Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

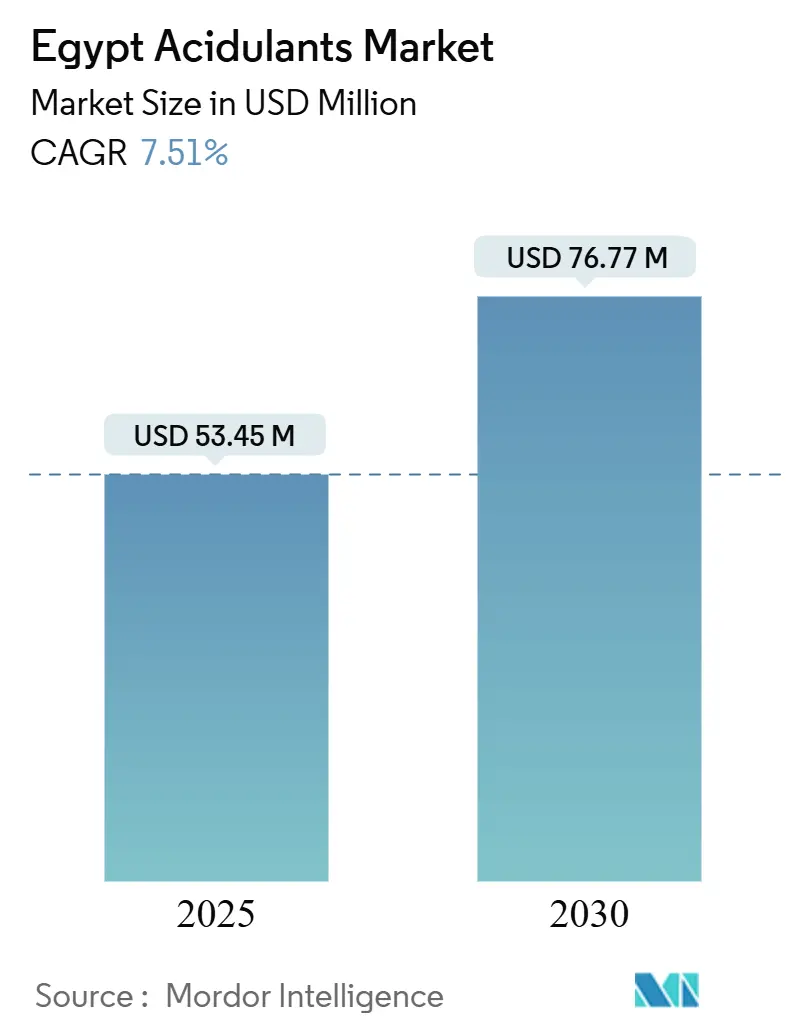

| Market Size (2025) | USD 53.45 Million |

| Market Size (2030) | USD 76.77 Million |

| Growth Rate (2025 - 2030) | 7.51% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Acidulants Market Analysis by Mordor Intelligence

The Egyptian acidulants market size is estimated to be valued at USD 53.45 million in 2025 and is forecast to reach USD 76.77 million by 2030, reflecting a 7.51% CAGR. Rising orange processing volumes, shelf-life mandates for meat and dairy, and fast-track customs clearance for food inputs are expanding demand well beyond beverages. Export-oriented complexes in Sadat City and the Suez Canal Economic Zone anchor new capacity, while golden-license approvals shorten project lead times. Moreover, currency weakness raises import costs for bulk acids, yet it simultaneously pushes manufacturers to localize fermentation and blending. Overall, the Egyptian acidulants market benefits from policy support, citrus abundance, and industry moves toward clean-label formulations that favor naturally fermented lactic and citric acids.

Key Report Takeaways

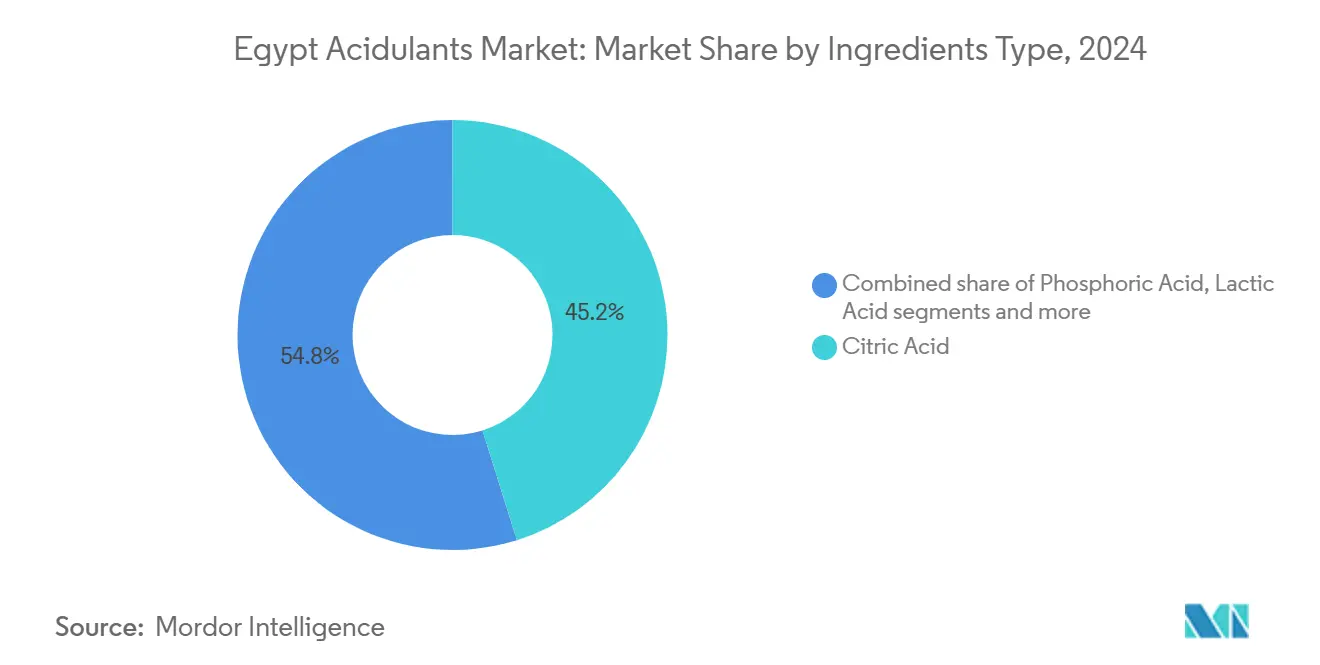

- By ingredients type, citric acid led with 45.16% revenue share in 2024; lactic acid is projected to expand at an 8.57% CAGR through 2030.

- By application, beverages captured 37.81% of the Egyptian acidulants market share in 2024; bakery and confectionery is forecast to advance at an 8.24% CAGR to 2030.

Egypt Acidulants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for processed and convenience foods boosts acidulant use for flavor enhancement | +1.5% | National, concentrated in Greater Cairo, Alexandria, and Delta governorates | Medium term (2-4 years) |

| Need for shelf-life extension in meat and frozen products supports acidulant integration | +1.3% | National, with export-oriented facilities in Suez Canal Economic Zone and Sadat City | Short term (≤ 2 years) |

| Clean-label preference for natural acidulants | +1.0% | Urban centers (Cairo, Giza, Alexandria); spillover to premium export channels | Long term (≥ 4 years) |

| Surging demand for RTD beverages | +1.4% | National, led by Greater Cairo and Delta; export to Arab markets | Medium term (2-4 years) |

| Consumer preference for tangy and sour flavors drives adoption in confectionery and bakery | +0.9% | National, with concentration in urban retail and modern trade | Medium term (2-4 years) |

| Export-oriented citrus processing expansion | +1.2% | Nile Delta citrus belt (Sharqia, Beheira, Ismailia); processing hubs in Sadat City and 10th of Ramadan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for processed and convenience foods boosts acidulant use for flavor enhancement

The growing demand for processed and convenience foods in Egypt is reinforcing the importance of acidulants as essential functional ingredients in value-added manufacturing. In 2024, the processed food sector in Egypt achieved exports worth USD 6.1 billion, reflecting a 21% year-on-year growth [1]Source: Daily News Egypt, "Egypt’s Food Exports Surge 21% in 2024", dailynewsegypt.com. This growth underscores a shift toward higher-margin, export-oriented products that depend on precise flavor modulation, pH control, and microbial stability, functions enabled by citric, phosphoric, and lactic acids in formulations. Local manufacturers are expanding production of ready-to-use tomato pastes, sauces, fruit preparations, juices, and frozen meals, where acidulants are critical for standardizing taste profiles and ensuring shelf life consistency, which are essential for export compliance and brand reliability. Companies such as Juhayna and Faragalla leverage these attributes to compete on both flavor and product stability. The government’s golden-license initiative, highlighted by the November 2024 establishment of a factory by Balkan Food Industries in New October City with an investment of EGP 850 million, demonstrates how industrial policies are driving demand for citric acid and related acidulants. These ingredients are vital in tomato paste and fruit concentrate production, ensuring acidity regulation, color retention, and microbial safety. Leading beverage and juice brands, including PepsiCo’s local operations and Juhayna’s juice portfolio, rely on acidulants to provide the characteristic tang in carbonated drinks and juices while harmonizing flavors despite seasonal variations in sugar levels or fruit solids. Retailers expanding private-label canned and ambient products, such as tomato paste, soups, and ready sauces, further drive demand for robust acidulant systems to achieve ambient stability without compromising sensory quality. The focus on locally sourced raw materials in projects like Balkan Food Industries promotes integration between agriculture and processing, supporting long-term supply contracts for food-grade acidulants and enhancing Egypt’s processed food industry competitiveness.

Need for shelf-life extension in meat and frozen products supports acidulant integration

The extension of shelf-life requirements for meat and frozen products is driving increased integration of acidulants in preservation processes across Egypt. Regulatory authorities have extended the shelf life of frozen beef and buffalo liver from 7 to 12 months, frozen fish from 6 to 10 months, and plain and flavored yogurt from 15 to 30 days, effective July 2024 [2]Source: United States Department of Agriculture, "Egypt Formalizes Twelve Month Shelf-Life Validity Period for Frozen Beef Liver", apps.fas.usda.gov. These changes necessitate the adoption of acidulant-based systems for pH adjustment and microbial control, enabling compliance without significant infrastructure changes. Research indicates that a 2% lactic acid spray can reduce microbial loads by 1.5 to 3.0 log CFU/g and extend chilled beef shelf life from 3 days to 7-9 days under refrigeration, offering small and medium processors a cost-effective alternative to vacuum packaging that integrates with existing spray or dip lines. Leading brands such as Americana Group utilize lactic acid applications to meet regulatory standards while maintaining product quality for export-ready lines targeting Gulf markets. Dairy producers like Juhayna and Beyti have incorporated acidulants into yogurt formulations, doubling the shelf life of flavored variants, facilitating broader retail distribution, and reducing supply chain waste. Fish processors, including suppliers to Metro Markets' private-label frozen seafood, benefit from phosphoric and lactic acid blends that enhance microbial inhibition and firmness retention, extending frozen viability to 10 months. These regulatory shifts, supported by research-backed techniques, enable mid-tier processors to scale production of value-added frozen meals without capital-intensive upgrades, while larger brands like Faragalla standardize acidulant dosing for consistent quality. This synergy between regulation and research underscores the essential role of acidulants in driving operational efficiency and supporting the growth of Egypt's meat and frozen products market.

Surging demand for RTD beverages

The increasing demand for ready-to-drink (RTD) beverages is significantly driving the consumption of acidulants in Egypt. Manufacturers are utilizing citric, phosphoric, and malic acids to achieve consistent tartness, balance sweetness, and ensure microbial stability in RTD products, aligning with the growing export momentum. In the first half of 2024, soft drink concentrates emerged as Egypt's top processed food export, generating USD 309 million in revenue as per the Cabinet's Information and Decision Support Centre (IDSC) [3]Source: State Information Service (SIS), "Egypt's Food Industry Exports Increase By 25% during H1 of 2024: IDSC", sis.gov.eg. This growth reflects a shift toward scalable RTD production, where acidulants are essential for replicating authentic fruit flavors and extending shelf life in carbonated juices, energy drinks, and flavored waters targeting both domestic and MENA markets. International players, such as Coca-Cola's Egyptian plants, incorporate phosphoric acid in cola formulations to achieve signature taste profiles and pH control, supporting high-volume RTD lines that capitalize on the export surge for private-label extensions. As RTD iced teas, lemonades, and functional beverages expand in urban convenience stores, acidulants like malic acid provide prolonged taste perception, helping mid-sized producers like V7 compete on sensory appeal without preservatives. Additionally, acidulants stabilize emulsions and prevent precipitation in clear beverages, ensuring reliability for e-commerce and out-of-home consumption. Brands leverage these attributes in RTD fruit punches, linking export growth to domestic innovation in low-calorie variants that demand fine-tuned acidity, thereby driving market growth through flavor consistency and production scalability in Egypt's beverage industry.

Consumer preference for tangy and sour flavors drives adoption in confectionery and bakery

The growing consumer preference for tangy and sour flavors is driving the increased use of acidulants in Egypt's confectionery and bakery industries. Citric and malic acids are being utilized to create sharp flavor profiles in products such as gummies, hard candies, and baked snacks, catering to regional taste preferences and enhancing product differentiation in competitive retail markets. Manufacturers are leveraging these acids to develop distinct sour notes that improve mouthfeel and appeal in items like fruit chews and lemon-flavored biscuits, aligning with consumer trends favoring bold, zesty flavors over traditional sweet options. This shift is further supported by multinational investments, including Barry Callebaut's October 2024 announcement of a USD 30 million chocolate manufacturing project in Egypt, aimed at meeting local demand and positioning the country as a regional export hub for the Middle East and Africa. Acidulants play a critical role in these markets as flavor enhancers and pH adjusters, ensuring consistent tartness in filled chocolates and compound coatings. Local brands such as Bisco Misr incorporate malic acid in products like sour cream crackers and fruit-filled pastries to deliver tangy flavor bursts that resonate with urban consumers, while confectionery manufacturers like Gandour use citric acid in Molto sour gummies and hard candies to achieve precise sourness levels that support export growth to Gulf markets. As premium chocolate fillings and coated snacks gain popularity, acidulants balance cocoa bitterness with fruit-forward acidity, enabling mid-tier producers to differentiate yogurt-coated sour treats in modern trade channels. Barry Callebaut's investment underscores the importance of acidulant-based formulations in compound coatings, where pH control prevents bloom and ensures shelf stability during export logistics, solidifying acidulants as essential components in the evolving confectionery and bakery landscape.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Geographic Relevance |

|---|---|---|---|

| Raw material price volatility | -0.8% | National, with acute impact on import-dependent processors in Greater Cairo and Alexandria | Short term (≤ 2 years) |

| Stringent regulatory standards limit synthetic acidulant usage | -0.6% | National, enforced by National Food Safety Authority (NFSA) and Egyptian Organization for Standardization and Quality (EOS) | Medium term (2-4 years) |

| FX shortages hindering bulk-acid imports | -1.0% | National, concentrated among small and medium processors lacking FX allocation | Short term (≤ 2 years) |

| Compliance requirements raise operational burdens for manufacturers | -0.5% | National, disproportionately affecting SMEs without ISO/IEC 17025 lab access | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw material price volatility

Volatility in raw material prices poses a significant challenge for the acidulants market in Egypt. Global fluctuations in the prices of citric, lactic, and phosphoric acids are closely tied to feedstock costs such as corn, molasses, and phosphate rock, as well as energy and freight expenses, compressing margins for processors lacking long-term supply security. The depreciation to over EGP 50 per USD in December 2024 has further amplified landed costs for imported bulk acids, with phosphoric acid sourced from Asian producers and acetic acid from European suppliers becoming significantly more expensive in local currency terms. This has particularly impacted small and medium-sized food manufacturers operating on thin margins. The currency depreciation, combined with volatile international contract prices, has forced many mid-tier players to narrow product portfolios or implement frequent price increases in carbonated soft drinks, juices, and processed foods, risking volume losses in price-sensitive retail channels. The absence of domestic fermentation capacity at a commercial scale entrenches import dependency for key inputs like citric and lactic acids, exposing local manufacturers to global spot market fluctuations, freight bottlenecks, and exchange rate volatility. Consequently, some manufacturers in segments such as bakery mixes or economy beverages reformulate with lower acidulant loadings or substitute with less effective, lower-purity alternatives, which can dilute flavor impact and reduce shelf life, undermining brand equity. Value-tier private-label beverage and sauce brands often reduce citric or phosphoric acid levels to maintain price points, while premium players like Juhayna or Faragalla prioritize sensory quality but face tighter profitability. This persistent input risk complicates long-term planning for multinational bottlers like PepsiCo, which must balance global formulation standards with locally volatile cost structures, ultimately constraining acidulant demand growth and slowing the adoption of higher-value acidulant systems.

Stringent Regulatory Standards Limit Synthetic Acidulant Usage

Stringent regulatory standards limiting the use of synthetic acidulants present significant challenges for manufacturers operating in Egypt. The National Food Safety Authority’s Decision No. 4/2020 on food additives incorporates European Union regulations while mandating halal certification, creating a dual compliance framework that complicates approvals for new formulations. This dual requirement restricts the use of synthetic acidulants in key categories such as beverages, confectionery, and dairy, as manufacturers must align with Euorpean Union additive codes and halal standards, extending registration and reformulation timelines. The Egyptian Organization for Standardization (EOS), through ES 2613-2/2008, further enforces shelf-life specifications that limit storage durations by product category, indirectly constraining the use of synthetic acidulants to ensure compliance with sensory and acceptable daily intake thresholds. International brands such as Coca-Cola encounter delays in launching new SKUs due to additional documentation and halal validation requirements, while smaller domestic manufacturers, with limited resources, avoid advanced synthetic systems, opting for simpler solutions that may compromise shelf life or flavor. Stricter enforcement and documentation requirements increase transaction costs for synthetic acidulant suppliers, reducing the appeal of promoting higher-value portfolios. These overlapping regulatory constraints are gradually steering the market toward natural, halal-compliant, and lower-intensity solutions, limiting the technical potential of acidulants in Egypt.

Segment Analysis

By Ingredients Type: Lactic Acid Fermentation Gains on Meat Preservation Mandates

Citric acid holds a dominant position in the market, accounting for 45.16% of the share in 2024, driven by its extensive application in beverages, confectionery, and bakery products. This leadership is supported by Egypt's significant citrus production, with an orange output of 3.7 million metric tonnes in 2024/25 and a forecasted 50% increase in processing utilization to 600,000 metric tonnes as per USDA. The integration of direct extraction and fermentation-based production using citrus molasses as feedstock enhances supply reliability and cost efficiency for local users. Leading beverage and juice brands, including Juhayna and Faragalla, rely on citric acid for acidity modulation, flavor consistency, and shelf-life optimization in their products. Phosphoric acid remains essential for the carbonated soft drink segment, with Coca-Cola HBC’s acquisition of Egyptian bottling operations consolidating demand under an integrated supply structure. However, the maturity of this category limits growth compared to lactic acid, which is gaining traction across diverse applications. Acetic acid continues to play a pivotal role in pickles, condiments, and sauces, as evidenced by Kraft Heinz’s expansion of its Cairo facility in September 2024 to include ketchup and mayonnaise lines, leveraging acetic acid for pH adjustment and emulsion stability.

Lactic acid is the fastest-growing ingredient segment, projected to grow at a CAGR of 8.57% through 2030, driven by its expanding use in meat preservation and functional applications. Research demonstrating its ability to extend chilled beef shelf life from 3 to 7-9 days has provided processors with a cost-effective solution to meet stricter safety standards. Regulatory changes in July 2024, extending frozen beef liver storage from 7 to 12 months, further support its adoption. Additionally, dairy producers like Beyti and Obour Land utilize lactic acid for fermentation control and pH management, while its role in bakery as a dough conditioner aligns with cleaner-label trends. Other acids, such as tartaric, fumaric, and malic, maintain specialized roles in confectionery and bakery, enhancing sourness profiles and pH levels in products for brands like Bisco Misr and Gandour.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Bakery and Confectionery Premiumization Outpaces Beverage Maturity

Beverages continue to dominate as the largest application segment, accounting for 37.81% of the application share in 2024. This is supported by Egypt’s USD 532 million in soft drink concentrate exports, which drive consistent demand for citric and phosphoric acids in carbonated soft drinks and juice-based ready-to-drink (RTD) products. However, as the beverage category matures, growth opportunities are becoming more limited. In contrast, the bakery and confectionery segment is expanding at a compound annual growth rate (CAGR) of 8.24% through 2030, driven by the premiumization of packaged snacks, cakes, and biscuits. These products increasingly incorporate citric and malic acids to enhance shelf life and provide tangy flavor profiles that differentiate products on crowded retail shelves. Barry Callebaut’s October 2024 announcement of a USD 30 million chocolate manufacturing project in Egypt underscores multinational confidence in the growth of premium confectionery. Local players such as Bisco Misr and Domty are also leveraging acidulant systems in coated cakes, filled biscuits, and sour candies to balance sweetness and acidity, tying the premiumization of impulse snacks to rising acidulant usage per unit of output.

Beyond beverages and bakery-confectionery, acidulants play a critical role in dairy, frozen desserts, meat, seafood, and specialized nutrition applications. Dairy and frozen desserts rely on citric acid and trisodium citrate for pH buffering and emulsification, with operators like Juhayna embedding acidulants into yogurt fermentation and cheese coagulation processes. Meat and seafood processors use lactic acid sprays and lactate blends to extend shelf life and reduce microbial loads, aligning with regulatory changes in July 2024. Additionally, infant and clinical nutrition applications, though smaller in volume, command premium pricing and use mineral salts such as calcium lactate gluconate and magnesium citrate for fortification and bioavailability, further diversifying the demand base for acidulants.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Industrial clusters in Greater Cairo and Alexandria serve as key hubs for acidulant distribution and technical support, given their proximity to beverage, dairy, bakery, and confectionery plants. These locations benefit from access to ports such as Alexandria and Damietta, which facilitate the import of citric, lactic, and phosphoric acids and the export of processed foods. This logistics network strengthens Egypt’s role as a processing and re-export platform. Additionally, government-backed projects in the New Delta and “Future of Egypt” agricultural zones are expanding processing capacity westward, integrating citrus, tomato, and livestock production areas with acidulant-consuming plants. This spatial alignment reduces transportation costs and enhances the potential for local fermentation or blending investments, supporting the rollout of acidulant-intensive products like ready-to-drink juices and flavored yogurts across modern and traditional retail channels.

Regionally, Egypt’s position as a processed food export hub drives acidulant demand, with 54% of processed food exports, valued at approximately USD 3.28 billion in 2024 as per Food Export Council (FEC), destined for Arab markets, including Saudi Arabia, Libya, and Gulf countries. High-demand categories such as soft drink concentrates, juices, sauces, and confectionery rely heavily on citric and phosphoric acids, making regional export contracts significant drivers of acidulant consumption. Soft drink exports alone grew by 27% in 2024, with African markets like South Sudan, Uganda, and Burundi emerging as key buyers. Centralized production facilities in Egypt standardize acidity and pH levels to meet diverse climatic and regulatory requirements, enabling brands like Coca-Cola HBC and Pepsi-linked bottlers to serve multiple neighboring markets efficiently.

Globally, Egypt’s status as a leading citrus producer and exporter connects its agricultural regions to international markets. Citrus-growing zones supply both fresh exports and juice processors, which increasingly generate by-products suitable for citric acid production, reducing reliance on imports. Meanwhile, global processed food exports, valued at USD 6.1 billion in 2024, necessitate compliance with stringent international standards. Multinational firms like Barry Callebaut leverage Egypt’s strategic location and port connectivity to distribute acidulant-intensive products efficiently, reinforcing the country’s competitive position in the global acidulants ecosystem.

Competitive Landscape

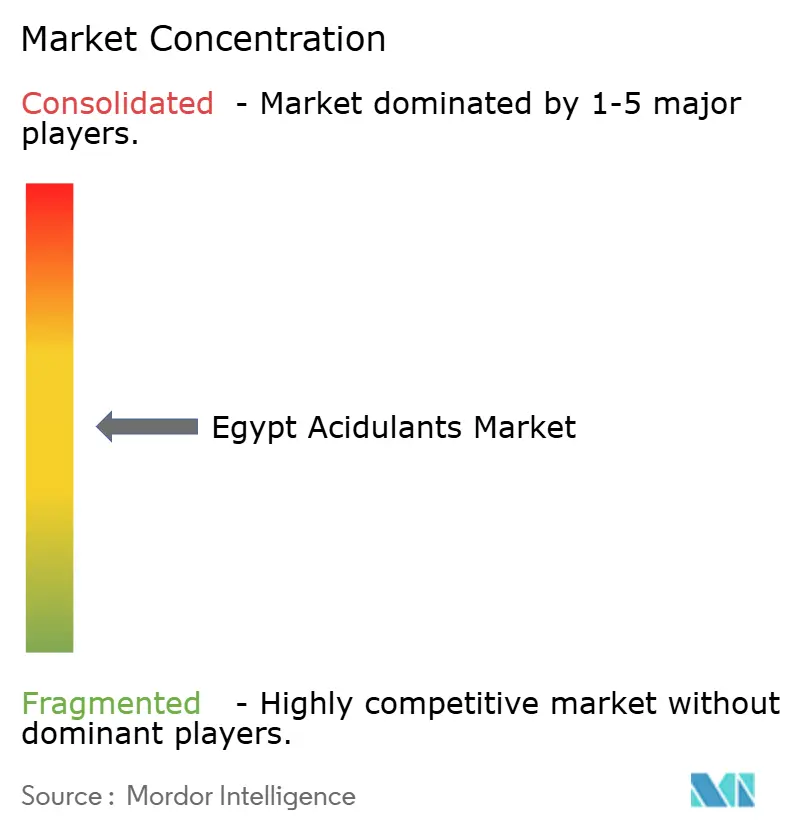

The market for acidulants in Egypt is characterized by moderate fragmentation, with multinational ingredient suppliers and local distributors competing on technical support, pricing, and supply reliability. This competitive environment provides downstream food manufacturers with diverse sourcing options. Multinational companies such as Cargill, ADM, and Tate & Lyle dominate the market by leveraging their global scale to supply citric, lactic, and phosphoric acids with consistent quality certifications. These certifications appeal to export-oriented processors, enabling them to meet international standards. For example, Cargill supports beverage manufacturers like Juhayna with customized citric acid blends for juice stabilization, while ADM supplies malic and fumaric acids to confectionery producers such as Gandour, ensuring precise sourness in gummies that align with MENA export requirements. Corbion, Jungbunzlauer, and Tate & Lyle also play pivotal roles in addressing specific needs in meat preservation, dairy fermentation, and bakery formulations, respectively.

Egyptian distributors, including Brenntag, BASF and NAMAA Egypt, act as intermediaries between global suppliers and domestic processors. They cater to mid-tier processors by offering competitive pricing and faster delivery times. Brenntag supplies phosphoric acid to Coca-Cola HBC bottlers, mitigating currency depreciation impacts through bulk hedging strategies. BASF supports Kraft Heinz's Cairo facility with acetic acid for ketchup emulsions, ensuring pH stability for their expanding mayonnaise line. NAMAA Egypt focus on localized blending and cost-effective solutions for juice and dairy operations, respectively, enabling processors to reduce import dependency and meet local standards. These distributors also handle secondary volumes and niche deliveries, providing flexibility to SMEs that cannot commit to large contracts.

Local producers, such as Egyptian Chemical Industries (KIMA) and Misr Phosphate Company, focus on supplying phosphoric and basic acids to cost-sensitive segments. KIMA provides acetic acid for pickle processors, ensuring pH control for condiments competing on price, while Misr Phosphate utilizes domestic resources to produce phosphoric acid for economy soft drinks. By concentrating on foundational acids, these producers support smaller processors and create a base layer in the market, allowing multinationals to upsell value-added blends and distributors to address specific requirements. This dynamic sustains moderate fragmentation and fosters innovation across the supply chain.

Egypt Acidulants Industry Leaders

-

Archer Daniels Midland Company

-

Cargill, Incorporated

-

Brenntag AG

-

Tate & Lyle PLC

-

NAMAA Egypt

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: The National Company for Maize Products (NCMP), a subsidiary of Cairo 3A Group, was awarded the “Best Localization Project” at the 2025 CIB | MEED Egypt Business Excellence Awards. The award recognized its “Citric Acid Plant,” the first of its kind in Egypt and the Middle East. With an annual production capacity of 33,000 tons and total investments of EGP 1.9 billion, the plant adhered to international manufacturing standards, supported local industries, and strengthened the presence of Egyptian products in regional and global markets.

- November 2025: Cairo 3A, the owner of NCMP, announced a significant investment program of approximately USD 150 million over several years. This program included the establishment of what was described as Egypt's first large-scale citric acid plant, along with the expansion of related product lines such as citric acid, sorbitol, mannitol, and starch derivatives. This initiative represented a notable step in the localization and expansion of acidulant production in Egypt and the broader region.

- June 2025: Several Egyptian companies finalized contracts with a Chinese consortium comprising China State Engineering Corp and East China Engineering Science and Technology Company to construct a phosphoric acid plant in Egypt's New Valley region. The plant, with an investment value of USD 658 million, was designed to produce 250,000 tons of concentrated phosphoric acid during the first phase of the project.

Egypt Acidulants Market Report Scope

The Egypt Acidulants Market Report is Segmented by Ingredients Type (Citric Acid, Phosphoric Acid, Lactic Acid, Acetic Acid, Other Acids), Application (Beverages, Dairy and Frozen Desserts, Bakery and Confectionery, Meat and Seafood, Others). The Market Forecasts are Provided in Terms of Value (USD Million).

By Ingredients Type

| Citric Acid |

| Phosphoric Acid |

| Lactic Acid |

| Acetic Acid |

| Other Acids (Tartaric, Fumaric, malic, etc.) |

By Application

| Beverages |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Meat and Seafood |

| Others (Sauces, Dressings and Condiments, Infant and Clinical Nutrition, etc) |

| By Ingredients Type | Citric Acid |

| Phosphoric Acid | |

| Lactic Acid | |

| Acetic Acid | |

| Other Acids (Tartaric, Fumaric, malic, etc.) | |

| By Application | Beverages |

| Dairy and Frozen Desserts | |

| Bakery and Confectionery | |

| Meat and Seafood | |

| Others (Sauces, Dressings and Condiments, Infant and Clinical Nutrition, etc) |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Egypt acidulants market?

The market is valued at USD 53.45 million in 2025.

Which acidulant holds the highest share in Egypt?

Citric acid leads with 45.16% revenue share in 2024.

Which segment is growing fastest for acidulants in Egypt?

Lactic acid is expanding at an 8.57% CAGR to 2030 due to meat and dairy shelf-life mandates.

What drives bakery and confectionery demand for acidulants?

The bakery and confectionery market is anticipated to grow at a CAGR of 8.24% through 2030, supported by increasing consumer demand for tangy flavors and enhanced shelf-life, driving the adoption of citric and malic acids.

Page last updated on: