Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

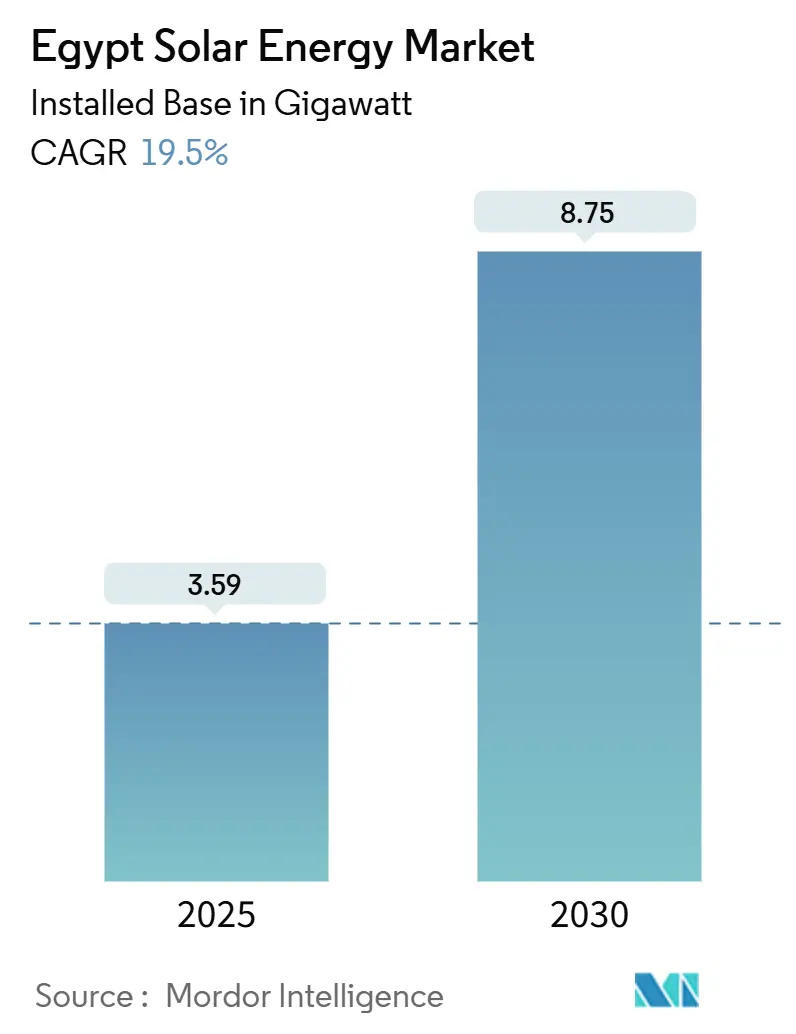

| Market Volume (2025) | 3.59 gigawatt |

| Market Volume (2030) | 8.75 gigawatt |

| Growth Rate (2025 - 2030) | 19.50% CAGR |

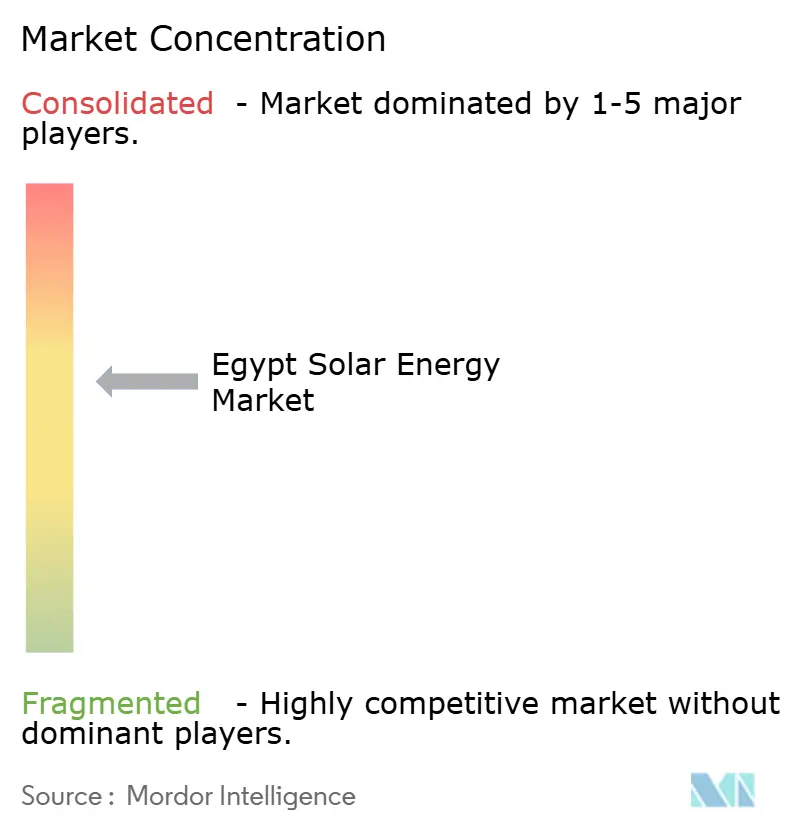

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Solar Energy Market Analysis by Mordor Intelligence

The Egypt Solar Energy Market size in terms of installed base is expected to grow from 3.59 gigawatt in 2025 to 8.75 gigawatt by 2030, at a CAGR of 19.5% during the forecast period (2025-2030).

Robust solar irradiation that exceeds 2,000 kWh/m²/year across vast desert zones, a clear government target of 42% renewable power by 2030, and deep pools of development-bank finance anchor the upward trajectory of the Egyptian solar energy market. International financiers led by the International Finance Corporation and the African Development Bank are funnelling low-cost capital into utility projects, while tariff revisions have strengthened the economics of commercial and industrial (C&I) self-consumption schemes. Localized manufacturing, exemplified by an 8 GW cell-and-module complex in New Alamein, offers a hedge against foreign-exchange swings and may eventually cut module import bills by 15-20% once scaled. Hybrid solar-plus-storage and green-hydrogen chains are emerging as the next growth layer, underpinned by Egypt’s USD 40 billion hydrogen roadmap and prime export corridors through the Suez Canal Economic Zone.

Key Report Takeaways

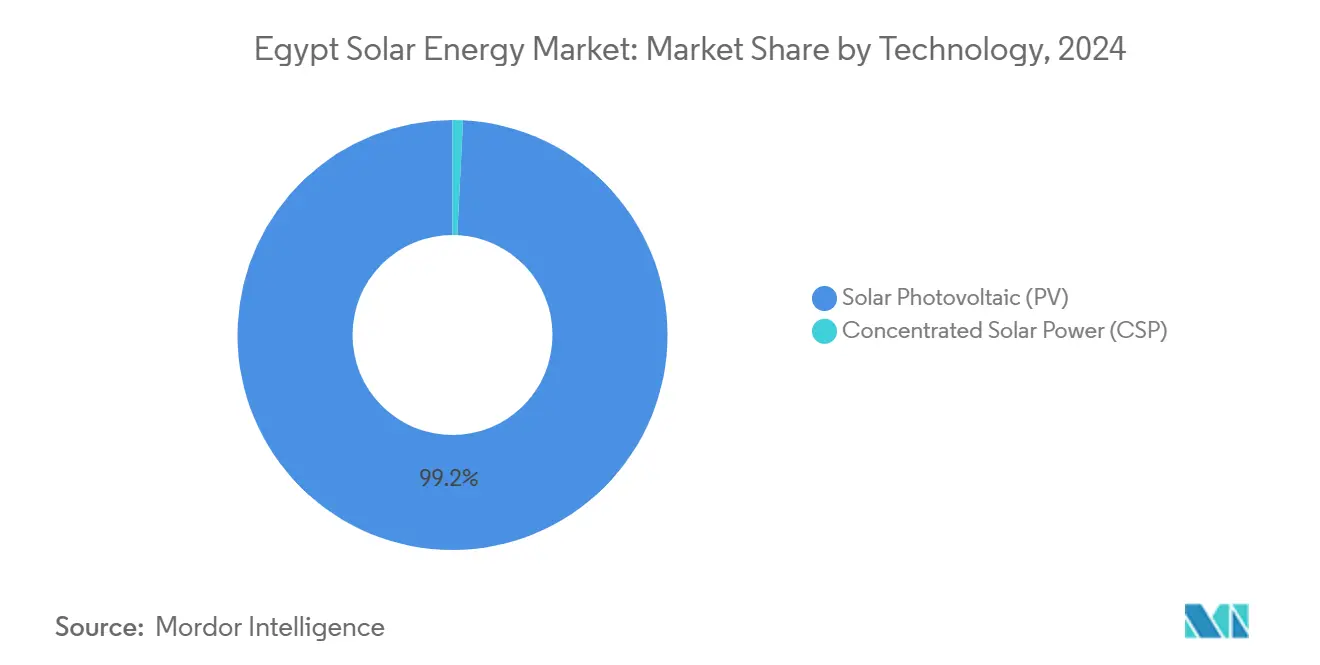

- By technology, solar photovoltaic (PV) led with 99.2% of Egypt's solar energy market share in 2024, while concentrated solar power (CSP) is projected to grow at a 65.7% CAGR through 2030.

- By grid type, on-grid systems held 97.4% share of the Egyptian solar energy market size in 2024, while off-grid solutions are forecast to expand at 27.5% CAGR through 2030.

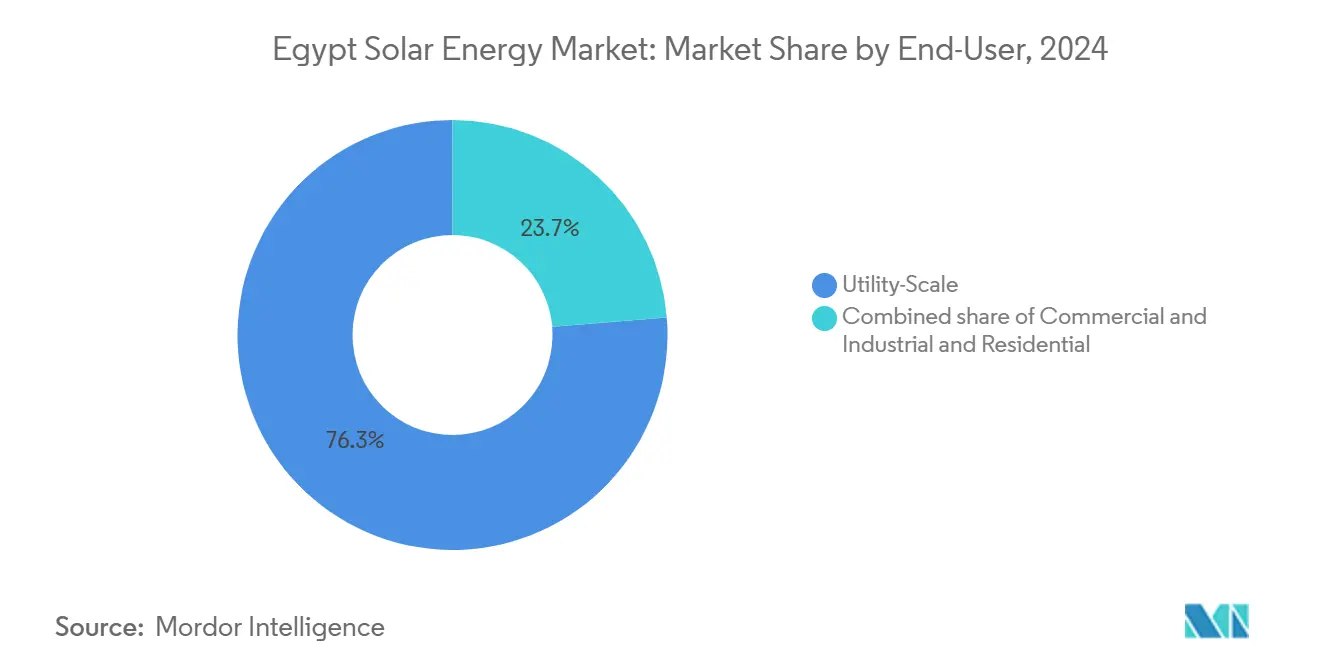

- By end-user, utility-scale plants accounted for 76.3% share of the Egyptian solar energy market size in 2024, and the commercial and industrial segment is advancing at a 29% CAGR to 2030.

Egypt Solar Energy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive government incentives & FIT revisions | +3.8% | National, especially Aswan, Benban, New Administrative Capital | Medium term (2 – 4 years) |

| High solar-irradiation levels across desert zones | +2.5% | Upper Egypt, Western Desert, Red Sea | Long term (≥ 4 years) |

| Rising international financing (IFC / EBRD / AIIB) | +4.2% | Nationwide utility-scale projects above 500 MW | Short term (≤ 2 years) |

| Green-hydrogen road-map boosting utility demand | +3.1% | Suez Canal Economic Zone, Gulf of Suez | Medium term (2 – 4 years) |

| Solar-powered desalination roll-outs in Red Sea | +1.6% | Red Sea, South Sinai, Marsa Alam | Medium term (2 – 4 years) |

| Agrivoltaics in desert reclamation projects | +1.2% | Western Desert, New Valley | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supportive Government Incentives & FIT Revisions

Egypt’s recalibrated feed-in tariff (FIT) now balances developer margins with fiscal prudence, a shift amplified by the pledge to allocate 50% of public spending to green projects by FY 2025.[1]Egyptian Electricity Regulatory Agency, “Electricity Tariff Schedule 2025,” egyptera.org New FIT bands sit comfortably below the average commercial grid tariff of 233 Pt/kWh, yet still deliver sub-six-year paybacks for well-sited arrays in sun-rich desert zones. The NWFE programme has mobilised 4.2 GW of bankable solar capacity, signalling policy credibility. As subsidies for conventional power are phased down, C&I entities are accelerating rooftop and ground-mount procurements to lock in long-term cost certainty. These reforms collectively uplift the Egyptian solar energy market by widening the pool of investable projects and compressing financing spreads.

High Solar-Irradiation Levels Across Desert Zones

Irradiation above 2,200 kWh/m²/year in Upper Egypt delivers capacity factors that rival leading global solar regions, easing the levelised cost of electricity below USD 25/MWh for the largest sites.[2]U.S. Commercial Service, “Egypt Wind and Solar Atlas,” trade.govDesert land availability side-steps the use-conflict issues that slow projects elsewhere, enabling mega-complexes such as the Benban cluster to exploit one-stop grid corridors. Recent agrivoltaic trials show yield increases in tomato and wheat crops of 10–15% when partial shading is applied, confirming dual-use land efficiency. [3]Nature, “Agrivoltaics Improves Water-Use Efficiency in Arid Climates,” nature.com Coupling high-insulation deserts with major consumption hubs via upgraded 500 kV lines further elevates project bankability. Long-run, unencumbered solar potential sits at 52 GW, nearly 18× current capacity, providing an enormous runway for the Egyptian solar energy market.

Rising International Financing

The IFC’s record USD 605 million package, matched by parallel lines from the EBRD and AIIB, has materially lowered the weighted average cost of capital for recent bids.[4]International Finance Corporation, “IFC Invests USD 605 Million in Egypt’s Green Transition,” ifc.org Multilateral lenders are now co-financing battery storage and grid-strengthening components, cutting curtailment risk. Local-currency facilities worth USD 150 million introduced by the IFC shield developers from pound volatility, an innovation quickly replicated by Egyptian banks eager to deploy green credit quotas. Grant-funded technical assistance programmes boost tender design and environmental governance, accelerating project close rates. These trends feed directly into the capital-intensity reduction pivotal for the sustained growth of the Egyptian solar energy market.

Green-Hydrogen Roadmap Boosting Utility Demand

Egypt’s aspirational 5 million t/y green-hydrogen target implies roughly 55 GW of new renewable capacity, translating into a multi-gigawatt upside for solar developers. Early-stage memoranda with European offtakers lock in take-or-pay ammonia exports from 2027, giving solar pipelines clear long-term offtake. The Green Hydrogen Incentives Law grants customs-duty relief on electrolyser imports and fast-tracks land allocation around the Suez Canal Economic Zone. Portfolio developers such as ACWA Power have already structured hybrid 2 GW solar-wind-hydrogen complexes to leverage complementary load curves. Market observers expect at least 8 GW of hydrogen-linked PV to reach financial close by 2026, injecting a demand backstop that supports the Egyptian solar energy market curve.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing wind share in Egypt's generation mix | -2.1% | Gulf of Suez, Ras Ghareb, Red Sea | Medium term (2 – 4 years) |

| FX volatility driving up imported module costs | -2.8% | National, acute for projects >60% imported content | Short term (≤ 2 years) |

| Grid-curtailment risks in Upper Egypt corridors | -1.9% | Aswan, Benban, Qena | Short term (≤ 2 years) |

| Heritage-site land-use restrictions | -0.7% | Giza, Luxor, Aswan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Wind Share in Egypt's Generation Mix

Ten-gigawatt wind concessions in the Gulf of Suez now absorb grid capacity once earmarked for solar, tightening tender volumes and raising bid competition. Capacity factors above 50% on the Red Sea coast help wind clear tariffs nearly USD 4/MWh lower than new PV at peak sunlight, skewing public-procurement preference. In auction rounds, wind has won two-thirds of awarded megawatts since 2024. While hybrid layouts exist, grid planners still schedule wind priority dispatch in coastal nodes, indirectly capping near-term additions to the Egyptian solar energy market.

FX Volatility Driving Up Imported Module Costs

A cumulative 600 bp policy-rate hike since March 2024 pushed the Egyptian pound into two-way swings exceeding 20%, inflating USD-denominated module contracts and triggering cost overruns on at least 0.7 GW of projects. Importers also face longer L/C approval queues, delaying delivery pipelines. Domestic capacity, led by an 8 GW factory in New Alamein, should supply the first modules in late 2026, but wafer inputs remain dollar-priced. Until local polysilicon output scales, foreign exchange swings may shave 2.1 percentage points from the forecast CAGR of the Egyptian solar energy market.

Segment Analysis

By Technology: CSP Acceleration From Minimal Base

Photovoltaics commanded 99.23% of Egypt's solar energy market share in 2024, reflecting turnkey EPC prices below USD 900/kW for single-axis tracking systems, while CSP's negligible baseline supports a 65.7% CAGR yet leaves its absolute footprint small through 2030. Developers see value in CSPs' built-in thermal storage for hydrogen hubs, but capital outlays of USD 3,000–11,000/kW remain a barrier.

Thermal energy storage of 6-15 hours lets CSP dispatch at night and during early-morning industrial peaks, complementing PV's daytime production and potentially trimming battery needs. Still, without a mandated CSP quota or a hydrogen off-take guarantee, financiers continue to favor crystalline-silicon PV for near-term capacity additions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Grid Type: Off-Grid Gains Amid Transmission Delays

On-grid installations held 97.4% of the Egyptian solar energy market size in 2024, yet new curtailment penalties and a 12- to 18-month substation upgrade gap spur off-grid solutions that grow at a 27.5% CAGR over 2025-2030. Rural clinics, telecom towers, and desert resorts adopt containerized solar-plus-battery kits that compete favorably with diesel at delivered fuel prices above USD 0.90/liter.

March 2024 rules waiving grid-connection fees for 1–500 kW systems sliced up-front costs by EGP 5,000–15,000 and enabled pay-as-you-go financing by local micro-lenders. Scaling hinges on aggregating small systems into portfolios large enough to satisfy institutional investors seeking predictable returns.

By End-User: C&I Surge on P2P Framework

Utility-scale plants represented 76.3% of the Egyptian solar energy market size in 2024, yet commercial and industrial installations will compound at 29% annually as factories lock in 25-year PPAs that shield them from gas curtailments and carbon-border taxes. The 1.1 GW Scatec-Egypt Aluminium deal couples 200 MWh batteries to guarantee 24/7 delivery, signaling a pivot to hybrid designs.

Textile, ceramic, and food-processing SMEs follow suit under the GIZ Egypt In-PV program, chasing paybacks under five years by replacing diesel gensets. Residential solar remains niche because subsidized retail tariffs keep household payback times above 10 years.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Upper Egypt remains the epicentre of the Egyptian solar energy market, hosting more than 70 % of installed capacity and drawing a further 2 GW pipeline over the next five years. Average irradiation surpasses 2,200 kWh/m²/year, while transmission expansion, anchored by a new 500 kV Aswan-Sohag link, will raise export capacity to the Delta load centres by 35%. Nevertheless, congestion management protocols that cap hourly feeds above 80% of rated output could dampen near-term utilisation rates until a second circuit is commissioned in 2027.

The Red Sea corridor is fast becoming a niche hub for water-energy coupling. Pilot CSP-desalination projects targeting 110 million m³/yr of potable water dovetail with tourism operators seeking carbon-neutral branding. Complementary wind regimes on the same coast enable future hybrid layouts that stabilise supply for hydrogen electrolyser farms envisioned near Ain Sokhna. Importantly, transmission spurs from the Gulf of Suez are already hydrogen-ready, featuring 400 kV ratings and redundant earthing.

The Western Desert and the New Valley Governorate mark a frontier zone where agrivoltaics intersects with desert reclamation. Early-stage data show crop-yield boosts up to 15% and water savings of roughly 50% under raised PV structures. Government grants covering 25 % of capex for dual-use pilots are attracting local farming cooperatives, a foundational customer class for distributed developers. In tandem, New Alamein’s emerging solar-component cluster could shorten inland logistics by 400 km compared with Alexandria port deliveries, tightening the supply chain for projects across the Western Desert. Collectively, geographic diversification cushions the Egyptian solar energy market against single-region policy or grid shocks.

Competitive Landscape

Strategic joint ventures dominate the competitive chessboard. BP and Masdar’s alliance with Hassan Allam and Infinity Power pools global balance sheets with local permitting acumen, positioning the consortium for hydrogen-linked solar deals exceeding 5 GW. EDF Renewables’ stake in KarmSolar grants EDF access to the fast-growing C&I niche, while injecting international governance standards into local operations. Multilateral banks’ appetite for scale tilts awards toward developers able to marshal ≥ 500 MW blocks, driving moderate consolidation within the Egyptian solar energy market.

Manufacturing localisation has emerged as a second contest front. EliTe Solar’s 8 GW module line and an adjacent USD 172 million silicon smelter promise domestic content ratios above 60% by 2027, a threshold that could unlock extra tariff premiums for qualifying projects. Rival plans tabled by China’s Jinko and the UAE’s AMEA include wafer-cutting and glass plants, signalling a race to anchor upstream value in Egypt. Over time, supply-chain proximity may shave 7-9% off total installed cost for compliant developers, tilting the cost curve in favour of local champions.

Technology differentiation now revolves around integrated storage and digital O&M. Scatec’s 1 GW Obelisk project features 200 MWh of battery storage plus AI-enabled performance analytics that predict soiling losses and automate cleaning schedules. Such innovations extend panel productivity by 3-4 % annually. Meanwhile, micro-inverter providers are courting the rooftop segment with 25-year warranties matched to evolving building-energy codes. Competitive intensity is not solely size-driven; agility in technology deployment and risk-management structures increasingly sets apart market leaders in the Egyptian solar energy market.

Egypt Solar Energy Industry Leaders

-

Abu Dhabi Future Energy Company PJSC (Masdar)

-

ACWA Power Company SJSC

-

Egyptian Electricity Holding Company

-

Scatec ASA

-

Infinity Power Holding

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: AMEA Power commissioned a 500 MW wind plant in Ras Ghareb, following its 500 MW solar PV launch in Aswan.

- June 2025: The African Development Bank approved USD 184.1 million for the Obelisk solar project with a 200 MWh storage element.

- March 2025: Scatec signed a PPA for a 1.1 GW solar-plus-storage development featuring 200 MWh of batteries.

- January 2025: ACWA Power closed financing for the 1.1 GW Suez wind project, backed by EBRD and AfDB loans.

Egypt Solar Energy Market Report Scope

Solar energy is a renewable energy source derived from the sun's radiation. It encompasses various technologies, including photovoltaic cells and solar thermal systems, which convert sunlight into electricity or heat. Solar energy is abundant, sustainable, and environmentally friendly, offering a clean alternative to traditional fossil fuels for power generation and heating applications.

The Egyptian solar energy market is segmented by Technology (Solar Photovoltaic (PV), Concentrated Solar Power (CSP)), by Grid Type (On-Grid and Off-Grid), by End-User (Utility-Scale, Commercial and Industrial (C&I), Residential), and by Component (Qualitative Analysis) (Solar Modules/Panels, Inverters (String, Central, Micro), Mounting and Tracking Systems, Balance-of-System and Electricals, Energy Storage and Hybrid Integration). For each segment, market sizing and forecasts have been done based on installed capacity.

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current installed solar capacity in Egypt?

Operational capacity stood at 3.59 GW in 2025 and is forecast to reach 8.75 GW by 2030.

How fast is photovoltaic capacity expected to grow?

Aggregate capacity is projected to rise at a 19.5% CAGR from 2025 to 2030, underpinned by concessional finance and battery-hybrid tenders.

Which segment will grow fastest through 2030?

Commercial and industrial installations are set to expand at a 29% CAGR, driven by Egypt’s P2P power framework and battery-coupled PPAs.

What policies support distributed solar adoption?

The March 2024 abolition of net-metering consolidation charges and exemption of 1–500 kW systems from grid fees significantly lowered entry costs.

How does currency risk affect project economics?

A 38% pound devaluation in 2024 inflated imported equipment costs, prompting sponsors to localize module production and renegotiate tariffs.

Who are the leading developers in Egypt’s solar space?

ACWA Power, Masdar, Scatec, AMEA Power, and Infinity Power collectively control more than 60% of capacity under construction.

Page last updated on: