Egypt Rigid Plastic Packaging Market Size

| Study Period | 2022 - 2029 |

| Base Year For Estimation | 2023 |

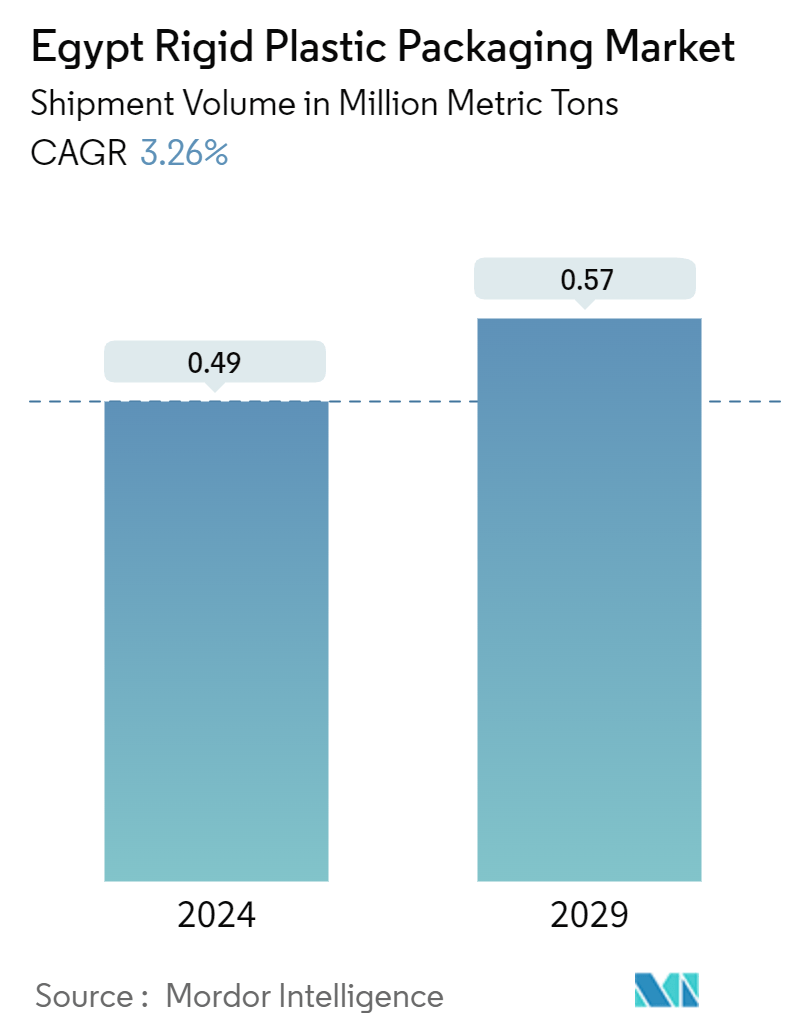

| Market Volume (2024) | 0.49 Million metric tons |

| Market Volume (2029) | 0.57 Million metric tons |

| CAGR (2024 - 2029) | 3.26 % |

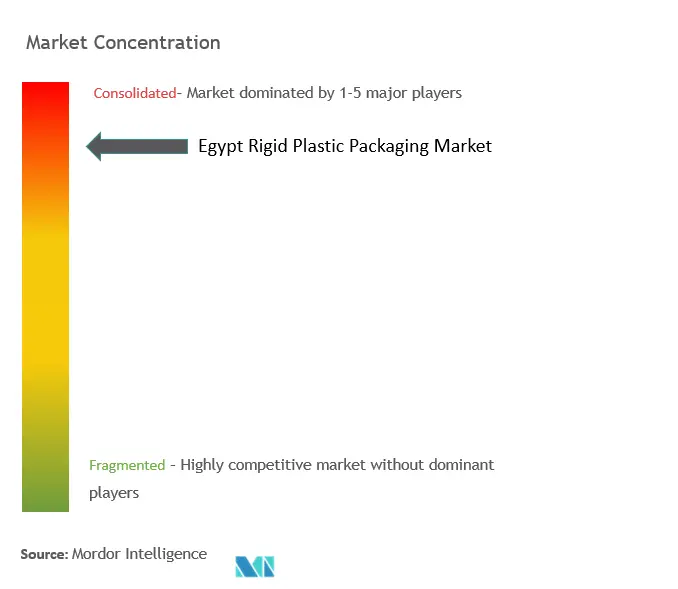

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Egypt Rigid Plastic Packaging Market Analysis

The Egypt Rigid Plastic Packaging Market size in terms of shipment volume is expected to grow from 0.49 Million metric tons in 2024 to 0.57 Million metric tons by 2029, at a CAGR of 3.26% during the forecast period (2024-2029).

Egypt's pivotal position in the Middle East, its political relevance to the United States, and its proximity to wealthy neighbors have bolstered its economy, fueling the nation's manufacturing sector, which has bolstered the packaging industry.

- As the Central Agency for Public Mobilization and Statistics (CAPMAS) reported, Egypt's population has surpassed 106 million and is on track to reach 124 million by 2030. With approximately ten million migrants from Iraq, Syria, Libya, Yemen, and Sudan residing in the country, there is a noticeable surge in food consumption. This uptick drives the demand for plastic packaging products in Egypt, including bottles, jars, trays, containers, and other rigid packaging solutions.

- Data from the United States Department of Agriculture (USDA) indicated that in Q4 2023, Egypt welcomed 3.6 million tourists, marking an 8% rise from the previous year. This influx, coupled with a robust demand for United States food products, is bolstering the country's food retail sector and, in turn, amplifying the need for rigid plastic packaging solutions, including trays, containers, and jars.

- Moreover, as urbanization accelerates, Egyptian retailers are turning to digital technology and e-commerce. This shift not only broadens consumer access to diverse food products and non-alcoholic beverages but also propels market expansion.

- In Egypt's rigid plastics packaging industry, sustainability is taking center stage. Local manufacturers, such as National Plastic Factory LLC, are prioritizing the creation of innovative, high-quality, and sustainable packaging solutions. This focus caters to the burgeoning demands of various end-use industries in the nation, driving market growth.

- Nonetheless, the Egyptian market faces challenges, primarily from shifting regulatory standards driven by heightened environmental concerns. In response to public apprehensions about plastic waste, the Egyptian government is enacting regulations aimed at curbing environmental waste and enhancing waste management. These measures, while addressing environmental concerns, pose challenges to the demand for plastic packaging solutions.

Egypt Rigid Plastic Packaging Market Trends

Polyethylene Terepthalate (PET) Segment is Estimated to Have the Largest Market Share

- PET is crucial in the rigid packaging industry, especially for producing microwavable food trays and plastic bottles. These bottles serve a range of products, from soft drinks and water to ketchup and salad dressings. Industries such as home care, beverages, and personal care are increasingly turning toward the usage of PET bottles. This trend is driven by shifting consumer preferences and the benefits of PET, notably its lightweight nature and high recycling rate.

- In Egypt, manufacturers such as Alpla Group, Bericap Holding GmbH, and Amcor GmbH prioritize developing sustainable and innovative rigid plastic packaging solutions. For example, in May 2024, Alpla Group, an Austrian company with a presence in Egypt, unveiled a recyclable PET wine bottle. This 0.75-litre bottle, weighing only 50 grams, is about eight times lighter than its glass counterpart.

- As Egypt's food service industry expands, so does the demand for PET-made packaging solutions such as jars, bottles, and containers. The rise of online food and beverage retail platforms and rapid delivery services further fuels this demand. The entry of international food chains such as KFC, Pizza Hut, and Starbucks amplifies the need for takeaway services, which predominantly use PET packaging.

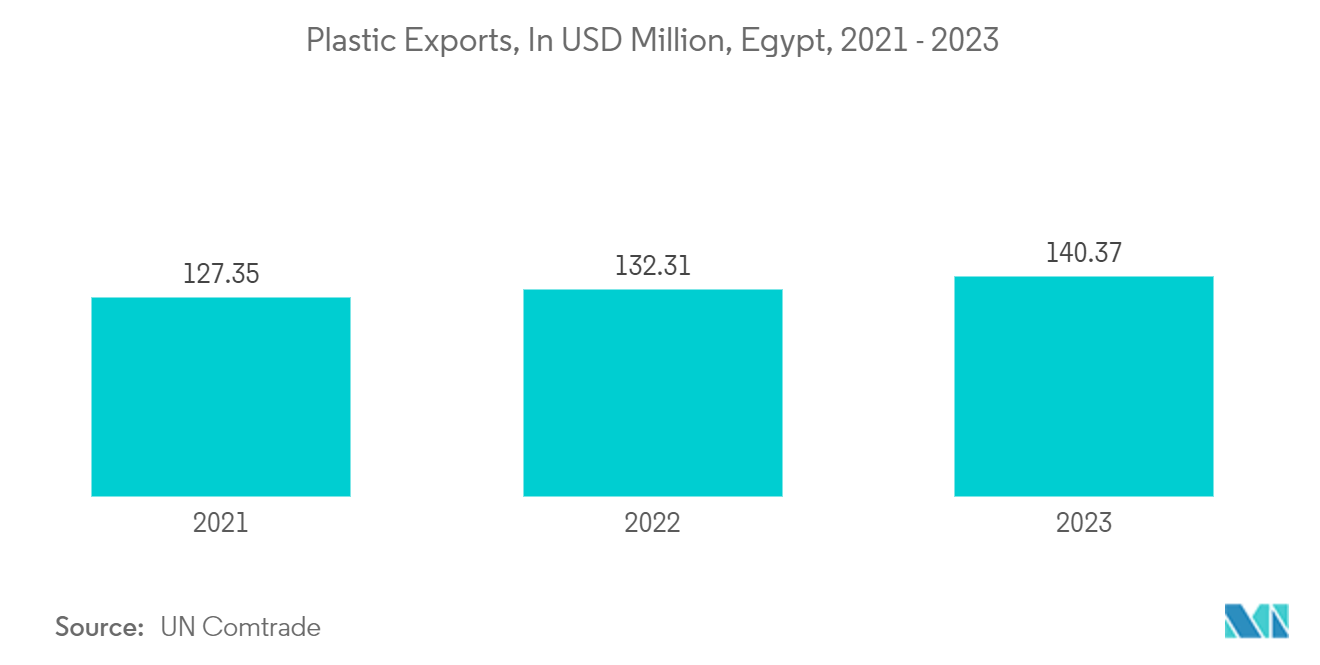

- Egypt's diverse industries, from food and beverages to personal care, heavily utilize plastic, positioning the country as a significant exporter of plastic products. Data from UN Comtrade highlighted this trend, showing Egypt's plastic product exports rose from USD 127.35 million in 2021 to USD 140.37 million in 2023.

Food Segment Expected to Hold High Market Share

- Despite facing economic challenges, Egypt welcomed 14.9 million tourists in 2023, as the US Department of Agriculture (USDA) reported. This influx set a new record for the nation and represented a 33% increase in Egypt's share of global tourism compared to 2019. By the close of 2023, Egypt had approximately 1,400 tourist restaurants. Egypt’s Minister of Tourism highlighted that this surge in tourism led to a notable uptick in food consumption across the country's hotels, restaurants, and various food service chains.

- Shifting consumer preferences fuel Egypt's rising appetite for convenience and ready-to-eat food products. The uptick in both local and imported consumer goods can be linked to the country's time-constrained middle class. For many, instant noodles and ready-to-eat frozen meals, often packaged in rigid plastic, serve as convenient dinner solutions. As packaged food products gain traction in Egypt, there is a corresponding surge in demand for plastic trays and containers.

- Changing consumer inclinations towards premium chocolate products, especially those utilizing rigid packaging such as trays and containers, make Egypt a prime market for confectionery manufacturers. Furthermore, the nation's booming e-commerce sector plays a pivotal role in driving confectionery sales, further fueling market expansion.

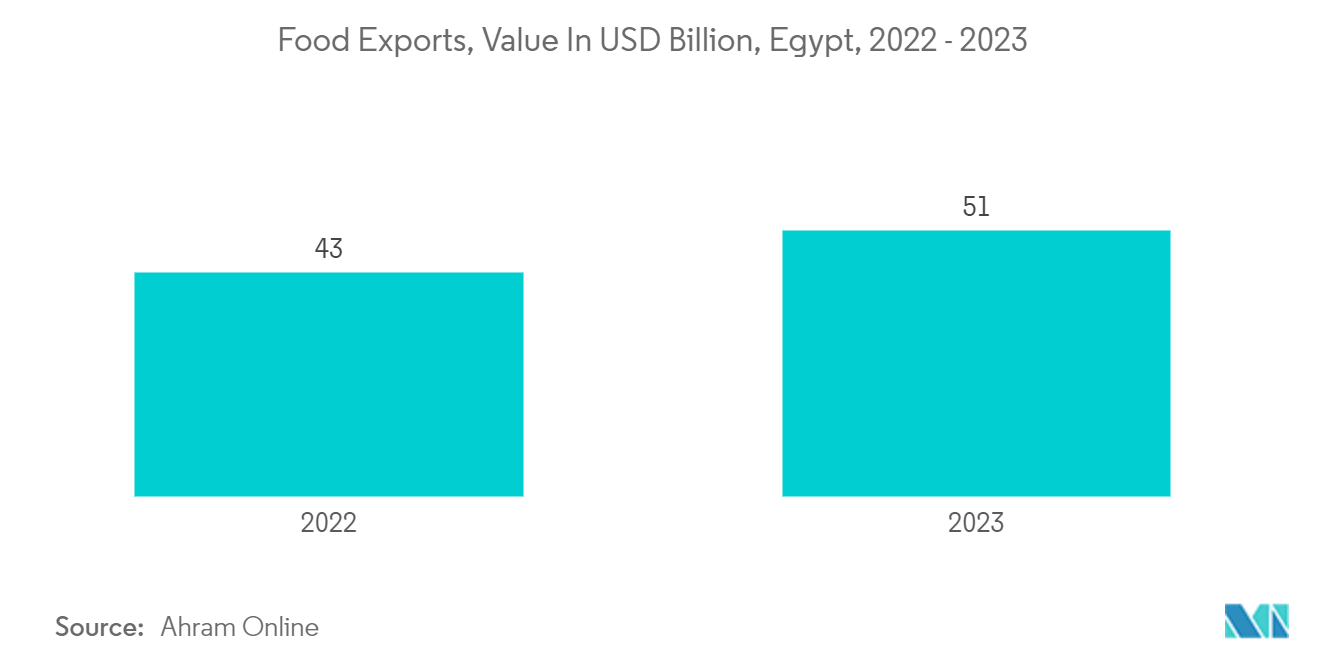

- Egypt's food exports, responding to rising consumer demand, are a significant catalyst for market growth. As reported by Ahram Online, an Egyptian newspaper, food exports surged from USD 43 billion in 2022 to USD 51 billion in 2023, marking an impressive 18.60% increase. This growth in exports amplifies the demand for rigid packaging solutions within the country.

Egypt Rigid Plastic Packaging Industry Overview

The Egyptian Rigid Plastic Packaging market is consolidated and includes players such as Amcor GmbH, Alpla Group, Bericap Holding GmbH, and NatPack, all competing for a larger slice of the market. These companies are pursuing growth through strategies such as new product development, strategic expansion, and mergers and acquisitions.

- May 2024: Alpla Group, an Austria-based company with a foothold in Egypt, bolstered its injection molding operations by launching the ALPLAInject division. This initiative enhances efficiency and drives innovation in producing injection molded items, including caps, closures, and jars.

Egypt Rigid Plastic Packaging Market Leaders

-

Alpla Group

-

Bericap Holding GmbH

-

Amcor GmbH

-

NatPack

-

PET Egypt

*Disclaimer: Major Players sorted in no particular order

Egypt Rigid Plastic Packaging Market News

- May 2024: Amcor GmbH, a Switzerland-based company with operations in Egypt, unveiled its "Bottles of the Year" program. This initiative highlights striking bottle designs that adapt to changing consumer preferences and leverage cutting-edge technology in polyethylene terephthalate (PET) plastic, underscoring a commitment to sustainability.

- November 2023: Bericap Holding GmbH, a Germany-based company with operations in Egypt, showcased its tethered caps at BrauBeviale in Nuremberg, Germany. The presentation highlighted sustainable and user-centric solutions tailored for a range of beverage categories, including juice, bottled water, carbonated soft drinks (CSD), and milk products, available in various diameters.

Egypt Rigid Plastic Packaging Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitutes

4.3.5 Intensity of Competitive Rivalry

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growth in Food Retail Sector in the Country

5.1.2 Rising Demand for Sustainable Packaging Solutions

5.2 Market Challenge

5.2.1 Stringent Regulations Pertaining to Plastic Industry

6. INDUSTRY REGULATION, POLICY AND STANDARDS

7. MARKET SEGMENTATION

7.1 By Product Type

7.1.1 Bottles and Jars

7.1.2 Trays and Containers

7.1.3 Caps and Closures

7.1.4 Intermediate Bulk Containers (IBCs)

7.1.5 Drums

7.1.6 Pallets

7.1.7 Other Product Types

7.2 By Material

7.2.1 Polyethylene (PE)

7.2.1.1 LDPE & LLDPE

7.2.1.2 HDPE

7.2.2 Polyethylene Terephthalate (PET)

7.2.3 Polypropylene (PP)

7.2.4 Polystyrene (PS) and Expanded polystyrene (EPS

7.2.5 Polyvinyl chloride (PVC)

7.2.6 Other Rigid Plastic Packaging Materials

7.3 By End-Use Industries

7.3.1 Food**

7.3.1.1 Candy & Confectionery

7.3.1.2 Frozen Foods

7.3.1.3 Fresh Produce

7.3.1.4 Dairy Products

7.3.1.5 Dry Foods

7.3.1.6 Meat, Poultry, And Seafood

7.3.1.7 Pet Food

7.3.1.8 Other Food Products

7.3.2 Foodservice**

7.3.2.1 Quick Service Restaurants (QSRs)

7.3.2.2 Full-Service Restaurants (FSRs)

7.3.2.3 Coffee and Snack Outlets

7.3.2.4 Retail Establishments

7.3.2.5 Institutional

7.3.2.6 Hospitality

7.3.2.7 Other Foodservice End-uses

7.3.3 Beverage

7.3.4 Healthcare

7.3.5 Cosmetics and Personal Care

7.3.6 Industrial

7.3.7 Building and Construction

7.3.8 Automotive

7.3.9 Other End-Use Industries (Household Products, and Logistics, among Others)

8. COMPETITIVE LANDSCAPE

8.1 Company Profiles*

8.1.1 Alpla Group

8.1.2 Bericap Holding GmbH

8.1.3 NatPack

8.1.4 Raya Plastics

8.1.5 Aquah Group

8.1.6 PET Egypt

8.1.7 National Plastic Factory LLC

8.1.8 Amcor GmbH

8.1.9 Aldelta Plastic & Co.

8.2 Heat Map Analysis

8.3 Competitor Analysis - Emerging vs. Established Players

9. RECYCLING & SUSTAINABILITY LANDSCAPE**

10. FUTURE OUTLOOK

Egypt Rigid Plastic Packaging Industry Segmentation

The scope of the study characterizes the rigid plastic packaging market based on the raw material of the product, including PP, PE, PET, and other raw materials used across various end-use industries such as food, pharmaceuticals, beverage, personal care, industrial and automotive, and more. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The Egypt Rigid Plastic Packaging Market is Segmented by Product Type (Bottles and Jars, Trays and Containers, Caps and Closures, Intermediate Bulk Containers (IMCs), Drums, Pallets, and Other Product Types), Material Type (Polyethylene (PE) (LDPE & LLDPE and HDPE), Polyethylene Terephthalate (PET), Polypropylene (PP), Polystyrene (PS) and Expanded Polystyrene (EPS), Polyvinyl Chloride (PVC), and Other Rigid Plastic Packaging Materials), and by End-Use Industries (Food (Candy & Confectionary, Frozen Foods, Fresh Produce, Dairy Products, Dry Foods, Meat, Poultry and Seafood, Pet Food and Other Food Products), Foodservice (Quick Service Restaurants, Full Service Restaurants, Coffee and Snack Outlets, Retail Establishments, Institutional, Hospitality and Other Foodservice End-uses), Beverage, Healthcare, Cosmetics and Personal Care, Industrial, Building and Construction, Automotive and Other End-Use Industries (Household Products, and Logistics)). The Market Sizing and Forecasts are Provided in Terms of Volume (Tons) for all the Above Segments.

| By Product Type | |

| Bottles and Jars | |

| Trays and Containers | |

| Caps and Closures | |

| Intermediate Bulk Containers (IBCs) | |

| Drums | |

| Pallets | |

| Other Product Types |

| By Material | ||||

| ||||

| Polyethylene Terephthalate (PET) | ||||

| Polypropylene (PP) | ||||

| Polystyrene (PS) and Expanded polystyrene (EPS | ||||

| Polyvinyl chloride (PVC) | ||||

| Other Rigid Plastic Packaging Materials |

| By End-Use Industries | ||||||||||

| ||||||||||

| ||||||||||

| Beverage | ||||||||||

| Healthcare | ||||||||||

| Cosmetics and Personal Care | ||||||||||

| Industrial | ||||||||||

| Building and Construction | ||||||||||

| Automotive | ||||||||||

| Other End-Use Industries (Household Products, and Logistics, among Others) |

Egypt Rigid Plastic Packaging Market Research FAQs

How big is the Egypt Rigid Plastic Packaging Market?

The Egypt Rigid Plastic Packaging Market size is expected to reach 0.49 million metric tons in 2024 and grow at a CAGR of 3.26% to reach 0.57 million metric tons by 2029.

What is the current Egypt Rigid Plastic Packaging Market size?

In 2024, the Egypt Rigid Plastic Packaging Market size is expected to reach 0.49 million metric tons.

Who are the key players in Egypt Rigid Plastic Packaging Market?

Alpla Group, Bericap Holding GmbH, Amcor GmbH, NatPack and PET Egypt are the major companies operating in the Egypt Rigid Plastic Packaging Market.

What years does this Egypt Rigid Plastic Packaging Market cover, and what was the market size in 2023?

In 2023, the Egypt Rigid Plastic Packaging Market size was estimated at 0.47 million metric tons. The report covers the Egypt Rigid Plastic Packaging Market historical market size for years: 2022 and 2023. The report also forecasts the Egypt Rigid Plastic Packaging Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Egypt Rigid Plastic Packaging Industry Report

Statistics for the 2024 Egypt Rigid Plastic Packaging market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Egypt Rigid Plastic Packaging analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Egypt Rigid Plastic Packaging Market Report Snapshots