Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

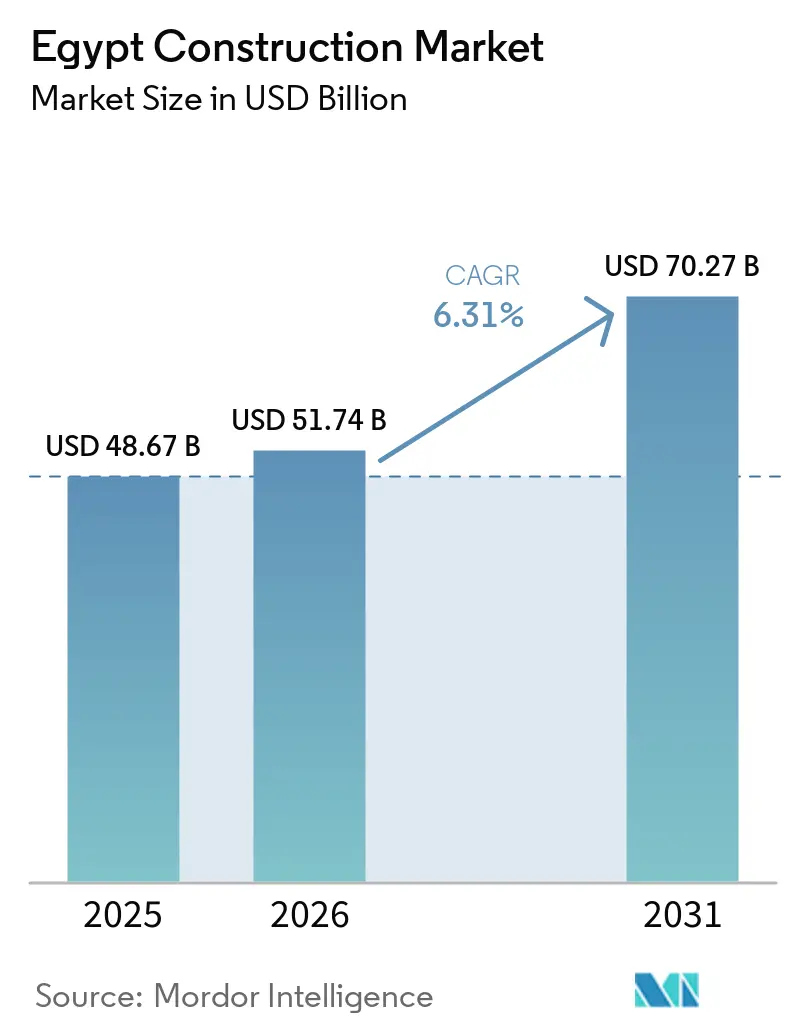

| Base Year Market Size (2025) | USD 48.67 Billion |

| Market Size (2026) | USD 51.74 Billion |

| Market Size (2031) | USD 70.27 Billion |

| Growth Rate (2025 - 2031) | 6.31% CAGR |

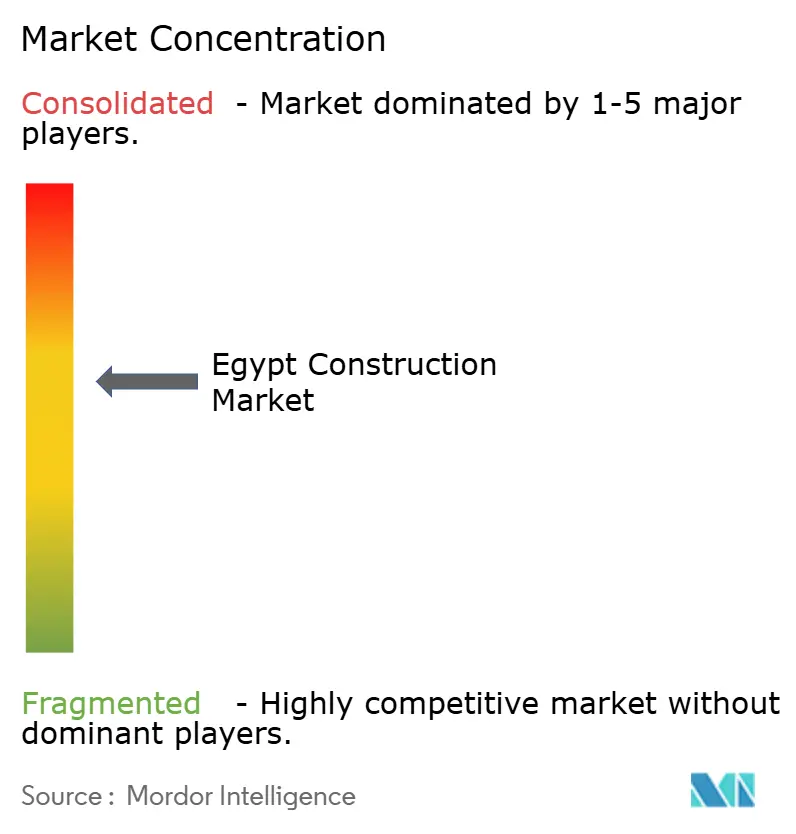

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Construction Market Analysis by Mordor Intelligence

The Egypt construction market size is projected to expand from USD 48.67 billion in 2025 and USD 51.74 billion in 2026 to USD 70.27 billion by 2031, registering a 6.31 % CAGR between 2026 and 2031. Growth is underpinned by large-scale public investment in cities, transport, energy, and water assets that anchor multi-year project pipelines and attract foreign capital to strategic industrial zones. Regulatory streamlining through instruments such as the Golden License and maturing PPP frameworks are gradually lowering barriers to entry for private participants and speeding up approvals for complex projects. Execution capabilities are consolidating around large contractors and technology-enabled consortia that can deliver to green-building, digital-twin, and safety requirements at scale. Currency stability and access to hard-currency financing remain vital to protect contractor margins and maintain predictable delivery schedules across import-reliant supply chains.[1]https://www.imf.org/en/home

Key Report Takeaways

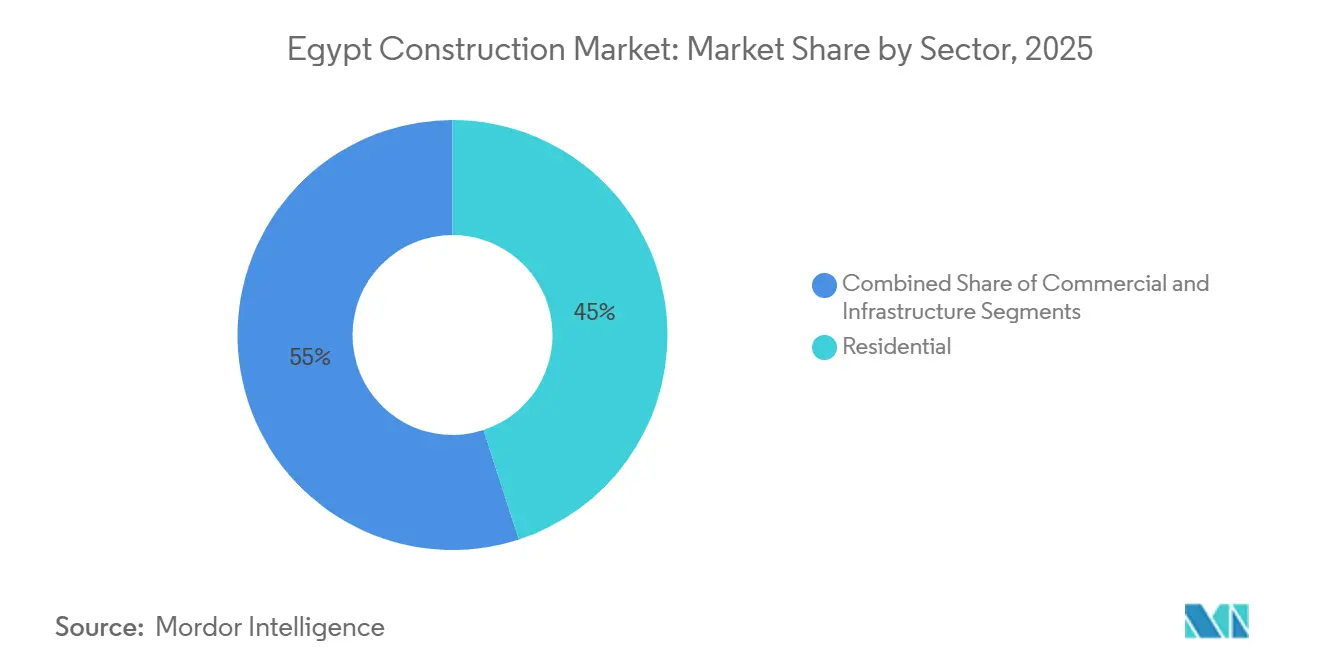

- By sector, Residential led with a 45% share of activity in 2025; Infrastructure is forecast to record the fastest growth at a 9.2% CAGR through 2031.

- By construction type, New Construction held 92% of the 2025 volume; Renovation is projected to expand at an 8.6% CAGR through 2031.

- By construction method, conventional on-site techniques retained a 90% share in 2025; Modern Methods of Construction are advancing at an 11.1% CAGR to 2031.

- By investment source, the public sector commanded 72% of the market in 2025; private capital is growing faster at a 9.9% CAGR through 2031.

- By geography, Greater Cairo accounted for 48% of activity in 2025 and is forecast to grow at a 9.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Government-Led Urban Expansion and Smart City Initiatives | +2.3% | National, concentrated in Greater Cairo, New Alamein, Qena, New Mansoura, and Damietta | Medium term (2-4 years) |

| Accelerated Energy Infrastructure Growth Driven by Decarbonization Goals | +1.8% | National, with intensity in the Gulf of Suez, Aswan, Nagaa Hammadi, SCZone Port Said | Long term (≥ 4 years) |

| Expansion of Multimodal Transport Networks Enhancing Connectivity and Regional Trade | +1.5% | National corridors, Greater Cairo, Alexandria, Upper Egypt axes | Medium term (2-4 years) |

| Rising Demand for Affordable and Middle-Income Housing Supported by State Financing and PPP Models | +1.2% | Greater Cairo, Giza, satellite cities, coastal resorts | Short term (≤ 2 years) |

| Increasing Foreign Investment in Industrial Zones, Logistics, and Infrastructure through Strategic Alliances | +1.2% | SCZone, West Qantara, NAC, Ras El-Hekma, North Coast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Government-Led Urban Expansion and Smart City Initiatives

A nationwide program of 24 new-generation cities, anchored by the USD 58 billion New Administrative Capital, is redefining how large-scale urban assets are planned, financed, and delivered. Phase 1 of the New Administrative Capital reached near-completion in 2025 with core government facilities, the Green River Park spine, and district services, establishing digital-ready standards for utilities and operations. The New Urban Communities Authority extended green-building incentives to May 2026 and set a June 2026 mandate for green-city standards across major new developments, which is accelerating the shift to energy-efficient designs and verified performance metrics. Modular high-rise systems deployed by China State Construction in the capital shortened schedules by six months compared with conventional approaches, proving the time and cost benefits of off-site manufacturing at scale. To reduce contracting frictions, an EBRD-backed Egypt Project Preparation Facility launched in September 2025 to improve feasibility and legal structuring ahead of tenders, while the Golden License scheme has fast-tracked permits for strategic projects by consolidating approvals, including 29 grants by March 2025. As digital requirements rise, contractors with BIM fluency and integrated project controls are capturing flagship work, while smaller firms without these capabilities are shifting to subcontract roles or to secondary-city projects with lighter specifications.[2]https://www.sis.gov.eg/

Accelerated Energy Infrastructure Growth Driven by Decarbonization Goals

Egypt targets 42% of electricity generation from renewables by 2030, supported by a national low-carbon hydrogen strategy that outlines industrial-scale electrolyzers, desalination, and export terminals in the Suez Canal Economic Zone. Scatec reached financial close in June 2025 on a multi-phase solar and storage complex at Nagaa Hammadi, with the first tranche set for commercial operation in 2026 under a 25-year PPA backed by a sovereign guarantee, signaling bankable structures for utility-scale build-out. AMEA Power began building a 1 GW solar facility with 600 MWh storage in Aswan in December 2025, with commissioning targeted for 2026, adding to the pipeline alongside Amunet wind at Ras Ghareb and ACWA Power’s Suez wind project. Desalination capacity is scaling as a strategic hedge for both industry and cities, with Phase I investments bringing significant daily output online toward longer-term goals to 2050, creating sustained opportunities in EPC, civil, and balance-of-plant works. The Egypt–Saudi interconnection line with 3 GW capacity advances Egypt’s hub ambitions despite milestone slippages, while the FY 2025/2026 public and private capital allocation of USD 2.8 billion to the electricity and renewables sector signals continued budget support for delivery. Codified standards like ISO 50001 and IEC 62446 are shaping prequalification and commissioning, tilting awards toward contractors with certified systems and trained personnel.[3]

Expansion of Multimodal Transport Networks Enhancing Connectivity and Regional Trade

Work is underway on a 2,000-kilometre high-speed rail backbone that links major urban and tourism centers, delivered by consortia with proven rail, signaling, and systems integration expertise. The Greater Cairo monorail has entered phased service, cutting peak travel times and stimulating mixed-use development around stations, while Metro Line 3’s January 2024 extension added six stations and increased passenger-carrying capacity. Alexandria’s Abu Qir corridor conversion to electric metro is advancing through a project management contract that improves energy efficiency and service reliability along the coastal axis. Upper Egypt recorded more than 3,000 kilometres of new and upgraded roads in recent programs, connecting agricultural zones, industrial parks, and tourism sites with national corridors. Port capacity at East Port Said expanded in November 2025 by 2.2 million TEUs through a USD 500 million investment, with automation and electric yard equipment improving throughput and environmental performance. The new Suez Canal Automotive Terminal adds roll-on roll-off and processing capability, enabling export-oriented assembly platforms aligned with SCZone incentives and global port security standards.

Rising Demand for Affordable and Middle-Income Housing Supported by State Financing and PPP Models

Delivery of 650,000 state-backed affordable units by May 2025 and subsidized mortgage rates at 3% widened access for lower-income households and de-risked demand for entry-level developments near transit and employment hubs. Developer participation has broadened and deepened, with top sellers recording USD 13.3 billion in first-half 2025 transactions, supported by flexible payment plans and brand-led communities that appeal to both domestic and expatriate buyers. Residential prices increased through 2025, prompting developers to use cash discounts to manage liquidity and accelerate collections in a high-rate environment. Cross-border appetite has strengthened, with foreign and expatriate buyers accounting for a material share of 2025 sales and property export receipts reaching USD 1.5 billion on improved legal protections and digitized processes in the pipeline. Mortgage origination rose to USD 340 million in the first five months of 2025 but remains a small share of total transactions, indicating room for policy-led expansion in the middle-income segment through tiered subsidy models under consideration. Law 165 of 2025 begins a multi-year transition away from fixed rents, which could lift renovation activity and new affordable supply as landlords and developers reposition rental stock over time.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Currency Volatility Impacting Import-Dependent Supply Chains and Contractor Profitability | -0.9% | National, acute in import-reliant sectors, steel, equipment, specialty materials | Short term (≤ 2 years) |

| Structural Bureaucratic Delays in Land Titling, Permitting, and Approvals Slowing Project Pipelines | -0.6% | National, more severe in urban governorates, Cairo, Alexandria, Giza | Medium term (2-4 years) |

| Chronic Skilled Labour Deficit in High-Demand Specializations Hindering Quality and Timelines | -0.5% | National, with a higher impact on infrastructure and industrial construction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Currency Volatility Impacting Import-Dependent Supply Chains and Contractor Profitability

Devaluations and exchange-rate resets in 2024 raised local-currency costs for imported materials and equipment, compressing margins on fixed-price contracts and complicating cash-flow planning across project portfolios. Steel import exposure through key inputs and duties intersects with supply gaps at domestic mills during demand spikes, while cement output gains in 2025 stabilized prices but left exporters constrained by domestic allocation rules. Foreign-exchange scarcity periodically delayed port clearances and spiked warehousing and demurrage fees, adding cost layers in already tight schedules. Contractors responded by front-loading procurement, seeking escalation clauses, and pivoting to localized supply lines, including new industrial plants within SCZone and Upper Egypt. Limited hedging options and shallow derivatives markets leave mid-tier contractors exposed to currency swings, while a 10% rise in imported inputs can lift total build cost by 5–7% and pressure net margins in a sector where listed developers often target 10–15% over multi-year cycles. Firms pursuing international finance also face stricter reporting under IFRS and national oversight by the financial regulator, which requires robust risk controls to unlock cross-border capital.

Structural Bureaucratic Delays in Land Titling, Permitting, and Approvals Slowing Project Pipelines

Complex overlapping authorities at national, governorate, and special-zone levels extend average land and permitting lead times by 6–12 months in dense urban governorates, delaying mobilization and raising pre-construction carrying costs. A significant subset of PPP contracts encounter legal challenges on dispute resolution and scope interpretation, prompting the launch of a dedicated project preparation facility in September 2025 to strengthen feasibility, risk allocation, and contracting clarity before tender. The Golden License consolidates approvals for strategic projects but remains tightly scoped, with 29 licenses issued by March 2025 and criteria that broadly favor very large investors and export-oriented platforms. Relaxed Private Free Zone rules lowered entry thresholds and capital minimums, though the geographic concentration of zones can leave mid-sized cities underserved by streamlined regimes. Policymakers are advancing a digital property-ID framework to reduce title disputes and lender risk perception, which could shorten timelines and improve collateral transparency once operational. Environmental approvals remain mandatory for projects above set thresholds and add to schedules, but they also enhance bankability and alignment with international standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Ascends as Public Capital Prioritizes Backbone Assets

Residential construction held the largest share at 45% in 2025, supported by state-backed delivery programs and mortgage subsidies that stabilize entry-level demand in key metros. Infrastructure is the fastest-growing segment at a projected 9.2% CAGR through 2031, reflecting policy emphasis on transport, energy, and water systems that underpin industrial activity and city expansion. Transport programs span a 2,000-kilometre high-speed rail network, phases of the Cairo monorail, and metro extensions, with award structures that align national contractors and technology partners on complex delivery. Energy and utilities projects are scaling under a national renewables target of 42% of generation by 2030 and a low-carbon hydrogen strategy that requires significant civil, mechanical, and electrical works. Commercial builds in office, retail, logistics, hospitality, healthcare, and education progress at mid-single-digit rates as financing costs moderate and foreign capital supports anchor developments in Greater Cairo and new cities. Tourism-linked assets benefit from major cultural openings like the Grand Egyptian Museum in 2025, which catalyzes hospitality and urban-realm projects with heritage integration.

Investors focus on program visibility and contracting capacity when allocating capital within the Egypt construction market, with PPP frameworks and sovereign support shaping risk-adjusted returns for backbone assets. Large public budgets dedicated to electricity and renewables in FY 2025/2026 reinforce demand for EPC contractors that meet stringent technical and safety standards. The Egypt construction market size for infrastructure is positioned to benefit from multi-year rollouts tied to transport corridors, desalination, and grid expansions that are already funded and in execution at scale. Data centers and industrial platforms are emerging demand nodes as manufacturers localize and service providers co-locate in new cities with reliable power and fiber connectivity. Portfolio developers continue to balance residential launches with mixed-use precincts linked to transit investments, adjusting payment schedules and project phasing to align with buyer liquidity and interest-rate trends.

By Construction Type: New Build Dominance Persists as Retrofit Economics Improve in Urban Cores

New Construction accounted for 92% of 2025 activity and is expected to maintain momentum as national programs advance greenfield cities, corridors, and industrial zones with modern codes and digitized utilities embedded from the start. The New Administrative Capital and sister new-city projects command the bulk of public funding and continue to attract private co-investment in residential and commercial parcels that align with phased infrastructure delivery. This bias reflects the need for scaled, integrated systems to meet urbanization and industrial goals and the relative predictability of large, state-led project pipelines for contractor planning. The Egypt construction market rewards teams that can deliver quality, safety, and schedule adherence under strict performance requirements on transformational assets.

Renovation and adaptive reuse, while a smaller share, are expanding as policy changes and energy-efficiency mandates lift demand for upgrades in established districts. Green-building incentives that extend into 2026 and become mandatory thereafter for new-city projects apply to major retrofits, which encourage owners to invest in performance improvements and lifecycle cost reductions. Landmark cultural and tourism precincts in Greater Cairo showcase combinations of conservation and modern building systems, raising the profile of specialized renovation contractors. The Egypt construction market also sees rising interest in energy retrofits and rooftop solar for commercial properties as electricity tariffs and corporate commitments to sustainability shape asset strategies. Building code compliance on fire safety and seismic standards remains a core requirement in large retrofit programs, reinforcing demand for firms with structural engineering and MEP integration expertise.

By Construction Method: Modular and Prefab Gain Share as Timelines and Labour Costs Escalate

Conventional on-site methods retained 90% of activity in 2025, reflecting deep contractor familiarity and an abundant labor pool for traditional workflows. Modern Methods of Construction, including prefabrication and modular techniques, are growing at an 11.1% CAGR as schedule compression and quality control gains become more visible in high-rise and repetitive-unit projects. Modular towers in the New Administrative Capital trimmed delivery by six months compared with conventional builds, signaling strong potential in urban cores where logistics and sequencing are complex. Rising wage floors and annual increases under the 2025 labor law amplify the case for factory-based production that reduces on-site labor requirements and rework. The Egypt construction market is shifting toward ISO-aligned digital workflows, and MMC aligns with BIM-driven precision and repeatability for faster and more predictable outcomes.

Barriers to broader MMC adoption include limited local manufacturing for prefabricated components and exposure to currency swings if imported modules or systems are required. Contractors weigh equipment and training investments against expected pipeline visibility and client acceptance, especially in segments where aesthetic customization is a priority. Standardization around ISO 19650 and national specifications is improving, and pro-innovation licensing frameworks signal policy support for technology transfer and industrialized building techniques. Renewable energy construction provides a natural proving ground for modular assembly, which can be replicated at scale across multiple sites. Oversight bodies continue to enforce structural, fire, and durability standards for factory-made components to ensure outcomes meet or exceed those of conventional builds.

By Investment Source: Private Capital Accelerates as PPP Reforms and FDI Inflows Narrow Public Dominance

Public-sector investment represented 72% of total activity in 2025, underscoring the state’s role as anchor client for transport, energy, water, defense, and city-building programs. Private capital accounted for 28% and is projected to grow at a 9.9% CAGR, supported by FDI inflows, refined PPP frameworks, and deepening mortgage and property-export channels. Net FDI reached USD 46.1 billion in 2024, with landmark commitments in coastal city development, logistics, and large-scale residential districts. Private Free Zone reforms widened access for mid-tier projects, while the Golden License and updated concession models improved visibility for multi-asset, multi-phase investments. The Egypt construction market is also seeing more diversified financing stacks, including development finance, export credit, and local bank participation on bankable structures.

Mortgage finance is expanding from a low base and gives developers an additional channel to sustain sales conversion for budget-sensitive buyers. SCZone continues to attract private manufacturing and logistics platforms that require dedicated utilities and bespoke civil works, broadening the construction pipeline beyond residential and traditional commercial assets. As legal and contracting clarity improves through pre-tender preparation support and standardized templates, more private sponsors can participate in infrastructure alongside state entities. The Egypt construction market will likely benefit from joint ventures that blend local delivery experience with global EPC specializations, especially in rail, power, and industrial facilities. The combined effect is a gradual rebalancing of funding mix and risk allocation that supports faster project cycling without compromising standards.

Geography Analysis

Greater Cairo anchors the Egypt construction market with 48% of 2025 activity and a forecast 9.1% CAGR through 2031 as government relocation, transit projects, and cultural assets concentrate demand for residential, commercial, and civic builds. The New Administrative Capital’s phased delivery and linked monorail lines expand the viable residential catchment and enable denser, mixed-use clusters near stations. The Grand Egyptian Museum’s 2025 opening amplifies hospitality and retail investments in adjacent areas and enhances Cairo’s status as a global culture and tourism hub. Developers are sequencing launches to align with transit milestones, new schools and healthcare facilities, and the progressive build-out of district utilities.

Alexandria’s program includes the Abu Qir Metro conversion to electric operations and port-area upgrades, which improve mobility, energy efficiency, and trade capacity in the Eastern Mediterranean axis. The city attracts buyers and tenants seeking lower land costs and strong logistics access compared with Greater Cairo, supporting mid-market residential and commercial builds. Giza’s catchment benefits from the GEM, pedestrian connections, and airport enhancements, creating opportunities for hospitality, retail, and premium residential near tourism anchors. The Egypt construction market in these metros favors projects that coordinate with transit timelines and tourism calendars to optimize absorption and pricing.

Upper Egypt and canal-adjacent zones show robust pipelines tied to renewables, irrigation, and port expansions, including large PV and storage complexes and new container and automotive terminals. SCZone’s regulatory environment and infrastructure readiness remain catalysts for export-oriented manufacturing and logistics projects that require upfront civil and MEP works. Public investments in water, roads, and grid strengthen the commercial case for industrial parks and suppliers seeking to localize near ports and corridors. The Egypt construction market continues to balance mega-projects in core metros with distributed industrial and infrastructure assets across governorates to widen economic opportunities.

Competitive Landscape

Competition in the Egypt construction market is moderate-to-high, with more than 1,900 private developers alongside state-owned champions and international EPCs active on mega-projects. Orascom Construction, Arab Contractors, and Hassan Allam dominate complex transport, energy, and water projects due to proven capacity, certifications, and safety records, while joint ventures with global partners deliver specialized rail and renewable systems. In 2025, Orascom Construction and OCI Global announced a combination to create a platform focused on infrastructure investment and delivery, targeting over USD 1 billion in equity deployment by year-end 2026. Residential and commercial development is led by brand-name platforms that differentiate on location, amenities, and payment flexibility, with rising regional diversification to offset currency and demand volatility.

Notable awards underscore momentum. Concrete Plus secured a USD 71 million package in December 2025 for CityGate New Cairo, an integrated project planned to generate significant jobs and community infrastructure. APM Terminals inaugurated a USD 500 million port expansion at East Port Said in November 2025, adding 2.2 million TEUs of capacity with electrified equipment for lower emissions. The Suez Canal Automotive Terminal and other SCZone assets have been launched to support vehicle processing and exports, complementing manufacturing and logistics pipelines. These moves reinforce the central role of port, logistics, and city-building projects in shaping contracting opportunities and technology adoption cycles.

Egypt Construction Industry Leaders

The Arab Contractors

Orascom Construction PLC

Hassan Allam Holding

Elsewedy Electric (Engineering & Construction, Utilities)

Petrojet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Qatari Diar Egypt awarded Concrete Plus a USD 71 million construction package for the CityGate New Cairo project, covering 300 residential units and infrastructure works over a 30-month delivery period within the USD 12 billion integrated urban development linking New Cairo to the New Administrative Capital. The project, spanning approximately 8.5 million square meters, is expected to generate over 200,000 direct and indirect job opportunities and includes business districts, world-class golf courses, and extensive educational, healthcare, and sports facilities.

- December 2025: Orascom Construction PLC and OCI Global announced a strategic combination to create a Global Infrastructure and Investment Platform, with OCI valued at approximately USD 1.35 billion and Orascom Construction at USD 1.52 billion. The combined entity, to be renamed "Orascom" and headquartered in Abu Dhabi with a secondary listing on the Egyptian Exchange, aims to deploy more than USD 1 billion of equity by year-end 2026 into scalable, cash-generative infrastructure assets, leveraging Orascom Construction's USD 8.6 billion backlog and renewable-energy concessions in Egypt.

- December 2025: AMEA Power began construction on a 1 GW solar photovoltaic facility integrated with 600 MWh of battery energy storage in Aswan Governorate, representing over USD 700 million in investment and expected to become Africa's largest single-site hybrid renewable facility upon commercial operation in June 2026.

- November 2025: APM Terminals inaugurated a USD 500 million expansion of the Suez Canal Container Terminal in East Port Said, adding 2.2 million TEUs of annual capacity to reach 7 million TEUs total, deploying 30 electric rubber-tired gantry cranes, and generating over 1,000 new jobs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Egypt construction market as the total annual spending, expressed in nominal US dollars, on new-build and major renovation activities across residential, commercial, industrial, energy and utilities, and transport infrastructure projects located within Egypt's borders. We treat spending at the project owner level, thereby capturing on-site labor, materials, professional services, and contractor margins.

Scope Exclusion: Small-ticket repair and maintenance work, second-hand equipment rental, and off-shore engineering design performed outside Egypt are excluded.

Segmentation Overview

- By Sector

- Residential

- Apartments/Condominiums

- Villas/Landed Houses

- Commercial

- Office

- Retail

- Industrial and Logistics

- Others

- Infrastructure

- Transportation Infrastructure (Roadways, Railways, Airways, others)

- Energy & Utilities

- Others

- Residential

- By Construction Type

- New Construction

- Renovation

- By Construction Method

- Conventional On-Site

- Modern Methods of Construction (Prefabricated, Modular, etc)

- By Investment Source

- Public

- Private

- By Geography

- Greater Cairo

- Alexandria

- Giza

- Rest of Egypt

Detailed Research Methodology and Data Validation

Primary Research

To close gaps, we conducted structured interviews with project developers, EPC contractors, real-estate financiers, and provincial permitting officials across Greater Cairo, Alexandria, and Upper Egypt. Inputs on average selling prices, lead-time slippage, and funding pipelines allowed us to validate desk estimates and adjust cost escalation assumptions.

Desk Research

Our analysts first gathered macroeconomic baselines and construction-specific indicators from tier-1 public sources such as CAPMAS, the Central Bank of Egypt, the Ministry of Housing, IMF's WEO, UN Comtrade shipment logs, and World Bank infrastructure dashboards. Project-level insights were enriched through reputable trade outlets and parliamentary budget papers, while D&B Hoovers and Dow Jones Factiva helped screen contractor financials and news flows. These examples are illustrative; many additional references supported data capture and clarification.

A follow-up scan of building permits, cement output, steel rebar imports, and sovereign bond prospectuses provided fresh volume and cost signals that guided segment splits and trend inflection checks.

Market-Sizing and Forecasting

The baseline originates from a top-down reconstruction of national investment accounts, calibrated with CAPMAS construction output tables and import duties, then cross-checked against sampled contractor backlogs (bottom-up cross-section). Key model drivers include population growth, mortgage uptake, public capital expenditure ceilings, building materials inflation, and high-speed rail kilometer additions. Forecasts use multivariate regression blended with scenario analysis; GDP growth, cement price index, and government capital spend plans are the lead variables. Where contractor roll-ups fell short, average selling prices from tender data bridged gaps before final triangulation.

Data Validation and Update Cycle

Mordor analysts run variance checks versus historical CAGR bands, peer ratios, and external cost indices, escalating anomalies for senior review. Models refresh every 12 months, with interim updates triggered by material policy shifts or megaproject awards; a final pre-publication sweep ensures clients receive the latest vetted view.

Why Our Egypt Construction Baseline Stands Firm

Published estimates often diverge because firms apply different scopes, inflation treatments, and update cadences. Mordor's disciplined scope alignment with national accounts and annual refresh timing narrows those gaps and yields a figure decision-makers can readily trace.

Key gap drivers include whether land acquisition is counted, if nominal or constant prices are used, and how megaproject outlays are staged through time.

Some publishers add equipment purchases or, conversely, report contractor output in real terms, generating sizable swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 50.9 bn (2025) | Mordor Intelligence | - |

| USD 74.4 bn (2024) | Regional Consultancy A | Counts building materials sales and equipment imports inside market value |

| USD 27.1 bn (2024) | Global Consultancy B | Excludes government-funded megaproject outlays; uses constant price contractor output |

In sum, our measured inclusion criteria, dual-angle modeling, and frequent validation cycles give Mordor Intelligence numbers a balanced middle ground that clients trust for budgeting and strategic planning.

Key Questions Answered in the Report

What is the current size and growth outlook for the Egypt construction market?

The market is projected to expand from USD 48.67 billion in 2025 to USD 51.74 billion in 2026, reaching USD 70.27 billion by 2031, registering a CAGR of 6.31% between 2026 and 2031, supported by large-scale public investments across urban infrastructure, transportation, energy, and water sectors.

Which segment grows fastest within the Egypt construction market to 2031?

Infrastructure is the fastest-growing segment with a forecast 9.2% CAGR as transport corridors, renewable energy, and water infrastructure attract sustained public and private investment.

What region leads activity within the Egypt construction market?

Greater Cairo leads with 48% of 2025 activity and is set for a 9.1% CAGR through 2031, driven by the New Administrative Capital, metro and monorail expansions, and cultural investments like the Grand Egyptian Museum.

How are PPP and regulatory reforms affecting the Egypt construction market?

PPP refinements, the Golden License, and improved pre-tender preparation are broadening private participation and speeding up approvals for strategic assets, improving bankability and delivery timelines.

What macro risks could affect project delivery in the Egypt construction market?

Currency volatility, bureaucratic delays, and skilled labour gaps remain key risks, affecting import costs, lead times, and quality, though policy and training initiatives aim to mitigate these factors.

Which recent milestones signal momentum in the Egypt construction market?

Notable 2025 milestones include APM Terminals’ USD 500 million East Port Said expansion, AMEA Power’s 1 GW solar-plus-storage groundbreaking, and the opening of the Grand Egyptian Museum, each reinforcing construction demand drivers.

Page last updated on: