| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 55.04 Billion |

| Market Size (2030) | USD 82.34 Billion |

| CAGR (2025 - 2030) | 8.39 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Egypt Construction Industry Analysis

The Egypt Construction Market size is estimated at USD 55.04 billion in 2025, and is expected to reach USD 82.34 billion by 2030, at a CAGR of 8.39% during the forecast period (2025-2030).

Egypt has emerged as a significant player in the Middle East and North Africa (MENA) construction sector, positioning itself as the third-largest project market in the region after Saudi Arabia and the United Arab Emirates. The construction industry in Egypt has witnessed substantial government support through infrastructure development initiatives, with the administration allocating an unprecedented budget of USD 80 billion in 2021-2022, of which 75% was designated for public investment. This commitment to infrastructure development has resulted in the completion of projects valued at approximately USD 106.25 billion within a span of less than two years, demonstrating the country's accelerated pace of construction and development activity.

The transportation sector has become a cornerstone of Egypt's construction landscape, with significant investments being channeled into modernizing the country's mobility infrastructure. The government has allocated USD 15.65 billion for the transport sector, encompassing roads, bridges, and river ports development. A landmark project in this sector is the nationwide high-speed train network, for which Siemens secured an USD 8.7 billion contract as the prime contractor. The project exemplifies Egypt's commitment to developing sophisticated transportation infrastructure that will connect various regions of the country.

The residential construction sector is experiencing a transformation driven by demographic factors and changing consumer preferences. With a population growth rate of 2.25%, Egypt has witnessed increased demand for housing across various segments. The market is particularly seeing growth in Grade A residential developments, with projections indicating the total number of such units to reach 169,200 by 2025 in West and New Cairo. This growth is accompanied by a shift towards modern lifestyle needs, reflected in enhanced product placements, innovative designs, and integration of services within mixed-use developments.

The energy sector is witnessing significant developments with several large-scale projects underway. The country has allocated over 7,000 square kilometers for renewable energy production projects, demonstrating its commitment to sustainable development. Recent initiatives include the planned construction of new nuclear projects adjacent to the Dabaa nuclear plant and the development of a wind power farm in the Gulf of Suez region with an investment of USD 600 million. Additionally, Egypt is venturing into green hydrogen production, with plans to invest up to USD 4 billion in a project utilizing water electrolysis technology, showcasing the country's dedication to diversifying its energy infrastructure portfolio.

Egypt Construction Market Trends

Government Infrastructure Initiatives and Investment Support

The Egyptian government's aggressive infrastructure development agenda has emerged as a primary driver for the construction sector, with approximately USD 93 billion worth of construction projects in Egypt under active development and an additional USD 425 billion worth of projects in various pre-execution stages as of 2022. This massive pipeline is supported by the government's commitment to implementing 45 major national and strategic infrastructure projects in the financial year 2022/2023, including the construction of 10 transverse axes on the Nile, establishment of 18 overpasses, and completion of 1,000 km of electrification of railway signals. The scale of these initiatives demonstrates the government's dedication to modernizing the infrastructure of Egypt.

The Urban Development Fund's (UDF) nationwide housing project, launched in December 2022 with a budget of EGP 600 billion, further exemplifies the government's role in driving construction activity. This comprehensive project encompasses the development of 230 urban areas across governorate capitals and important cities, covering more than 14,422 acres. The strategic implementation approach, with 35 sites being developed urgently, 60 sites on a priority basis, and 135 sites on second priority, ensures sustained construction activity over the next five years, providing steady growth opportunities for the building and construction sector.

Understand The Key Trends Shaping This Market

Download PDF

Foreign Investment and Economic Growth

The construction sector's robust growth is significantly bolstered by increasing foreign investment interest, particularly from Middle East sovereign wealth funds, which have expressed intentions to invest up to USD 120 billion in Egypt in the upcoming years. This substantial foreign investment commitment, coupled with the construction sector's significant 14% contribution to Egypt's GDP, underscores the industry's crucial role in the country's economic development. The involvement of foreign governments through export credit financing agreements has further strengthened the sector's financial foundation, enabling the execution of large-scale construction projects in Egypt.

The real estate segment has emerged as a particular beneficiary of this investment momentum, with total real estate investments in Cairo reaching USD 20 billion in 2022, of which USD 16 billion was dedicated to the residential sector. The government's initiatives to boost real estate exports, including the establishment of a real estate fund with administrative and commercial assets and the trading of properties on the Egyptian Stock Exchange (EGX), have created additional channels for investment in the construction sector. This diversification of investment opportunities, combined with the average 10% increase in residential property prices during 2022, has created a favorable environment for sustained construction activity.

Energy and Transportation Infrastructure Development

The ambitious development of Egypt's energy and transportation infrastructure has become a significant driver for the construction market, exemplified by major projects such as the USD 4.8 billion Cairo Metro Line 3 project spanning 17.7 km with 15 stations, and the USD 4.5 billion East Cairo-NAC monorail extending 54 km with 22 stations. These transportation initiatives are complemented by significant energy infrastructure projects, including nuclear power plant developments and renewable energy facilities, creating a diverse portfolio of construction opportunities across multiple sectors. The comprehensive nature of these projects ensures sustained demand for construction services across various specializations.

The expansion of transportation networks is further emphasized by projects like the LE6.3 billion first phase of Metro Line 4, which includes 19 km of rail for 16 stations, and the USD 4.5 billion King Salman Bridge. These developments are part of a larger strategy to modernize Egypt's transportation infrastructure, creating interconnected networks that support economic growth. The simultaneous development of energy infrastructure, including nuclear power plants and renewable energy facilities, demonstrates the government's commitment to creating a comprehensive modern infrastructure network, driving continued growth in the construction sector.

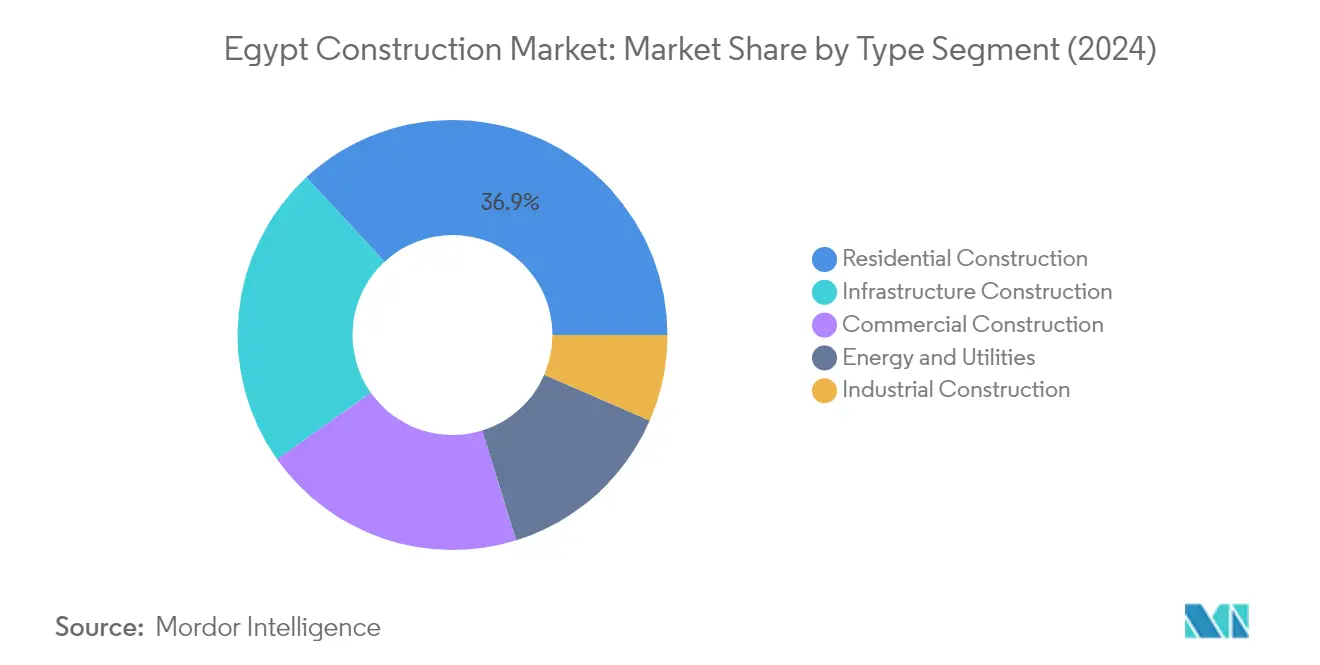

Segment Analysis: By Type

Residential Construction Segment in Egypt Construction Market

The residential construction segment continues to dominate the Egypt construction market, holding approximately 37% market share in 2024, with a market value of 18.89 billion USD. This segment's prominence is driven by Egypt's favorable demographics with a young population base and the government's ongoing initiatives to increase homeownership. The emergence of organized and Grade A residential communities has gained significant popularity, particularly in new micro-markets. The residential offering is gradually evolving to adapt to modern lifestyle needs, reflected in enhanced product placements regarding finishing materials, designs, and unit sizes. The focus has shifted toward providing more services within mixed-use developments, enhancing the appeal to potential residents. The current trend shows strong demand concentration across the mid-to-high-end segment, making them a preferred investment choice for the top income category of the population.

Industrial Construction Segment in Egypt Construction Market

The industrial construction segment is emerging as the fastest-growing sector in Egypt's construction industry segments, with a projected growth rate of approximately 12% during 2024-2029. This remarkable growth is primarily driven by Egypt's strategic efforts to expand its industrial capacity across various sectors. The country has witnessed significant developments in processing, storage, and transportation of hydrocarbons, along with the establishment of several industrial areas for light and medium industries. The segment is seeing substantial investments in new manufacturing facilities, petrochemical complexes, and industrial parks. The government's focus on developing specialized industrial zones and the increasing foreign direct investment in manufacturing sectors are further accelerating this growth. Additionally, the implementation of advanced technologies and sustainable building practices in industrial projects is contributing to the segment's rapid expansion.

Remaining Segments in Egypt Construction Market

The other segments in Egypt's construction industry segments, including infrastructure (transportation), commercial construction, and energy & utilities construction, each play vital roles in the country's development landscape. The infrastructure segment is particularly significant with major investments in transportation projects including railways, metros, and ports. The commercial construction sector continues to evolve with the development of new business districts and retail spaces, particularly in emerging urban areas. The energy and utilities construction segment is gaining prominence through renewable energy projects and power infrastructure development, supporting Egypt's transition toward sustainable energy sources. These segments collectively contribute to the comprehensive development of Egypt's built environment, with each addressing specific needs in the country's urbanization and modernization journey.

Egypt Construction Industry Overview

Top Companies in Egypt Construction Market

The construction companies in Egypt market features prominent players like Hassan Allam Construction, DORRA Group, Arab Contractors, Orascom Construction, and SIAC Industrial Construction & Engineering leading the industry. These leading construction companies in Egypt are increasingly focusing on technological advancement through Building Information Modeling (BIM) adoption and modular construction techniques to enhance operational efficiency. Strategic partnerships with international firms have become a key trend to access advanced construction methodologies and expand project capabilities. Companies are diversifying their portfolios beyond traditional construction into specialized sectors like renewable energy infrastructure and smart building solutions. The market leaders are also emphasizing sustainable construction practices and green building certifications to align with global environmental standards, while simultaneously investing in workforce development and equipment modernization to maintain competitive advantages.

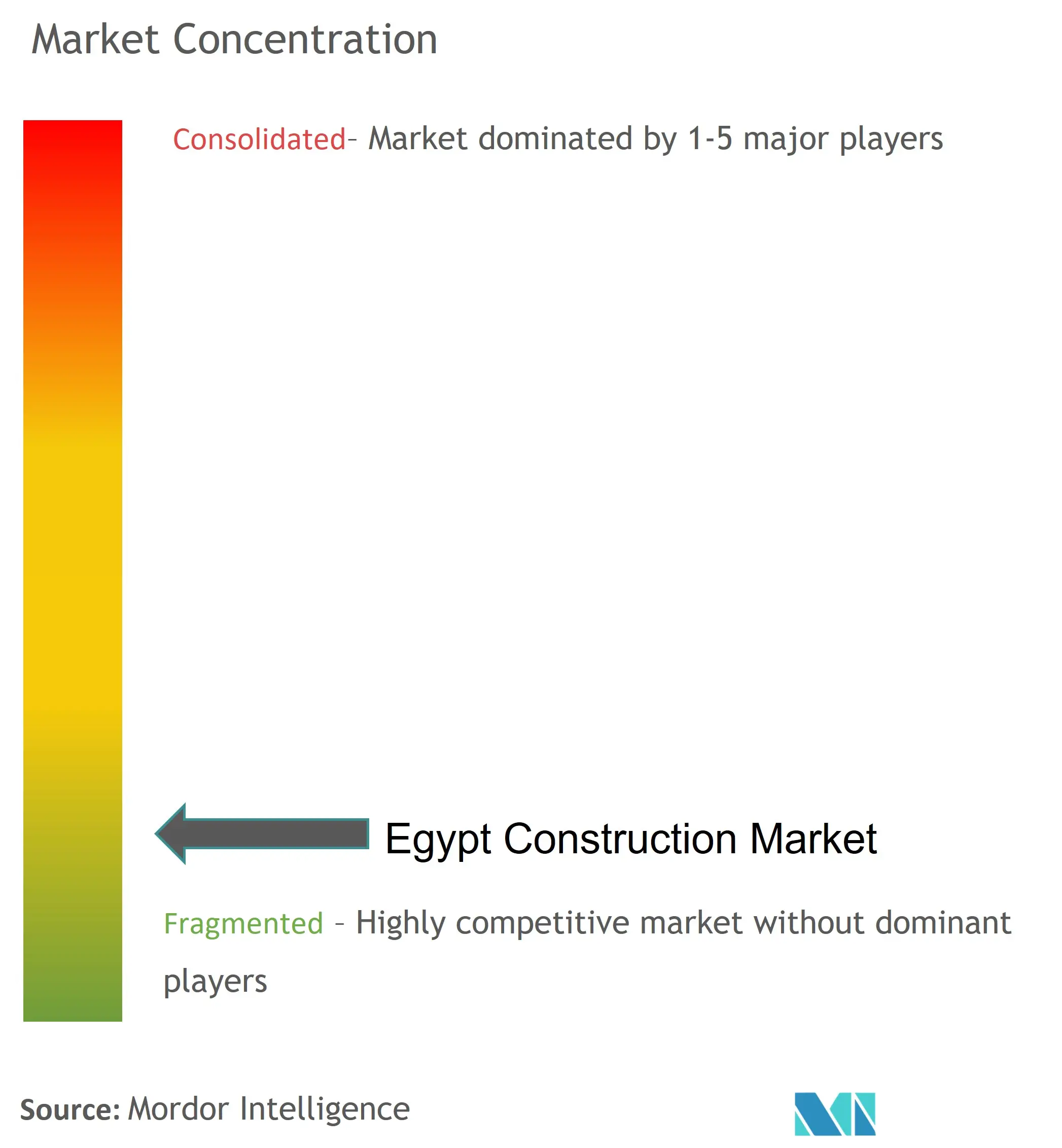

Dynamic Market with Strong Local Leadership

The Egyptian construction market exhibits a balanced mix of well-established local conglomerates and international construction firms, with domestic players maintaining a strong market position due to their deep understanding of local regulations and business networks. The market structure shows moderate consolidation, with major local players holding significant market share while still allowing space for specialized contractors in niche segments. The industry has witnessed increased joint venture formations between local and international firms, particularly for large-scale infrastructure and development projects, fostering knowledge transfer and technical expertise sharing.

The market demonstrates a trend toward vertical integration, with major construction companies in Egypt expanding into related sectors such as building materials manufacturing and real estate development to strengthen their market position. Foreign companies are increasingly entering the market through strategic partnerships with local firms, bringing advanced construction technologies and international best practices. The competitive dynamics are further shaped by government initiatives promoting private sector participation in infrastructure development and housing projects, creating opportunities for both established players and new entrants.

Innovation and Adaptability Drive Future Success

Success in the Egyptian construction market increasingly depends on companies' ability to embrace technological innovation while maintaining cost competitiveness. Market leaders are strengthening their positions through investments in digital construction technologies, sustainable building practices, and workforce development programs. For emerging players, specialization in high-growth segments like affordable housing and renewable energy infrastructure presents opportunities to gain market share. The industry's future competitiveness will be significantly influenced by companies' ability to manage project risks, maintain strong supplier relationships, and adapt to evolving regulatory requirements.

Companies looking to expand their market presence must focus on developing strong local supply chains and establishing efficient project management systems. The increasing emphasis on sustainable construction and energy-efficient buildings creates opportunities for firms with specialized expertise in these areas. Success factors also include the ability to secure project financing, maintain strong relationships with government entities, and develop innovative solutions for urban development challenges. Market participants must carefully balance cost optimization with quality delivery while adhering to evolving environmental and safety regulations to maintain competitive advantages in the market.

Egypt Construction Market Leaders

-

H.A.Construction (H.A.C)

-

DORRA Group

-

AL-AHLY Development

-

Palm Hills Developments

-

The Arab Contractors

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Egypt Construction Market News

- October 2022: ERG Developments in the New Administrative Capital (NAC) has begun construction on the residential complex Ri8 for an estimated 3.5 billion Egyptian pounds. The 25-acre Ri8 Compound is part of Zawya Projects, which was to be built in three phases and includes 34 residential structures with 1,063 units.

- November 2022: Orascom Construction PLC announced that it joined forces exclusively with COBOD, a Denmark-based company, to introduce cutting-edge 3D Printing Construction ("3DPC") technology to Egypt for the first time. Three business areas were to get most of the partnership's attention: project completion, equipment sales, and operation and maintenance. The partnership was expected to also look into ways to use 3DPC technology to print whole buildings on the Egyptian market.

Egypt Construction Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

- 2.1 Analysis Method

- 2.2 Research Phases

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

-

4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Increasing demand for green construction to reduce carbon footprint

- 4.2.1.2 Introduction of technology for manufactruing the of building construction material

- 4.2.2 Market Restraints

- 4.2.2.1 High cost of purchasing the equipment for development and manufacturing of various construction material

- 4.2.3 Market Opportunities

- 4.2.3.1 Rapid indutrialization, and urbanization leading to establisment for new construction projects

- 4.3 Value Chain / Supply Chain Analysis

-

4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Technological Innovations in the Construction Sector

- 4.6 Spotlight on the Construction Costs

- 4.7 Impact of Government Regulations and Initiatives on the Industry

- 4.8 Key Production, Consumption, Export and Import Statistics for Construction Materials

- 4.9 Spotlight on Prefabricated Buildings Market in Egypt

- 4.10 Insights on Key Distributors/Traders

- 4.11 Impact of COVID-19 on the Market

5. MARKET SEGMENTATION

-

5.1 By Sector

- 5.1.1 Residential

- 5.1.2 Commercial

- 5.1.3 Industrial

- 5.1.4 Transportation Infrastructure

- 5.1.5 Energy and Utilities

6. COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

-

6.2 Company Profiles

- 6.2.1 H.A.Construction (H.A.C)

- 6.2.2 AL-AHLY Development

- 6.2.3 Palm Hills Developments

- 6.2.4 DORRA Group

- 6.2.5 Construction & Reconstruction Engineering Company

- 6.2.6 Energya- PTS

- 6.2.7 The Arab Contractors

- 6.2.8 Osman Group

- 6.2.9 GAMA Constructions

- 6.2.10 RAYA Holdings*

- *List Not Exhaustive

7. FUTURE OF THE MARKET

8. APPENDIX

- 8.1 Marcroeconomic Indicators (GDP breakdown by sector, Contribution of construction to economy, etc.)

- 8.2 Demographic Indicators

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Egypt Construction Industry Segmentation

Construction includes any on-site physical work that involves erecting a structure, cladding, external finishing, formwork, fixtures, installing services, unloading equipment, supplies, or the like.

A complete background analysis of the Egypt Construction Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, geographical trends, and COVID-19 impact, is included in the report.

The Egypt construction market is segmented by sector (residential, commercial, industrial, transportation infrastructure, and energy and utilities).

The report offers market size and forecasts for the Egyptian construction market in value (USD) for all the above segments.

| By Sector | Residential |

| Commercial | |

| Industrial | |

| Transportation Infrastructure | |

| Energy and Utilities |

Need A Different Region or Segment?

Customize Now

Egypt Construction Market Research Faqs

How big is the Egypt Construction Market?

The Egypt Construction Market size is expected to reach USD 55.04 billion in 2025 and grow at a CAGR of 8.39% to reach USD 82.34 billion by 2030.

What is the current Egypt Construction Market size?

In 2025, the Egypt Construction Market size is expected to reach USD 55.04 billion.

Who are the key players in Egypt Construction Market?

H.A.Construction (H.A.C), DORRA Group, AL-AHLY Development, Palm Hills Developments and The Arab Contractors are the major companies operating in the Egypt Construction Market.

What years does this Egypt Construction Market cover, and what was the market size in 2024?

In 2024, the Egypt Construction Market size was estimated at USD 50.42 billion. The report covers the Egypt Construction Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Egypt Construction Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Egypt Construction Industry Report

Mordor Intelligence provides a comprehensive analysis of the construction industry in Egypt. We leverage our extensive experience in market research and consulting services. Our detailed examination of the building and construction sector offers stakeholders crucial insights into the rapidly evolving construction market. The report, available as an easy-to-read PDF for download, covers an extensive analysis of construction companies in Egypt. It includes both established players and emerging infrastructure companies in Egypt.

The report thoroughly examines construction industry segments, offering detailed insights into the construction market size and growth trajectories. Our analysis encompasses major construction projects in Egypt, emerging trends, and future opportunities within the building industry. Stakeholders, including contracting companies in Egypt and industry professionals, benefit from our comprehensive coverage of regulatory frameworks and competitive landscapes. We also provide detailed profiles of the top 10 construction companies in Egypt. The report offers valuable intelligence on the infrastructure of Egypt, supporting strategic decision-making and market entry strategies for both domestic and international players in the construction sector.