Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

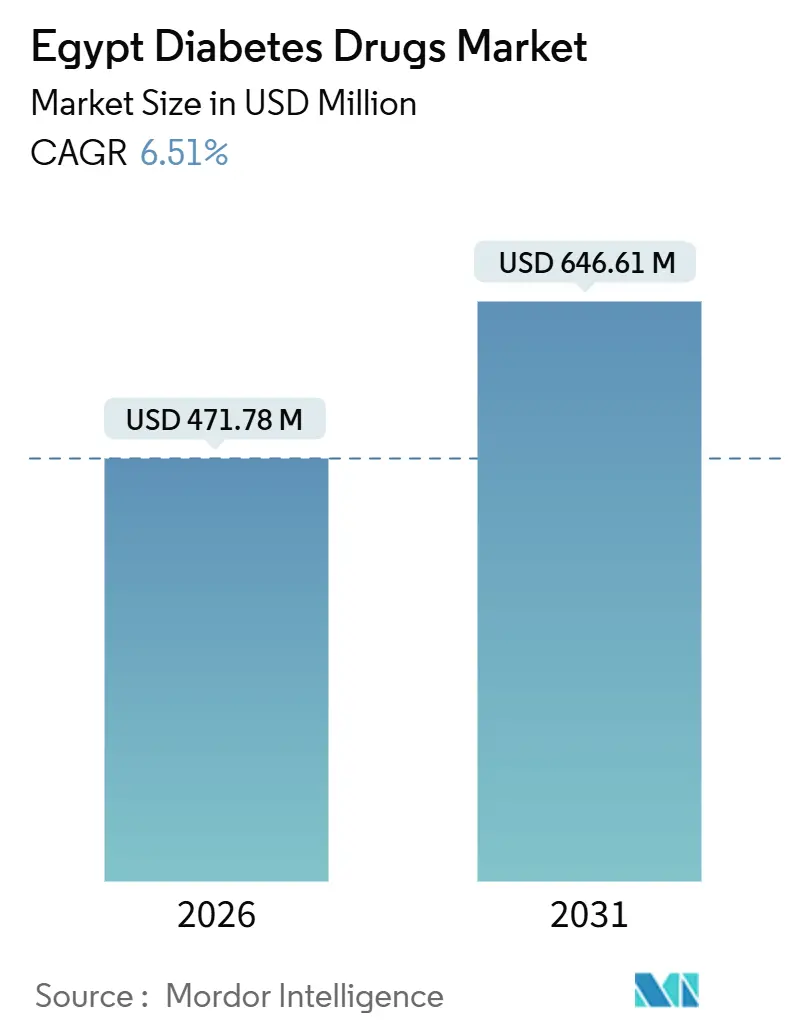

| Market Size (2026) | USD 471.78 Million |

| Market Size (2031) | USD 646.61 Million |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Diabetes Drugs Market Analysis by Mordor Intelligence

The Egypt diabetes drugs market size is valued at USD 471.78 million in 2026 and is projected to reach USD 646.61 million by 2031, registering a 6.51% CAGR through the forecast period. Sustained double-digit prevalence, now at 22.4% of adults, rising local biosimilar insulin production, and phased roll-out of the Universal Health Insurance (UHI) scheme jointly underpin growth across the Egypt diabetes drugs market. Currency devaluation in March 2024 forced a 40%–50% rise in import costs, yet it simultaneously strengthened the domestic manufacturing base, accelerating Eva Pharma’s insulin glargine scale-up and prompting new biosimilar pipelines at Hikma and Pharco. Oral therapies are gaining momentum: cardiovascular outcome data generated at Kasr Al-Ainy and Zagazig University hospitals catalyzed national SGLT-2 uptake, while DPP-4 combinations attract primary-care prescribers looking to avoid injections.[1]Kasr Al-Ainy Hospital & Zagazig University, “Empagliflozin Outcomes in Egyptian Type-2 Patients,” PLOS ONE, journals.plos.org Digital health interventions—from Shefae’s nationwide e-prescribing network to Chefaa’s 1,000-pharmacy marketplace—further enlarge the reachable patient pool, amplifying the addressable opportunity for the Egypt diabetes drugs market.

Key Report Takeaways

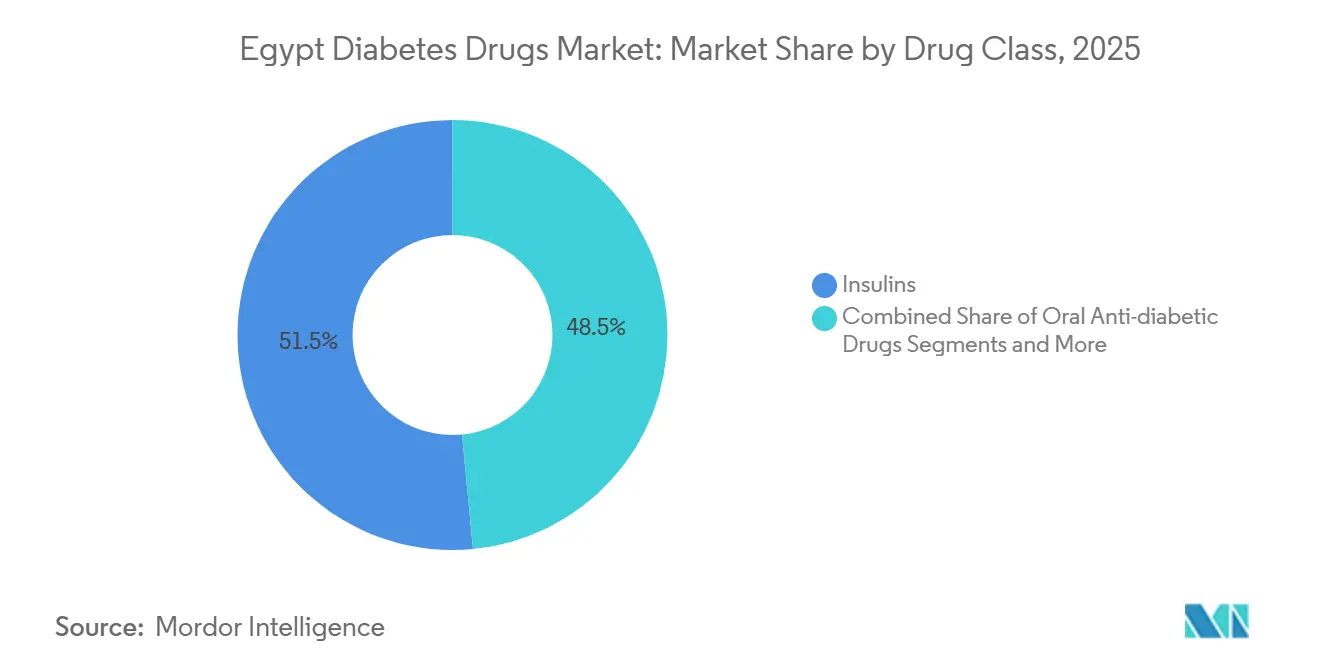

- By drug class, insulins led with 51.52% of Egypt diabetes drugs market share in 2025; oral anti-diabetic drugs are forecast to post the fastest 9.35% CAGR through 2031.

- By route of administration, subcutaneous delivery accounted for 78.24% share of the Egypt diabetes drugs market size in 2025, while oral formulations are expanding at 8.46% CAGR.

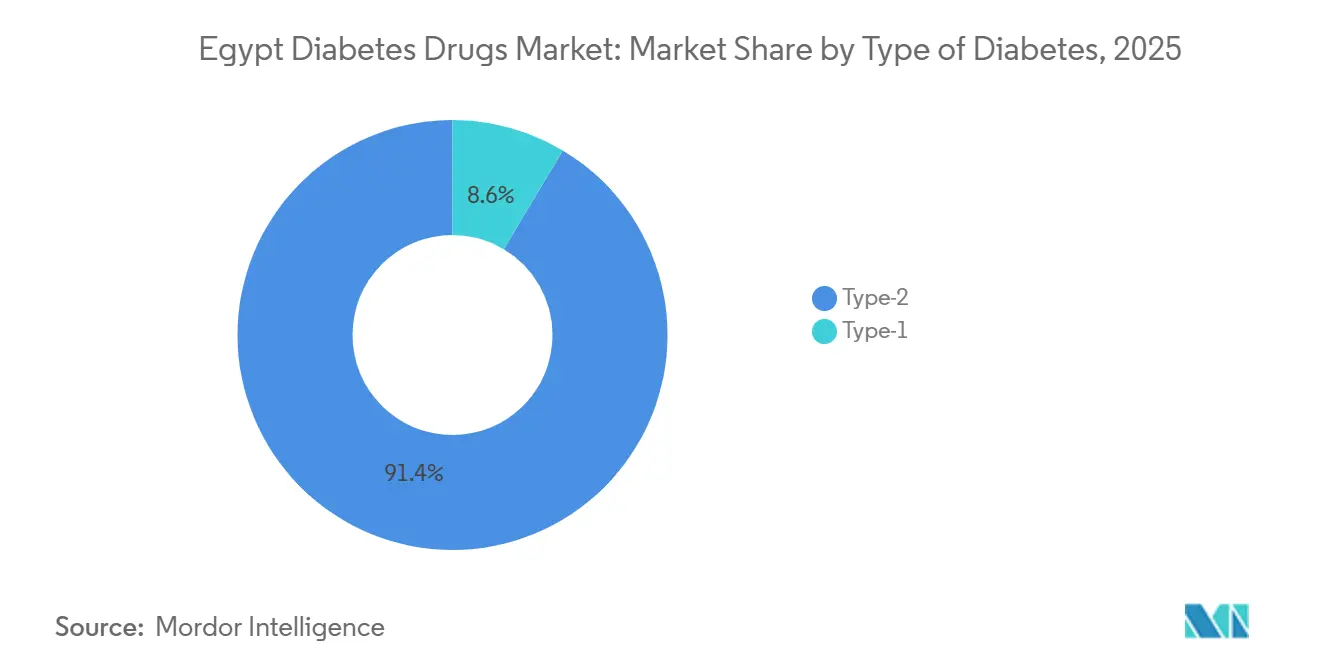

- By type of diabetes, Type-2 cases commanded 91.42% of the Egypt diabetes drugs market in 2025, whereas the pediatric Type-1 segment is projected to grow at 9.01% CAGR.

- By distribution channel, retail pharmacies held 58.36% share in 2025; e-commerce platforms are expected to record the highest 10.78% CAGR through 2031.

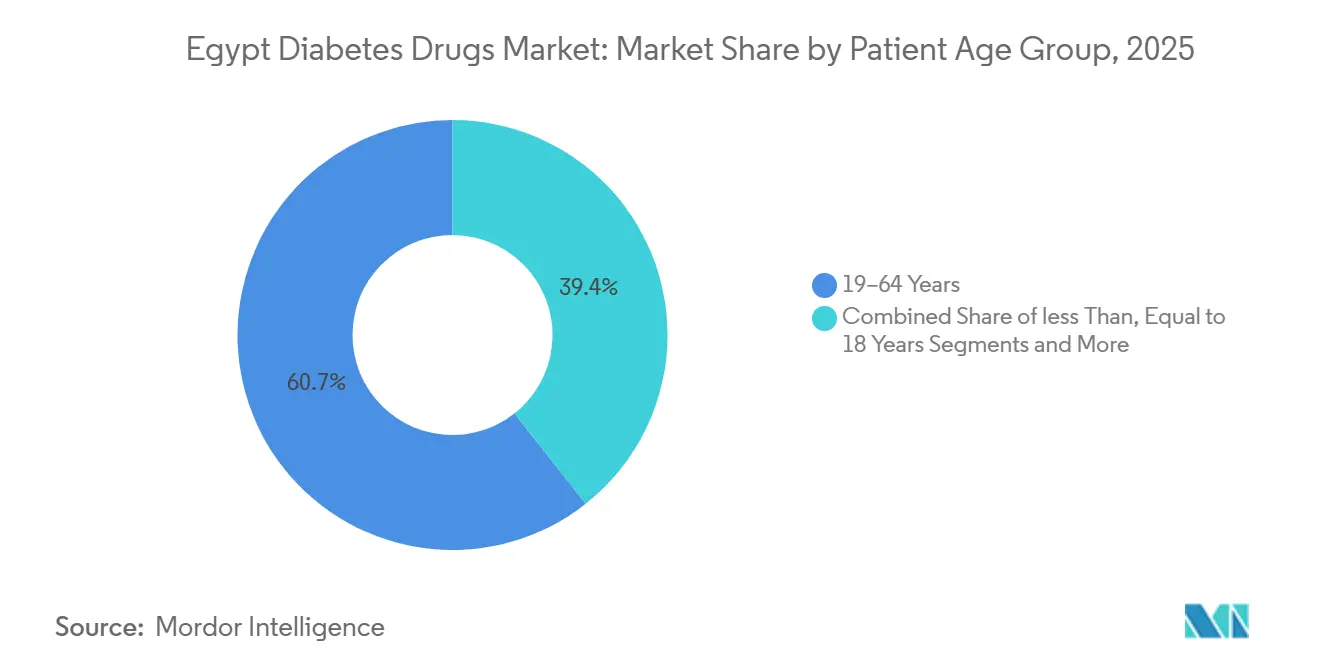

- By patient age group, the 19-64 cohort captured 60.65% of Egypt diabetes drugs market size in 2025; however, ≤18 years remains the quickest-expanding bracket at 9.01% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Diabetes Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of diabetes | +1.2% | Urban governorates (Cairo, Giza, Alexandria) | Long term (≥ 4 years) |

| Advancements in treatment options & UHI | +1.0% | 12 governorates under UHI Phase II | Medium term (2-4 years) |

| Launch of lower-priced biosimilar insulins | +0.9% | Manufacturing hub in 10th of Ramadan City | Short term (≤ 2 years) |

| Rapid SGLT-2 uptake on cardiovascular data | +0.8% | Tertiary hospitals nationwide | Medium term (2-4 years) |

| Expansion of private health-insurance cover | +0.7% | Major urban centers and industrial zones | Medium term (2-4 years) |

| Growth of e-prescription & digital platforms | +0.6% | Early traction in Cairo, Alexandria, Giza; rolling out to Delta governorates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Diabetes

Egypt’s adult prevalence reached 22.4% in 2024, ranking among the world’s top ten and ensuring long-run demand for both insulin and oral agents. The 100 Million Healthy Lives campaign screened more than 50 million citizens, revealing a large undiagnosed pool primed for treatment initiation.[2]Ministry of Health and Population Egypt, “Universal Health Insurance Program Update,” Ministry of Health, mohp.gov.egRapid urbanization elevates calorie-dense diets and sedentary habits, pushing prevalence in Cairo, Giza, and Alexandria 3–5 percentage points above the national mean. Middle-aged adults represent the fastest-growing cohort; CAPMAS projects the 45-64 bracket to rise 2.1% annually to 2030. Pediatric Type-1 incidence is also climbing, moving from 8.9 to 12.3 per 100,000 children between 2015 and 2023, creating a forward pipeline of insulin-dependent patients.

Advancements in Treatment Options & Active Government Initiatives

UHI allocated LE 115 billion to subsidize essential medicines for 12.8 million citizens across 12 governorates by 2025, raising adherence 34% among insured patients versus out-of-pocket payers. May 2024 pharmacy guidelines from the Egyptian Drug Authority require pharmacist-led medication therapy management, cutting dosing errors 18% in pilot sites.[3]Egyptian Drug Authority, “Regulatory Approvals and National Formulary 2024,” Egyptian Drug Authority, eda.mohp.gov.eg The National Digital Health Strategy targets full electronic health-record interoperability across 500 facilities by 2027, with Vodafone Egypt already linking 314 hospitals and delivering a 22% HbA1c reduction in early pilots. Together these measures systematize care pathways and sustain volume across the Egypt diabetes drugs market.

Launch of Lower-Priced Biosimilar Insulins

Eva Pharma’s December 2024 approval for insulin glargine offers a supply capacity of 90 million vials and 50 million cartridges annually, covering up to 1 million patients at a 30% discount to Lantus. Local supply shields payers from the 50% pound devaluation that inflated imported insulin prices 40%–50% in 2024. Hikma and Pharco are following with insulin aspart, lispro, and human insulin biosimilars, deepening competition and affordability. Rapid uptake allowed biosimilars to secure 11% of basal insulin volume within three months of launch, illustrating material impact on the Egypt diabetes drugs market.

Rapid Uptake of SGLT-2 Inhibitors Driven by Cardiovascular Evidence

A multicenter Egyptian real-world study showed empagliflozin lowered heart-failure hospitalization 28% and cardiovascular mortality 19% over 24 months, validating global trials in a local high-HbA1c population. Egyptian Society of Cardiology guidelines now position SGLT-2 therapy immediately after metformin for patients with ASCVD or CKD, a group representing 35% of Type-2 cases. Generic brands such as Diacurimap and Glimpacare entered at 40% below originator pricing, already holding 12% share of the SGLT-2 segment by early 2025. These catalysts raise oral-therapy intensity and reinforce the growth outlook for the Egypt diabetes drugs market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs & limited reimbursement | -0.9% | Rural Upper Egypt (Assiut, Sohag, Qena) | Long term (≥ 4 years) |

| Gaps in healthcare infrastructure | -0.7% | Rural & frontier governorates (Matrouh, New Valley, Red Sea) | Long term (≥ 4 years) |

| Currency-driven supply-chain disruptions | -0.6% | Nationwide, especially private pharmacies reliant on imports | Short term (≤ 2 years) |

| Low long-term adherence | -0.5% | Informal-sector populations across Egypt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs & Limited Reimbursement

Out-of-pocket spending represents 62% of national health expenditures, forcing many patients to choose cheaper human insulin or generic metformin despite the clinical superiority of analog regimens. The 50% pound devaluation pushed Ozempic’s retail price to 4,000 EGP (USD 81), pricing it out of reach for households earning below LE 5,000 per month, which encompass 73% of Egyptians. UHI covers human insulin and sulfonylureas but not GLP-1 or SGLT-2 agents, limiting reimbursement scope and curbing premium-product adoption across the Egypt diabetes drugs market.

Gaps in Healthcare Infrastructure Outside Major Cities

Physician density averages 8.5 per 10,000 nationally but falls to 3.2 in Upper Egypt, hampering early diagnosis and continuous follow-up. Only 5% of rural primary-care units possess full diabetes-management equipment, compelling patients to travel an average 47 km for adequate services. Cold-chain lapses degrade 23% of insulin stocks in Fayoum and Beni Suef pharmacies, compromising therapeutic potency

Segment Analysis

By Drug Class: Biosimilars Reshape Insulin Economics

Insulins accounted for 51.52% of Egypt diabetes drugs market share in 2025, yet oral anti-diabetic drugs are on track to expand at 9.35% CAGR between 2026 and 2031, propelled by the domestic launch of lower-cost SGLT-2 and DPP-4 preparations. The Eva Pharma-Eli Lilly biosimilar glargine carved out 11% of basal insulin volume within three months, validating the affordability thesis and lifting overall Egypt diabetes drugs market size for insulin therapies. Human insulin continues to dominate rural governorates where analog cold-chain reliability and higher prices remain hurdles; a cold-chain audit showed 23% degradation incidence in Fayoum and Beni Suef.

SGLT-2 inhibitors are the fastest-growing oral subclass, underwritten by Egyptian cardiovascular outcome data that demonstrated a 28% reduction in heart-failure hospitalizations. DPP-4 inhibitors captured 16% of the oral segment by 2025, led by vildagliptin and sitagliptin, which attract patients seeking hypoglycemia-free regimens. Combination drugs simplify dosing and lifted adherence ≥80% rates from 47% to 61% in a 2024 cohort study, a trend likely to keep the Egypt diabetes drugs industry in robust expansion mode.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Route of Administration: Oral Formulations Gain Ground

Subcutaneous delivery dominated 78.24% of Egypt diabetes drugs market size in 2025 as insulin remains indispensable for Type-1 and advanced Type-2 patients. Nevertheless, oral agents are projected to close the gap with an 8.46% CAGR through 2031, riding on guideline-supported earlier use of dual oral therapy before injectable escalation. Needle aversion persists; 42% of Type-2 patients delayed insulin initiation by over two years, buttressing oral-drug volume growth.

Connected insulin pens remain under 5% penetration, citing device cost and limited reimbursement, though university pilots show 19% time-in-range gains among adolescents. Intravenous administration is confined to hospital settings for acute crises, a segment too small to materially affect Egypt diabetes drugs market share yet vital for tertiary-care readiness.

By Type of Diabetes: Type-2 Drives Volume, Type-1 Demands Innovation

Type-2 diabetes held 91.42% of Egypt diabetes drugs market share in 2025 and is forecast to compound at 8.27% CAGR, supported by urban lifestyle changes and the aging mid-life demographic. The Egypt diabetes drugs market size for Type-2 therapies further benefits from guideline-endorsed SGLT-2 and DPP-4 positioning that delays insulin initiation and lengthens oral-therapy cycles.

Type-1 volumes are smaller but rising at 9.01% CAGR, led by pediatric incidence gains and expanded diagnosis initiatives from the Egyptian Pediatric Endocrinology Society. Poor glycemic control remains widespread; 83.2% of children registered HbA1c above 9% in a 2024 study, underscoring unmet needs in glucose monitoring and caregiver education

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Retail pharmacies amassed 58.36% of Egypt's diabetes drug market size in 2025, propelled by Seif Pharmacies’ 220-outlet network, yet regulated price caps squeeze profitability amid currency spikes. Online channels, processing half-a-million prescriptions monthly, are projected to expand at 10.78% CAGR, surpassing all other outlets by 2031. Hospital pharmacies continue to play a key role in insulin initiation under the UHI program, dispensing 38% of reimbursed diabetes medications in 2024.

Counterfeit risk spurred the Egyptian Drug Authority’s blockchain pilot, slashing fraudulent dispensing by one-third and reinforcing consumer confidence in regulated e-commerce supply chains. Cold-chain discipline remains the limiting factor for rural e-pharmacy insulin deliveries.

By Patient Age Group: Pediatric Segment Demands Targeted Solutions

Adults aged 19-64 captured 60.65% of Egypt diabetes drugs market in 2025, reflecting the dominance of Type-2 prevalence in working-age Egyptians. The pediatric (≤18 years) segment, however, will grow fastest at 9.01% CAGR owing to rising Type-1 incidence and better detection. Continuous glucose monitoring penetration reached 8% of Type 1 patients by early 2025, yet affordability constraints persist, with sensors priced at LE 1,200 every 14 days (USD).

Elderly (≥65) patients exhibit heavy insulin reliance; 68% require basal-bolus regimens because of beta-cell exhaustion and high comorbidity load, pointing to sustained insulin volume contributions within the Egypt diabetes drugs industry

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Greater Cairo, Alexandria, and Giza generated 64% of Egypt diabetes drugs market value in 2025, driven by superior physician density, robust pharmacy infrastructure, and 71% of private insurance policies. UHI Phase II improved access in Delta governorates—Dakahlia, Sharqia, Gharbia—where insulin dispensing climbed 18% year-over-year in 2024. In Upper Egypt, shortages of endocrinologists and fully equipped clinics restrict per-capita consumption; 60.5% of Assiut patients cited cost-related non-adherence versus 38% in Cairo.

Frontier governorates such as Matrouh and New Valley average fewer than 2 pharmacies per 100,000 residents, forcing reliance on hospital supply or periodic mobile units. Devaluation-induced price hikes were felt nationwide, yet urban patients could trade down to biosimilar insulin glargine at a 30% discount while rural areas remained dependent on higher-priced imports.

Digital disruption narrows gaps: Chefaa now offers 48-hour delivery in secondary cities, while Vodafone’s telemedicine platform improved HbA1c by 22% in Dakahlia and Sharqia pilots. Nonetheless, pediatric ketoacidosis episodes stay disproportionately high in Upper Egypt—42% of children experienced at least one episode annually versus 18% in Lower Egypt—highlighting persisting regional inequalities.

Competitive Landscape

The Egypt diabetes drugs market remains moderately concentrated: Novo Nordisk, Sanofi, and Eli Lilly/Eva Pharma together hold roughly major share of therapeutic value. Eva Pharma’s 2024 glargine launch captured 11% of basal volumes within a quarter by underpricing imports 30% and guaranteeing steady supply from its 10th of Ramadan site. Hikma plans late-2026 introductions of aspart and lispro biosimilars, while Pharco’s generic insulin lispro secured an 8% share six months post-launch.

Strategic focus is shifting to digital safety nets: Eva Pharma’s April 2025 hotline authenticates every tirzepatide script after counterfeit GLP-1 incidents, signaling that supply-chain integrity is now a competitive differentiator. Chefaa processes 500,000 monthly diabetes prescriptions, monetizing data analytics and last-mile logistics to outflank traditional wholesalers in peri-urban zones.

Emerging challengers include Sun Pharma, which established a manufacturing subsidiary in 10th of Ramadan City to supply sitagliptin and vildagliptin generics, and Julphar, scaling its Delta-region distribution footprint. Anticipated white spaces encompass connected insulin pens (sub-5% penetration), GLP-1 biosimilars (Ozempic still priced at 4,000 EGP), and oral semaglutide, not yet registered but expected to disrupt injection-averse segments of the Egypt diabetes drugs market.

Egypt Diabetes Drugs Industry Leaders

AstraZeneca

Novo Nordisk A/S

Eli Lilly and Company

Sanofi

Merck & Co.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: EVA Group introduced Mounjaro (tirzepatide) KwikPen in Egypt under a distribution partnership with Eli Lilly to broaden obesity and Type-2 therapy access.

- April 2025: Eva Pharma launched a prescription-authentication hotline for tirzepatide after reports of counterfeit GLP-1 products.

- March 2025: Tonghua Dongbao and Kexing Biopharm completed Egyptian GMP inspection for locally supplied liraglutide injectables.

- December 2024: Egyptian Drug Authority approved Eva Pharma’s insulin glargine, targeting sustainable supply for 1 million patients annually.

Egypt Diabetes Drugs Market Report Scope

Antidiabetic medications are drugs used to manage high blood sugar levels in individuals with diabetes by regulating insulin production, utilization, sugar absorption, or excretion, aiming to prevent complications like heart or kidney diseases.

The Egyptian diabetes drugs market is segmented by drug class into insulin, oral anti-diabetic drugs, non-insulin injectable drugs, and combination drugs. By Route of Administration, the market is segmented into Subcutaneous, Oral, and Intravenous. By Type of Diabetes, the market is segmented into Type-1 and Type-2. By Distribution Channel, the market is segmented into Hospital Pharmacies, Retail Pharmacies, and E-Commerce/Online Pharmacies. By Patient Age Group, market is segmented into Less Than, Equal to 18 Years, 19–64 Years, Equal to, More than 65 Years. The report offers the value (USD) for the above segments.

By Drug Class

| Insulins | Basal/Long-acting |

| Bolus/Fast-acting | |

| Traditional Human Insulins | |

| Biosimilar Insulins | |

| Oral Anti-diabetic Drugs | Biguanides |

| Alpha-glucosidase Inhibitors | |

| Dopamine-D2 Receptor Agonists | |

| SGLT-2 Inhibitors | |

| DPP-4 Inhibitors | |

| Sulfonylureas | |

| Meglitinides | |

| Non-insulin Injectables | GLP-1 Receptor Agonists |

| Amylin Analogues | |

| Combination Drugs | Insulin Combinations |

| Oral Combinations |

By Route of Administration

| Subcutaneous |

| Oral |

| Intravenous |

By Type of Diabetes

| Type-1 |

| Type-2 |

By Distribution Channel

| Hospital Pharmacies |

| Retail Pharmacies |

| E-Commerce/Online Pharmacies |

By Patient Age Group

| Less Than, Equal to 18 Years |

| 19-64 Years |

| Equal to, More than 65 Years |

| By Drug Class | Insulins | Basal/Long-acting |

| Bolus/Fast-acting | ||

| Traditional Human Insulins | ||

| Biosimilar Insulins | ||

| Oral Anti-diabetic Drugs | Biguanides | |

| Alpha-glucosidase Inhibitors | ||

| Dopamine-D2 Receptor Agonists | ||

| SGLT-2 Inhibitors | ||

| DPP-4 Inhibitors | ||

| Sulfonylureas | ||

| Meglitinides | ||

| Non-insulin Injectables | GLP-1 Receptor Agonists | |

| Amylin Analogues | ||

| Combination Drugs | Insulin Combinations | |

| Oral Combinations | ||

| By Route of Administration | Subcutaneous | |

| Oral | ||

| Intravenous | ||

| By Type of Diabetes | Type-1 | |

| Type-2 | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| E-Commerce/Online Pharmacies | ||

| By Patient Age Group | Less Than, Equal to 18 Years | |

| 19-64 Years | ||

| Equal to, More than 65 Years | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Egypt diabetes drugs market in 2026?

The Egypt diabetes drugs market size stands at USD 471.78 million in 2026 and is forecast to grow to USD 646.61 million by 2031.

What is driving the rapid growth of SGLT-2 inhibitors in Egypt?

Local cardiovascular outcome studies showing a 28% cut in heart-failure hospitalizations and the entry of 40%-cheaper generics have accelerated national adoption of SGLT-2 therapy.

Why are biosimilar insulins important for Egyptian patients?

Biosimilars produced by Eva Pharma and others are priced about 30% below imported analogs, mitigating currency-related price spikes and widening access for cost-sensitive users.

Which distribution channel is expanding fastest?

E-commerce and online pharmacies are projected to post a 10.78% CAGR through 2031, supported by Chefaa’s 1,000-pharmacy network and nationwide home delivery.

What challenges limit long-term adherence to diabetes medicines?

High out-of-pocket costs, cultural reliance on herbal remedies, and income volatility among informal-sector workers keep adherence rates below 50% nationally.

Which patient group is growing quickest?

The pediatric Type-1 cohort (≤18 years) is expected to rise at 9.01% CAGR due to increasing incidence and improved diagnostic coverage.