Egypt Real Estate Brokerage Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

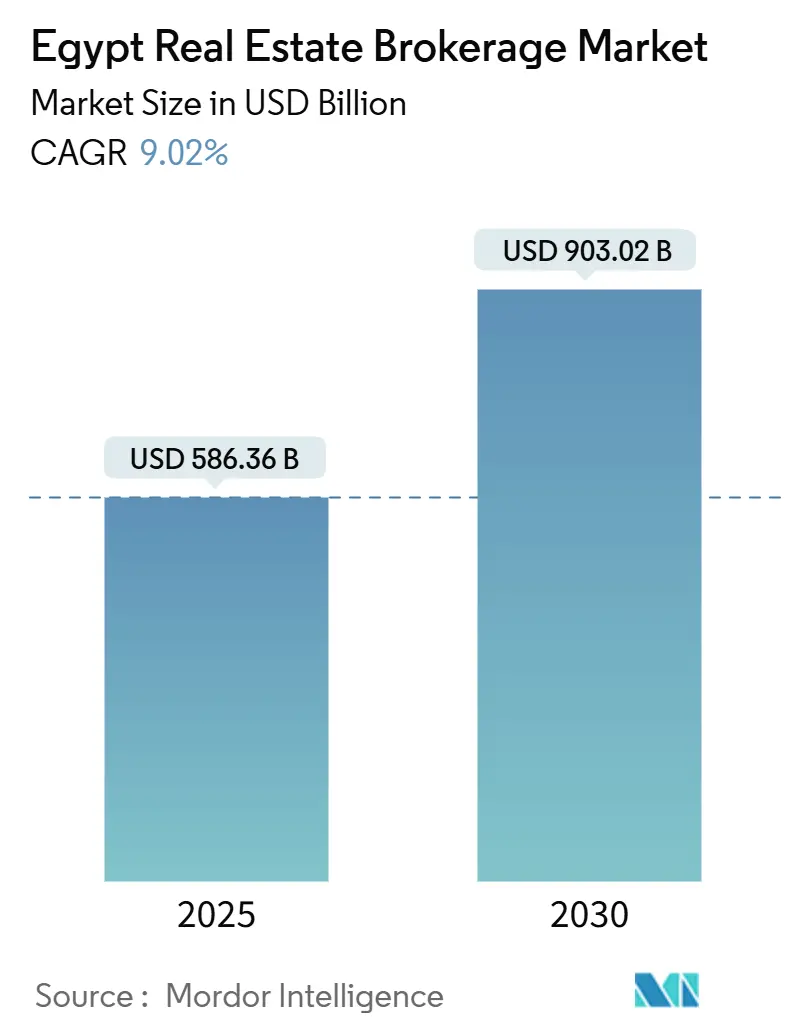

| Market Size (2025) | USD 586.36 Billion |

| Market Size (2030) | USD 903.02 Billion |

| Growth Rate (2025 - 2030) | 9.02% CAGR |

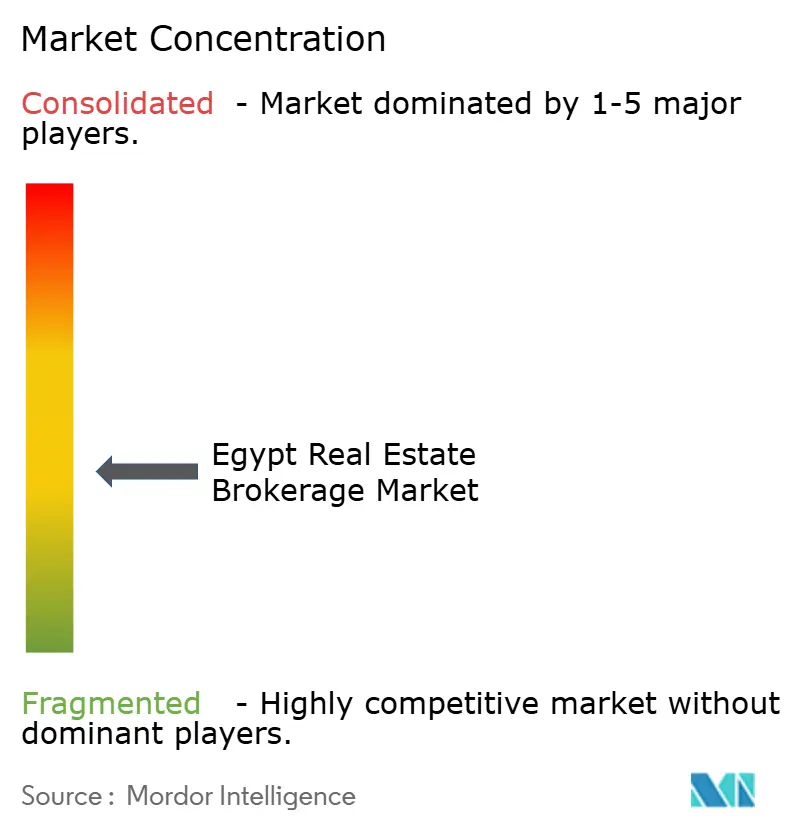

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Real Estate Brokerage Market Analysis by Mordor Intelligence

The Egypt Real Estate Brokerage Market size is estimated at USD 586.36 billion in 2025, and is expected to reach USD 903.02 billion by 2030, at a CAGR of 9.02% during the forecast period (2025-2030). This sustained expansion is supported by accelerated urban development programs, a gradual rebound in mortgage availability, and growing foreign participation following the liberalization of property ownership rules. Rising demand for brokerage support in both primary and secondary transactions around the New Administrative Capital, combined with widening adoption of PropTech platforms, is enlarging deal pipelines and pushing margins higher. Brokerage firms able to blend traditional relationship networks with data-driven lead-generation tools continue to gain wallet share as clients seek faster closings and transparent pricing. Currency volatility and fragmented title-registration processes remain short-term headwinds, yet these pressures are partly offset by the government’s commitment to streamline land registries and maintain infrastructure spending.

Key Report Takeaways

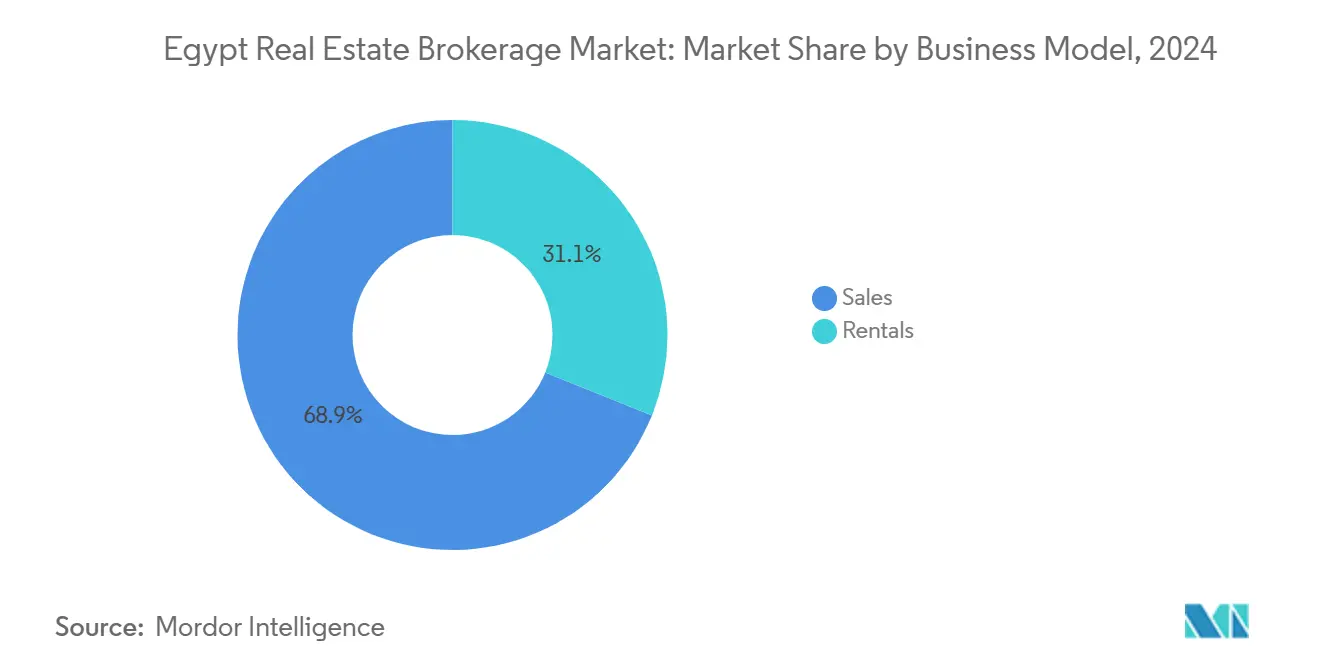

- By business model, sales transactions led with 68.9% revenue share in 2024, while rental services are projected to compound at a 9.85% CAGR through 2030.

- By property type, residential brokerage captured 71.2% of the Egypt real estate brokerage market share in 2024; commercial brokerage is poised for a 9.71% CAGR to 2030.

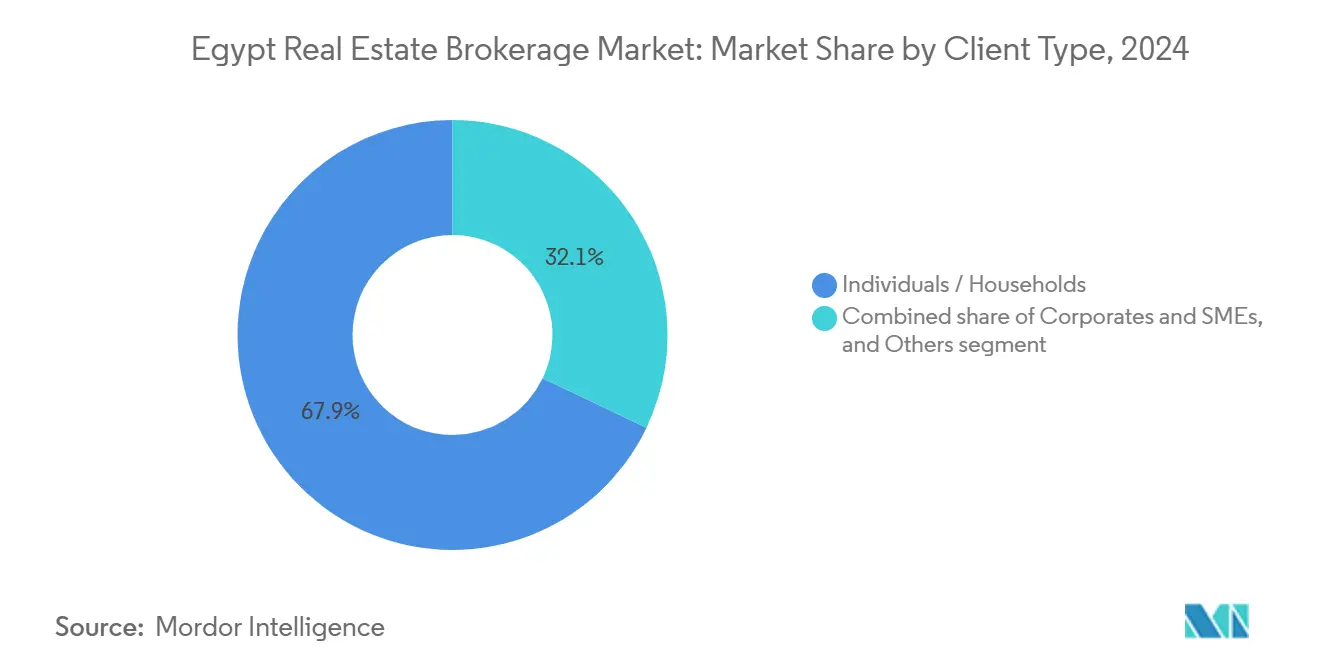

- By client type, individual and household buyers accounted for 67.9% of total activity in 2024, whereas corporate and SME clients represent the fastest-growing cohort at 9.95% CAGR to 2030.

- By geography, Greater Cairo generated 86.9% of 2024 revenues; Giza is forecast to expand at a 10.09% CAGR over the outlook period.

Egypt Real Estate Brokerage Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban expansion in Greater Cairo and new city developments increasing transaction volumes | +1.4% | Greater Cairo, New Administrative Capital, satellite cities | Medium term (2-4 years) |

| Government-led new urban communities creating steady primary and resale activity | +1.1% | National, concentrated in Greater Cairo and Giza | Long term (≥ 4 years) |

| Developer installment plans and gradual mortgage expansion broadening buyer access | +0.9% | National, with higher penetration in urban centers | Medium term (2-4 years) |

| Rapid growth of digital listings and PropTech tools improving lead generation and conversions | +0.7% | National, urban-focused with Greater Cairo leading adoption | Short term (≤ 2 years) |

| Diaspora and foreign interest in prime/second-home locations supporting brokerage pipelines | +0.5% | North Coast, New Administrative Capital, premium Cairo districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban expansion in Greater Cairo and new city developments are increasing transaction volumes

In Egypt, the New Administrative Capital's Central Business District is transforming the urban landscape. This area features several towers over 160 meters tall, designed to achieve the highest environmental certification, LEED platinum. Additionally, the Nour Capital Gardens project, covering 5,000 acres, plans to deliver 140,000 housing units. This large-scale project supports ongoing property sales and future resales, ensuring a steady supply of inventory for years. The New Urban Communities Authority’s predictable land-release schedules allow real estate brokers to plan their marketing efforts and staffing efficiently. As government ministries and major companies relocate to the new capital, demand for rental housing nearby has increased significantly. These developments are expanding the area’s real estate market, creating a need for expert brokerage services, particularly in property valuation and compliance with zoning regulations[1]Assem El Gazzar, “Official Statement on New Administrative Capital Progress,” Ministry of Housing Utilities and Urban Communities, moh.gov.eg.

Government-led new urban communities are creating steady primary and resale activity

Major projects, such as the USD 35 billion Ras El-Hekma development, have already caused land prices on the North Coast to double. This increase creates immediate opportunities for brokers to earn commissions, with additional resale opportunities expected after the first properties are handed over. Similarly, Talaat Moustafa Group's USD 21 billion South Med project highlights how government policies are successfully attracting large-scale private investments. The New Urban Communities Authority has introduced transparent tender processes, making it easier for brokers to access property listings. However, political factors in site allocation still require careful research and analysis. These new developments are expanding the real estate brokerage market in Egypt beyond Greater Cairo, offering steady income as early buyers resell properties or purchase additional units.

Developer installment plans and gradual mortgage expansion broaden buyer access

Banks are gradually restarting mortgage services, supported by a USD 35 billion agreement with the UAE and an USD 8 billion package from the IMF. These developments are helping potential homebuyers move from paying in cash to using structured financing options. Developers are now offering installment plans that can last up to seven years, which has become a common practice. This approach reduces the upfront payment required and allows more people to qualify for home purchases. The updated Real Estate Mortgage Law provides clear legal guidelines for both lenders and borrowers. Additionally, brokers who assist with paperwork and work with non-banking finance companies can earn extra fees. Currently, about 50% of property transactions are still completed in cash, leaving significant room for mortgages to grow, which could increase the number and speed of transactions across different price ranges.

Diaspora and foreign interest in prime and second-home locations supporting brokerage pipelines

Egypt introduced a policy allowing non-residents to own unlimited properties in late 2024, expanding the potential customer base for its real estate brokerage market. This change led to a 15% increase in property purchases by foreign buyers during the year. Remittances, which surpassed USD 29.4 billion, have provided brokers with a strong source of funds to market high-end coastal and urban properties. Buyers from Gulf countries are particularly interested due to rental returns of 6-8%, which help them diversify their income. To serve this growing demand, real estate agencies now offer services like bilingual documentation, secure payment options, and property management after purchase. This trend has boosted the sale of luxury and vacation properties, driving growth in both new property launches and resale listings.[2]Mohamed Salah Eldin, “Cabinet Approves Unlimited Foreign Property Ownership Decree,” Government of Egypt Gazette, egypteconomy.gov.eg.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency instability and high inflation dampening purchasing power and deal closure rates | -0.7% | National, with urban areas experiencing higher price volatility | Short term (≤ 2 years) |

| Title verification and regulatory complexity increasing due-diligence timelines | -0.5% | National, with particular challenges in older urban areas | Medium term (2-4 years) |

| Limited mortgage penetration versus cash purchases constraining scalable demand | -0.3% | National, rural areas most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency instability and high inflation are dampening purchasing power and deal closure rates

In 2024, the Egyptian pound lost 40% of its value, while inflation rose sharply to 32%. These economic challenges reduced household purchasing power, forcing developers to increase unit prices and delay project completions. In 2025, property prices are expected to rise by 10-30%, which could strain middle-income buyers unless wages grow at a similar rate. By the end of 2024, the Central Bank's reserves reached USD 46.4 billion. However, buyers remain cautious, preferring payment plans or smaller properties to manage costs. For Egyptians living abroad, unstable exchange rates make it difficult to plan money transfers effectively. Although the IMF predicts inflation will ease by early 2025, real estate brokers still face challenges, such as negotiating prices and addressing buyer concerns about fluctuating costs[3]Hassan Abdalla, “Monthly Statistical Bulletin December 2024,” Central Bank of Egypt, cbe.org.eg.

Title verification and regulatory complexity are increasing due diligence timelines

In Cairo, only 5% of properties are officially registered, causing delays in verifying ownership and completing legal checks. The city’s digital deeds program aims to reduce the time needed to register properties to 30 days, but implementation challenges remain, particularly in crowded areas. Rules requiring foreign buyers to pay in hard currency add extra paperwork, while tax assessments on land and buildings by the Real Estate Tax Department further complicate the process. Although recent reductions in fees have been welcomed, unresolved issues with historical ownership records continue to slow progress. Consequently, real estate brokerages with their own legal teams or strong connections with notaries are charging higher fees for their advisory services.

Segment Analysis

By Business Model: Sales Dominance Amid Rental Acceleration

Sales brokerage retained 68.9% of 2024 revenue, supported by Egypt’s top developers doubling contracted sales to USD 28.6 billion, which generated sizeable commission pools. The Egypt real estate brokerage market size for sales is projected to expand steadily yet at a slower clip than rentals as the market matures. Rental services, propelled by rent-control reforms introducing seven-year transition periods and escalation clauses, are outpacing overall market growth with a 9.85% CAGR. The Egypt real estate brokerage market is witnessing rising corporate leasing tied to ministry relocations and the influx of multinational tenants into the New Administrative Capital. Brokers that diversify into tenant-representation and rent-review advisory stand to gain, especially where rental yields average 6-8%.

Regulatory modernization is unlocking sizeable previously frozen stock, prompting landlords to seek professional agents for pricing guidance and tenant screening. Simultaneously, sales intermediaries are leveraging digital tools to shorten deal cycles and maintain share of wallet. The Egypt real estate brokerage market continues to favor hybrid agencies capable of servicing both sales and leasing because clients increasingly demand end-to-end life-cycle support. As households weigh buy-versus-rent decisions against inflation and financing terms, brokers offering comparative analytics will differentiate. Over the forecast horizon, rental momentum is unlikely to erode sales leadership entirely, yet it will even out commission seasonality.

By Property Type: Residential Leadership with Commercial Momentum

Residential transactions generated 71.2% of 2024 volumes, anchoring the Egypt real estate brokerage market size in absolute dollar terms. Rapid urbanization, metro extensions, and the popularity of gated communities around New Cairo and Sixth of October City sustain high absorption. Commercial brokerage, however, is forecast to log a 9.71% CAGR, reflecting demand for Grade-A offices in the New Administrative Capital and the proliferation of logistics parks along the Cairo-Ismailia corridor. The Egypt real estate brokerage market is an accommodating sectoral diversification as mixed-use master plans combine retail, hospitality, and data-center components.

Commercial lease tenures are lengthening, improving recurring income for agencies skilled in facility management and tenant-improvement negotiations. Residential brokers face rising price sensitivity among middle-income buyers and must match aspirational lifestyles with installment plans. Smart-city certifications such as LEED are now differentiators for office towers, requiring brokers to translate technical green-building metrics into value propositions for corporate clients. Meanwhile, the “other commercial” bucket, data centers, healthcare campuses, and education assets, demands niche valuation approaches and is opening advisory niches for specialist firms.

By Client Type: Corporate Acceleration Reshaping Service Models

Individuals and households still command 67.9% of the Egypt real estate brokerage market share, driven by first-time buyers and upgraders pursuing suburban villas or coastal second homes. Yet corporate and SME clients are compounding at 9.95% CAGR, buoyed by Egypt’s manufacturing push and privatization pipeline. The Egypt real estate brokerage market is therefore rebalancing toward enterprise-grade advisory covering headquarters consolidation, sale-and-leaseback structures, and portfolio optimization.

Brokers now package space-utilization analytics and ESG compliance reviews to meet multinational corporate governance requirements. For individuals, brokers emphasize school proximity, transport links, and payment-plan flexibility. A growing subset of diaspora buyers requires dual-language support and escrow safeguards. Institutional investors and REITs, while still niche, demand sophisticated financial modeling and regulatory liaison, offering higher fee yields per deal.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Greater Cairo maintained an 86.9% revenue share in 2024 as it hosts the lion’s share of premium inventory, public institutions, and multinational employer campuses. Average prime-area prices climbed to USD 1,500 per square meter in 2024 on improved metro connectivity and the halo from the New Administrative Capital. The Egypt real estate brokerage market size in Greater Cairo remains considerable, but urban density is triggering spillover demand toward satellite communities such as New Cairo, Mostakbal City, and El Shorouk. Brokers operating here must juggle traditional resales within central districts and greenfield launches on the periphery.

Giza is forecast to log a 10.09% CAGR, the fastest nationwide, thanks to upgraded ring-road links and land-bank releases adjacent to the Grand Egyptian Museum precinct. The Egypt real estate brokerage market increasingly views Giza as a natural westward expansion zone for Cairo’s workforce. Alexandria, Egypt’s Mediterranean gateway, confronts aging infrastructure yet holds latent upside tied to its waterfront redevelopment master plan targeting a population jump to 5.2 million by 2030. Brokerage assignments here mix heritage refurbishments with new hospitality-driven projects aiming to capture tourism inflows.

The Rest-of-Egypt category covers Sinai’s New Rafah city, upgraded Arish Port, and the transformational Ras El-Hekma coastal hub, where land prices have already doubled. The Egypt real estate brokerage market faces varied regulatory frameworks across governorates, compelling agencies to invest in local partnerships. Coastal plots appeal to high-net-worth Egyptians and Gulf investors, while inland governorates bank on industrial-zone incentives. Nationwide, geographic diversification is reshaping agent networks, encouraging mergers and franchise models to provide consistent service standards across cities.

Competitive Landscape

The Egypt real estate brokerage market is moderately fragmented. Digital platforms such as Nawy and Aqarmap leverage big-data matching and performance marketing to capture online leads, eroding the traditional dominance of relationship-based boutiques. In 2024, Nawy raised USD 75 million to scale its technology stack, underscoring investor belief in virtual brokerage’s scalability. Traditional franchised networks, Coldwell Banker, RE/MAX, Century 21, retain strong brand equity and deeper compliance know-how, positioning them as preferred advisors for international corporates.

Strategic alliances are proliferating: the Egyptian Real Estate Platform’s tie-up with New Avenue Real Estate to onboard 300 agents onto a CoreLogic-powered MLS shows incumbents embracing data-standardization to enhance listing accuracy. Brokerage firms are investing in automated valuation models and CRM analytics to trim customer acquisition costs and lift close rates. Competition now hinges on the ability to offer bundled services, mortgage facilitation, property management, and legal assistance, rather than simple match-making.

White-space opportunities persist in commercial advisory for the New Administrative Capital’s Central Business District, logistics park leasing, and diaspora-oriented cross-border transaction management. Compliance complexity around foreign-ownership laws and title registration favors firms with in-house legal units. Meanwhile, fee compression in the high-volume residential space is pushing smaller agencies toward niche focus or franchise affiliation. Over the outlook period, selective consolidation is expected as tech-enabled platforms acquire smaller specialists to secure geographic reach.

Egypt Real Estate Brokerage Industry Leaders

Coldwell Banker Egypt

RE/MAX Egypt

The Address Investments

Nawy

Aqarmap

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Egypt's Parliament enacted a pivotal amendment to the rental law, introducing a seven-year transition for residential units and a five-year period for commercial properties. This reform is expected to significantly impact the real estate market by allowing rents to increase up to 20 times their current levels, with annual escalations capped at 15%.

- May 2025: Nawy successfully secured USD 52 million in Series A equity funding and an additional USD 23 million in debt financing. The company aims to accelerate its expansion across the MENA region while strengthening its mortgage and fractional-ownership service offerings.

- July 2024: Talaat Moustafa Group announced a USD 21 billion investment in the South Med project on the North Coast. This initiative is set to enhance the luxury residential market by introducing high-end housing options in the region.

- July 2024: Egypt, in partnership with the UAE's ADQ, launched the USD 35 billion Ras El-Hekma project, marking the country's largest single foreign direct investment (FDI) inflow. This strategic development is expected to drive the growth of new coastal submarkets and attract further investments.

Egypt Real Estate Brokerage Market Report Scope

The real estate brokerage market, a subset of the expansive real estate industry, comprises intermediaries, commonly referred to as real estate brokers or agents. These professionals represent buyers, sellers, or both, facilitating negotiations for the sale, lease, or rental of properties spanning residential, commercial, industrial, and agricultural segments.

The Egyptian real estate brokerage market is segmented by type (residential and non-residential), service (sales and rental), and city (Cairo, Alexandria, and the Rest of Egypt). The report offers market sizes and forecasts in value (USD) for all the above segments.

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

What is the current value of the Egypt real estate brokerage market?

The market is valued at USD 586.36 million in 2025.

How fast is the brokerage sector expected to grow?

The market is forecast to post a 9.02% CAGR and reach USD 903.20 million by 2030.

Which segment is expanding the quickest?

Rental brokerage services lead with a projected 9.85% CAGR through 2030.

Why is Giza registering the fastest regional growth?

Spillover from Greater Cairo’s saturation and new infrastructure investments are lifting Giza’s brokerage revenues at a 10.09% CAGR.