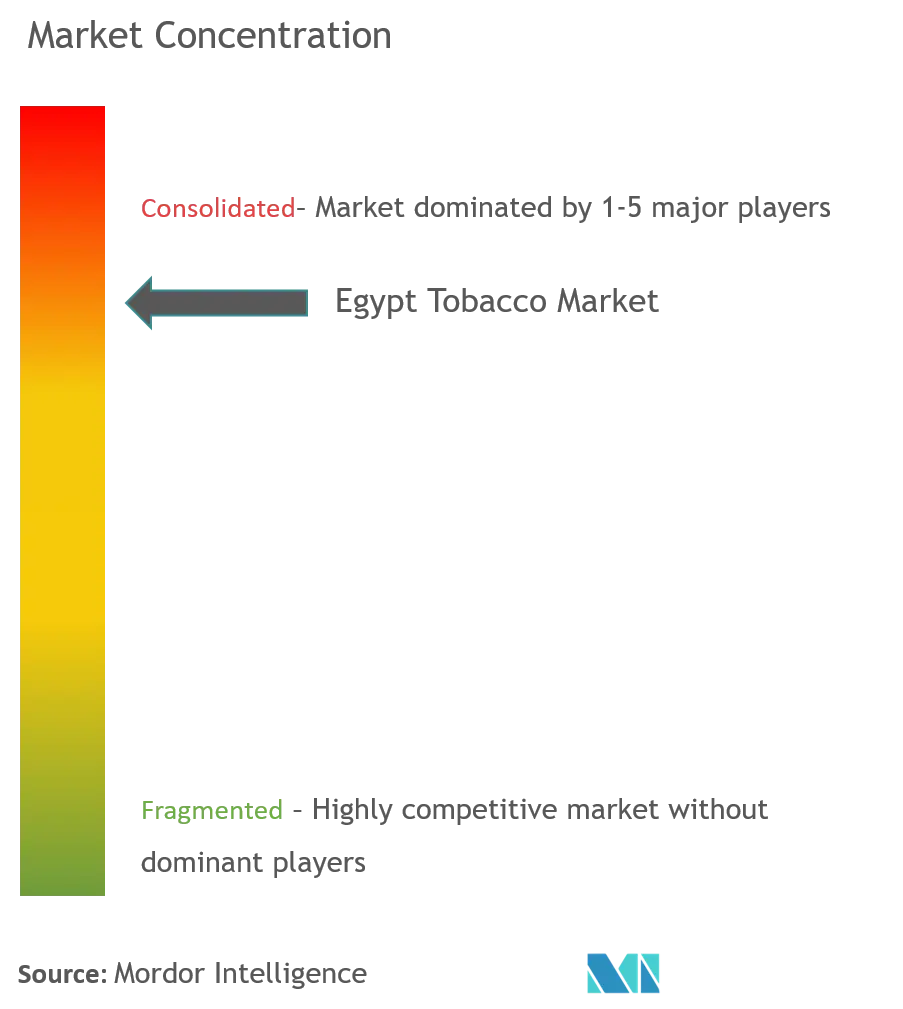

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Tobacco Market Analysis by Mordor Intelligence

By 2030, the Egyptian tobacco market, valued at USD 9.39 billion in 2025, is projected to grow to USD 12.36 billion, marking a CAGR of 5.65%. This growth is buoyed by demographic expansion, rising disposable incomes in urban centers, and a notable shift towards premium and alternative tobacco formats. Data from the International Labour Organization highlights an uptick in employment, with Egypt's workforce growing from 31.3 million in 2023 to nearly 32 million in 2024[1]Source: International Labour Organization, "Number of people employed in Egypt", www.ilostat.ilo.org. Innovations in shisha flavors, the rise of heated tobacco sticks, and changing consumption patterns among women and youth are driving both volume and value in the market. Fiscal reforms have not only stabilized the Egyptian pound but have also bolstered foreign direct investment and attracted multinational players. Concurrently, enhanced tax administration and watermark authentication efforts are targeting the 20% of illicit volume that has historically skewed legal sales. The landscape is further intensified by strategic consolidations, notably Philip Morris International's equity stakes in Eastern Company and United Tobacco, underscoring a race for technology transfer, smoke-free product development, and retail dominance.

Key Report Takeaways

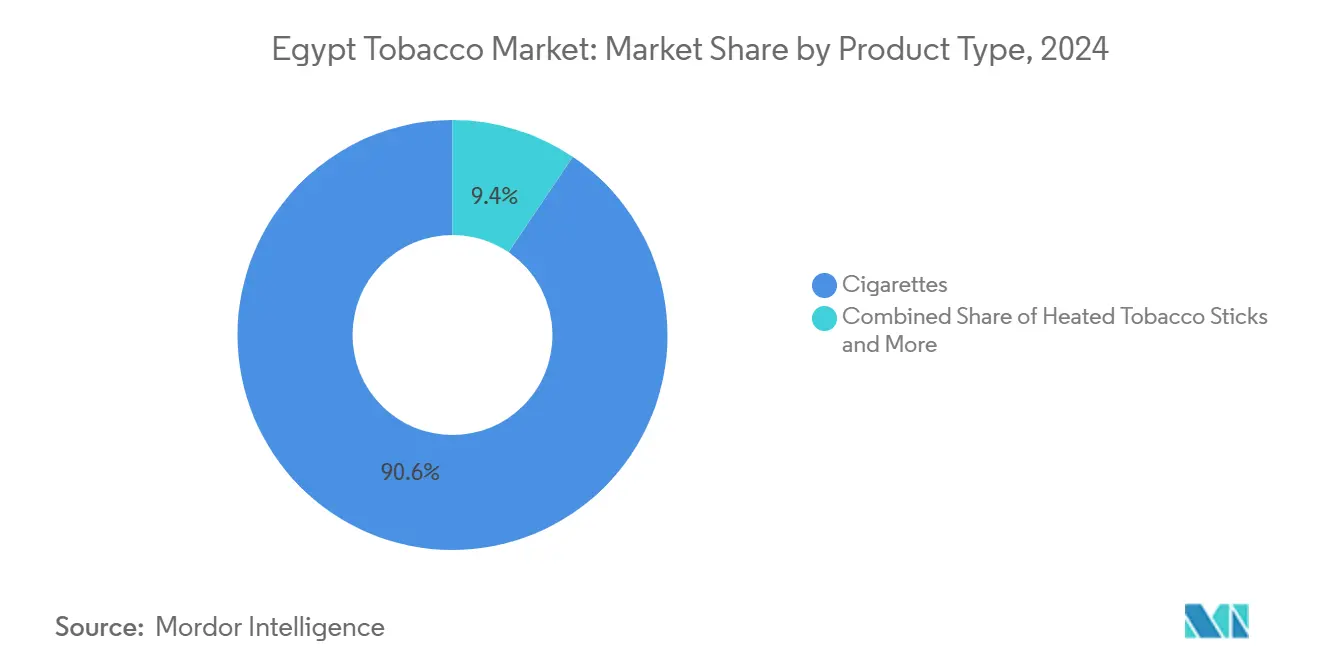

By product type, cigarettes led with 90.56% of the Egyptian tobacco market share in 2024, while heated tobacco sticks are advancing at 12.23% CAGR through 2030.

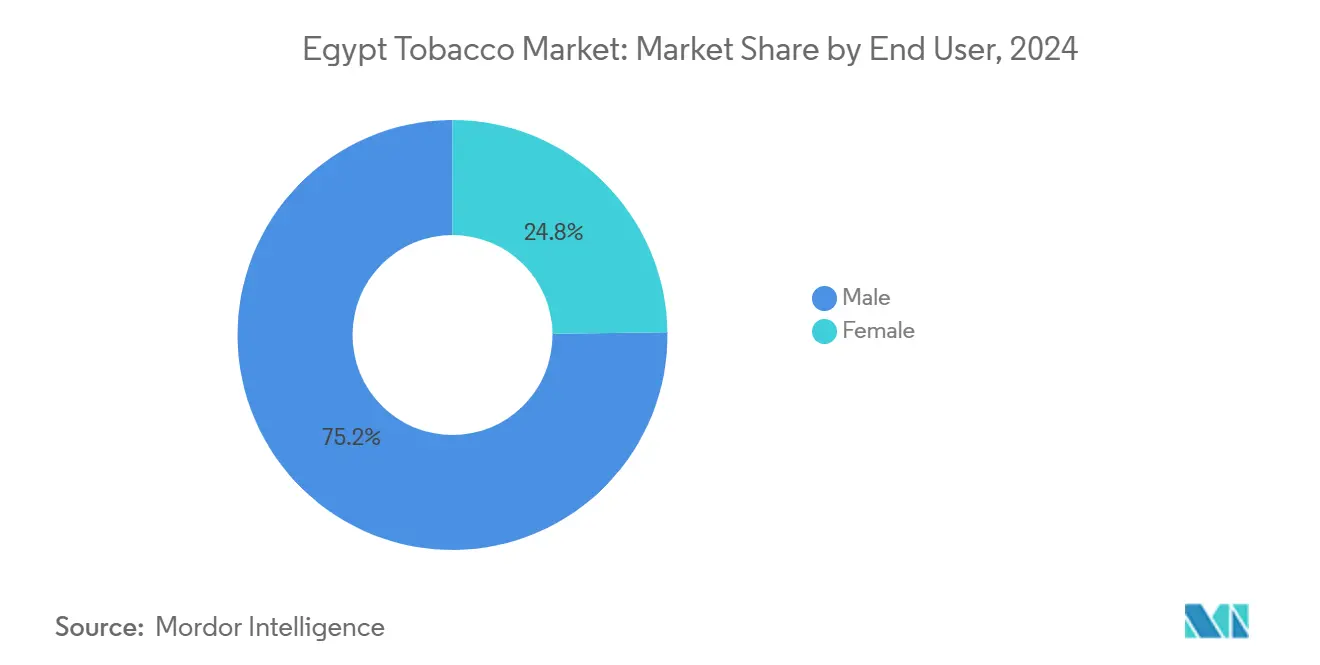

By end user, males retained 75.20% share of the Egypt tobacco market size in 2024, whereas female consumption is projected to grow at 7.89% CAGR by 2030.

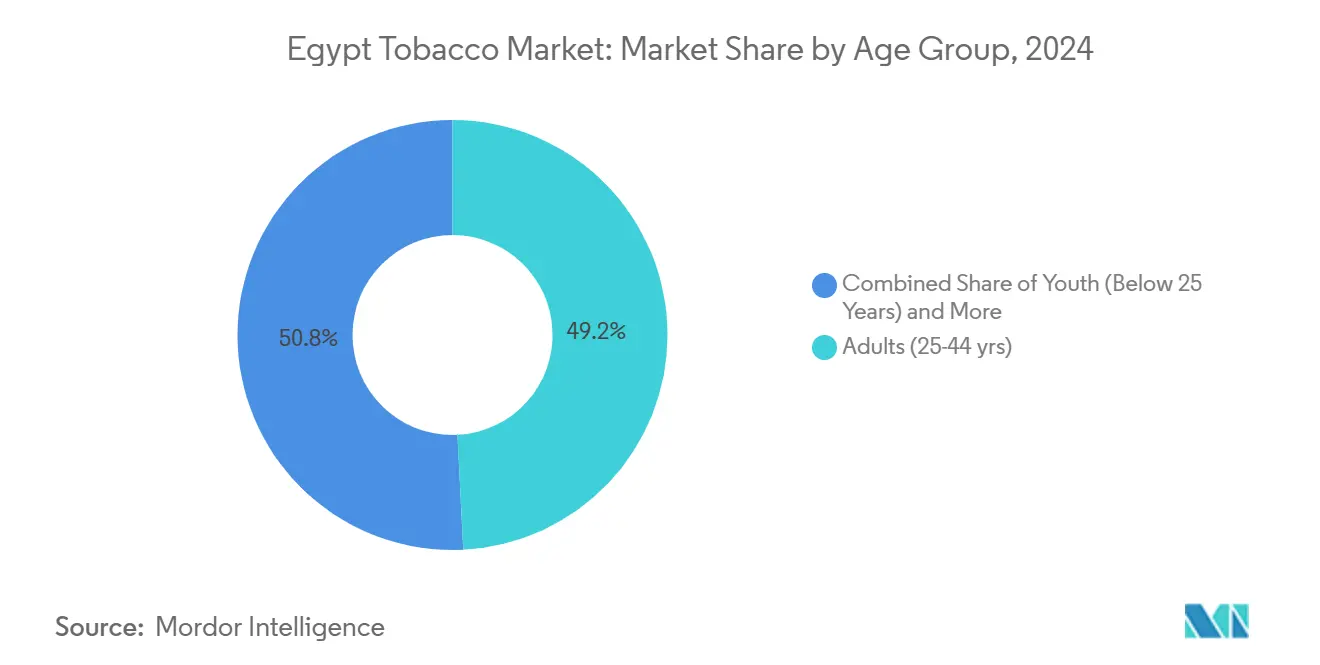

By age group, adults aged 25–44 commanded 49.20% of the Egyptian tobacco market size in 2024, and the below-25 cohort is expanding at a 7.21% CAGR through 2030.

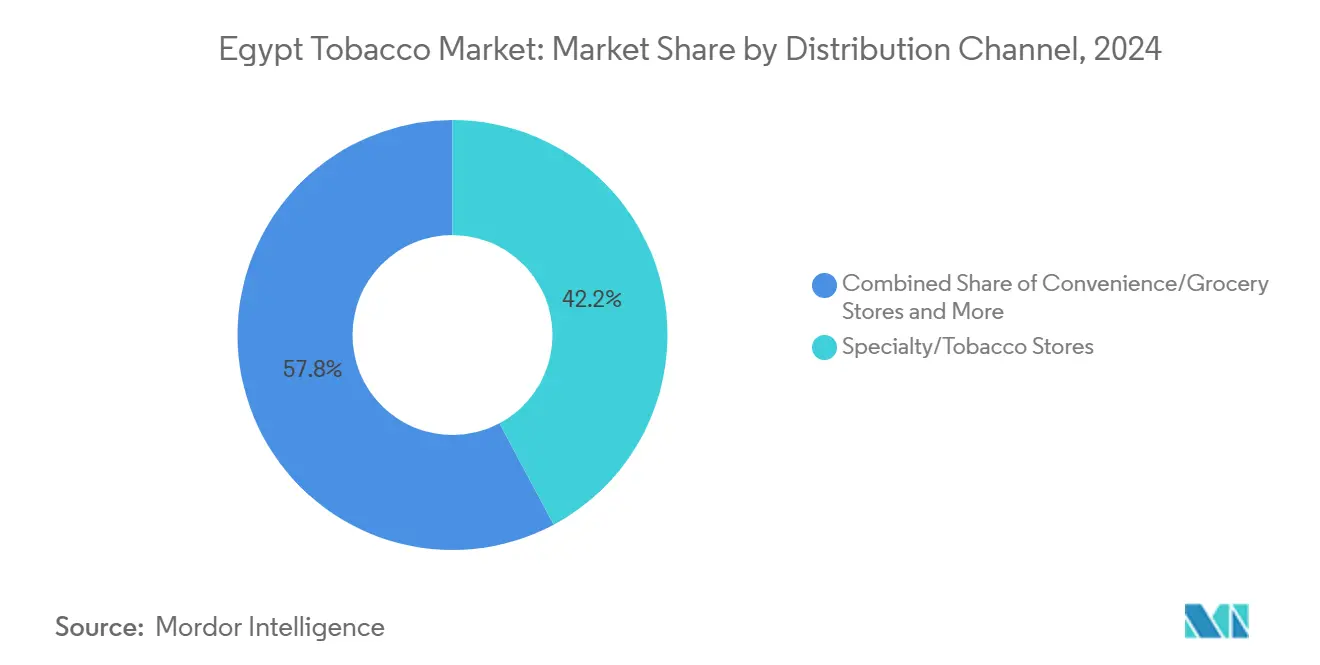

By distribution channel, specialty tobacco stores held a 42.20% share of the Egyptian tobacco market size in 2024, while convenience and grocery stores exhibit a 6.89% CAGR outlook to 2030.

Egypt Tobacco Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving Consumer Preferences Toward Diverse Product Formats | +1.2% | National, with premium segments in Cairo, Alexandria | Medium term (2-4 years) |

| Increasing Tourism and Hospitality Sector Influence | +0.8% | Red Sea resorts, Cairo, Luxor tourism corridors | Short term (≤ 2 years) |

| Accelerated Adoption of Alternative Tobacco Products | +1.5% | Urban centers, expanding to secondary cities | Long term (≥ 4 years) |

| Innovations in Flavoring and Product Customization | +0.7% | National, with early adoption in metropolitan areas | Medium term (2-4 years) |

| Enhanced Point-of-Sale Engagement and Packaging | +0.4% | National retail network | Short term (≤ 2 years) |

| Expansion of Organized and Modern Retail Channels | +0.9% | Urban and suburban markets nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Evolving Consumer Preferences Toward Diverse Product Formats

As disposable incomes rise, Egyptian tobacco consumers are increasingly leaning towards premium and alternative product categories. This shift is especially evident in the heated tobacco segment, where products like HEETS and TEREA have gained popularity, even in the face of price hikes throughout 2024. Beyond just product types, consumers are also evolving in their preferences for packaging aesthetics and brand positioning, seeking products that resonate with their lifestyle aspirations. Research shows that 41.1% of Egyptian households smoke cigarettes, with a clear preference for branded products over generic ones. This trend opens doors for companies to enhance profit margins through product differentiation and premium positioning. Notably, international brands stand to gain the most, as they can tap into global innovation pipelines to roll out new formats that cater to local tastes.

Increasing Tourism and Hospitality Sector Influence

Post-COVID, Egypt's tourism resurgence has spurred a heightened demand for traditional tobacco products, notably shisha and waterpipe tobacco, in hospitality venues spanning Red Sea resorts and historic sites. The World Tourism Organization (UN Tourism) reported that in 2023, Egypt welcomed approximately 15 million tourists, a notable rise from the 12 million recorded the prior year[2]Source: World Tourism Organization (UN Tourism), "Number of tourist arrivals in Egypt", www.unwto.org. Beyond mere consumption, the sector plays a pivotal role in shaping the cultural experiences tourists link to genuine Egyptian leisure pursuits. This tourism-induced shift in tobacco consumption patterns leads to seasonal demand variations, compelling companies to adopt agile supply chain strategies. The hospitality industry's inclination towards premium shisha tobacco and foreign cigarette brands not only boosts sales but also aligns with domestic consumption trends. Furthermore, data from the World Health Organization reveals that 7% of Egyptian households engage with waterpipe tobacco, with a considerable chunk of this activity occurring in tourism hotspots. This surge in demand, fueled by tourism, presents tobacco firms with a golden opportunity to carve out a premium brand image and tap into the international clientele flocking to Egypt.

Accelerated Adoption of Alternative Tobacco Products

Egyptian consumers are increasingly turning to heated tobacco products and e-cigarettes, signaling a heightened health consciousness and a preference for perceived harm-reduction alternatives. Even with official bans on vaping, underground markets flourish. Notably, around 80% of users in prominent social media circles claim they've successfully quit smoking using these alternative products. This trend underscores a regulatory tug-of-war: balancing public health goals against consumer demand. Such dynamics hint at possible policy shifts that might legitimize these alternative markets. Philip Morris International is betting big on Egypt, aiming for smoke-free products to account for two-thirds of its net income by 2030. This underscores the industry's bullish stance on Egypt's alternative product landscape. Moreover, users of these alternatives report significant savings over traditional cigarettes, making them particularly appealing to cost-conscious consumers. Japan Tobacco's global 40% surge in Reduced-Risk Products further bolsters the argument, pointing to a similar trajectory for Egypt as its regulatory landscape matures.

Innovations in Flavoring and Product Customization

Egyptian tobacco firms are ramping up investments in flavor innovations and product customization, aiming to stand out and align with shifting consumer tastes. The WHO's push to ban eye-catching designs and flavored products underscores the regulatory challenges tied to this trend, especially concerning its allure to the youth. In response, companies are crafting intricate flavor profiles targeting adult consumers, steering clear of any overt appeal to younger audiences. This customization wave isn't limited to flavors; packaging design is also evolving. Firms are now embedding QR codes and other transparency features, not just to engage consumers but also to fight counterfeiting. Such innovations offer a competitive edge to those adept at juggling regulatory demands with market appeal. Shisha tobacco manufacturers, in particular, are reaping the rewards. For them, flavor variety isn't just an attribute; it's a key driver of consumer loyalty and a gateway to premium pricing.

Restrains Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak Enforcement of Tobacco Control Laws | -0.3% | National, with enforcement gaps in rural areas | Long term (≥ 4 years) |

| Rising Anti-Tobacco Campaigns and Public Health Initiatives | -0.8% | Urban centers, expanding to rural communities | Medium term (2-4 years) |

| High Taxation and Regulatory Costs | -1.1% | National impact with varying regional effects | Short term (≤ 2 years) |

| Increasing Legal Restrictions on Advertising and Promotion | -0.6% | National, with stricter enforcement in major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Taxation and Regulatory Costs

Egypt's rising tobacco taxes are straining the market and limiting consumer access. The government, aiming to rake in an extra EGP 8 billion, has slapped new VAT taxes on cigarettes and vape products, underscoring the financial weight on the tobacco industry. These fresh tax hikes add to the already hefty regulatory costs, which include adapting to new watermark mandates and bolstering anti-smuggling efforts—both demanding significant shifts from manufacturers. The tax burden hits lower-income households hardest; they spend 11.1% of their budget on tobacco, facing affordability challenges that might push them towards illegal options. Studies indicate that smarter cigarette tax strategies can boost revenues and curb consumption. However, Egypt's regulatory hurdles might hinder these benefits. In response, companies are adjusting prices strategically. For instance, Philip Morris Egypt has raised prices three times in 2024, but this tactic could lead to a loss of market share to cheaper competitors.

Rising Anti-Tobacco Campaigns and Public Health Initiatives

As public health campaigns and anti-tobacco initiatives intensify, they pose challenges for market expansion, especially among younger and health-conscious consumers. Data from the WHO highlights troubling trends in tobacco use among Egyptian youth, particularly high smoking rates in adolescent boys, leading to targeted intervention programs. Campaigns draw on evidence that 24.4% of Egyptian adults use tobacco, and half are exposed to secondhand smoke at home, crafting compelling narratives for reducing consumption. The impact of these public health initiatives isn't uniform; urban, educated populations respond more to anti-tobacco messages than their rural counterparts. Amidst tightening promotional restrictions, companies grapple with brand visibility and consumer engagement. The emphasis on pictorial health warnings and enforcing smoke-free environments imposes operational challenges, demanding strategic shifts from tobacco manufacturers. Furthermore, international backing for Egypt's tobacco control, as seen in the WHO Framework Convention's implementation, indicates ongoing pressures on the industry's growth prospects.

Segment Analysis

By Product Type: Heated Tobacco Drives Innovation Wave

In 2024, cigarettes command a dominant 90.56% share of Egypt's tobacco market, underscoring deep-rooted consumer preferences and their widespread availability. Yet, the market's most dynamic growth segment is heated tobacco sticks, projected to expand at a 12.23% CAGR through 2030, driven by health-conscious consumers seeking perceived harm-reduction alternatives. Philip Morris International's strategic push of its HEETS and TEREA products underscores the commercial viability of heated tobacco in Egypt. Notably, price hikes throughout 2024 signal a strong demand, even amidst cost pressures. While cigars and cigarillos carve out a niche in the premium segment, e-cigarettes grapple with regulatory hurdles, stunting their formal market growth, even as they enjoy underground popularity.

Shisha and waterpipe tobacco, deeply woven into Egypt's cultural fabric and buoyed by tourism, see consumption in 7% of Egyptian households, per WHO data. With Egypt's tourism rebounding and its hospitality sector expanding, there's a ripe opportunity for premium product positioning and global brand recognition. E-cigarettes find themselves in a regulatory quagmire: officially banned yet readily accessible through informal avenues. Notably, around 20% of smokers over 15 view vaping as a viable alternative. This regulatory gray area not only breeds market uncertainty but also underscores a palpable consumer demand for alternatives, hinting at a potential formal market evolution should policies shift.

Note: Segment shares of all individual segments available upon report purchase

By End User: Female Segment Accelerates Consumption Growth

In 2024, male consumers dominate Egypt's tobacco market, holding a 75.20% share. This trend mirrors longstanding cultural norms where tobacco use has been predominantly male. However, the female segment, though smaller, is on a rapid ascent, boasting a 7.89% CAGR growth rate projected through 2030. This shift presents a pivotal moment for tobacco firms, urging them to craft marketing strategies and product designs that resonate with female consumers, all while being mindful of cultural nuances and advertising regulations.

Men's stronghold in the market is bolstered by societal norms and greater disposable incomes, leading to a pronounced preference for traditional cigarettes and shisha. Meanwhile, the uptick in female consumption is linked to factors like rising workforce participation, urbanization, and evolving societal views on women's tobacco use. As companies eye the burgeoning female market, they must tread carefully, weighing the potential for growth against the backdrop of regulatory scrutiny and public health debates. This demographic evolution hints at a transformative journey for the market, prompting shifts in product innovation, marketing tactics, and distribution strategies as firms strive to balance emerging trends with established market positions.

By Age Group: Youth Adoption Challenges Traditional Patterns

In 2024, adults aged 25-44 command the largest consumer segment, holding a 49.20% market share. This demographic, often in their peak earning years, showcases established consumption habits that bolster market stability. Meanwhile, consumers under 25 are emerging as the fastest-growing segment, boasting a 7.21% CAGR projected through 2030. This surge presents both lucrative opportunities and regulatory hurdles for tobacco firms. Public health authorities, alarmed by this youth trend, underscore the urgency for stricter tobacco control measures, especially against product designs that allure younger audiences. Seniors, aged 45 and above, show consistent consumption patterns, yet health concerns may steer them towards perceived lower-risk products.

The shifting age group dynamics mirror broader societal shifts, from urbanization and changing lifestyles to evolving perceptions of tobacco use. While the youth segment's growth hints at a promising market expansion, it simultaneously amplifies regulatory risks, potentially leading to tighter enforcement and advertising curbs. In response, companies are crafting age-sensitive marketing strategies and championing responsible consumption, signaling their dedication to curbing underage tobacco use. The adult segment's steadiness offers a reliable revenue base, while the youth segment's growth presents expansion avenues, albeit with a need for astute regulatory navigation and active stakeholder dialogue.

By Distribution Channel: Modern Retail Transforms Market Access

In 2024, specialty tobacco stores command a dominant 42.20% market share, capitalizing on their product expertise and extensive inventory to cater to loyal tobacco enthusiasts. Meanwhile, convenience and grocery stores are rapidly gaining ground, boasting a 6.89% CAGR through 2030. This surge underscores Egypt's retail evolution and a growing consumer inclination towards easily accessible shopping. As these channels evolve, tobacco firms see a golden opportunity, eyeing strategic alliances with contemporary retail chains and amplifying their point-of-sale interactions. Additionally, other avenues like online platforms and duty-free outlets emerge as valuable distribution channels, targeting niche consumer segments and specific buying moments.

This shift in distribution channels mirrors Egypt's overarching economic modernization and its allure for foreign direct investments, both of which bolster retail infrastructure growth. With the rise of modern retail, tobacco firms are seizing the chance to adopt advanced inventory systems, cutting-edge consumer engagement tools, and robust compliance monitoring, all aimed at boosting operational efficiency. The pivot towards convenience-centric channels highlights a shift in consumer habits, especially in urban areas where quick access to tobacco products is paramount. Yet, as companies diversify their channels, they must navigate a maze of regulatory mandates, from age verification to advertising limitations, which differ across retail formats.

Geography Analysis

Cairo and Giza, the heart of Egypt's tobacco market, account for over a quarter of the nation's smokers and generate nearly USD 3 billion in sales. Alexandria, with its maritime economy and diverse consumer base, adds another USD 1 billion to the tally. Meanwhile, resorts along the Red Sea, from Sharm el-Sheikh to Hurghada, see seasonal surges in sales, with premium shisha blends often outpacing standard cigarettes during peak tourist holidays. The World Travel and Tourism Council highlighted that in 2023, this sector contributed 8% to Egypt's GDP[3]Source: World Travel and Tourism Council, "Egypt 2024 - Annual Research: Key Highlights", www.researchhub.wttc.org.

In Upper Egypt's rural provinces, despite lower incomes, there's a strong demand for value cigarette packs and locally blended molasses. The region's lax enforcement has led to a surge in parallel imports and counterfeit products, challenging brand integrity. While the government has deployed mobile scanning units and police checkpoints on major highways to curb this leakage, the porous southern borders remain a challenge.

Governorates near the Libyan and Sudanese borders grapple with deep-rooted illicit transit routes. A watermark-stamp initiative introduced in 2024 has reportedly reduced counterfeiting by about 14% annually. With currency conditions stabilizing and foreign investments flowing into bonded warehouse infrastructure, there's a glimmer of hope for improvement. However, these high-risk areas still demand unwavering vigilance to safeguard legal sales.

Competitive Landscape

Egypt's tobacco market, characterized by a blend of established domestic players and burgeoning international firms, showcases a moderate concentration. This mix fuels competitive tensions, spurring innovation and strategic maneuvers. A pivotal shift in the market landscape emerged with the privatization of Eastern Company SAE. This move allowed Philip Morris International to make strategic inroads, acquiring stakes in both United Tobacco and Eastern Company, marking a departure from the erstwhile state dominance. Such consolidation not only paves the way for technology transfers and operational efficiencies but also accelerates product innovations. Notably, PMI has set its sights on deriving two-thirds of its net income from smoke-free alternatives by 2030.

In a market sensitive to pricing, companies are honing their competitive strategies, emphasizing premium positioning, diversifying product offerings, and broadening distribution channels. The industry's embrace of anti-counterfeiting technologies, highlighted by the use of QR codes and transparency measures, underscores a commitment to brand integrity and heightened consumer engagement. Established players eye white-space opportunities in heated tobacco products, targeting female consumers, and tapping into modern retail channels. By marrying global expertise with local insights, they aim to harness this burgeoning demand. The competitive terrain hints at further consolidation, with international firms eager to fortify their foothold in one of the few expanding global tobacco markets. Meanwhile, stringent regulatory compliance acts as a gatekeeper, favoring those incumbents with deep pockets.

Egypt Tobacco Industry Leaders

-

Eastern Company SAE

-

Philip Morris International Inc.

-

British American Tobacco PLC

-

Japan Tobacco International SA

-

Imperial Brands PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Philip Morris Misr updated and launched its heated tobacco lines HEETS and TEREA, along with new pricing for conventional cigarettes, including Merit, Marlboro, and L&M brands. This launch emphasized transparency with QR codes on packaging to inform pricing and product details for adult smokers.

- July 2025: Eastern Company, a major local tobacco manufacturer, announced a unified retail price for all its cigarette brands at LE 44 per pack. This launch included popular products such as Cleopatra King Size, Cleopatra Soft Queen, Mondial variants, and Matossian Super. The move was part of regulatory compliance with tax and health insurance systems and aimed at market stability.

- December 2024: Eastern Company and Al-Mansour International Distribution Company signed a distribution agreement to manufacture and distribute Davidoff Evolve cigarettes in Egypt. This marked a new launch of a premium cigarette brand under Imperial Brands' ownership, available in local retail channels.

- November 2024: Philip Morris Misr expanded its smoke-free product portfolio in Egypt, including market availability of HEETS and TEREA heated tobacco sticks brands and capsule varieties by the end of 2025. These launches formed part of their push toward smoke-free alternatives.

Egypt Tobacco Market Report Scope

As far as tobacco products are concerned, they are anything that contains tobacco, such as cigarettes, cigars, pipes, snuff, chewing tobacco, smokeless tobacco, or any other substance containing tobacco. The Egyptian tobacco market is segmented by product type, end-user, and distribution channel. Based on product type, the market is segmented into Cigarettes, Cigar, Cigarillos, and Cigar Pipes, E-Cigarette/HTPs. Based on end users the market is segmented into male and female. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience/small grocery stores, specialty/tobacco stores, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Cigarettes |

| Cigars and Cigarillos |

| Shisha / Waterpipe Tobacco |

| E-Cigarettes |

| Heated Tobacco Sticks |

By End User

| Male |

| Female |

By Age Group

| Youth (Below 25 Years) |

| Adults (25-44 yrs) |

| Seniors (45+ yrs) |

By Distribution Channel

| Specialty/Tobacco Stores |

| Convenience/Grocery Stores |

| Other Retail Channels |

| By Product Type | Cigarettes |

| Cigars and Cigarillos | |

| Shisha / Waterpipe Tobacco | |

| E-Cigarettes | |

| Heated Tobacco Sticks | |

| By End User | Male |

| Female | |

| By Age Group | Youth (Below 25 Years) |

| Adults (25-44 yrs) | |

| Seniors (45+ yrs) | |

| By Distribution Channel | Specialty/Tobacco Stores |

| Convenience/Grocery Stores | |

| Other Retail Channels |

Key Questions Answered in the Report

How large is the Egyptian tobacco market in 2025?

The Egyptian tobacco market size is valued at USD 9.39 billion in 2025, with a forecast to reach USD 12.36 billion by 2030.

What is the expected growth rate for tobacco sales in Egypt?

Sales are projected to increase at a 5.65% CAGR between 2025 and 2030.

Which product category is growing fastest?

Heated tobacco sticks are expanding at a 12.23% CAGR, making them the most dynamic product segment.

How significant is illicit trade in Egypt?

Illicit products account for about 20% of national volume, prompting watermark and tax-stamp countermeasures.

What share of consumption comes from female smokers?

Females represented 24.8% of legal sales in 2024, and their consumption is advancing at 7.89% CAGR to 2030.

Which retail channel shows the strongest growth?

Convenience and grocery stores are rising fastest, supported by a 6.89% CAGR as modern retail formats spread nationwide.

Page last updated on: