Market Trends of East Africa Oil and Gas Upstream Industry

This section covers the major market trends shaping the East Africa Oil & Gas Upstream Market according to our research experts:

Onshore Sector to Dominate the Market

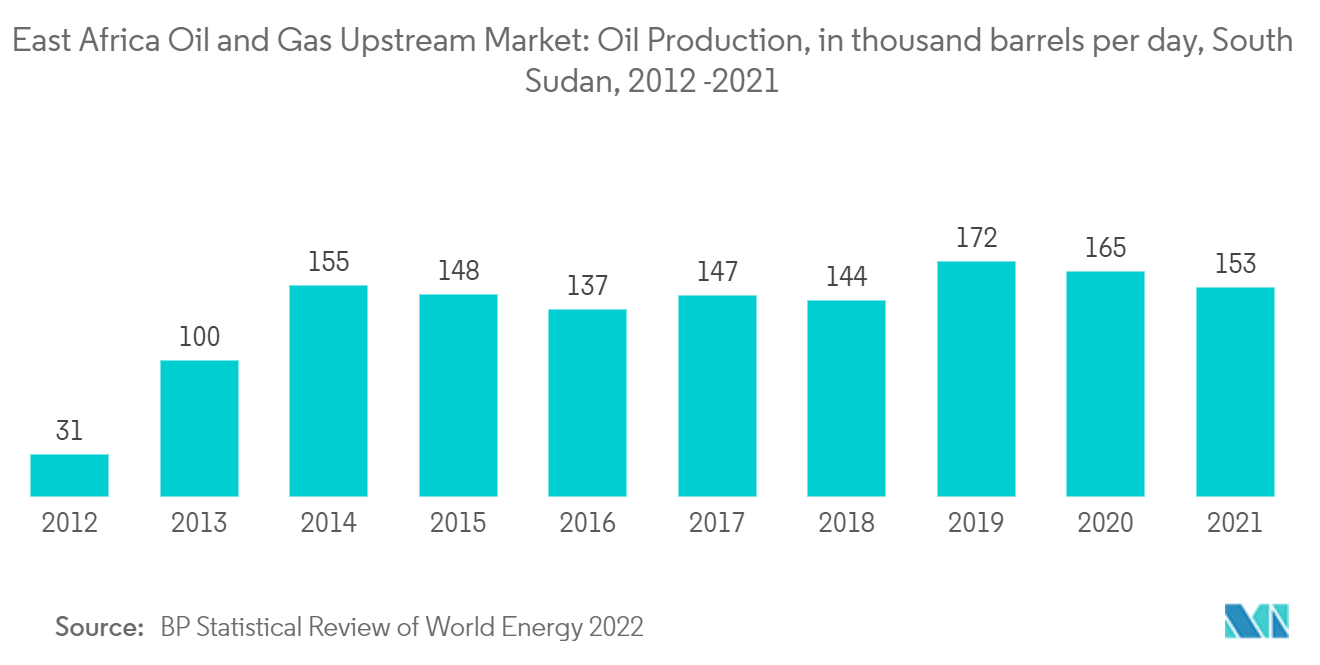

- As of 2021, onshore oil and gas fields accounted for a significant share of the total oil and gas production in East Africa. For example, South Sudan's oil production, which solely comes from onshore oilfields, increased from 31 thousand barrels per day in 2010 to 153 thousand barrels per day in 2021.

- The increasing demand for petroleum products and the East African countries' efforts to boost oil and gas production through existing and new discoveries are expected to drive the upstream activities in the onshore segment during the forecast period.

- In July 2022, the government of the Democratic Republic of Congo (DRC ) announced its plans to put on offer 27 oil blocks and three gas blocks in its upcoming licensing round. Of the 27 oil blocks, three are in the coastal basin of the Kongo Central province, 11 are near Lake Tanganyika, nine are in the Cuvette Centrale, and four are near Lake Albert. The three gas blocks are located on Lake Kivu.

- In October 2022, a consortium of India's national oil company's subsidiary ONGC Videsh Ltd (OVL) and Indian Oil Corp. Ltd (IOCL) announced that they are in talks with Tullow Oil PLC to jointly acquire around 50% participating interest in the latter's USD 3.4 billion oil project in Kenya.

- Therefore, due to such factors, the onshore sector is expected to dominate the market during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

Kenya to Witness Significant Growth

- In the East African region, Kenya is likely to be one of the significant countries witnessing a significant ramp-up of crude oil production during the forecast period, up from approximately 2% of the country's current oil consumption.

- The production growth is expected due to the investment decision made by companies like ONGC Videsh, IOCL, and TotalEnergies.

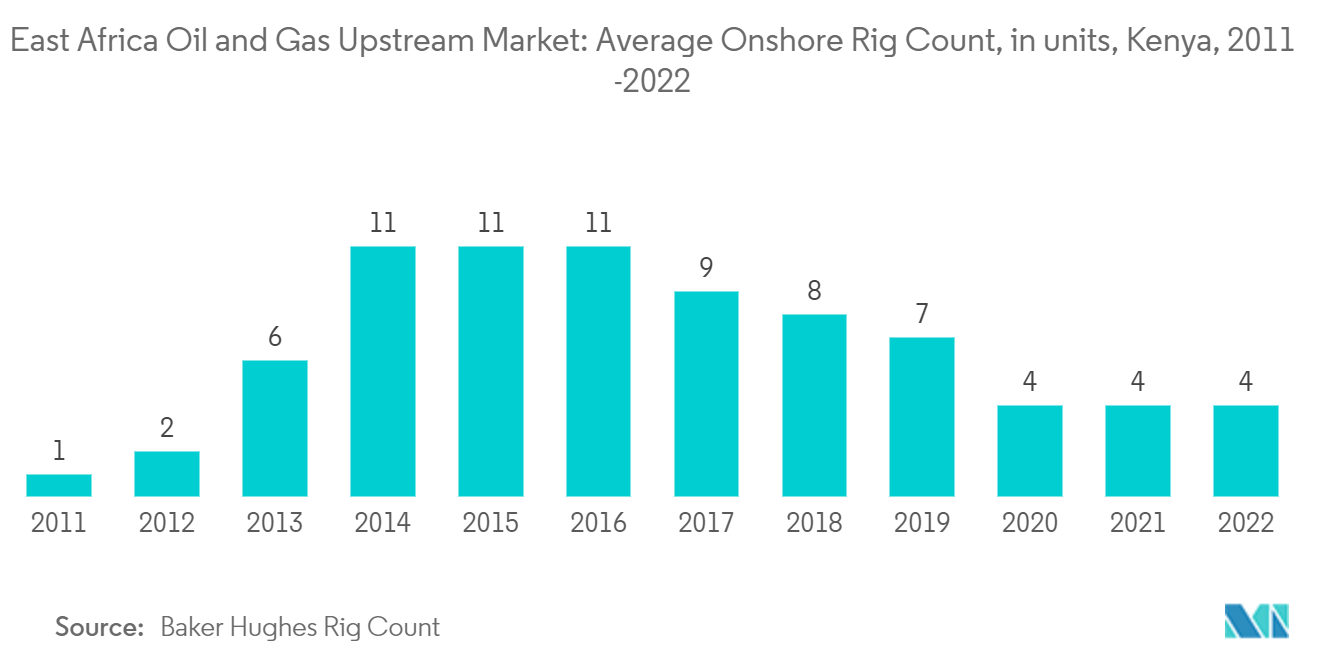

- The country witnessed a significant rise in exploration and production activities from a number of international oil companies, starting in 2014 when the rig count in the country increased to 11 from a mere 1 in 2011. However, in 2021, the country only had four operational rigs.

- In February 2022, TotalEnergies and the Lake Albert Development Project partners announced the final investment decision and the launch of the project in Uganda and Tanzania, representing a total investment of approximately USD 10 billion.

- The crude oil prices crash of 2014 and 2020 severely impacted the market. However, it has recovered since then, which can be observed through the increasing number of final investment decisions in the country's oil and gas sector.

- The increased investment in upstream oil and gas projects is likely to drive the growth of Kenya's oil and gas upstream market during the forecast period.

Get Analysis on Important Geographic Markets

Download PDF